Compressor Wheel Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

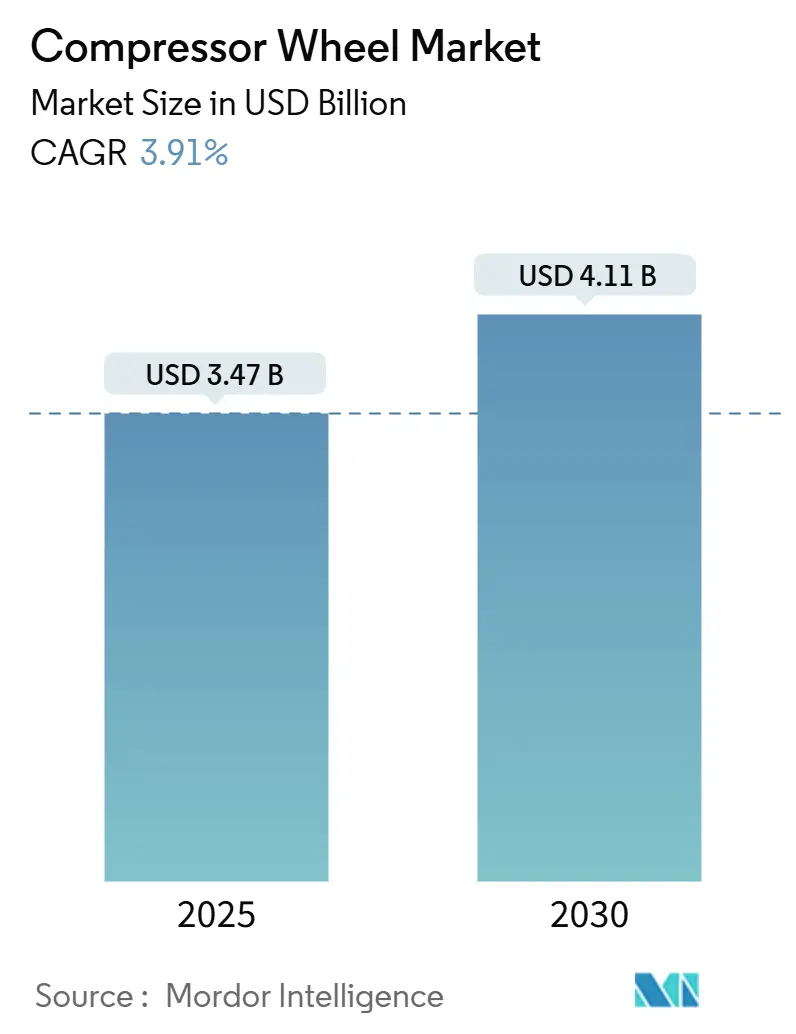

| Market Size (2025) | USD 3.47 Billion |

| Market Size (2030) | USD 4.11 Billion |

| Growth Rate (2025 - 2030) | 3.91% CAGR |

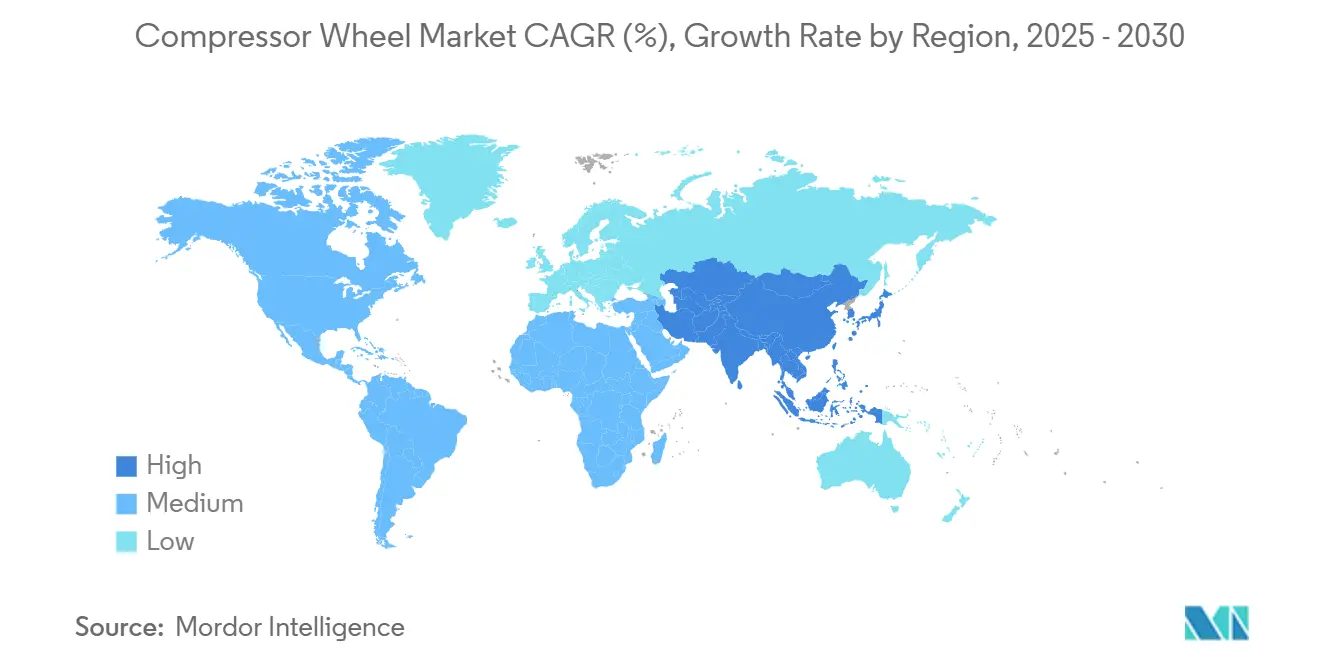

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Compressor Wheel Market Analysis by Mordor Intelligence

The compressor wheel market size equals USD 3.47 billion in 2025 and is forecast to rise to USD 4.11 billion by 2030, reflecting a 3.91% CAGR over the period. Demand pivots from volume gains toward precision manufacturing, with billet and forged wheels commanding premium prices as OEMs chase thermal stability, fatigue resistance, and tighter dimensional tolerances. Asia-Pacific leads both scale and momentum because China adds 5-axis machining centers while Japan continues to perfect ultra-thin blade milling, lifting regional exports to European and North American vehicle programs.

Key Report Takeaways

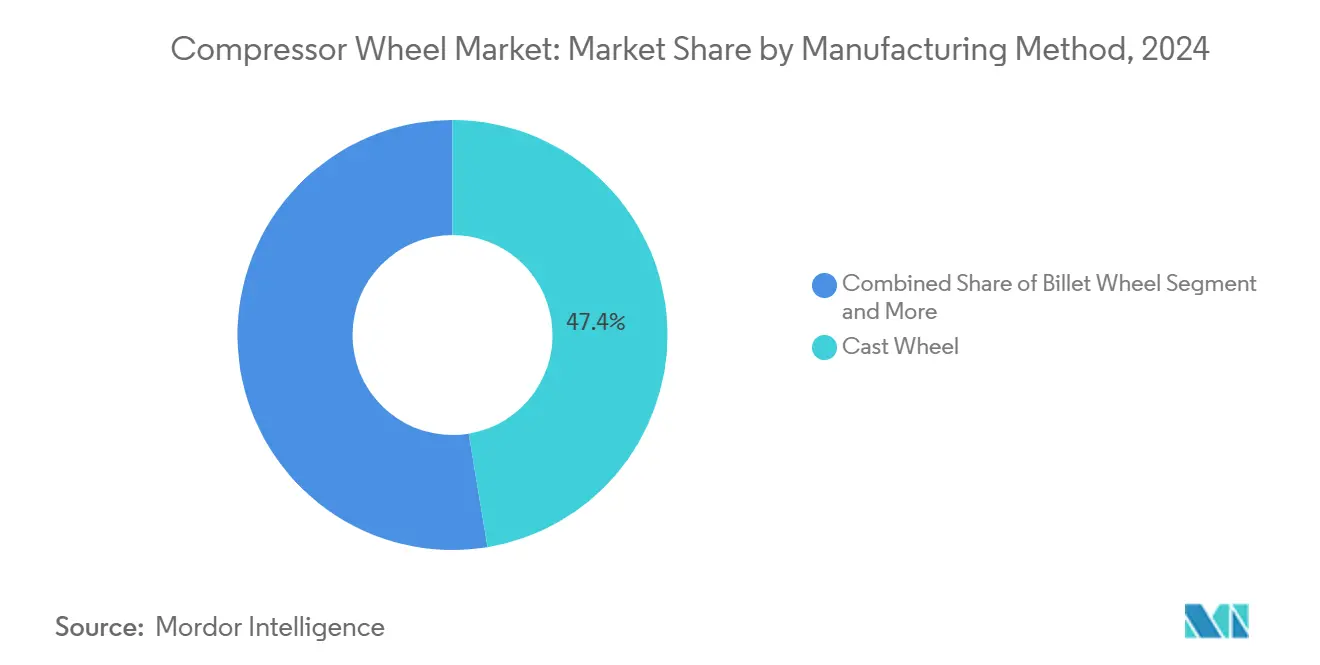

- By manufacturing method, cast wheels held 47.39% of the compressor wheel market share in 2024, while billet wheels are projected to pace the segment at an 8.23% CAGR to 2030.

- By blade design, radial blades commanded 57.82% share of the compressor wheel market in 2024, whereas backward-curved blades are slated to advance at a 7.48% CAGR through 2030.

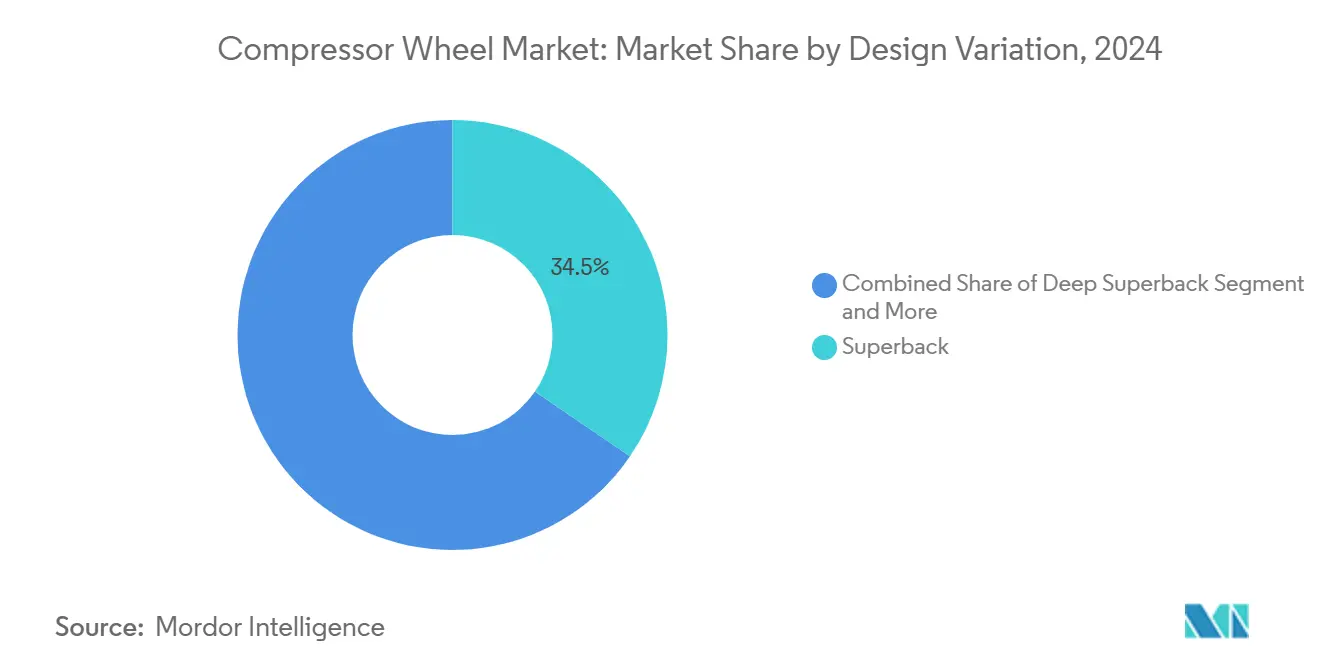

- By design variation, superback configurations accounted for a 34.17% share of the compressor wheel market size in 2024 and deep superback variants are forecast to expand at a 7.94% CAGR between 2025-2030.

- By structural form, open-type wheels captured 45.63% share of the compressor wheel market size in 2024; semi-open wheels are positioned for the fastest growth at a 7.12% CAGR to 2030.

- By geography, Asia-Pacific led with 37.89% share of the compressor wheel market in 2024 and is expected to register the highest CAGR of 8.77% through 2030.

Global Compressor Wheel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle Turbo-Downsizing Demand Surge | +1.2% | Europe and China | Medium Term (2-4 Years) |

| Industrial Centrifugal-Compressor Build-Out | +0.8% | Asia-Pacific, MEA | Long Term (≥ 4 Years) |

| Lightweight Billet-Wheel Adoption | +0.6% | North America and EU | Medium Term (2-4 Years) |

| Additive-Manufactured Wheel Geometries | +0.5% | Global | Long Term (≥ 4 Years) |

| Hydrogen Fuel-Cell Compressor Uptake | +0.3% | Europe and North America | Long Term (≥ 4 Years) |

| E-Turbo High-Strength Forged Wheels | +0.2% | Global | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Vehicle Turbo-Downsizing Demand Surge

Automotive manufacturers accelerate turbocharging adoption to meet stringent emissions standards while maintaining power density, creating sustained compressor wheel demand across passenger and commercial segments. European automakers lead this transition, with turbo penetration rates exceeding 65% in new vehicle launches during 2024, while China's implementation of National VI emission standards drives similar adoption patterns. The shift toward smaller displacement engines with higher boost pressures demands precision-manufactured compressor wheels capable of sustained high-speed operation, typically exceeding 200,000 rpm in modern applications. BorgWarner's February 2025 contract extension with a major North American OEM for wastegate turbochargers through 2028 exemplifies this trend, emphasizing electrically actuated systems for precise boost control and improved fuel efficiency[1]"BorgWarner Solidifies Extended Wastegate Turbo Contracts with Major OEM," borgwarner.com.. This downsizing momentum creates particular demand for advanced compressor wheel materials and geometries that can withstand thermal cycling while delivering consistent performance across wide operating maps.

Industrial Centrifugal-Compressor Build-Out

Process industries expand centrifugal compressor installations to support petrochemical capacity additions and natural gas processing infrastructure, particularly in the Asia-Pacific and Middle East regions, where energy project investments exceed USD 150 billion annually. These applications require larger, more robust compressor wheels designed for continuous operation under severe service conditions, driving demand for forged and billet manufacturing methods over traditional cast alternatives. The industrial segment's growth trajectory benefits from increasing automation in manufacturing facilities and rising demand for compressed air systems across semiconductor, food processing, and pharmaceutical applications. Cummins' extensive 2024-2025 developments in natural gas engine turbocharging and marine applications demonstrate the breadth of industrial compressor wheel applications, from stationary power generation to marine propulsion systems[2]"What is an Electric Turbocharger? Exploring the Power and Efficiency of Garrett’s E-Turbo," garrettmotion.com.. Industrial compressor wheels typically feature larger diameters and more conservative stress margins compared to automotive applications, creating a distinct value segment focused on reliability over peak performance optimization.

Lightweight Billet-Wheel Adoption

Manufacturing advances in 5-axis machining and precision tooling enable cost-effective production of billet compressor wheels, offering superior material properties and design flexibility compared to cast alternatives. Billet manufacturing eliminates porosity concerns inherent in casting processes while enabling complex geometries like integral shrouds and optimized blade thickness distributions that improve aerodynamic efficiency. The aerospace sector drives initial adoption, where weight reduction directly translates to fuel savings, but automotive applications increasingly specify billet wheels for high-performance and electric turbocharger applications. Garrett Motion's development of high-speed electric motor technology for e-boosting systems creates new demand for billet wheels capable of rapid acceleration and deceleration cycles. The manufacturing process's flexibility allows rapid prototyping and customization for niche applications, supporting the market's evolution toward application-specific optimization rather than one-size-fits-all solutions.

Hydrogen Fuel-Cell Compressor Uptake

Hydrogen fuel cell systems require specialized air compressors operating at precise flow rates and pressure ratios, creating new demand for compressor wheels optimized for clean, oil-free operation. These applications demand exceptional reliability and contamination resistance, as any particulate ingress can poison fuel cell membranes and cause system failure. The emerging hydrogen economy drives compressor wheel specifications toward corrosion-resistant materials and surface treatments capable of handling humid, potentially corrosive operating environments. Bosch, Garrett, and Cummins have developed dedicated fuel cell air compressor systems throughout 2024, with Garrett's zero-emission R&D center in Wuhan, China, focusing specifically on electrified turbocharger and e-boosting technologies for hydrogen applications. This application segment remains nascent but represents significant long-term growth potential as hydrogen infrastructure deployment accelerates globally.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Specialty-Alloy Prices | -0.7% | Global | Short Term (≤ 2 Years) |

| Stringent Fatigue-cycle Certification | -0.4% | Global | Medium Term (2-4 Years) |

| Solid-state Hydrogen Compression Threat | -0.2% | Europe and North America | Long Term (≥ 4 Years) |

| China 5-Axis Machining Capacity Risk | -0.3% | Global | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Volatile Specialty-Alloy Prices

Raw material cost fluctuations create significant margin pressure for compressor wheel manufacturers, particularly affecting titanium alloys, superalloys, and tungsten-based materials essential for high-temperature applications. Tungsten prices surged 110% since January 2025, while the titanium Producer Price Index increased 3.37% in 2024, reflecting supply chain constraints and geopolitical tensions affecting key mining regions. These cost pressures force manufacturers to implement dynamic pricing mechanisms and explore alternative materials, though performance requirements often limit substitution options. Nickel surcharge volatility from trade tariffs further complicates cost management for stainless steel and superalloy applications, creating unpredictable input costs that challenge long-term contract negotiations with OEMs. The industry's response includes increased vertical integration and strategic supplier partnerships to mitigate price volatility, though smaller manufacturers remain vulnerable to sudden material cost spikes that can eliminate project profitability.

Stringent Fatigue-Cycle Certification

Regulatory requirements for compressor wheel durability testing extend development timelines and increase certification costs, particularly for aerospace and critical industrial applications. API 617 standards mandate extensive centrifugal compressor testing protocols, while CFR 33.27 requires turbine and compressor rotor overspeed testing to 120% of maximum operating speed, creating substantial validation expenses for new designs. These certification processes can extend product development cycles by 12-18 months and require specialized test facilities capable of high-speed operation under controlled conditions. ISO standards for vibration measurement and fatigue analysis add additional layers of compliance requirements that smaller manufacturers struggle to meet independently. The regulatory framework's evolution toward more stringent safety margins reflects lessons learned from field failures, but creates barriers to innovation and market entry for emerging technologies like additive manufacturing and novel materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Manufacturing Method: Billet Wheels Drive Premium Shift

Cast wheels maintain 47.39% market share in 2024 through cost advantages in high-volume automotive applications, yet billet wheels accelerate at 8.23% CAGR through 2030 as manufacturers prioritize performance over initial cost. The casting process remains dominant for standard turbocharger applications where material properties meet operational requirements and tooling costs can be amortized across large production runs. However, billet manufacturing gains traction in applications demanding superior fatigue resistance, complex geometries, or rapid prototyping capabilities. Forged wheels occupy a middle ground, offering improved material properties over cast alternatives while maintaining reasonable production costs for medium-volume applications.

Advanced manufacturing techniques blur traditional boundaries between these methods, with semi-solid molding (SSM) technology enabling cast wheels to approach billet-like material properties at reduced cost. Additive manufacturing emerges as a fourth category, particularly for prototype development and low-volume specialty applications where geometric complexity justifies higher unit costs. Research into Inconel 625 wire arc additive manufacturing (WAAM) demonstrates the potential for hybrid manufacturing approaches that combine additive and subtractive processes. The manufacturing method selection increasingly depends on application-specific requirements rather than cost alone, reflecting the market's evolution toward performance optimization.

By Blade Design: Efficiency Drives Backward-Curved Adoption

Radial blade configurations dominate with 57.82% market share in 2024, leveraging decades of proven performance in automotive turbocharging applications where packaging constraints favor compact designs. These designs offer predictable performance characteristics and established manufacturing processes that support high-volume production requirements. Backward-curved blades accelerate at 7.48% CAGR through 2030, driven by superior efficiency characteristics that reduce fuel consumption and emissions in both automotive and industrial applications. The aerodynamic advantages of backward-curved designs become more pronounced at higher pressure ratios and flow rates, making them particularly attractive for downsized engines and industrial process applications.

Computational fluid dynamics advances enable more sophisticated blade optimization, with studies showing that backward-curved designs can achieve 1-2% efficiency improvements over radial alternatives in specific operating ranges. Forward-curved blades remain limited to specialized applications where high flow rates at low pressure ratios are required, though they offer manufacturing simplicity for cost-sensitive applications. The blade design selection process increasingly incorporates multi-objective optimization considering efficiency, surge margin, and manufacturing constraints simultaneously, reflecting the industry's move toward application-specific solutions rather than generic designs.

By Design Variation: Deep Superback Gains Momentum

Superback configurations lead with 34.17% market share in 2024, representing the industry standard for balancing aerodynamic performance with manufacturing feasibility across diverse applications. This design variation offers proven performance characteristics while maintaining reasonable production complexity and cost structures. Deep superback variants grow fastest at 7.94% CAGR through 2030, driven by their superior aerodynamic efficiency and extended operating range capabilities that benefit both automotive and industrial applications. The deeper blade curvature enables better flow control and reduced losses, particularly at off-design operating conditions.

Flatback and stepped back designs serve specific niche applications where packaging constraints or cost considerations override aerodynamic optimization. These simpler geometries remain relevant for high-volume, cost-sensitive applications where performance requirements are less demanding. The trend toward more sophisticated design variations reflects advances in manufacturing capabilities and computational design tools that enable cost-effective production of complex geometries. Optimization studies demonstrate that deep superback configurations can achieve 1.5-2% efficiency improvements over standard superback designs, justifying the additional manufacturing complexity for performance-critical applications.

By Structural Form: Semi-Open Designs Gain Traction

Open type configurations maintain 45.63% market share in 2024, benefiting from manufacturing simplicity and cost advantages that make them attractive for high-volume automotive applications. These designs eliminate the complexity of integral shrouds while providing adequate performance for most turbocharging applications. Semi-open structures grow fastest at 7.12% CAGR through 2030, offering improved aerodynamic efficiency through partial shrouding while maintaining reasonable manufacturing complexity. The semi-open design provides better tip clearance control and reduced leakage losses compared to fully open configurations.

Closed impellers serve specialized applications requiring maximum efficiency and minimal leakage, though their manufacturing complexity and cost limit adoption to high-value applications. The structural form selection depends heavily on application requirements, with automotive applications typically favoring open designs for cost reasons while industrial and aerospace applications increasingly specify semi-open or closed configurations for performance advantages. Recent advances in 5-axis machining and additive manufacturing reduce the cost penalty associated with more complex structural forms, enabling broader adoption of semi-open designs in previously cost-sensitive applications. applications. applications.

Geography Analysis

Asia-Pacific commands 37.89% market share in 2024 while leading global growth at 8.77% CAGR through 2030, driven by China's expanding manufacturing capacity and Japan's precision engineering expertise. China's machine tool industry expansion includes significant investments in 5-axis machining centers specifically designed for complex compressor wheel geometries, creating both opportunities and competitive pressures for global suppliers. Japanese manufacturers like IHI Corporation and Mitsubishi Heavy Industries leverage advanced materials science and precision manufacturing to serve high-performance applications, while South Korean companies focus on automotive turbocharger components for domestic and export markets. India's growing automotive sector and industrial infrastructure development create additional demand, though local manufacturing capabilities remain limited compared to China and Japan.

North America and Europe represent mature markets with stable demand patterns but slower growth rates, focusing on high-value applications and advanced technology development. North American manufacturers like BorgWarner and Garrett Motion emphasize innovation in electric turbocharging and hydrogen fuel cell applications, leveraging strong R&D capabilities and close OEM relationships. European suppliers concentrate on efficiency optimization and emissions reduction technologies, driven by stringent regulatory requirements and premium automotive applications.

South America, Middle East, and Africa represent emerging opportunities with modest current market shares but growing industrial infrastructure demands. Brazil's automotive sector creates demand for turbocharger components, while Middle Eastern petrochemical investments drive industrial compressor wheel requirements. African mining and energy projects generate specialized demand for robust, high-reliability compressor wheels capable of operating in harsh environments.

Competitive Landscape

The compressor wheel market exhibits moderate concentration with established players leveraging decades of aerodynamic expertise and manufacturing scale to maintain competitive positions. Market leaders like BorgWarner, Garrett Motion, and Cummins Turbo Technologies benefit from long-standing OEM relationships and integrated supply chain capabilities that create barriers to entry for smaller competitors. However, the landscape faces disruption from additive manufacturing technologies and emerging applications like hydrogen fuel cells, creating opportunities for nimble suppliers with specialized capabilities.

Technology adoption patterns favor companies that can integrate advanced materials science with precision manufacturing, as evidenced by the industry's shift toward billet and forged wheel production methods. Strategic patterns emphasize vertical integration and technology differentiation, with leading suppliers investing heavily in R&D capabilities and manufacturing automation.

White-space opportunities emerge in specialized applications like hydrogen fuel cell compressors and electric turbocharger systems, where traditional automotive suppliers face competition from aerospace and industrial equipment manufacturers. Patent filings in additive manufacturing and advanced materials indicate intensifying competition for next-generation technologies, while established players defend market positions through exclusive OEM partnerships and manufacturing scale advantages. The competitive dynamics increasingly favor suppliers that can offer complete system solutions rather than standalone components, driving consolidation and strategic partnerships across the value chain.

Compressor Wheel Industry Leaders

-

BorgWarner Turbo Systems

-

Garrett Motion Inc.

-

Cummins Turbo Technologies (Holset)

-

Continental AG

-

Mitsubishi Heavy Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Garrett Motion launched G-Series Gen II compressor products, representing next-generation turbocharger technology that leverages the company's legacy expertise while incorporating advanced materials and manufacturing processes for improved performance and durability.

- February 2025: BorgWarner secured extended wastegate turbocharger contracts with a major North American OEM for midsize gasoline engines, with production continuing through 2028 and beyond, emphasizing electrically actuated wastegate systems for precise boost control and emissions compliance .

Global Compressor Wheel Market Report Scope

| Cast Wheel |

| Billet Wheel |

| Forged Wheel |

| Radial Blade |

| Backward-Curved Blade |

| Flatback |

| Stepped Back |

| Superback |

| Deep Superback |

| Open Type |

| Semi-Open |

| Closed |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Manufacturing Method | Cast Wheel | |

| Billet Wheel | ||

| Forged Wheel | ||

| By Blade Design | Radial Blade | |

| Backward-Curved Blade | ||

| By Design Variation | Flatback | |

| Stepped Back | ||

| Superback | ||

| Deep Superback | ||

| By Structural Form | Open Type | |

| Semi-Open | ||

| Closed | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which manufacturing method is growing fastest?

Billet wheels grow at an 8.23% CAGR thanks to superior fatigue resistance and design flexibility, especially for electric turbo and fuel-cell programs.

Why is Asia-Pacific the leading region?

Asia-Pacific controls 37.89% of global revenue because China adds large-scale 5-axis machining while Japan supplies high-precision wheels for export.

What is driving backward-curved blade adoption?

CFD-validated efficiency gains of up to 2 percentage points at higher pressure ratios make backward-curved blades attractive for emissions-focused engines.

How are raw material prices affecting suppliers?

A 110% jump in tungsten and a 3.37% rise in titanium costs squeeze margins, prompting hedge strategies and vertical integration among large vendors.

Which new technology could disrupt traditional wheels?

Solid-state hydrogen compression, now in pilot trials, could limit future demand for centrifugal wheels if it scales commercially after 2030.

Page last updated on: