Automotive Electric HVAC Compressor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

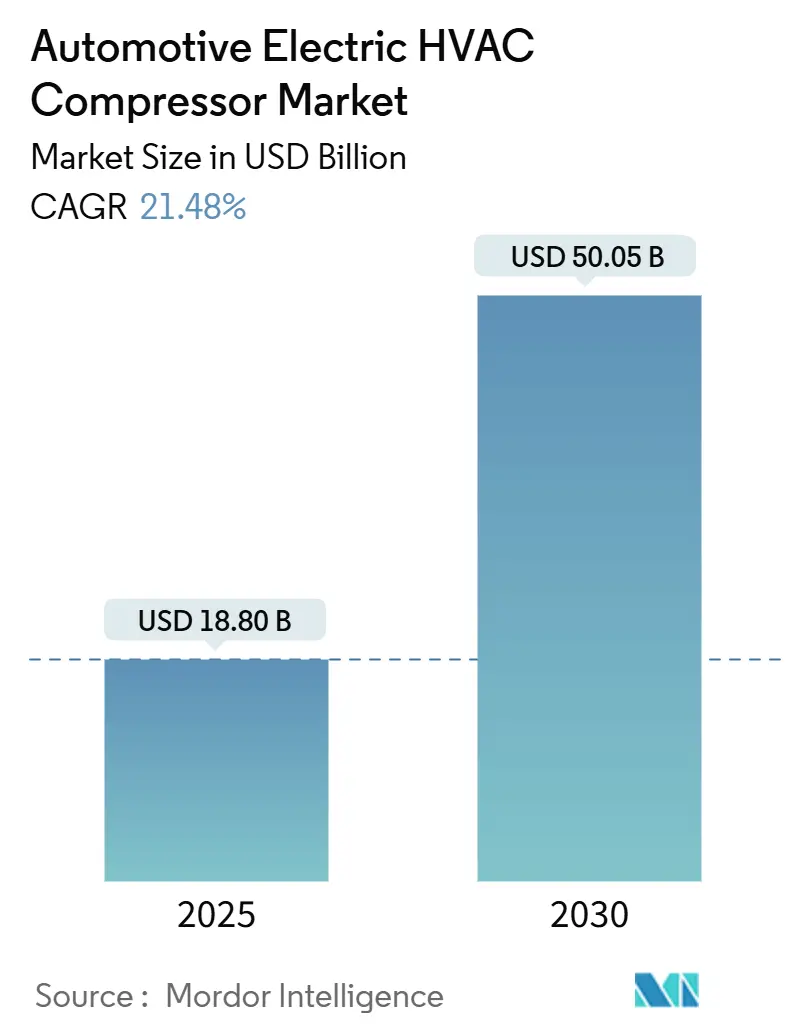

| Market Size (2025) | USD 18.80 Billion |

| Market Size (2030) | USD 50.05 Billion |

| Growth Rate (2025 - 2030) | 21.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Electric HVAC Compressor Market Analysis by Mordor Intelligence

The automotive electric HVAC compressor market size reached USD 18.8 billion in 2025 and is forecast to hit USD 50.05 billion by 2030, expanding at a 21.48% CAGR. Growth stems from the shift away from belt-driven mechanical units toward electrically powered compressors that decouple HVAC performance from engine speed, letting automakers refine cabin and battery temperatures with minimal energy loss. Faster adoption of integrated thermal-management systems, surging electric-vehicle (EV) production, and stricter refrigerant rules widen the addressable opportunity for suppliers. Scroll e-compressors, 48 V architectures, and CO₂ refrigerants stand out as accelerants because they improve efficiency while easing regulatory risk. Asia-Pacific keeps its lead on the back of China’s aggressive EV rollout, domestic supply-chain scale, and supportive industrial policy. Competitive dynamics remain fluid: tier-1 incumbents defend share through advanced heat-pump platforms even as cost-focused Chinese makers enter global programs. Capital-intensive consolidation signals an industry racing to secure volume, technology, and geographic reach before EV demand peaks.

Key Report Takeaways

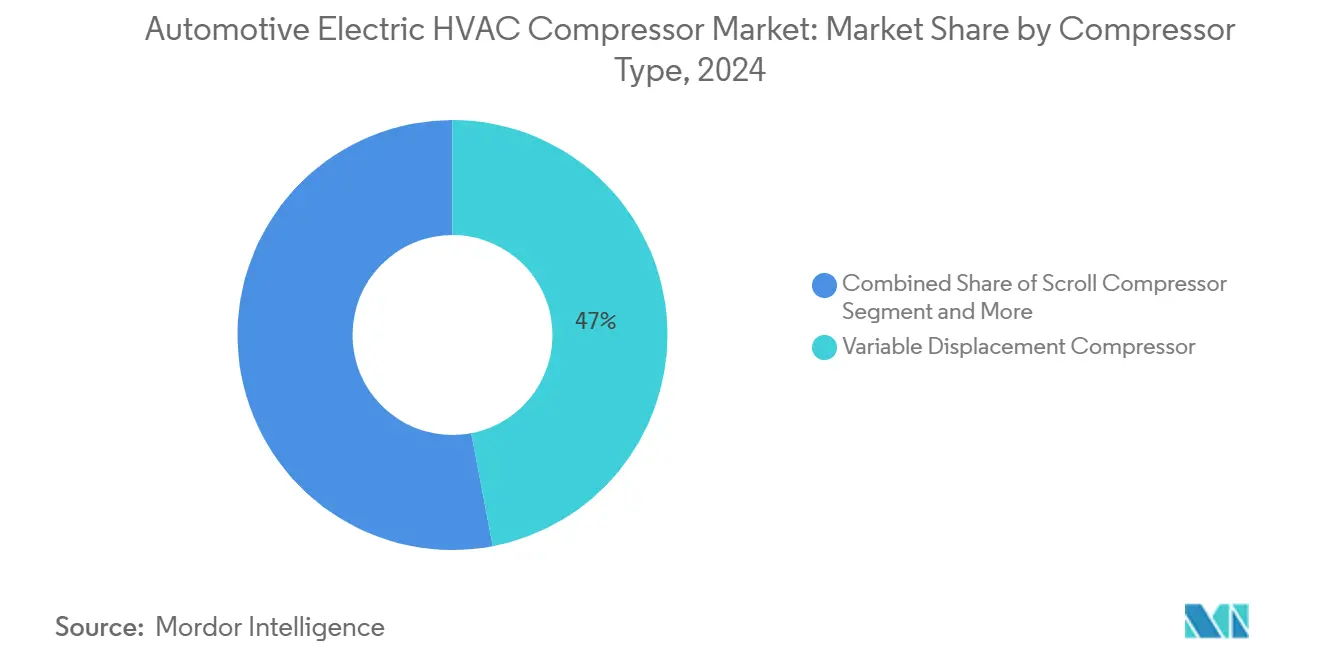

- By compressor type, variable displacement captured 47.02% of the automotive electric HVAC compressor market share in 2024, while scroll technology is projected to post the fastest 14.12% CAGR to 2030.

- By voltage, 12 V systems held 52.48% of the automotive electric HVAC compressor market size in 2024; 48 V platforms are anticipated to advance at an 18.52% CAGR through 2030.

- By refrigerant, HFO-1234yf dominated with a 68.03% share of the automotive electric HVAC compressor market size in 2024, whereas CO₂ systems are set to expand at a 27.01% CAGR by 2030.

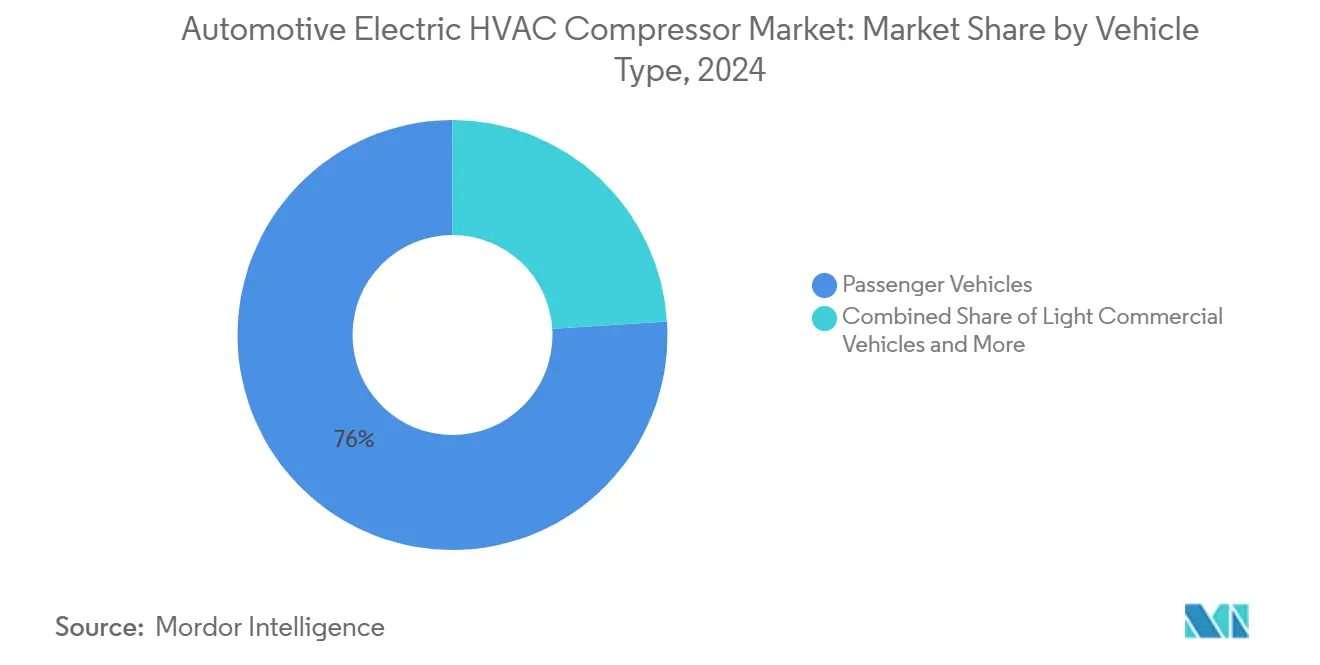

- By vehicle type, passenger cars accounted for 76.05% of 2024 revenue; medium and heavy commercial vehicles are expected to grow at a 9.81% CAGR to 2030.

- By sales channel, OEM programs represented 79.07% of 2024 demand and are on track for a 10.32% CAGR through 2030.

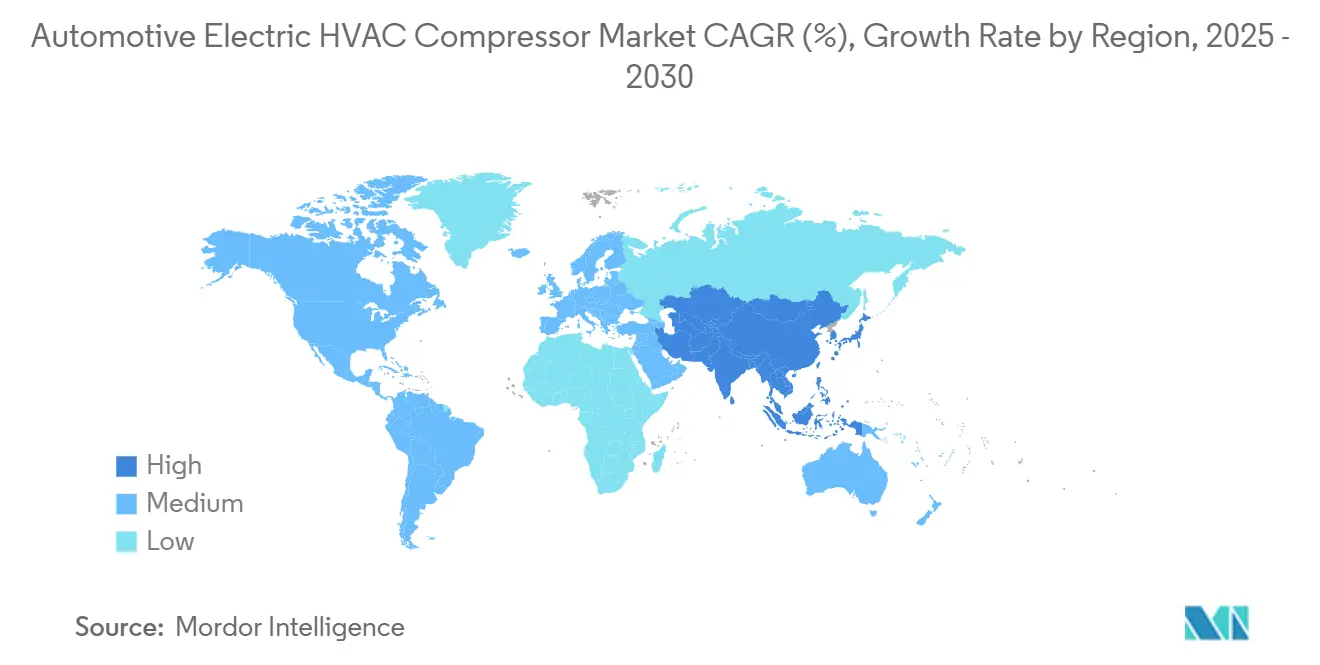

- By region, Asia-Pacific represented 54.06% of 2024 demand and is on track for 12.59% CAGR through 2030.

Global Automotive Electric HVAC Compressor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Adoption Driving Demand for High-Voltage E-Compressors | +6.2% | Global, with Asia-Pacific and Europe leading | Medium term (2-4 years) |

| Regulatory Migration to Low-GWP Refrigerants (R-1234yf, CO₂) | +4.8% | Europe and North America core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising Comfort and Automatic Climate-Control Penetration in Emerging Markets | +3.1% | Asia-Pacific core, spill-over to MEA and South America | Medium term (2-4 years) |

| Shift to 48V Mild-Hybrid Architectures Enabling Belt-Less E-Compressors | +2.9% | Global, with early adoption in Europe and North America | Short term (≤ 2 years) |

| Battery Thermal-Management Integration Upsizing Compressor Capacity | +2.7% | Global EV markets | Medium term (2-4 years) |

| Localization of E-Scroll Compressor Supply Chain in China Lowers Costs | +1.8% | Asia-Pacific core, global cost benefits | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV adoption driving demand for high-voltage e-compressors

Rapid EV proliferation eliminates mechanical belt drives and demands compressors that operate during charge, idle, and pre-conditioning cycles. High-voltage units support simultaneous cabin cooling and battery conditioning, as shown by Hanon Systems’ fourth-generation heat-pump architecture that debuted in 2024 and combines waste-heat recovery with ambient sources. The modular design trims part count and improves thermal efficiency, signaling a move toward consolidated systems that raise revenue per vehicle in the automotive electric HVAC compressor market.

Regulatory migration to low-GWP refrigerants (R-1234yf, CO₂)

Europe’s 2024 F-Gas revision and the United States’ 2025 Technology Transitions Program phase out high-GWP gases, tilting OEM preference toward R-1234yf today and CO₂ long term. Hanon Systems surpassed 500,000 R744 e-compressor units for Volkswagen’s MEB platform, proving commercial readiness of natural refrigerants. PFAS scrutiny could accelerate migration, favoring suppliers already fluent in CO₂ system engineering.

Rising comfort and automatic climate-control penetration in emerging markets

Middle-income buyers in China, India, Southeast Asia, and Latin America now view automatic HVAC as a baseline feature. Electric compressors allow stable cooling when engines shut off during start-stop events, meeting comfort expectations without fuel penalties. Variable-speed control fine-tunes energy use, critical for hybrids where energy budget is tight. Chinese vendor Guchen’s 540 V, 8.5 kW bus unit illustrates how local suppliers scale capability for harsh climates.

Shift to 48 V mild-hybrid architectures enabling belt-less e-compressors

Automakers embrace 48 V systems to comply with near-term CO₂ targets at lower cost than full battery electric. The voltage supplies enough power for HVAC without high-voltage safety protocols, paving a mandatory path to electric compressors. Belt-less configuration removes parasitic drag, sharpening fuel economy in congested city driving. European OEMs lead installations as they face 2025 fleet-average emission ceilings, with North American pickups next in line.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Unit Cost of Electric Scroll and Inverter Compressors | -3.4% | Global, with cost sensitivity highest in emerging markets | Medium term (2-4 years) |

| Raw-Material and Semiconductor Price Volatility | -2.1% | Global supply chains | Short term (≤ 2 years) |

| EU-Level PFAS/TFA Scrutiny of R-1234yf Creating Refrigerant Uncertainty | -1.6% | Europe | Medium term (2-4 years) |

| Shortage of Technicians Certified for HV-HVAC Service/Repair | -1.2% | Global, with Asia-Pacific focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High unit cost of electric scroll and inverter compressors

Electric units sell at USD 200–600 apiece versus USD 100–300 for mechanical equivalents, while professional installation adds USD 500–1,200 because high-voltage safety protocols apply. Scroll geometry needs tight tolerances, and inverter modules drive up semiconductor content, making cost a barrier in entry-level vehicles. Fleet buyers scrutinize total cost of ownership and delay adoption until payback is proven, dampening short-term volume in the automotive electric HVAC compressor market.

Raw-material and semiconductor price volatility

Copper, electrical steel, and power chips trade in volatile global markets. In 2024–2025, chip lead times stretched beyond automotive planning windows, forcing compressor makers to redesign around available components or accept lower margins. Copper spikes raise motor and harness expense, while electrical-steel shortages constrain high-efficiency stator production. Even with localization strategies, most suppliers lack the bargaining power to stabilize commodity cost swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compressor Type: Scroll Technology Gains Traction

Variable displacement held 47.02% of 2024 revenue, reflecting entrenched use in legacy platforms. Scroll e-compressors, however, are forecast to log a 14.12% CAGR to 2030 as OEMs favor their quiet, vibration-free operation. This pace lifts the automotive electric HVAC compressor market size for scroll designs from a single-digit base toward mainstream volumes. Fixed-displacement units linger in cost-sensitive cars but lose share each year.

Scroll designs excel across wide speed ranges, supporting heat-pump modes that harvest ambient or waste heat for cabin warmth. Tompress’s second-generation scroll proves the architecture’s adaptability. As integrated thermal-management becomes standard, scroll efficiency enables longer EV range, further accelerating share capture.

By Voltage: 48 V Architecture Accelerates Adoption

The 12 V category still tops shipments with 52.48% share in 2024, yet 48 V platforms will grow 18.52% annually. That expansion should lift 48 V’s portion of the automotive electric HVAC compressor market size beyond one-third by 2030. Mild-hybrid rollouts in Europe and China push demand as these cars need engine-off cooling without the cost of 400 V packs.

48 V bridges legacy and full-EV worlds. A DC-DC step-down keeps compatibility with existing 12 V loads, easing engineering change. Suppliers fine-tune inverter drives for the 48 V envelope, balancing safety, power, and price. Fleet adopters in urban logistics favor the architecture because idling regulations demand engine-off HVAC.

By Refrigerant Type: Natural Refrigerants Challenge Synthetics

HFO-1234yf controlled 68.03% of units in 2024 thanks to earlier rollouts, but CO₂ solutions are set to record 27.01% CAGR as regulations and PFAS concerns bite. That swing will noticeably alter the automotive electric HVAC compressor market share mix by 2030. HFC-134a shrinks to residual demand in unregulated territories.

Hanon Systems’ half-million CO₂ units for Volkswagen validate scale. CO₂ performs especially well in cold climates where HFOs lose heating efficiency, giving northern European brands a clear incentive to switch. Compressor makers respond with reinforced housings and thicker seals to withstand higher operating pressures.

By Vehicle Type: Commercial Segments Drive Innovation

Passenger cars contributed 76.05% of the 2024 value, but medium and heavy trucks will clock a 9.81% CAGR. Range-extended duty cycles and driver-comfort mandates make reliable cooling essential during mandatory rest or loading stops. That need elevates per-vehicle compressor power and durability specifications, lifting the average selling price for vendors active in commercial realms.

Electric buses and urban delivery vans spotlight the trend. Guchen’s 8.5 kW, 540 V compressor meets harsh, long-hour usage, illustrating how commercial specs outstrip passenger car demands. As city-cleansing policies tighten, trucks and buses electrify, sustaining above-trend growth for heavy-duty compressors.

By Sales Channel: OEM Integration Dominates

OEMs absorbed 79.07% of 2024 unit shipments and should pace ahead at 10.32% CAGR through 2030. Complex controls, warranty integration, and safety certification make automakers reluctant to source high-voltage HVAC modules from aftermarket installers. This dominance anchors the automotive electric HVAC compressor market, while replacement volumes remain niche. Valeo supplies blowers to one-third of European cars, demonstrating why tier-1 footprints matter. High-voltage service requires specialist tooling, limiting independent garages and reinforcing OEM service lock-in.

Geography Analysis

Asia-Pacific had 54.06% of 2024 revenue, projected to compound at 12.59% until 2030. China’s NEV quotas, localized component sourcing, and vast manufacturing base underpin this leadership. Domestic compressor champions leverage proximity to BYD and SAIC programs to gain volume quicker than Western peers.

Europe ranks second because stringent CO₂ and F-Gas laws steer every new platform to electric compressors and natural refrigerants. Volkswagen, Stellantis, and Mercedes are already rolling out CO₂ heat pumps beyond premium lines, accelerating regional conversion. Government incentives for heat-pump-equipped EVs further spur demand. North America trails slightly but ramps fast as the United States’ 2025 refrigerant rule and Inflation Reduction Act credits propel EV output. New e-compressor plants, such as Hanon Systems’ Ontario site capable of 900,000 units yearly, signal supply readiness.

South America, the Middle East, and Africa offer long-run upside. Rising car ownership, hot climates, and eventual emissions standards will generate pull; however, lower purchasing power keeps mechanical systems prevalent in the near term. As localized assembly expands and used EV imports climb, electric compressors will penetrate, starting with premium fleets and buses.

Competitive Landscape

Industry concentration is moderate: the five largest suppliers account for most of the market share, assigning a market concentration score 6. Denso, Hanon Systems, and Valeo maintain scale through multiregional plants and deep OEM ties. Chinese participants, such as Shanghai Highly Group and BYD, drive prices lower, trading margin for shares.

Strategic differentiation focuses on integrated heat pump systems, scroll IP, and natural refrigerant know-how. Hanon’s fourth-generation module, combining refrigerant and coolant control in a single package, illustrates the push to system-level value. Meanwhile, Denso’s 2025 EcoPass certification for digital product passports prepares the firm for EU traceability mandates on battery components.

Consolidation emerged in 2024 when Hankook Tire agreed to buy 33.16% of Hanon Systems for KRW 1.733 trillion (USD 1.29 billion), broadening its EV parts portfolio. Such deals bundle thermal-management IP with adjacent systems—tires, batteries, brake-by-wire—creating broader solution sets for automakers scaling electric models.

Automotive Electric HVAC Compressor Industry Leaders

Denso Corporation

Hanon Systems

Valeo SA

Sanden Holdings Corporation

Mahle GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: DENSO acquired EcoPass certification from Catena-X, becoming the first Japan-headquartered company to achieve this verification for Digital Product Passport applications, positioning the supplier for European Battery Regulation compliance requirements effective February 2027.

- October 2024: Hanon Systems announced construction of its first North American electric compressor plant in Woodbridge, Ontario, Canada, with 26,400 square meters facility capacity to produce 900,000 electric compressors annually starting first half 2025.

Global Automotive Electric HVAC Compressor Market Report Scope

| Fixed Displacement Compressor |

| Variable Displacement Compressor |

| Scroll Compressor |

| 12 V |

| 24 V |

| 48 V |

| HFC-134a |

| HFO-1234yf |

| CO₂ (R-744) |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Compressor Type | Fixed Displacement Compressor | |

| Variable Displacement Compressor | ||

| Scroll Compressor | ||

| By Voltage | 12 V | |

| 24 V | ||

| 48 V | ||

| By Refrigerant Type | HFC-134a | |

| HFO-1234yf | ||

| CO₂ (R-744) | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which compressor technology is expanding fastest?

Scroll e-compressors are on track for a 14.12% CAGR thanks to high efficiency and compact design.

Why are 48 V systems important for future compressor demand?

They enable belt-less HVAC on mild-hybrid cars, delivering engine-off comfort without the costs of 400 V architectures.

How will refrigerant rules reshape product choices?

European and U.S. bans on high-GWP gases push OEMs toward R-1234yf now and CO₂ solutions over the longer term.

Which region leads consumption today?

Asia-Pacific holds 54.06% share, powered by China’s aggressive EV rollout and localized supply chains.

What impact does battery thermal management have on compressor sizing?

Integrated cabin-and-battery cooling raises capacity requirements, lifting revenue per vehicle for suppliers.

Page last updated on: