Electric Vehicle Plastics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

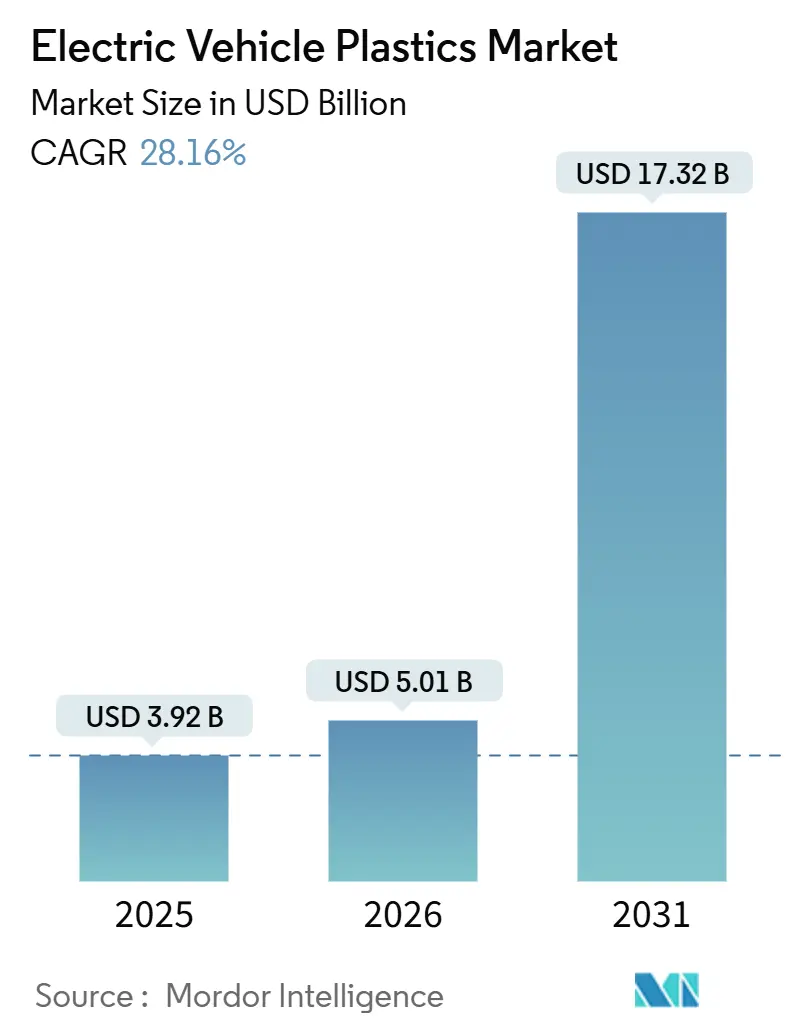

| Market Size (2026) | USD 5.01 Billion |

| Market Size (2031) | USD 17.32 Billion |

| Growth Rate (2026 - 2031) | 28.16% CAGR |

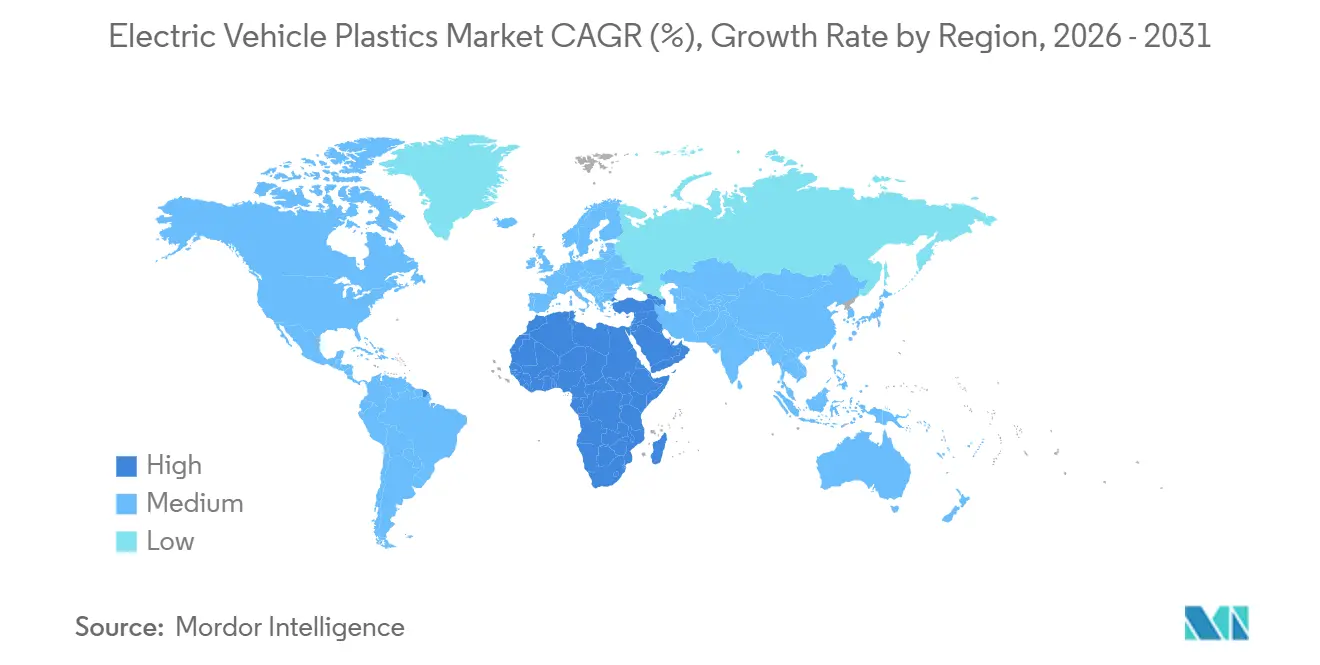

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Plastics Market Analysis by Mordor Intelligence

The Electric Vehicle Plastics Market size is expected to increase from USD 3.92 billion in 2025 to USD 5.01 billion in 2026 and reach USD 17.32 billion by 2031, growing at a CAGR of 28.16% over 2026-2031. Swelling cell-to-pack battery adoption, 800-volt electrical architectures, and China’s January 2026 energy-consumption cap are jointly accelerating polymer demand as automakers shift from aluminum to glass-fiber-reinforced polyamide to meet lightweighting targets. The electric vehicle plastics market is also benefiting from the EU Battery Regulation 2023/1542, which is forcing redesigns around recyclable, flame-retardant resins that tolerate chemical depolymerization without additive loss. Meanwhile, the industry’s pivot to more than 800 V systems compels dielectric-robust resins able to withstand greater than or equal to 20 kV/mm, opening premium niches for polyimide, PEEK, and PPS grades. Finally, Asia-Pacific’s control of about 70% of phosphorus-based flame-retardant capacity keeps supply risk high and encourages Western OEMs (original equipment manufacturers) to dual-source compounds, preserving a fragmented supply structure that restrains margin compression.

Key Report Takeaways

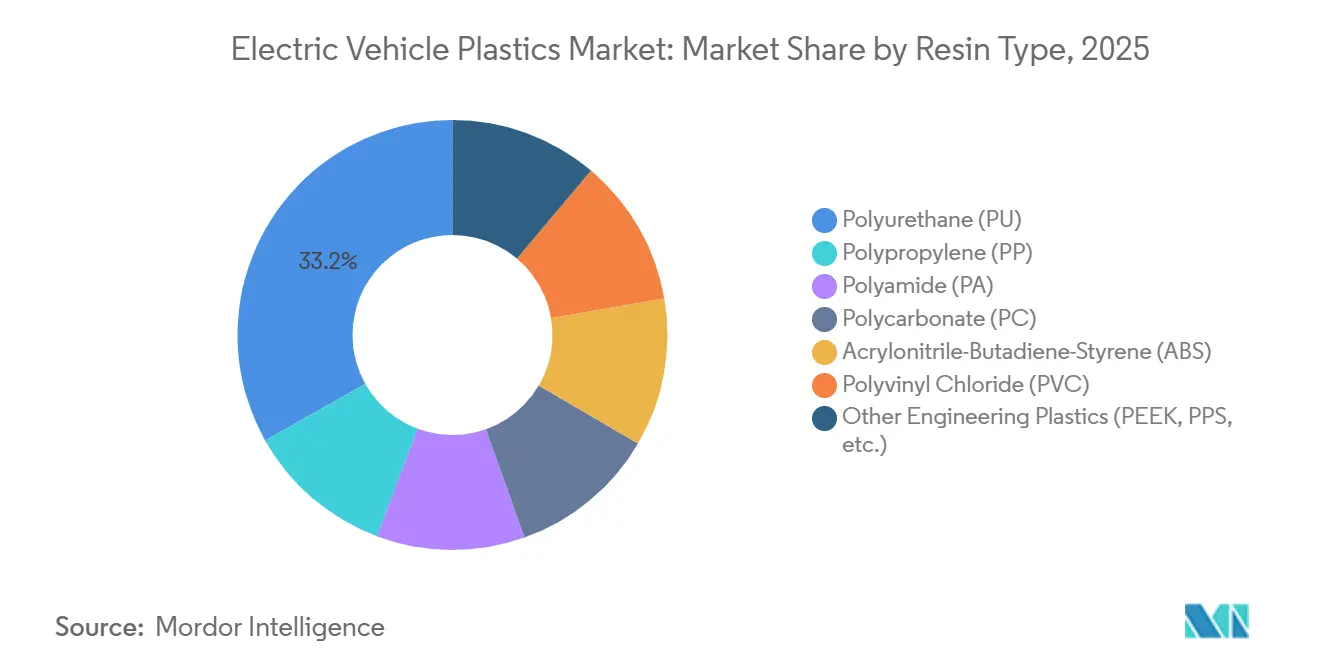

- By resin type, polyurethane (PU) led with 33.15% of the electric vehicle plastic market share in 2025, whereas polyamide (PA) is on track for 29.31% CAGR through 2031.

- By processing method, injection molding held 45.20% revenue share in 2025, while injection molding is projected to post the fastest 29.45% CAGR to 2031.

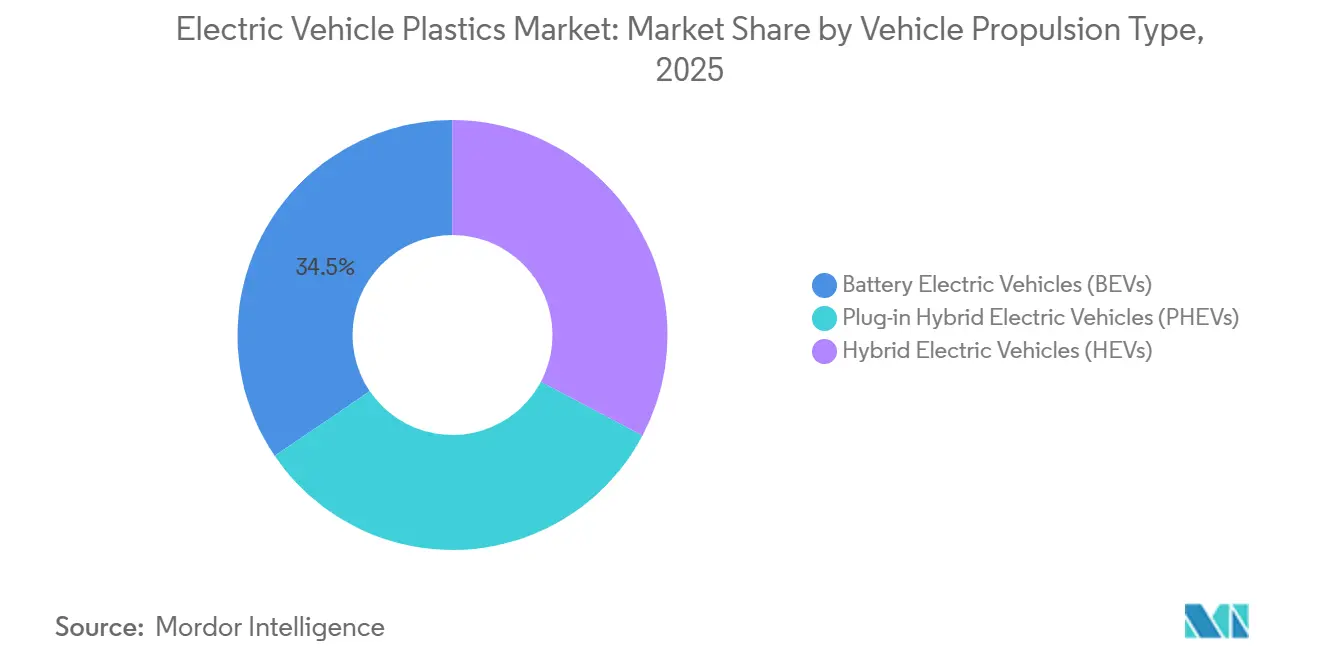

- By vehicle type, battery electric vehicles (BEVs) captured 34.50% of the electric vehicle plastic market size in 2025, and the share of Hybrid Electric Vehicles (HEVs) will expand at 29.41% CAGR over the forecast horizon (2026-2031).

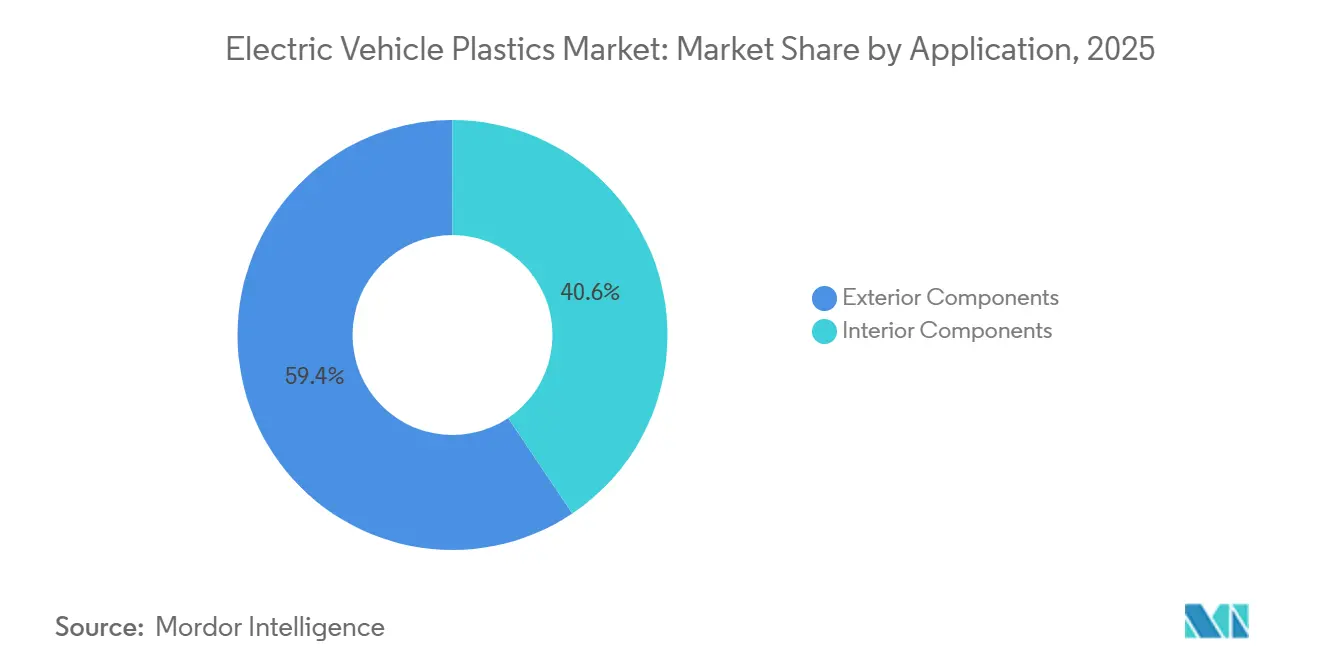

- By application, exterior components commanded 59.40% of the electric vehicle plastic market size in 2025; interior components are advancing at 29.74% CAGR to 2031.

- By geography, the Asia-Pacific accounted for 43.20% revenue share in 2025. The share of the Middle East and Africa is expected to increase at a CAGR of 29.51% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electric Vehicle Plastics Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global EV production and adoption | +8.2% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Lightweighting imperative to extend range | +6.5% | Global, particularly Europe and North America facing stringent efficiency mandates | Long term (≥ 4 years) |

| Tightening CO₂/efficiency regulations | +5.8% | Europe (EU CO₂ standards), China (energy consumption limits), North America (EPA CAFE) | Short term (≤ 2 years) |

| Cell-to-pack designs need flame-retardant housings | +4.7% | Asia-Pacific (CATL, BYD leadership), spill-over to North America and Europe | Medium term (2-4 years) |

| Demand for dielectric-robust polymers for greater than or equal to 800V systems | +3.0% | Global, led by premium OEMs in Germany, South Korea, United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global EV Production and Adoption

Global electric-vehicle sales climbed to 20.7 million units in 2025, a 20% jump year-on-year, anchored by China’s 12.9 million units[1]International Energy Agency, “Global EV Outlook 2026,” iea.org. Such a scale compresses material-qualification windows from 24 to 12 months, pushing resin suppliers to pre-approve grades with multiple OEMs in parallel. The surge fragments demand by propulsion architecture, forcing compounders to stock both premium polycarbonate for battery-electric modules and cost-sensitive ABS for hybrid trims. China’s dual-credit scheme, worth up to 5.6 credits per BEV in 2026, is already creating spot shortages of flame-retardant polyamide in the Pearl River Delta. Tier-one suppliers calculate that every additional million EVs consumes 12,000-15,000 tons of engineering plastics, a ratio expected to hold through 2028.

Lightweighting Imperative to Extend Range

Replacing aluminum with glass-fiber-reinforced polyamide in battery trays cuts 8-12 kg per vehicle, extending range 2-3 km under WLTP, enough to shift models past key psychological thresholds. BASF’s UL 94 V-0-rated Ultramid Advanced N3U42G6 lets designers remove a further 15% mass from 800-V connector housings without losing dielectric safety. The imperative intensifies in Eastern Europe, where 62% of shoppers still cite range anxiety as the top barrier. Lightweighting cascades into suspension: swapping steel links for PA66-GF50 trims unsprung mass, enabling smaller dampers that shave another 2-3 kg. China’s 15.1 kWh/100 km cap for a 2-ton car, effective January 2026, essentially mandates polymer substitution in at least three vehicle systems[2]China Association of Automobile Manufacturers, “Energy Consumption Standard for Passenger Vehicles,” caam.org.cn.

Tightening CO₂/Efficiency Regulations

The EU (European Union)’s 2030 fleet target of 93.6 g/km forces OEMs to electrify nearly half their sales or risk EUR 95 per gram fines. EPA (Environmental Protection Agency) rules finalized in March 2024 aim for 56% U.S. zero-emission penetration by 2032, creating a projected 1.2 Mt incremental polymer pull for battery housings and thermal ducts. China’s CAFÉ rules now penalize fleets above 4 L/100 km, shifting ICE line-ups into hybrid territory where polymers still dominate smaller pack designs. Regulation even dictates additive chemistry: EU Battery Regulation requires 16% recycled cobalt by 2031, forcing flame-retardant compounds compatible with closed-loop recycling that avoids additive volatilization. South Korea’s Eco-Friendly Vehicle Act ties subsidies to 50% domestic content, stimulating LG Chem’s 30 kt polycarbonate expansion.

Cell-to-Pack Designs Need Flame-Retardant Housings

Cell-to-pack trims part counts by 30% yet concentrates thermal-runaway risk into larger housings that must survive 1,200°C flame for five minutes per UN 38.3. SABIC’s long-glass PP Stamax 30YH570 passed nail-penetration tests without propagation at CATARC in 2024. Ultra-low-density polyurethane foams such as H.B. Fuller EV Protect 4006 fill voids and cut peak runaway temperature by 4.1°C. ISO 6469-1 (2024) now requires 30-minute post-impact integrity, steering designs to PA6-GF40 for creep resistance ISO.ORG. Cell-to-chassis iterations tighten dimensional tolerances to ±0.02 mm, driving demand for warp-stable liquid-crystal polymers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced engineering polymers (PEEK, PPS) | -2.8% | Global, most acute in cost-sensitive markets (India, Southeast Asia, South America) | Medium term (2-4 years) |

| End-of-life recycling and material-compatibility gaps | -1.9% | Europe (circular economy mandates), North America, China | Long term (≥ 4 years) |

| Supply volatility of phosphorus-based FR additives | -1.5% | Global, with acute impact in Asia-Pacific and Europe dependent on Chinese exports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Engineering Polymers (PEEK, PPS)

PEEK and PPS trade at USD 45-65/kg and USD 18-28/kg, respectively, versus USD 3.5-5.5/kg for PA6-GF, restricting their use to connectors and slot liners that must survive greater than or equal to 200°C. Toray’s PPS grew at 7% CAGR between 2024 and 2026, yet it stays below 15 kilotons global volume because OEMs ration usage to sub-200 gram parts. Production economics remain unfavorable: PEEK synthesis at 320°C under inert atmosphere drives costs 12-fold above PA66. Substitution trials replacing PEEK with PPA failed Volkswagen’s 145°C thermal-cycling tests in 2024. Cost pressure is most acute in India, where less than or equal to USD 25,000 BEV price points force a shift to PA9T, sacrificing 15% dielectric margin.

End-of-Life Recycling and Material-Compatibility Gaps

Mechanical recycling of FR-polyamide loses 15-25% impact strength after a single pass as aluminum diethylphosphinate volatilizes above 280°C. EU Battery Regulation compels 63% collection by 2027, but only 5% of auto plastics are recycled today, mainly for non-structural parts. Chemical recycling shows promise; BASF’s ChemCycling produced virgin-grade PA6 via mass balance, but 20 kilotons/year plants need EUR 50-80 million capex and 2.5-3.5 megawatt-hour/ton energy input. Thermoset PU foams contaminate PA streams, adding USD 1.20-1.80/kg disassembly cost. BMW-BASF pilots achieve 92% material purity yet scale only to 1.2 kilotons/year against a 15 kilotons retirement need by 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Dominates, Polyamide Accelerates

Polyurethane retained 33.15% share of the electric vehicle plastics market size in 2025, reflecting its dual function as structural foam and potting for cell-to-pack batteries. Huntsman’s Shokless 2.0 foam passed UL 94 V-0 at 12 mm and secured CATL’s Qilin battery business by halting thermal propagation in nail-penetration tests. Polyamide is projected to expand at a 29.31% CAGR for the forecast period (2026-2031), displacing PA66 with PA6 that processes at lower temperatures, trims cycle time 12%, and extends hydrolysis life beyond 100,000 hours per BASF Ultramid Endure trials.

Polycarbonate holds mid-teens share and wins transparent battery covers and panoramic roofs, with Covestro’s 50% bio-attributed Makrolon RE landing BMW and Mercedes orders in 2025. ABS remains the interior trim workhorse despite a 15% density penalty versus PP; Trinseo’s 30% PCR Emerge 3000 is gaining European traction as OEMs chase 25% recycled mandates. Long-glass-fiber PP, such as SABIC’s Stamax, now molds 9-kg battery enclosures in a single shot, challenging PA66 in some cost-driven programs. Niche engineering plastics, PEEK, PPS, and LCP, collectively under 5% electric vehicle plastics market share, remain indispensable for 800-V connectors and slot liners; Syensqo’s Ajedium PEEK enabled 30% thinner insulation on Lucid’s tri-motor Air Sapphire.

By Processing Method: Injection Molding’s Precision Premium

Injection molding accounted for 45.20% electric vehicle plastics market share in 2025 and is poised to rise at 29.45% CAGR during the forecast period (2026-2031), owing to ±0.03 mm tolerances essential for HV connectors. Engel’s all-electric e-motion presses eliminated shot-weight variability, enabling Volkswagen’s Zwickau plant to boost battery-tray output 33% in 2025. Extrusion (~25% share) dominates cable sheathing; Evonik’s Vestamid HTplus co-extrudes PA outer/TPU inner layers to maintain flexibility to -40°C.

Blow-molding remains a niche for fluid reservoirs, while thermoforming serves large interior panels where 90s cycles trump injection’s tooling cost. Compression-molded SMC underbody shields offer specific stiffness 2 times that of aluminum but suffer 3-5 min cure cycles. Additive manufacturing still has less share, yet Vexma’s MJF-printed PA12 prototypes cut tool lead-time from 12 weeks to 48 h, accelerating OEM validation loops.

By Vehicle Propulsion Type: BEVs Lead, HEVs Surge

Battery electric vehicles held 34.50% of the electric vehicle plastics market demand in 2025. Their 75 kWh packs consume 18-22 kg polymers versus 8-11 kg in plug-in hybrids, reflecting more cells and stringent UL 94 V-0 barriers. Tesla’s structural 4680 pack removes 370 metal parts yet needs PU foam greater than or equal to 2 MPa to avert cell deformation under 1.5 g loads. Hybrid electric vehicles will advance at 29.41% CAGR during the forecast period (2026-2031) as Toyota launches 12 new models through 2028, sustaining polymer demand for smaller yet flame-retardant enclosures.

Plug-in hybrids balance EV range with cost, pulling 10-14 kg of plastics per unit and thriving where charging is sparse. European BEV penetration peaks in Norway at 87%, driving per-vehicle polymer intensity to 1.8 kg versus 1.2 kg in southern markets. Fuel-cell EVs remain sub-1%, yet Hyundai’s Nexo employs PPS and PEEK for 700-bar hydrogen valves, hinting at future specialty-resin upside.

By Application: Exterior Components’ Structural Shift

Exterior components captured 59.40% of 2025 revenue as underbody shields and aerodynamic cladding demand long-glass PP or PA capable of surviving 80 km/h stone impacts. Charge-port covers, though 200 grams each, must keep IP67 seals over 150,000 cycles, favoring UV-stabilized polycarbonate. Front-end carriers in PA66-GF35 joined VW’s MEB trio in 2024, eliminating up to 18 brackets and saving 3 kg.

Interior components are expected to grow at 29.74% CAGR for the forecast period (2026-2031) as minimalist cabins require stronger substrates for 17-inch displays; talc-filled PP dashboards limit warpage to 0.5 mm over 1.2 m spans. Door panels migrate to PC/ABS blends with 110 R hardness against scratches, a choice highlighted by Lucid’s 2025 interior spec. Center consoles in PA-GF bear 150 kg loads, demonstrated by Rivian’s gear-tunnel lid. Acoustic polyurethane foams with NRC 0.85 trim cabin noise 2.4 dB at 100 km/h. Tesla’s self-imposed 70 mm/min burn-rate cap is driving halogen-free FR adoption despite a USD 0.80-1.20/kg cost uptick.

Geography Analysis

Asia-Pacific dominated with 43.20% of the electric vehicle plastics market size in 2025, buoyed by China’s 11.76 million NEV output and vertical integration into 70% of global phosphorus FR capacity. Kingfa’s 100 kilotons PA facility in Guangdong now feeds BYD’s blade battery and CATL’s Qilin pack, lifting regional polymer content per vehicle by 22%. Japan contributes high-value PPS and bio-PC grades with 25-40% price premiums, while South Korea’s LG Chem added 30 kilotons of polycarbonate at Yeosu for Hyundai-Kia’s 800 V E-GMP. India lures investment via Covestro’s 2025 Pune PU system house to serve Tata’s EV ramp, and Thailand offers eight-year tax holidays for compounding plants geared to 725,000-unit EV output by 2030.

North America gains from the Inflation Reduction Act’s 50% domestic-content rule that anchored BASF’s USD 150 million PA expansion in Michigan and DuPont’s 25 kilotons PA66 line in Delaware. Mexican compounding under USMCA fulfills “domestic” status, letting Celanese’s Querétaro plant feed GM’s Ultium packs. Canada’s cold-soak needs drive Lanxess Durethan PA6 adoption in Ford’s F-150 Lightning. EPA 2027-2032 rules could lift the United States polymer demand by up to 220 kilotons/year.

Europe faces recycling hurdles: FR-PA loses 15-25% toughness after one loop, yet Regulation 2023/1542 mandates 63% collection by 2027. Lanxess opened an 8 kilotons PA6-PCR line in Germany for VW’s ID series, while Arkema’s bio-based PA11 answers Scope 3 goals at Renault and Stellantis. Post-Brexit United Kingdom aligns with EU rules to dodge 10% tariffs under the TCA, forcing Jaguar Land Rover to meet 45% local-content thresholds. Nordic BEV saturation lifts per-capita polymer intensity, whereas Russia’s sub-5,000-unit EV market remains immaterial.

The Middle East and Africa show the fastest pace at 29.51% CAGR; Lucid’s 155,000-unit Jeddah plant and UAE’s 50% EV-sales target by 2050 trigger local-content rules favoring regional compounding. Brazil’s 35% import tariff spurs BASF’s 15 kilotons PA expansion in Guaratinguetá. South Africa’s load-shedding adds USD 0.15-0.25/kg to molding costs, eroding its labor edge.

Competitive Landscape

The electric vehicle plastics market is moderately fragmented. Process innovation creates white space. RTP Company offers pre-colored Flame Retardant Polyamide (FR-PA), excising paint and trimming USD 1.80-2.40/part for GM Ultium trays in 2024. Digital twins are another moat: BASF’s fiber-orientation model cut prototype loops from seven to three, granting VW a nine-month lead over laggards. Chemical recyclers Pyrowave and Agilyx struck 2025 offtake deals with tier-ones, hinting that circular PA and PS could reach cost parity once European Union (EU) carbon prices exceed EUR 100/ton.

Electric Vehicle Plastics Industry Leaders

BASF

Covestro AG

SABIC

LyondellBasell Industries

LG Chem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Toray Industries, Inc. announced that it has developed Toraypearl polyamide (PA) 12, a spherical PA12 powder widely compatible with powder bed fusion (PBF)-type 3D printers. This powder can help in producing plastic components for electric vehicles.

- May 2025: Toyoda Gosei Co., Ltd. developed a new technology to recycle high-quality plastic from end-of-life vehicles (ELV) in order to meet the growing demand for recycled plastic in the electric vehicle and the rest of the automotive industry against strengthened environmental regulations.

Global Electric Vehicle Plastics Market Report Scope

Electric vehicle (EV) plastics are specialized, lightweight, and flame-retardant polymers designed for battery enclosures, powertrain components, and interior or exterior parts.

The electric vehicle plastics market is segmented by resin type, processing method, vehicle propulsion type, application, and geography. By resin type, the market is segmented into polypropylene (PP), polyamide (PA), polycarbonate (PC), acrylonitrile-butadiene-styrene (ABS), polyurethane (PU), polyvinyl chloride (PVC), and other engineering plastics (PEEK, PPS, etc.). By processing method, the market is segmented into injection molding, extrusion, blow molding, thermoforming, compression molding, and additive manufacturing/3-D printing. By vehicle propulsion type, the market is segmented into battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and hybrid electric vehicles (HEVs). By application, the market is segmented into exterior components and interior components. The report also covers the market size and forecasts for electric vehicle plastics in 18 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Polypropylene (PP) |

| Polyamide (PA) |

| Polycarbonate (PC) |

| Acrylonitrile-Butadiene-Styrene (ABS) |

| Polyurethane (PU) |

| Polyvinyl Chloride (PVC) |

| Other Engineering Plastics (PEEK, PPS, etc.) |

| Injection Molding |

| Extrusion |

| Blow Molding |

| Thermoforming |

| Compression Molding |

| Additive Manufacturing/3-D Printing |

| Battery Electric Vehicles (BEVs) |

| Plug-in Hybrid Electric Vehicles (PHEVs) |

| Hybrid Electric Vehicles (HEVs) |

| Exterior Components |

| Interior Components |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Polypropylene (PP) | |

| Polyamide (PA) | ||

| Polycarbonate (PC) | ||

| Acrylonitrile-Butadiene-Styrene (ABS) | ||

| Polyurethane (PU) | ||

| Polyvinyl Chloride (PVC) | ||

| Other Engineering Plastics (PEEK, PPS, etc.) | ||

| By Processing Method | Injection Molding | |

| Extrusion | ||

| Blow Molding | ||

| Thermoforming | ||

| Compression Molding | ||

| Additive Manufacturing/3-D Printing | ||

| By Vehicle Propulsion Type | Battery Electric Vehicles (BEVs) | |

| Plug-in Hybrid Electric Vehicles (PHEVs) | ||

| Hybrid Electric Vehicles (HEVs) | ||

| By Application | Exterior Components | |

| Interior Components | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast for global demand up to 2031?

The Electric Vehicle Plastics Market size is expected to increase from USD 3.92 billion in 2025 to USD 5.01 billion in 2026 and reach USD 17.32 billion by 2031, growing at a CAGR of 28.16% over 2026-2031.

Which resin held the largest share in 2025?

Polyurethane led with 33.15% of electric vehicle plastics market share in 2025.

Why are 800-volt systems reshaping material choices?

Higher voltages demand dielectric strengths above 20 kV/mm, steering OEMs toward polyimide, PEEK, and PPS grades.

Which region currently leads in revenue?

Asia-Pacific secured 43.20% of 2025 revenue, driven mainly by China’s NEV production.

Page last updated on: