Automotive Electric Vacuum Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.72 Billion |

| Market Size (2030) | USD 2.42 Billion |

| Growth Rate (2025 - 2030) | 6.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Electric Vacuum Pump Market Analysis by Mordor Intelligence

The Automotive Electric Vacuum Pump Market size is estimated at USD 1.72 billion in 2025, and is expected to reach USD 2.42 billion by 2030, at a CAGR of 6.60% during the forecast period (2025-2030).

The Automotive Electric Vacuum Pump Market is valued at USD 1.72 billion in 2025 and is projected to reach USD 2.42 billion by 2030, registering a compound annual growth rate of 6.60% during the forecast period. This growth trajectory reflects the automotive industry's accelerated transition toward electrified powertrains, where traditional engine-driven vacuum sources become unavailable, necessitating electrically powered alternatives for brake assist and auxiliary systems. The market's expansion coincides with stricter global emission standards and the proliferation of turbocharged gasoline direct injection engines that require supplementary vacuum generation beyond what naturally aspirated engines traditionally provided.

Key Report Takeaways

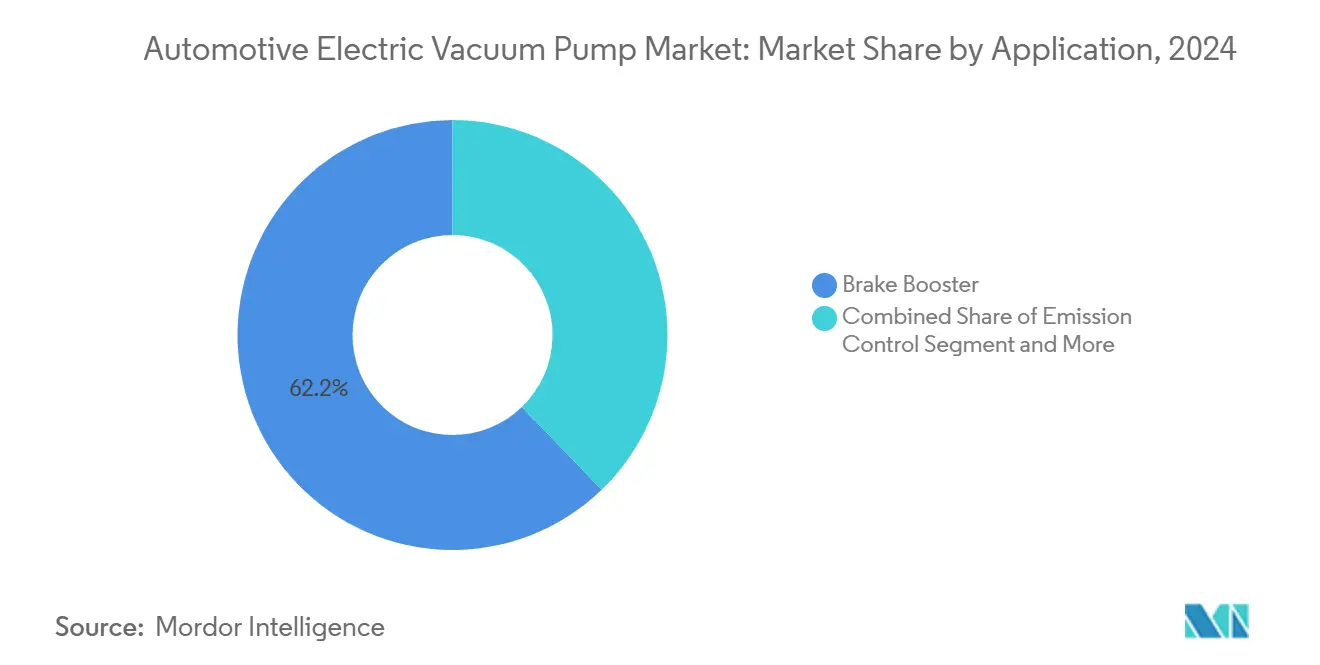

- By application, brake booster systems led with 62.16% of automotive electric vacuum pump market share in 2024; emission control is projected to grow at a 12.42% CAGR through 2030.

- By vehicle type, passenger vehicles accounted for 68.05% share of the automotive electric vacuum pump market size in 2024, while battery electric vehicles are advancing at a 16.68% CAGR to 2030.

- By propulsion type, internal combustion engines commanded 54.08% of the automotive electric vacuum pump market size in 2024; battery electric vehicles record the highest forecast CAGR at 18.92%.

- By sales channel, the OEM segment held 71.11% automotive electric vacuum pump market share in 2024, whereas the aftermarket is set to expand at a 10.21% CAGR through 2030.

- Asia-Pacific captured 42.07% of the automotive electric vacuum pump market size in 2024 and is poised to post an 11.49% CAGR through 2030, driven primarily by China’s EV leadership.

Market Trends and Insights

Drivers Impact Analysis of Automotive Electric Vacuum Pump Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in BEV and HEV Production | +2.1% | Global, with Asia-Pacific core leadership | Medium term (2-4 years) |

| Stricter Global Brake-Safety and Emission Norms | +1.8% | Global, EU and China leading adoption | Long term (≥ 4 years) |

| OEM Migration to Electrified Auxiliaries | +1.4% | North America and EU focus, Asia-Pacific following | Medium term (2-4 years) |

| AI-Optimised Pump Control Cutting Battery Size | +0.9% | Premium segments globally | Long term (≥ 4 years) |

| Turbo-GDI Engines Need Supplementary Vacuum | +0.4% | Global, mature markets emphasis | Short term (≤ 2 years) |

| Expansion of Autonomous Driving Features Increasing Vacuum Demand | +0.7% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in BEV and HEV Production

The electrification wave fundamentally reshapes vacuum generation requirements, as battery electric and hybrid vehicles lack the engine-driven vacuum sources that conventional powertrains provide naturally. This transition creates mandatory demand for electric vacuum pumps in every electrified vehicle platform, transforming the component from optional to essential. BMW's March 2025 announcement of its Gen6 eDrive system for the Neue Klasse platform demonstrates how major OEMs are standardizing electric auxiliary systems across their electrified lineups. The shift extends beyond pure EVs, as mild hybrid systems increasingly adopt 48-volt architectures that enable more efficient electric vacuum pump operation while reducing parasitic losses compared to traditional 12-volt systems.

Stricter Global Brake-Safety and Emission Norms

Regulatory frameworks increasingly mandate advanced braking performance standards that electric vacuum pumps help achieve through consistent, controllable vacuum generation independent of engine operation. NHTSA's November 2024 finalization of FMVSS 127 for automatic emergency braking systems, requiring compliance by September 2029, exemplifies how safety regulations drive demand for reliable auxiliary vacuum systems. Euro 7 brake particulate emission limits, effective 2026, further influence vacuum system design as OEMs seek precise brake modulation capabilities that electric pumps enable through programmable control algorithms. These standards create technical barriers favoring established suppliers with proven regulatory compliance capabilities and testing infrastructure.

OEM Migration to Electrified Auxiliaries

Automotive manufacturers systematically replace belt-driven auxiliary systems with electric alternatives to improve overall vehicle efficiency and enable flexible packaging in electrified architectures. This transition reflects broader industry efforts to eliminate parasitic losses and optimize energy management across vehicle systems. Continental's development of zone control units and software-defined vehicle architectures enables centralized control of electric auxiliaries, including vacuum pumps, through integrated power management systems. The migration accelerates as OEMs pursue weight reduction and packaging flexibility, particularly in electric vehicle platforms where every efficiency gain directly impacts driving range and battery sizing requirements.

AI-Optimized Pump Control Cutting Battery Size

Advanced control algorithms enable electric vacuum pumps to operate with unprecedented precision, reducing energy consumption and allowing smaller battery packs in electric vehicles. These intelligent systems predict braking events and pre-charge vacuum reservoirs during regenerative braking phases, effectively harvesting energy that would otherwise be lost. The integration of machine learning algorithms allows pumps to adapt to individual driving patterns and optimize performance accordingly, representing a significant evolution from traditional on-off control strategies. This technological advancement particularly benefits premium vehicle segments where manufacturers can justify the additional sensor and processing costs required for sophisticated control systems.

Restraints Impact Analysis of Automotive Electric Vacuum Pump Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of Vacuum-Free Brake-By-Wire Systems | -1.2% | Premium segments globally, EU leading | Long term (≥ 4 years) |

| Durability/Contamination Warranty Issues | -0.8% | Global, aftermarket focus | Medium term (2-4 years) |

| Integrated SiC Inverter E-Boosters Displacing Pumps | -1.0% | Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| Supply Chain Constraints for High-Voltage Pump Components | -0.7% | Global, Asia-Pacific critical | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise of Vacuum-Free Brake-By-Wire Systems

Brake-by-wire technology eliminates vacuum requirements entirely by replacing traditional hydraulic-pneumatic brake assist with direct electronic actuation, potentially disrupting the electric vacuum pump market's long-term growth trajectory. Bosch's February 2025 launch of its drive-by-wire brake system, targeting over 5.5 million vehicle applications by 2030, demonstrates the technology's commercial viability and OEM acceptance. Continental's iBooster system similarly provides brake assistance without vacuum dependency, offering faster response times and integration with autonomous driving systems that require precise, electronically controlled braking. The technology's adoption accelerates in premium vehicle segments where cost sensitivity is lower and advanced driver assistance system integration provides additional value justification. However, the transition timeline extends over decades due to cost considerations and the need for extensive validation in safety-critical applications.

Durability and Contamination Warranty Issues

Electric vacuum pump reliability challenges in harsh automotive environments create warranty exposure and aftermarket replacement demand that can constrain OEM adoption and increase the total cost of ownership. Contamination from brake fluid vapors, oil mist, and particulate matter can compromise pump performance and longevity, particularly in systems lacking adequate filtration or separation mechanisms. These durability concerns become more pronounced as vehicles operate in increasingly diverse environmental conditions and as manufacturers extend warranty periods to match electric vehicle expectations. The issue particularly affects aftermarket growth dynamics, where replacement pumps must meet original equipment performance standards while competing on cost with potentially lower-quality alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Electric Vacuum Pump Market Segment Analysis

By Application:

Brake Assist Drives Core DemandBrake booster applications command 62.16% market share in 2024, reflecting the fundamental safety-critical nature of brake assistance across all vehicle types and powertrains. This dominance stems from regulatory requirements and consumer expectations for consistent braking performance regardless of engine vacuum availability. Emission control systems emerge as the fastest-growing application segment at 12.42% CAGR through 2030, driven by increasingly stringent particulate and NOx reduction requirements that demand precise vacuum control for EGR valves and emission system actuators. Turbocharger and fuel system applications maintain steady demand as turbocharged engines proliferate across vehicle segments, requiring supplementary vacuum for wastegate control and fuel vapor management systems.

The application landscape reflects broader automotive trends toward system integration and multi-functional components. Continental's development of integrated brake control units demonstrates how suppliers combine vacuum generation with electronic brake distribution and stability control functions. This integration strategy enables cost reduction through shared electronics and packaging while improving system response times and diagnostic capabilities. Emission control applications particularly benefit from electric vacuum pumps' precise control characteristics, enabling optimized EGR flow rates and improved catalyst efficiency under varying operating conditions.

By Vehicle Type:

Passenger Dominance Amid Commercial GrowthCommercial vehicle segments demonstrate accelerating adoption rates despite passenger vehicles' 68.05% market share dominance in 2024, as fleet operators prioritize reliability and fuel efficiency improvements that electric vacuum pumps enable. Medium and heavy commercial vehicles increasingly adopt electric auxiliary systems to reduce maintenance requirements and improve driver comfort through consistent brake pedal feel regardless of engine load conditions. Light commercial vehicles bridge passenger and commercial applications, benefiting from economies of scale in passenger vehicle component development while requiring enhanced durability specifications.

Battery electric vehicles represent the fastest-growing vehicle type segment at 16.68% CAGR, fundamentally altering vacuum pump requirements through the elimination of engine-driven vacuum sources and integration with regenerative braking systems. Tesla's approach of integrating vacuum pumps with brake control modules exemplifies how EV manufacturers optimize system architecture for weight and packaging efficiency. The transition creates opportunities for suppliers offering integrated solutions that combine vacuum generation with brake control electronics and thermal management systems required for high-performance electric vehicle applications.

By Propulsion Type:

ICE Legacy Meets EV InnovationInternal combustion engines maintain 54.08% market share in 2024 despite battery electric vehicles' explosive 18.92% CAGR growth, indicating the market's dual-track evolution serving both traditional and electrified powertrains simultaneously. This dynamic creates complex supply chain requirements as manufacturers must support legacy ICE applications while investing in next-generation electric vehicle technologies. Hybrid electric vehicles occupy a middle ground, requiring electric vacuum pumps during engine-off operation while benefiting from traditional engine vacuum during combustion phases.

The propulsion type segmentation reveals fundamental shifts in vacuum pump design requirements, as electric vehicles demand integration with high-voltage systems and sophisticated energy management algorithms. Plug-in hybrid electric vehicles present particular complexity, requiring vacuum pumps capable of seamless operation across multiple power sources and operating modes. Fuel cell electric vehicles represent an emerging segment with unique requirements for hydrogen system integration and ultra-high reliability standards. Continental's zone control unit architecture enables centralized management of vacuum systems across different propulsion types, providing scalability and cost reduction through platform sharing.

By Sales Channel:

OEM Integration Drives Aftermarket GrowthOEM channels dominate with 71.11% market share in 2024, reflecting the component's integration-critical nature and the automotive industry's emphasis on system-level validation and warranty coverage. This dominance stems from electric vacuum pumps' role as safety-critical components requiring extensive testing and certification processes that favor established OEM relationships. The aftermarket segment's 10.21% CAGR growth through 2030 signals expanding replacement demand as early electric vehicle fleets mature and require component replacement, creating new revenue streams for suppliers and distributors.

The sales channel dynamics reflect broader automotive industry trends toward direct OEM relationships and reduced tier structures, as electric vacuum pumps' electronic integration requirements favor suppliers with comprehensive system capabilities. Independent aftermarket growth faces challenges from increasing component complexity and diagnostic requirements that favor authorized service networks with access to OEM calibration tools and software updates. However, the segment benefits from growing electric vehicle parc and extended vehicle lifecycles, creating sustained replacement demand beyond traditional warranty periods.

Geography Analysis

APAC Automotive Electric Vacuum Pump Market

Asia-Pacific's commanding 42.07% market share in 2024 and sustained 11.49% CAGR through 2030 reflects the region's dual role as both the world's largest automotive production center and the epicenter of electric vehicle adoption. China's dominance in EV manufacturing creates concentrated demand for electric vacuum pumps, with domestic suppliers like Ningbo Tuopu Group leveraging proximity advantages and cost competitiveness to serve both local and export markets. The region benefits from established supply chains for electric motor components and power electronics that electric vacuum pump manufacturers can leverage for cost reduction and technical advancement. Japan's automotive suppliers, including Denso and Mikuni Corporation, maintain technological leadership through advanced materials and precision manufacturing capabilities that enable high-performance pump designs for premium applications.

Europe Automotive Electric Vacuum Pump Market

Europe faces near-term production challenges with Continental forecasting 3% to 5% passenger vehicle production declines, yet this creates opportunities for higher-value electric vacuum pump integration as OEMs prioritize efficiency gains and regulatory compliance. The region's stringent Euro 7 emission standards and advanced driver assistance system adoption drive demand for sophisticated vacuum control systems that command premium pricing. German suppliers like Continental AG and Robert Bosch GmbH leverage their brake system expertise and OEM relationships to maintain market leadership despite regional production headwinds. The region's focus on premium vehicle segments and advanced technology integration supports higher average selling prices and profit margins compared to volume-focused markets.

North America Automotive Electric Vacuum Pump Market

North America's market development reflects the region's gradual electric vehicle adoption and the domestic automotive industry's emphasis on light trucks and SUVs that require robust auxiliary systems. The region benefits from reshoring initiatives and trade policies that favor domestic suppliers, creating opportunities for established players to expand manufacturing capacity and reduce supply chain risks. Canada's automotive sector integration with U.S. production networks enables efficient cross-border supply chains for electric vacuum pump components and assemblies. The region's aftermarket strength, driven by extended vehicle lifecycles and DIY maintenance culture, supports sustained replacement demand and premium pricing for performance-oriented applications.

Competitive Landscape

The automotive electric vacuum pump market exhibits moderate concentration among established tier-1 suppliers who leverage existing brake system relationships and manufacturing scale to maintain competitive advantages. Continental AG, Robert Bosch GmbH, and Denso Corporation dominate through comprehensive system integration capabilities that combine vacuum generation with brake control electronics and vehicle network interfaces. These suppliers benefit from decades-long OEM relationships and extensive validation infrastructure that creates significant barriers for new entrants seeking to penetrate safety-critical applications. The competitive landscape increasingly favors suppliers offering complete brake system solutions rather than standalone pump components, as OEMs prioritize single-source responsibility and integrated warranty coverage.

Emerging competitive dynamics center on technology differentiation through advanced control algorithms, integrated power electronics, and multi-functional system designs that combine vacuum generation with other auxiliary functions. Smaller specialists like Youngshin Precision Co. Ltd. and VIE Science and Technology compete through focused innovation and cost advantages in specific market segments or geographic regions. The industry's evolution toward brake-by-wire systems creates both threats and opportunities, as suppliers must balance investment in traditional vacuum pump technology with development of alternative actuation methods. Continental's 2024 R&D expenditure of EUR 2.356 billion in its Automotive division demonstrates the scale of investment required to maintain technological leadership across multiple competing architectures.

White-space opportunities exist in emerging markets where local suppliers can leverage cost advantages and government support to challenge established players, particularly in commercial vehicle and aftermarket applications where technical requirements may be less stringent than premium passenger car segments.

Automotive Electric Vacuum Pump Industry Leaders

Hella GmbH and Co. KGaA

Continental AG

Robert Bosch GmbH

Rheinmetall AG

Youngshin Precision Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Automotive Electric Vacuum Pump Market Companies Covered in this Report

- Hella GmbH and Co. KGaA

- Continental AG

- Robert Bosch GmbH

- Rheinmetall AG

- Youngshin Precision Co. Ltd.

- Johnson Electric Holdings

- Mikuni Corporation

- Ningbo Tuopu Group

- Magna International

- Valeo SA

- DENSO Corporation

- SHW AG

- Stackpole International

- VIE Science and Technology

- Fuxin Dare Automotive Parts

- Pierburg (Pierburg Pump Technology)

- WABCO Holdings

- LPR Global

- Hitachi Astemo

- BorgWarner Inc.

Recent Industry Developments in Automotive Electric Vacuum Pump Market

- April 2025: Pedro Gil launched the RVM vacuum booster featuring magnetic coupling technology that eliminates dynamic shaft seals and reduces maintenance requirements. The innovation addresses durability concerns in automotive applications by preventing leakage and extending equipment lifespan through friction reduction at motor coupling interfaces.

- March 2025: BMW Group announced its Gen6 eDrive system for the Neue Klasse electric vehicle platform, incorporating advanced electric auxiliary systems including integrated vacuum generation for brake assist applications. The system demonstrates OEM commitment to standardizing electric vacuum pumps across electrified vehicle lineups.

Global Automotive Electric Vacuum Pump Market Report Scope

Segmentation Overview

| Brake Booster |

| Turbocharger and Fuel Systems |

| Emission Control |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Brake Booster | |

| Turbocharger and Fuel Systems | ||

| Emission Control | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which vehicle category drives the highest unit demand for electric vacuum pumps?

Passenger vehicles account for 68.05% of 2024 volumes, underpinned by global light-vehicle production scale.

Why are electric vacuum pumps critical for battery electric vehicles?

BEVs lack manifold vacuum, so an electric pump is essential to guarantee brake-assist performance independent of engine operation.

What is the primary threat to future pump volumes?

Vacuum-free brake-by-wire systems could reduce pump demand, especially in premium segments adopting the technology after 2028.

Which region leads the automotive electric vacuum pump market?

Asia-Pacific dominates with 42.07% share in 2024, propelled by China’s leadership in electric-vehicle manufacturing.

How are suppliers improving pump energy efficiency?

AI-enabled control predicts braking events and charges vacuum reservoirs during regenerative deceleration, cutting battery load and enabling smaller battery packs in EVs.

Page last updated on: