Automotive Turbocharger Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

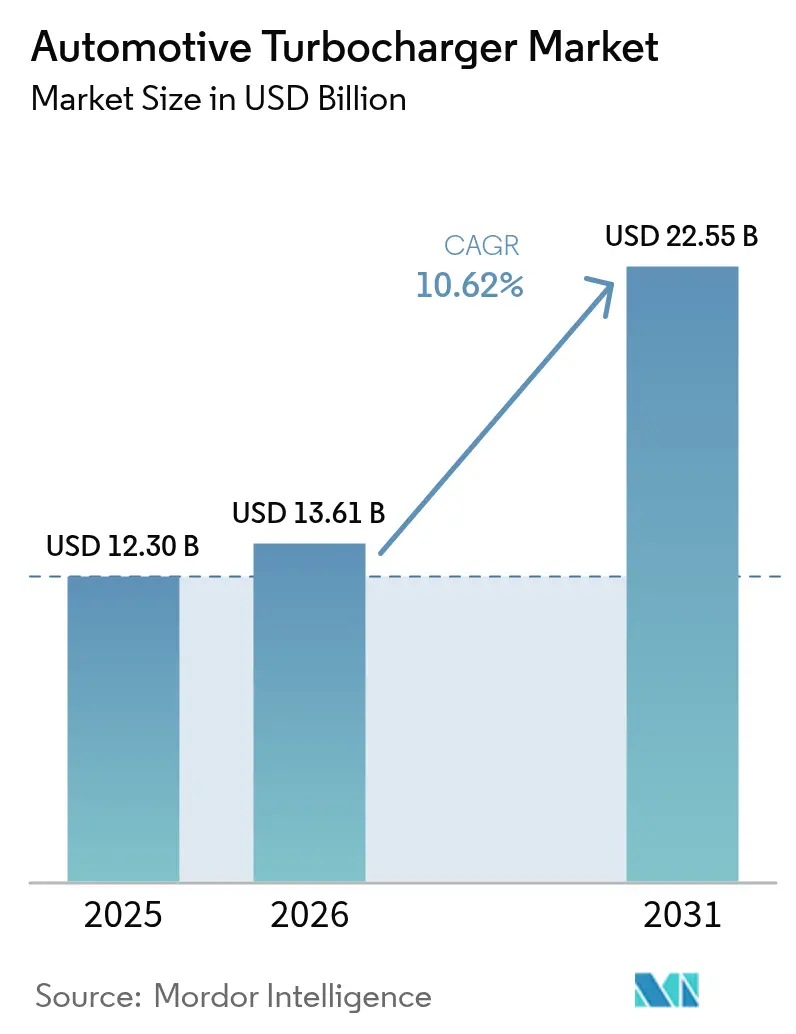

| Market Size (2026) | USD 13.61 Billion |

| Market Size (2031) | USD 22.55 Billion |

| Growth Rate (2026 - 2031) | 10.62% CAGR |

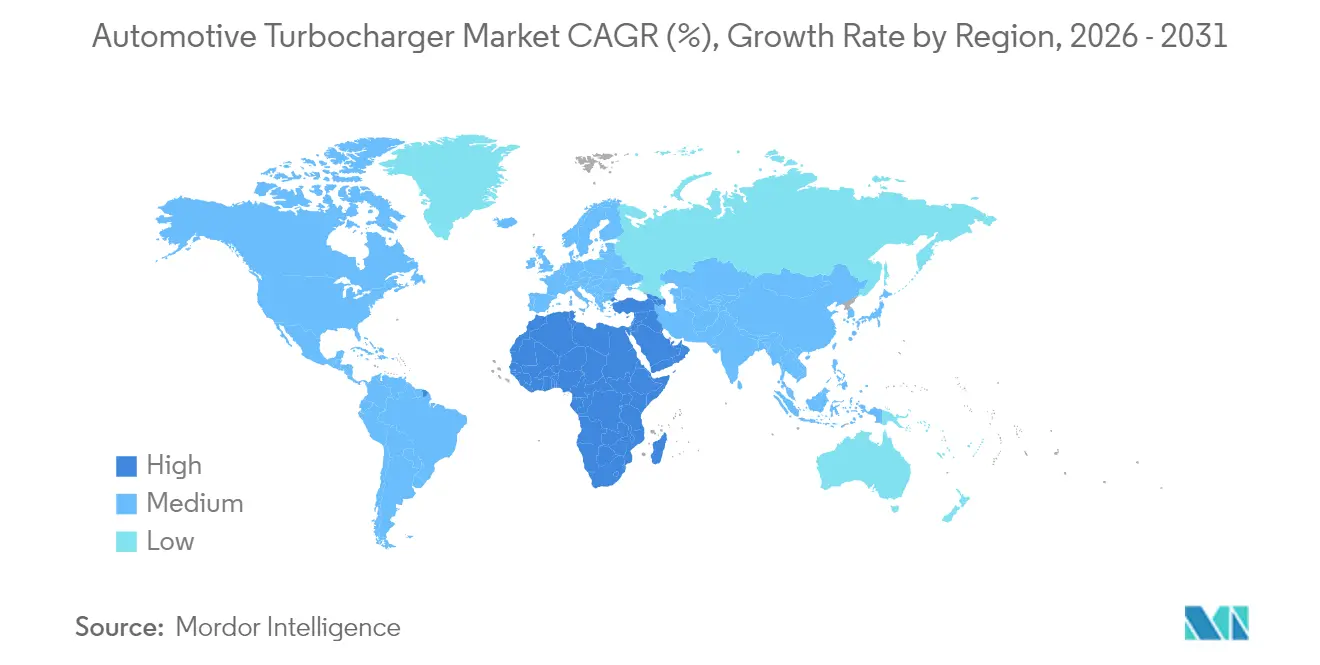

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

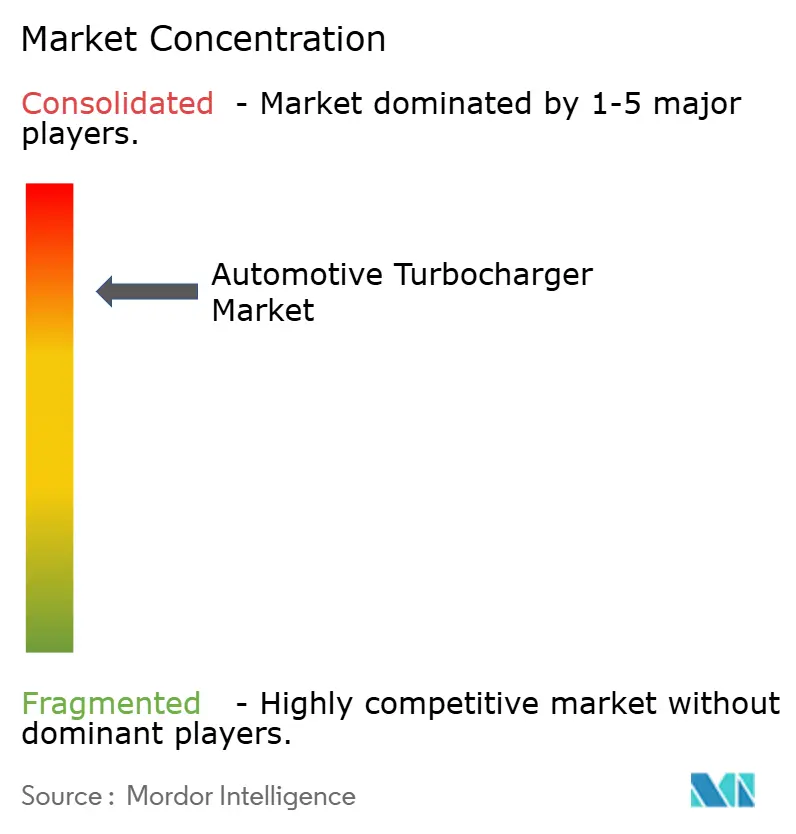

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Turbocharger Market Analysis by Mordor Intelligence

The automotive turbocharger market size was valued at USD 12.30 billion in 2025 and estimated to grow from USD 13.61 billion in 2026 to reach USD 22.55 billion by 2031, at a CAGR of 10.62% during the forecast period (2026-2031). Persistent emissions mandates, engine-downsizing strategies, and the shift to hybrid powertrains drive the turbocharger market toward higher-efficiency, electric-assist, and hydrogen-ready solutions. Technology spending is moving quickly from simple wastegate architectures to variable geometry and 48 V e-boost systems that can meet Euro 7 and similar regulations.[1]"EU Euro 7 Emissions Regulation Published", InterRegs, www.interregs.com. Automakers view electric turbochargers as the most direct path to near-instant torque delivery without compromising fleet-average fuel economy. At the same time, component makers prioritize designs that suit fuel-cell air management. Competitive dynamics remain intense because the top five suppliers already supply most global volume. Yet, each is racing to secure design wins in hydrogen ICE, fuel-cell, and 400 V hybrid platforms.

Key Report Takeaways

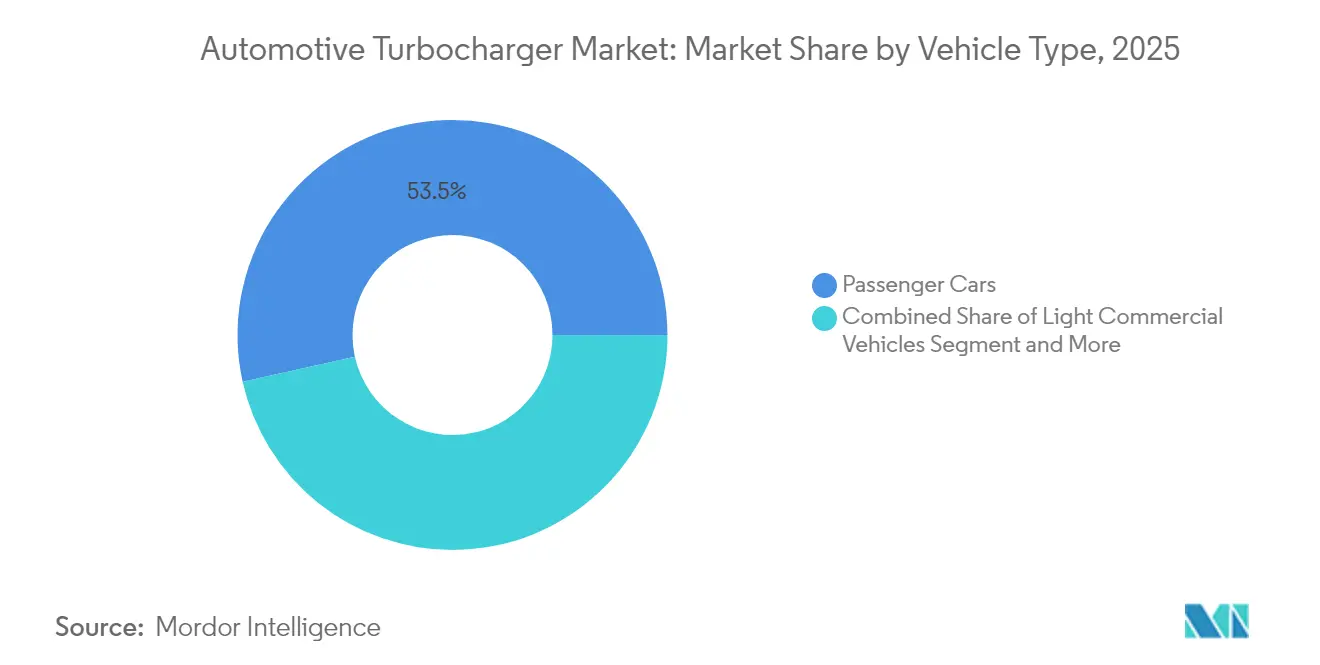

- By vehicle type, passenger cars led the turbocharger market with 53.48% of the share in 2025, while off-highway equipment is projected to expand at a 12.35% CAGR to 2031.

- By fuel type, diesel engines held 60.02% of the turbocharger market size in 2025; hydrogen ICE applications post the fastest growth at 25.10% through 2031.

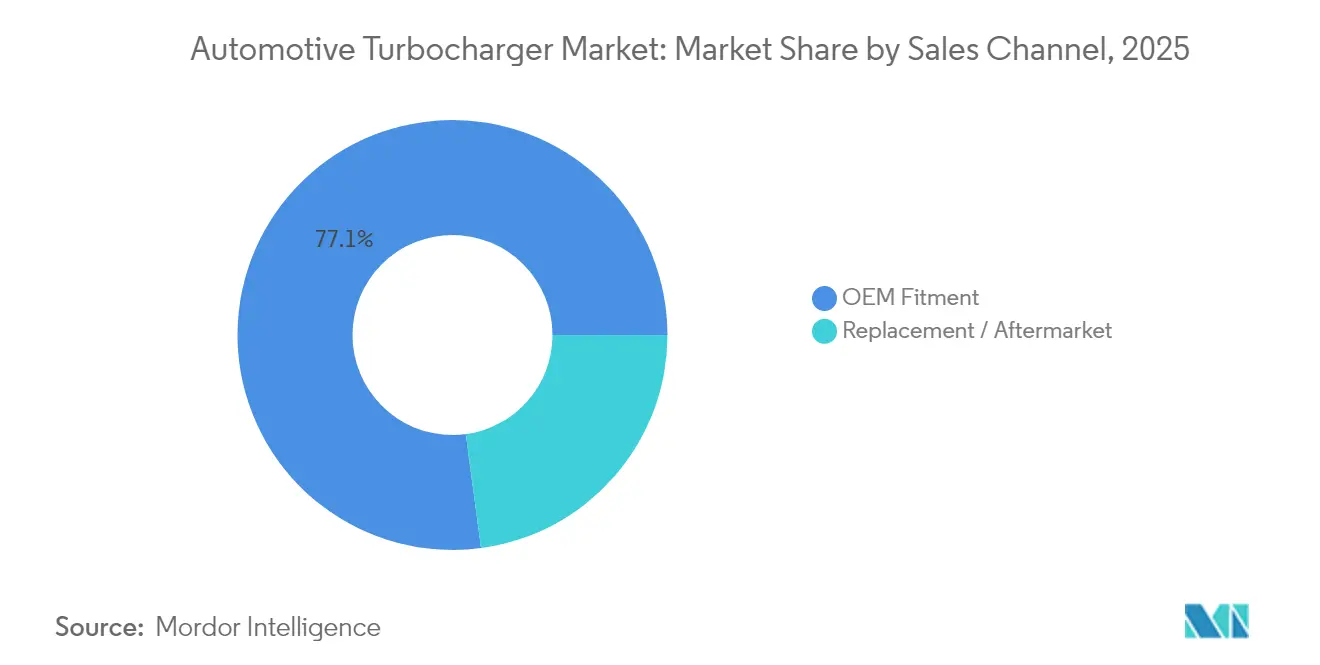

- By sales channel, OEM fitment commanded 77.12% share of the turbocharger market size in 2025, whereas the replacement aftermarket is advancing at a 9.12% CAGR.

- By turbo technology, wastegate units accounted for 43.74% of the market share in 2025, and electric turbochargers show the highest projected CAGR at 18.62%.

- By geography, Asia-Pacific dominates the global turbocharger market with a 48.41% share in 2025, while the Middle East and Africa region is forecast to grow the fastest at 12.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Turbocharger Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter CO₂ and NOx Legislation Accelerating Turbo-gasoline Adoption | +2.8% | Global, with EU and China leading implementation | Medium term (2-4 years) |

| Engine Downsizing for Fleet-average Fuel-economy Compliance | +2.1% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising Commercial-vehicle Output in Asia-Pacific Elevates Turbo Demand | +1.9% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| OEM shift to 48V Electric-assist Turbos for Transient Response | +1.7% | Global, with premium segment early adoption | Medium term (2-4 years) |

| Integration of e-turbos in Hybrid and Plug-in Hybrid Architectures | +1.4% | North America and EU, expanding globally | Long term (≥ 4 years) |

| Early Adoption in Hydrogen ICE and Fuel-cell Air-compression Stacks | +1.0% | EU and Japan leading, with global expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter CO₂ and NOx Legislation Accelerating Turbo-Gasoline Adoption

Emissions regulations are fundamentally altering turbocharger deployment strategies across global automotive markets. The Euro 7 regulation introduces particulate number limits for spark ignition vehicles and mandates gasoline particulate filters for all engines, creating technical requirements that favor turbocharged configurations. Light-duty gasoline engines must integrate enhanced fuel injection and combustion technologies to meet ultra-low emissions thresholds, positioning turbochargers as essential for achieving required power density while maintaining emissions compliance. The regulation's phased implementation creates sustained demand for variable geometry turbochargers to optimize exhaust gas recirculation and aftertreatment system efficiency. This regulatory framework extends beyond Europe, with China and India implementing similar standards, representing over 40% of global vehicle production. The technical complexity of meeting these standards while maintaining performance characteristics drives manufacturers toward sophisticated turbocharging solutions that can modulate boost pressure in real-time based on emissions requirements.

Engine Downsizing for Fleet-Average Fuel-Economy Compliance

Fleet-average fuel economy regulations are compelling manufacturers to extract maximum efficiency from smaller displacement engines through advanced turbocharging. The Corporate Average Fuel Economy standards in North America and similar regulations in Europe create economic incentives for manufacturers to replace larger naturally aspirated engines with smaller turbocharged alternatives. This trend enables manufacturers to maintain performance characteristics while achieving significant fuel economy improvements, with turbocharged engines delivering 20-40% better fuel efficiency compared to naturally aspirated equivalents. The downsizing strategy particularly benefits from twin-scroll and variable geometry turbocharger technologies that minimize turbo lag while maximizing low-end torque production. Manufacturers are increasingly adopting integrated exhaust manifold designs and electric wastegate actuators to optimize transient response characteristics. The economic pressure to meet fleet-average targets creates sustained demand for turbocharging solutions across vehicle segments, from compact passenger cars to mid-size SUVs where downsizing strategies yield the greatest compliance benefits.

Rising Commercial-Vehicle Output in Asia-Pacific Elevates Turbo Demand

Commercial vehicle production expansion across Asia-Pacific markets generates substantial turbocharger demand driven by infrastructure development and logistics sector growth. China's heavy-duty truck market rebounded to approximately 900,000 units in 2023 following a 45% decline in 2022, with CNG and LNG trucks gaining market share due to lower fuel costs and emissions advantages. The shift toward alternative fuel powertrains creates opportunities for specialized turbocharger designs optimized for natural gas combustion characteristics. Indonesia's heavy truck market maintained stability at 26,325 units in 2023, with Japanese manufacturers dominating the segment and driving demand for reliable turbocharging solutions. The region's focus on intercity road network improvements and logistics infrastructure development sustains demand for turbocharged commercial vehicles. Mitsubishi Heavy Industries expanded its Chinese turbocharger production capacity by 20% annually to meet rising local demand, establishing four additional assembly lines to achieve an annual output of 4.35 million units.[2]"Mitsubishi Heavy revving up Chinese turbocharger output", Nikkei Asia, asia.nikkei.com. This capacity expansion reflects manufacturers' confidence in sustained Asia-Pacific commercial vehicle growth and the region's strategic importance for global turbocharger supply chains.

OEM Shift to 48V Electric-Assist Turbos for Transient Response

Automotive manufacturers are integrating 48V electric-assist turbochargers to address transient response limitations while maintaining fuel efficiency benefits. Garrett Motion's 48-volt electric compressor technology enables rapid boost delivery within 300 milliseconds, eliminating traditional turbo lag characteristics that limit consumer acceptance. Technology integrates seamlessly with existing mild-hybrid architectures, providing instantaneous torque delivery at low engine speeds while supporting regenerative braking systems. BorgWarner's eBooster technology eliminates turbo lag entirely through electrically driven compression, allowing smaller high-performance turbocharged engines to deliver naturally aspirated response characteristics. These systems operate independently of exhaust gas flow, enabling precise boost control across all engine operating conditions. The 48V architecture provides sufficient power for high-speed electric motors while maintaining cost competitiveness compared to high-voltage hybrid systems. Valeo's electric supercharger technology delivers boost within 300 milliseconds using switched-reluctance motors, improving fuel economy by up to 20% when combined with regenerative braking capabilities. This technological convergence positions electric-assist turbochargers as essential components for next-generation powertrain architectures that balance performance, efficiency, and emissions compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid BEV Penetration Eliminates Forced-Induction Requirements | -2.3% | Global, with EU and China leading adoption | Medium term (2-4 years) |

| Competitive Cost of Modern Naturally-Aspirated Engines in Less Than 1.2L | -1.1% | Asia-Pacific markets, particularly India and Southeast Asia | Short term (≤ 2 years) |

| Turbo-Lag Perception Limiting Consumer Acceptance in Key Markets | -0.8% | North America and emerging APAC markets | Short term (≤ 2 years) |

| Critical-Metal (Nd-Fe-B) Supply Risk for High-Speed E-Machine Rotors | -0.6% | Global, with China controlling rare earth supply | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid BEV Penetration Eliminates Forced-Induction Requirements

Battery electric vehicle adoption creates structural headwinds for turbocharger demand as manufacturers transition production capacity toward electric powertrains. The fundamental architecture of BEVs eliminates internal combustion engines, removing the need for forced induction systems and creating a zero-sum relationship between electric vehicle penetration and turbocharger market growth. China's new energy vehicle market demonstrates this dynamic, with BEV sales growth directly correlating with reduced demand for traditional turbocharging solutions. However, the transition creates opportunities for turbocharger manufacturers in fuel cell applications, where compressed air delivery systems require specialized centrifugal compressors. IHI Corporation developed electric turbochargers specifically for hydrogen fuel cell systems, featuring oil-free operation and mechatronic integration to optimize fuel cell efficiency[3]"Electric TurboCharger(ETC) for hydrogen-based fuel cell systems," IHI, ihi.co.jp.. The technology addresses fuel cell air supply requirements while maintaining turbocharger manufacturers' core competencies in rotating machinery and aerodynamic design.

Competitive Cost Of Modern Naturally-Aspirated Engines in Less than 1.2L

Small displacement naturally aspirated engines present cost-competitive alternatives to turbocharged configurations in price-sensitive market segments. Modern naturally aspirated engines under 1.2 liters achieve acceptable performance characteristics while avoiding the complexity and cost associated with turbocharging systems. This dynamic particularly affects emerging markets where vehicle affordability remains paramount and consumers prioritize initial purchase price over long-term fuel efficiency benefits. The cost differential becomes more pronounced when considering the additional components required for turbocharged engines, including intercoolers, boost control systems, and enhanced cooling requirements. Manufacturers in India and Southeast Asia continue to offer naturally aspirated variants in compact vehicle segments, where the performance benefits of turbocharging may not justify the additional cost burden. However, this restraint diminishes as emissions regulations tighten and fuel economy standards become more stringent, forcing manufacturers to adopt turbocharging even in entry-level segments. Developing low-cost turbocharger technologies, including simplified wastegate designs and integrated exhaust manifolds, helps manufacturers maintain price competitiveness while meeting regulatory requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Off-highway Drives Mechanization Surge

Passenger cars, by contrast, hold the largest turbocharger market share at 53.48% in 2025, due to the widespread use of small, turbo-gasoline engines that satisfy fleet targets. Commercial trucks and buses contribute 22.37%, and light commercial vans make up 18.29%. Equipment makers now specify variable-geometry and electrically assisted units that maintain boost under constant-speed operation and dusty conditions. Off-highway machinery is on track for a 12.35% CAGR between 2026 and 2031, the fastest in the global turbocharger market.

The agriculture and construction machinery boom in developing economies underpins this momentum. Turbo suppliers are designing water-cooled bearing housings and wider compressor maps for these harsh duty cycles. As emissions laws reach non-road engines, OEMs adopt exhaust-aftertreatment that works best with a responsive turbo. The turbocharger market size allocated to off-highway platforms therefore, scales in tandem with government spending on rural mechanization and infrastructure builds. OEM service programs also push remanufactured units to control lifecycle cost and keep uptime high.

By Fuel Type: Hydrogen ICE emerges as growth catalyst

Diesel held 60.02% of the turbocharger market size in 2025 because of its dominance in freight and off-highway segments, yet hydrogen ICE applications will accelerate at a 25.10% CAGR. Cummins’ new hydrogen engine turbo features bespoke aerodynamics to cope with higher exhaust flow and water vapor. Gasoline engines account for 32.24%, lifted by Euro 7 conformity, while CNG and LPG combined sit at 6.08%.

Hydrogen ICE testing shows up to 165% more power with turbocharging compared to naturally aspirated modes, and zero-carbon combustion is possible when renewable hydrogen is used. Turbo suppliers are therefore investing in seals and stainless materials that defeat hydrogen embrittlement. The turbocharger market share for hydrogen systems is low today, but strong policy backing positions it as a strategic segment for decade-end growth.

By Sales Channel: Aftermarket gains momentum amid fleet aging

OEM fitment represented 77.12% of the turbocharger market in 2025 because every new light vehicle in Europe and over 60% in China now ships with a turbo. However, the replacement segment will grow at 9.12% CAGR as the global turbocharger fleet ages. Modern variable-geometry vanes suffer erosion and require precise calibration, so many fleets choose factory-approved reman units to keep warranties intact.

Garrett’s aftermarket division already supplies 14% of total revenue. BorgWarner launched nine new replacement models in 2024 for BMW and Porsche, illustrating demand from premium car workshops. Distributors also report higher demand for upgraded actuators and e-motor repair kits, evidence that the turbocharger industry now blends hardware with electronic service offerings.

By Turbo Technology: Electric systems reshape performance paradigms

Wastegate designs retained 43.74% of the turbocharger market share in 2025 because they balance cost and durability in high-volume vehicles. Variable geometry units totaled 36.32%, most in light-duty diesel and emerging gasoline variants that need precise exhaust energy control. Twin-scroll accounted for 14.12%, favored by performance models.

Electric turbochargers will grow at 18.62% CAGR as 48 V mild hybrids move mainstream. Garrett’s E-Turbo integrates an e-motor on the shaft, delivering boost irrespective of exhaust mass flow. Ferrari’s 2024 patent for a gear-driven module signals parallel mechanical innovation. Automakers are also experimenting with blended e-turbos that recover turbine energy and feed it back to the crankshaft or a 48 V battery pack. As a result, the turbocharger market size allocated to electric-assist designs is expected to quadruple by 2030.

Geography Analysis

Asia-Pacific dominates the global turbocharger market with a 48.41% share in 2025, reflecting the region's position as the world's largest automotive manufacturing hub and fastest-growing vehicle market, while the Middle East and Africa region is forecast to grow the fastest at 12.98% CAGR. China's heavy-duty trucking industry demonstrates the region's market dynamics, with approximately 900,000 units sold in 2023 following recovery from previous year declines. CNG and LNG trucks gain market share due to lower fuel costs and advantages in emissions. The region benefits from substantial manufacturing capacity expansion, with Mitsubishi Heavy Industries increasing Chinese turbocharger production by 20% annually to meet rising local demand, establishing four additional assembly lines to achieve an annual output of 4.35 million units.

Europe maintains a significant market share, driven by stringent emissions regulations and technological leadership in advanced turbocharger systems. The European Union's Euro 7 emissions regulation, published in May 2024, mandates stricter NOx and particulate matter limits while introducing onboard monitoring systems for emissions compliance, creating sustained demand for variable geometry and electric turbocharger technologies. The regulation's implementation timeline, spanning 2026 to 2034 across vehicle categories, positions Europe as a testing ground for next-generation turbocharger technologies that will eventually spread to global markets.

North America represents 18.37% of the global market, with growth driven by Corporate Average Fuel Economy standards that incentivize turbocharger adoption across vehicle segments. The region benefits from manufacturers achieving 20-40% fuel efficiency improvements through engine downsizing strategies that rely heavily on advanced turbocharging technologies. Cummins' launch of its next-generation 6.7L Turbo Diesel engine for Ram Heavy Duty trucks in January 2025, featuring a new variable-geometry turbocharger and improved air management systems, demonstrates the region's focus on high-performance commercial vehicle applications. The North American market's emphasis on pickup trucks and commercial vehicles creates demand for robust turbocharger designs capable of handling high-torque applications, while the region's adoption of 48V mild-hybrid systems drives innovation in electric-assist turbocharger technologies.

Regulatory Landscape

Emissions compliance is the main regulatory lever shaping turbocharger specifications across major automotive markets. In the European Union, Euro 7 was published as Regulation (EU) 2024/1257, with partial application starting on 29 November 2026 for new types of M1 and N1 vehicles, and with an implementation window extending across vehicle categories through 2034. This pushes OEMs and Tier-1s toward boost systems that support tighter NOx and particulate control alongside on-board monitoring requirements.

In the United States, the U.S. Environmental Protection Agency finalized the Multi-Pollutant Emissions Standards for Model Years 2027 and later light-duty and medium-duty vehicles (published 18 April 2024), phasing requirements through 2032 and influencing certification strategies that link combustion efficiency with tailpipe controls. On the EU execution side, Commission Implementing Regulation (EU) 2025/1706 (published 25 July 2025) sets test procedures and type-approval methodology for Euro 7, increasing the emphasis on durability and repeatable compliance. That, in turn, affects turbocharger materials, actuator calibration, and validation cycles.

Value Chain Analysis

The automotive turbocharger value chain runs from upstream high-temperature alloy and steel inputs (for turbine housings, shafts, and wheels) to precision component manufacturing and joining, then into Tier-1 assembly, OEM integration, and aftermarket service. Core manufacturing steps include casting or forging, friction welding of shaft-to-turbine wheel, heat treatment, CNC machining and grinding, and high-speed balancing, followed by calibration of actuators and controls for wastegate, VGT, and e-turbo variants. Mitsubishi Heavy Industries has highlighted leaner flow concepts, including one-piece flow production with small lots, and local procurement models that keep suppliers within a short radius of plants, showing how throughput and localization are used to manage quality and inventory.

Downstream, OEM fitment remains the dominant route to market, with supply shaped by multi-year platform awards and localized production footprints. In 2025, BorgWarner disclosed several turbocharger wins supporting hybrid and light-vehicle programs with future SOPs across facilities, including Pyeongtaek (Korea), Rzeszow (Poland), and Ramos (Mexico). This reflects how Tier-1s align capacity to customer regions and emissions regimes. Parallel activity in electrified axles and related drivetrain modules, such as Garrett Motion's partnership with Shaanxi Hande Axle, also points to a broader supplier strategy of bundling air-management know-how with electrification-adjacent content to remain embedded in OEM programs.

Competitive Landscape

The turbocharger market exhibits high concentration, with the top 5 manufacturers controlling a significant percentage of global market share, creating intense competitive dynamics among established players. This concentrated structure reflects the significant capital and technology barriers required for advanced turbocharger development and mass production. Regional market dynamics heavily influence the competitive landscape, with Asia-Pacific commanding 48.89% of global market share, Europe 25%, and North America 18.5%. This geographic distribution underscores the strategic importance of Asian manufacturing capabilities and the region's role as both a production hub and end market for turbocharged vehicles.

Strategic positioning varies significantly across regions. Asian manufacturers like IHI Corporation and Mitsubishi Heavy Industries leverage proximity to major automotive production centers to capture market share through cost-competitive solutions and rapid capacity expansion. European and North American players, including BorgWarner and Garrett Motion, focus on technological differentiation through electric turbocharging and hydrogen-compatible systems to maintain premium positioning despite lower regional market shares.

The emerging markets of South America, as well as the Middle East and Africa, present white-space opportunities for market expansion, particularly as infrastructure development and commercial vehicle adoption accelerate in these regions. Ferrari's patent activity around gear-driven turbocharger systems exemplifies how intellectual property is being used to secure competitive advantage in a rapidly evolving market. The industry's pivot toward electrification and alternative fuels creates disruption risk for traditional players and opportunities for smaller contenders to challenge incumbents through specialized electric turbo solutions and digital service integration.

Automotive Turbocharger Industry Leaders

-

BorgWarner Inc.

-

Continental AG

-

Mitsubishi Heavy Industries Ltd

-

IHI Corporation

-

Garrett Motion Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hybridization-driven air-management complexity is creating whitespace for turbocharging systems engineered for fast transient response, thermal cycling durability, and tighter integration with EGR and emissions controls. BorgWarner's February 2026 award to supply variable turbine geometry (VTG) turbochargers for a major European OEM's North American hybrid electric vehicle platform (with production scheduled for 2028) and its May 2026 wins for passenger car and van applications (with phased production starting Q2 2026 through Q2 2029) show that new platform decisions are being made around turbo architectures tuned for hybrid duty cycles rather than legacy steady-state operation.

Regionalized capacity and the aftermarket are also opportunity areas where suppliers are backing demand visibility with capital and product strategy. BMTS Technology announced a USD 25 million expansion at its Ramos Arizpe, Mexico plant in February 2025 to lift capacity by 40% (targeting over 2 million turbochargers per year), supporting North American supply proximity for OEM programs. On the regulatory-technical side, Euro 7 implementation work, including the EU's 2025/1706 implementing rules, reinforces demand for validated, durable boost solutions. California-focused design considerations tied to CARB LEV IV (2026) further highlight the need for turbo systems that tolerate frequent engine on-off cycling in hybrid architectures without emissions drift.

Recent Industry Developments

- May 2026: BorgWarner secured multiple turbocharger business awards with a major European OEM for passenger car and van applications, with production planned to begin in phases from Q2 2026 through Q2 2029. The awards support a multi-site manufacturing approach, including ramp activity in Europe, and reinforce the role of turbocharging as an emissions-and-response enabler for high-volume light vehicles.

- March 2026: Garrett Motion received CARB certification (Executive Order D-871-5) for its PowerMax direct-fit turbocharger for 2015-2019 Ford 6.7L Power Stroke engines. The approval formalizes emissions-compliant aftermarket replacement for a high-use diesel application and strengthens the certified aftermarket channel as fleets and owners extend vehicle life.

- October 2025: BorgWarner agreed to supply 50 mm variable turbine geometry turbochargers for the Stellantis Hurricane 4 Turbo engine, debuting on the 2026 Jeep Grand Cherokee. This program links VTG adoption to a new mainstream gasoline powertrain rollout and tightens Tier-1 positioning on an OEM platform with broad regional volume potential.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value generated from turbochargers fitted on automotive engines, counted across new vehicle fitment and replacement demand, and sized in USD with unit volumes used as a cross-check.

Scope exclusions: We exclude non-automotive turbo machinery used in industrial, marine, and stationary power applications, even if suppliers overlap.

Segmentation Overview

-

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Off-highway (Agricultural, Construction)

-

By Fuel Type

- Gasoline

- Diesel

- CNG/LPG

- Hydrogen Internal-Combustion

-

By Sales Channel

- OEM Fitment

- Replacement / Aftermarket

-

By Turbo Technology

- Wastegate Turbocharger

- Variable Geometry Turbocharger (VGT)

- Twin-Scroll Turbocharger

- Electric Turbocharger

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- Turkey

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool and anchor the model to real vehicle activity before interview-based adjustments were applied. We relied on public sources such as national vehicle registration and production statistics, customs trade databases for turbo-related parts, and emissions policy documents from government transport and environment agencies.

To keep assumptions grounded, technical and adoption signals were also reviewed through patent databases, peer-reviewed automotive engineering journals, and industry association publications tied to powertrain and component standards. These were supported by company annual reports, investor presentations, and reputable press coverage to understand capacity additions, product mix shifts, and regional exposure, along with a paid subscription used for company financials and news screening where public detail was limited. The sources listed above are illustrative and not exhaustive, and many other references were consulted to collect, validate, and clarify the final dataset.

Primary Interviews and Surveys

Primary work focused on validating which turbo technologies are actually being adopted in each major vehicle class, and how OEM fitment and replacement volumes change with parc age and service behavior. We spoke with a mix of component suppliers, distributors, and engineering or sales leaders across APAC, EMEA, and the Americas, so assumptions on pricing, penetration, and regulatory impact could be tightened before final sign-off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 17% | APAC: 45% |

| Mid tier: 53% | Functional/Unit leaders: 26% | EMEA: 36% |

| Smaller Players: 21% | Managers: 57% | Americas: 19% |

Market-Sizing & Forecasting

Our core model uses a top-down approach, where vehicle production and parc signals are reconstructed by region and then filtered by turbo penetration rates for passenger cars, LCVs, and heavier platforms. That demand pool is split into OEM fitment and replacement demand using service rates and typical replacement cycles, followed by an average selling price curve that reflects technology mix.

Selective bottom-up approximations were used as a check, mainly by rolling up a sample of supplier revenue disclosures, channel markups, and region-level volume cues from interviews, then adjusting totals if the two views drift too far. Key inputs used in the model include passenger car versus commercial vehicle output, diesel versus gasoline mix, share of VGT versus wastegate and twin-scroll fitments, OEM fitment share versus aftermarket share, and regional emissions timelines that shift turbo adoption in smaller engines. For forecasting, scenario analysis was used so that different paths for electrification, downsizing, and regulatory tightening can be applied, and then aligned to expert consensus on likely adoption and pricing progression. Where bottom-up detail was missing in smaller regions, gaps were handled through proxy ratios based on similar vehicle parc structures and validated through follow-up calls.

Data Validation & Update Cycle

Outputs were triangulated across multiple checks, including unit-to-value sanity tests, OEM fitment shares versus production volumes, and region splits versus known vehicle manufacturing centers. When unusual spikes appeared, assumptions were rechecked against interview notes and public filings, and then a second analyst review was completed before values were finalized.

The report is refreshed annually, and interim updates are made when there are material shifts such as regulation changes, major capacity expansions, or sharp currency moves that distort USD sizing. Before delivery, a final pass confirms that the latest news and policy signals are reflected in the assumptions and the forecast path.

Mordor Intelligence's Automotive Turbocharger Market Size Versus Other Published Estimates

Published market sizes for automotive turbochargers can look far apart because each study draws the line differently around what counts as an automotive turbocharger, which years are treated as the base, and how pricing is projected as technology shifts. Differences also show up when one estimate leans more on manufacturer revenue reporting, while another leans more on vehicle demand indicators.

The largest gaps usually come from scope and counting logic, such as whether off-highway equipment is included, whether hydrogen ICE applications are counted, and how the split between OEM fitment and replacement demand is handled. Currency conversion timing and the assumed pace of ASP changes, for example higher-priced electric turbo or higher VGT content in the mix, can move the USD total by a noticeable amount when not validated through channel checks and engineering feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.61 B (2026) | |

| Global Consultancy A | USD 16.26 B (2024) | Uses an earlier base year and a broader application frame that explicitly includes agriculture tractors and construction equipment, which can lift totals versus an on-road led demand pool. |

| Regional Consultancy B | USD 16.24 B (2024) | Often blends OEM and replacement channels with limited transparency on unit-to-value checks, and the technology mix assumptions for electric turbo and VGT adoption can push ASP upward faster. |

The table shows a clear year and scope effect behind the spread, and in the Mordor Intelligence model OEM fitment and aftermarket are kept as separate streams, followed by pricing adjusted for the share of VGT, wastegate, and twin-scroll systems. With that setup, the final size stays traceable to measurable vehicle output and parc drivers, and it can be rechecked quickly when an annual refresh is done.

Key Questions Answered in the Report

What is the current size of the turbocharger market?

The turbocharger market stands at USD 13.61 billion in 2026 and is projected to reach USD 22.55 billion by 2031.

Which turbo technology segment is growing the fastest?

Electric turbochargers are expanding at a 18.62% CAGR as 48 V mild-hybrid systems proliferate.

How does Euro 7 influence turbocharger demand?

Euro 7 tightens particulate and NOx limits, making advanced variable-geometry and electric-assist turbos essential for compliance.

Which region will see the quickest turbocharger market growth by 2031?

The Middle East and Africa region leads with a forecast 12.98% CAGR due to infrastructure spending and commercial-vehicle expansion.

Page last updated on: