Elastomeric Membrane Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

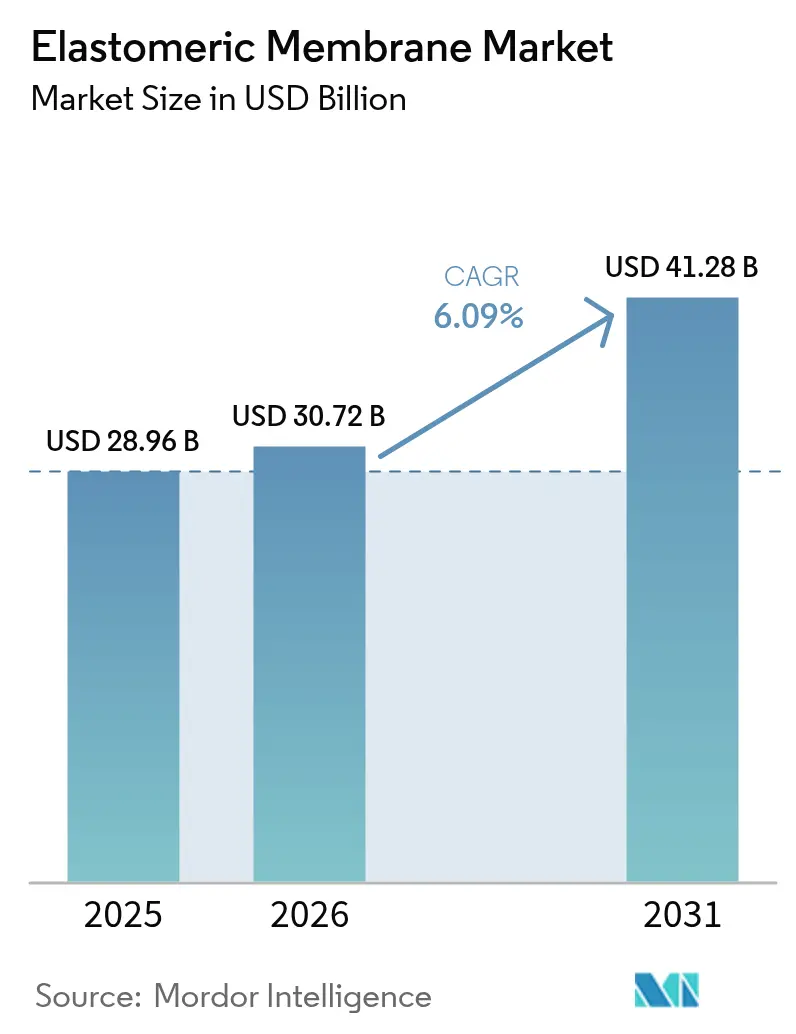

| Market Size (2026) | USD 30.72 Billion |

| Market Size (2031) | USD 41.28 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

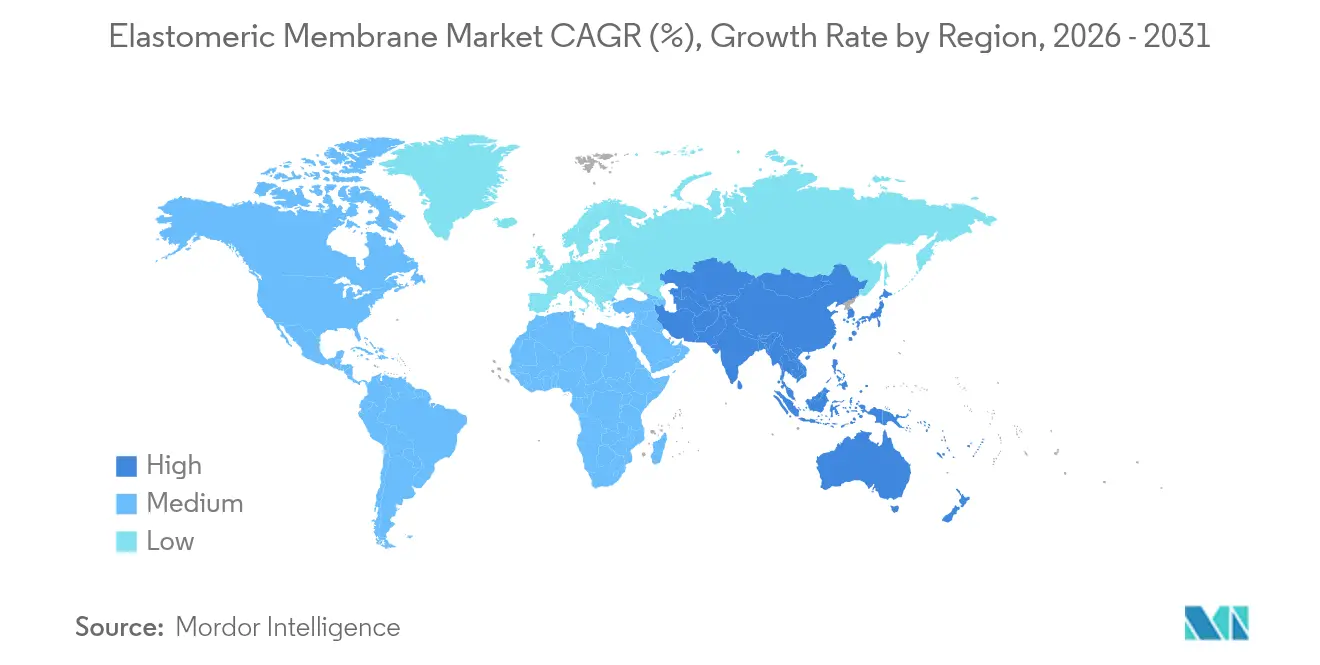

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Elastomeric Membrane Market Analysis by Mordor Intelligence

The Elastomeric Membrane market size is expected to grow from USD 28.96 billion in 2025 to USD 30.72 billion in 2026 and is forecast to reach USD 41.28 billion by 2031 at 6.09% CAGR over 2026-2031. Demand is advancing because rehabilitation projects now outnumber new-build activity in mature economies, while governments everywhere tighten energy-efficiency codes that specify low-permeability membranes with high solar reflectance. Technology selection has become performance-led rather than price-led as contractors look to limit liability in an era of volatile weather patterns. Liquid-applied solutions are carving out share thanks to their seamless installation over existing substrates, and suppliers able to document 20-year warranties or longer gain preference on major bids. Competitive advantage is shifting toward companies that combine polymer innovation with on-site technical support, reflecting the growing complexity of membrane specification on high-performance envelopes.

Key Report Takeaways

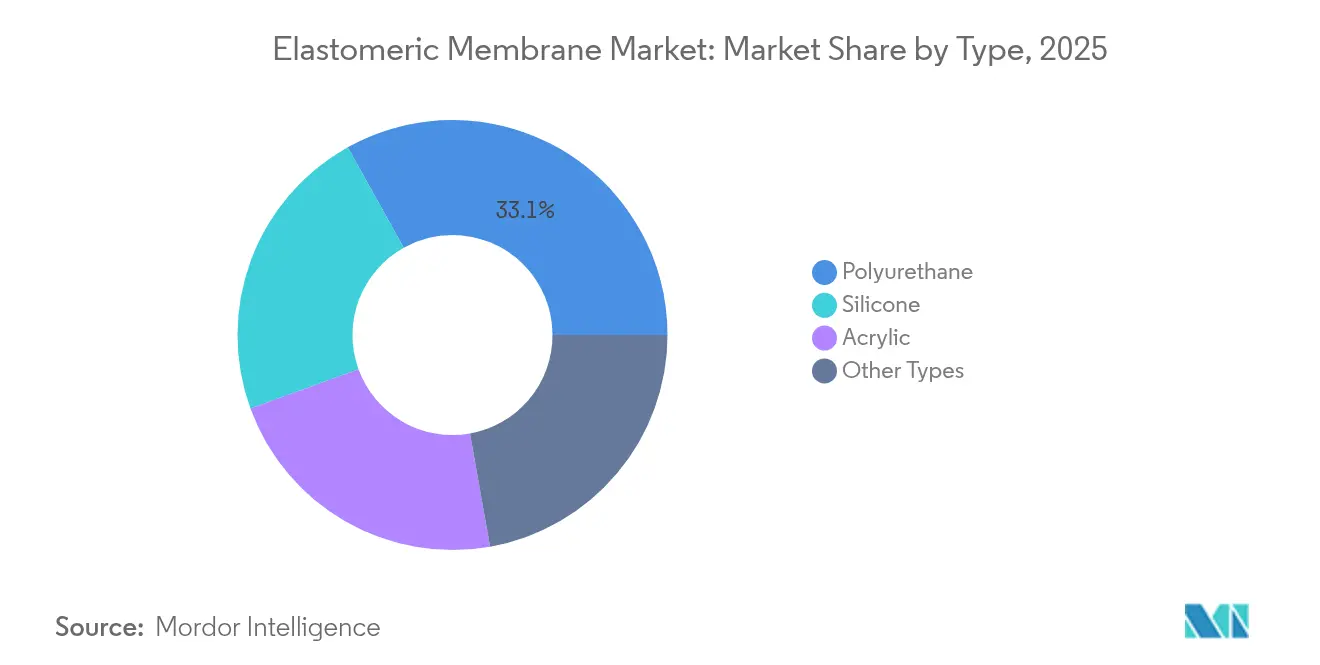

- By type, polyurethane captured 33.10% revenue share of the elastomeric membrane market in 2025, whereas silicone is projected to expand at a 6.44% CAGR through 2031.

- By application, roofing commanded 51.05% share of the elastomeric membrane market size in 2025, while wet areas are advancing at a 6.83% CAGR to 2031.

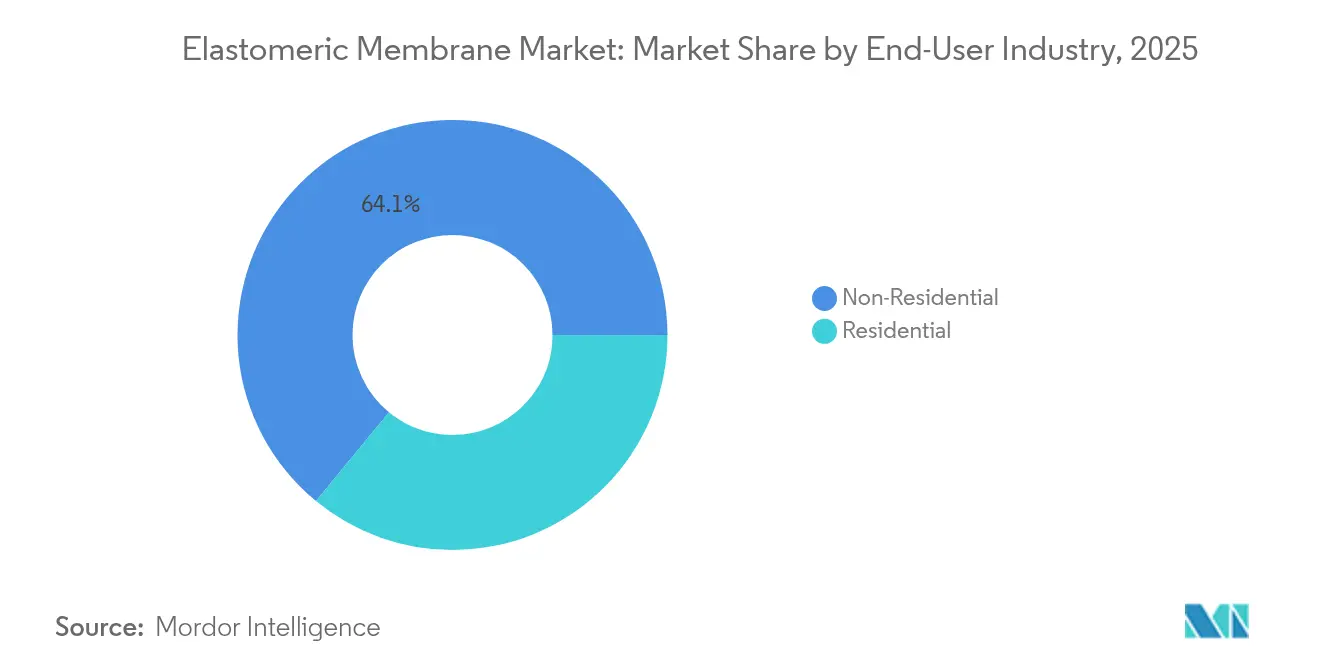

- By end-user, non-residential accounted for 64.05% of demand in 2025; residential is the fastest-growing user segment at 6.55% CAGR through 2031.

- By geography, Asia-Pacific led with 35.40% of the elastomeric membrane market share in 2025 and is tracking a 6.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Elastomeric Membrane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for durable waterproofing in infrastructure rehabilitation | +1.80% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid urban & commercial construction growth | +2.10% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Stringent energy-efficiency & green-building codes | +1.20% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Aging roof stock driving refurbishment activities | +0.90% | North America & Europe primarily | Short term (≤ 2 years) |

| Adoption of liquid-applied membranes in modular off-site builds | +0.60% | Global, early gains in Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Durable Waterproofing in Infrastructure Rehabilitation

Infrastructure rehabilitation dominates procurement agendas as owners replace membranes installed in the 1980s and 1990s. Sika AG recorded 13.5% sales growth in EMEA and 15.1% in the Americas during 2024, largely from rehabilitation work that specified high-performance coatings over concrete structures. Liquid-applied elastomeric systems benefit because they form seamless barriers across irregular substrates without full tear-off, reducing downtime on bridges, tunnels, and parking decks. Climate volatility further raises the stakes: membranes must tolerate more intense freeze-thaw and storm events without splitting. Because failures can trigger costly litigation, specifiers increasingly demand 20- to 30-year warranty cover backed by field performance data. Suppliers that can certify adhesion to damp substrates earn preference in fast-track repair programs where surfaces cannot always be fully dried.

Rapid Urban & Commercial Construction Growth

Asia-Pacific’s building boom is stretching beyond sheer volume into technical sophistication. Smart-city master plans require membranes that integrate moisture protection, heat reflectivity, and, in some cases, photovoltaic compatibility. High-rise developers specify elastomeric membranes able to accommodate structural sway without cracking, a performance envelope that traditional bituminous sheets rarely meet. Contractors running concurrent projects across multiple provinces favor systems with standardized application protocols to minimize retraining, boosting preference for single-component polyurethanes and silicones supplied with manufacturer-certified installer programs. Spill-over demand is visible in Gulf Cooperation Council countries where large commercial complexes mirror Asian design templates.

Stringent Energy-Efficiency & Green-Building Codes

Regulators now frame membrane selection as an energy-management decision. California’s Title 24, for example, mandates aged solar reflectance of 0.63 and thermal emittance of 0.75 for low-slope roofs, effectively excluding dark or non-reflective membranes from many specifications[1]California Energy Commission, “2008 Building Energy Efficiency Standards,” energy.ca.gov . European directives are moving the same way, and Australia’s NCC requires named performance classes for wet-area waterproofing[2]Australian Building Codes Board, “Part 10.2 Wet Area Waterproofing,” ncc.abcb.gov.au . Beyond reflectivity, certification systems such as LEED award points for recyclability and low embodied carbon, prompting suppliers to reformulate with bio-based feedstocks such as Dow’s NORDEL REN EPDM launched in 2025. Owners view premium membranes as a hedge against rising energy tariffs, balancing higher upfront cost with lower cooling loads.

Adoption of Liquid-Applied Membranes in Modular Off-Site Builds

Modular construction relies on factory-assembled volumetric units that must ship weather-tight. Liquid-applied membranes deliver continuous coverage over complex junctions created by bolted modules, eliminating joints that would otherwise require tapes or heat welding. European contractors piloting net-zero schools report cycle-time reductions of three days per block when liquids replace sheets because crews avoid mechanical fastening and cuts. Global adoption should accelerate as automated spray lines scale within modular factories, supported by robotic QA imaging that verifies wet-film thickness in real time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-effective bituminous alternatives | -1.40% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Installation-skill shortages delaying projects | -0.80% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Fire-performance regulatory scrutiny on some polymers | -0.30% | Global, with stricter enforcement in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Effective Bituminous Alternatives

Built-up felt and asphaltic rubber membranes can undercut elastomeric material costs by up to 50%, a gap persuasive to cash-constrained owners. In emerging economies, labor remains inexpensive, and crews are already trained on torch-applied systems, reducing switching incentives. However, rising energy-performance penalties and carbon taxes are eroding this price advantage because bituminous roofs often fail cool-roof criteria. Commodity suppliers respond with reflective mineral granules, but these coatings degrade faster under UV, reopening lifecycle-cost debates and indirectly supporting elastomerics.

Installation-Skill Shortages Delaying Projects

Modern elastomeric membranes require calibrated mixing, substrate moisture checks, and strict ambient-temperature windows. The North American Roofing Contractors Association reports vacancies for skilled applicators remain near a decade high, leading to scheduling delays that erode contractor margins. Manufacturers are accelerating certified-installer programs, supplying mobile mixing rigs, and integrating IoT sensors that log application conditions for warranty validation. While these measures ease the bottleneck, they add cost and complexity, limiting adoption where contractor ecosystems are fragmented.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polyurethane Dominance Faces Silicone Innovation

Polyurethane held 33.10% of the elastomeric membrane market share in 2025, confirming its status as the workhorse for commercial roofs and parking decks. Widespread availability, balanced tensile strength, and chemical resistance keep volume high, especially in refurbishment where adhesion to aged bitumen is critical. Yet silicone grades are accelerating at a 6.44% CAGR as designers prioritize superior UV stability and service temperatures from –50 °C to +200 °C, qualities essential in desert or alpine climates. The elastomeric membrane market size for silicone is therefore projected to close rapidly on polyurethane, buoyed by demand for long-life cool roofs that retain solar reflectance beyond ten years. Suppliers differentiate through one-part moisture-cure chemistries that simplify application and extend open-time in humid conditions.

Innovation also surfaces in bio-content and hybrid chemistries. Dow’s NORDEL REN EPDM line, manufactured with bio-residues under ISCC PLUS, exemplifies how the elastomeric membrane industry is aligning with net-zero targets while preserving mechanical performance. Acrylic dispersions gain niche traction in residential repaint programs where odor restrictions rule out solvent systems, though their lower elongation limits structural applications. Overall, competition is shifting from raw tensile strength to demonstrated service-life data under accelerated-weathering protocols, encouraging transparent third-party testing and longer warranty offers.

By Application: Roofing Leadership Challenged by Wet-Area Growth

Roofing accounted for 51.05% of the value in 2025, reflecting decades of experience with elastomeric sheets and liquids on low-slope commercial decks. Owners value ease of inspection, straightforward repairs, and compatibility with photovoltaic mounts. However, wet areas—bathrooms, balconies, and plant rooms—are set to grow at a 6.83% CAGR, making them the fastest-expanding slice of the elastomeric membrane market. Australia’s NCC now stipulates specific moisture-transmission benchmarks for internal wet zones, pushing builders toward membranes with higher elongation at break and resistance to alkaline screeds. Similar rulemaking is underway in Singapore and parts of the EU, elevating technical entry barriers.

The elastomeric membrane market size for wet-area systems will rise as multifamily residential towers proliferate and as health-care facilities retrofit for infection control, where monolithic, easy-to-clean surfaces are mandatory. Roofing nonetheless remains the brand-recognition platform where manufacturers prove credibility before cross-selling to interior trades. Emerging integrated-envelope designs encourage products certified for multiple uses, enabling contractors to hold one stock-keeping unit for roofs, walls, and wet zones, reducing waste and simplifying training.

By End-User Industry: Non-Residential Dominance Amid Residential Acceleration

Non-residential clients—commercial offices, factories, transport infrastructure—represented 64.05% of 2025 revenue. This segment values corporate-level supply agreements, long warranties, and tested assemblies under FM 4470 or EN 13501, factors suiting global brands with strong technical staffs. Infrastructure, particularly bridge and tunnel waterproofing, adopts customized EPDM sheets with ribbed profiles that bond to concrete decks, exemplified by Polyguard’s bridge membranes. Project scales and public-sector funding make this channel less sensitive to upfront price.

Residential demand is gaining momentum at 6.55% CAGR because stricter building codes mandate resilient wet-area barriers and reflective roof coatings to cut cooling loads. Homeowners increasingly view membranes as energy-saving investments rather than hidden construction items. DIY-friendly acrylic membranes that roll on like paint broaden the addressable base, yet premium single-component polyurethanes are gaining as housing markets shift toward multi-storey concrete construction where movement joints and vibration demand greater elongation.

Geography Analysis

Asia-Pacific maintained 35.40% of global spending in 2025 and is advancing at 6.30% CAGR to 2031, making the region the primary engine of the elastomeric membrane market. National programs—from India’s Smart Cities Mission to Australia’s Resilient Buildings Package—embed waterproofing and heat-island mitigation criteria in public-works tenders, thereby standardizing high-performance membranes. Local producers rapidly climb the technology ladder, licensing European formulations while engineering cost-down versions tailored to tropical or monsoon climates. Singapore’s green-roof mandates encourage cool roof membranes with root-inhibitor additives, a niche where APAC firms now export know-how globally.

North America remains a premium market focused on refurbishment and code-driven upgrades. Consolidation is reshaping supply: Carlisle Companies invested more than USD 2 billion between 2024 and 2025 to add Henry Company, MTL Holdings, and Plasti-Fab, linking membranes with insulation and sealants to deliver complete envelope packages. Energy codes such as ASHRAE 90.1 push cool-roof adoption, while insurance providers reward high-impact-resistance ratings; these features sustain elastomeric adoption despite competition from cheaper modified bitumen.

Europe’s mature construction scene drives innovation in sustainability. Architects specify EPDM systems advertised to last 50+ years and be fully recyclable, aligning with circular-economy regulations. Net-zero directives under the EU Green Deal are ratcheting up reflectivity and VOC limits. Growth rates lag APAC but value per square metre is highest worldwide. Meanwhile, the Middle East and Africa leverage investment in mega-projects and climate-resilient infrastructure. The UAE and Saudi Arabia together consume over half of regional sealants and membranes, stimulated by decision-makers seeking LEED or Estidama certification. Hot-climate performance and sand-abrasion resistance become critical selling points.

Competitive Landscape

The elastomeric membrane market features moderate consolidation. The top five suppliers collectively control an estimated 58% of revenue, led by Sika AG, Carlisle Companies, Soprema Group, Dow, and BASF, each employing acquisition-driven expansion to assemble end-to-end envelope portfolios. Sika’s 2025 purchase of Cromar Building Products adds traditional roofing materials that complement its liquid-applied lines, illustrating a strategic pivot toward “one-stop” offerings. Carlisle, meanwhile, embeds membranes within a bundle that includes rigid insulation and metal edge systems, promoting single-source warranties attractive to design-build contractors.

Technological differentiation outweighs capacity scale. Niche rivals focusing on liquid-applied silicone or polyurea systems win projects where extreme UV exposure or rapid return-to-service is critical. Warranty extensions to 30 years are emerging weapons, backed by accelerated-weathering datasets and remote moisture-scan monitoring embedded in the membrane surface. Sustainability credentials also shape competition; Dow’s bio-based EPDM gives specifiers a tangible carbon-reduction narrative, while BASF promotes solvent-free polyurethanes to comply with urban VOC caps.

Distribution partnerships and certified-installer networks act asgatekeepers; manufacturers that train roofers and provide on-site quality audits gain pricing power, whereas generic commodity providers remain exposed to project delays and skill shortages. Digitization adds another frontier: suppliers now embed QR-coded batch data, allowing contractors to verify shelf life and installation conditions via mobile apps, pushing the market toward traceable, performance-assured supply chains. As technology and sustainability outpace simple volume scale, new entrants offering specialized chemistries continue to pressure incumbents, ensuring that product innovation rather than price remains the decisive battlefield.

Elastomeric Membrane Industry Leaders

Sika AG

Carlisle Companies Inc.

Soprema Group

BASF

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sika acquired Cromar Building Products, strengthening its roofing systems portfolio and reinforcing its position in the European membrane sector. This acquisition expands Sika's expertise in traditional roofing materials while complementing its existing elastomeric membrane solutions.

- July 2024: Dow introduced its bio-based NORDEL REN EPDM at DKT 2024, developed using bio residues to reduce Scope 3 emissions while delivering performance comparable to virgin materials. The ISCC PLUS certified manufacturing process signifies a major advancement in sustainable elastomeric membrane production.

Global Elastomeric Membrane Market Report Scope

The Elastomeric Membrane Market report includes:

| Polyurethane |

| Acrylic |

| Silicone |

| Other Types |

| Residential | |

| Non-Residential | Commercial |

| Industrial | |

| Infrastructure |

| Roofs |

| Walls |

| Wet Areas |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Polyurethane | |

| Acrylic | ||

| Silicone | ||

| Other Types | ||

| By End-user Industry | Residential | |

| Non-Residential | Commercial | |

| Industrial | ||

| Infrastructure | ||

| By Application | Roofs | |

| Walls | ||

| Wet Areas | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the elastomeric membrane market?

The elastomeric membrane market size stands at USD 30.72 billion in 2026.

How fast is demand expected to grow over the next five years?

Global value is projected to expand at a 6.09% CAGR, reaching USD 41.28 billion by 2031.

Which geographic region leads consumption?

Asia-Pacific holds 35.40% of global expenditure and posts the fastest regional CAGR at 6.30%.

Which application is growing quickest?

Wet-area waterproofing demand is forecast to rise at a 6.83% CAGR, outpacing roofing.

What factors most constrain adoption?

Cost-competitive bituminous sheets and shortages of skilled installers remain the primary restraints.

How are suppliers addressing sustainability targets?

Leading firms introduce bio-based or solvent-free chemistries and publish third-party carbon footprints to meet green-building specifications.

Page last updated on: