Automotive Light Weight Material Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 78.89 Billion |

| Market Size (2030) | USD 104.98 Billion |

| Growth Rate (2025 - 2030) | 5.88% CAGR |

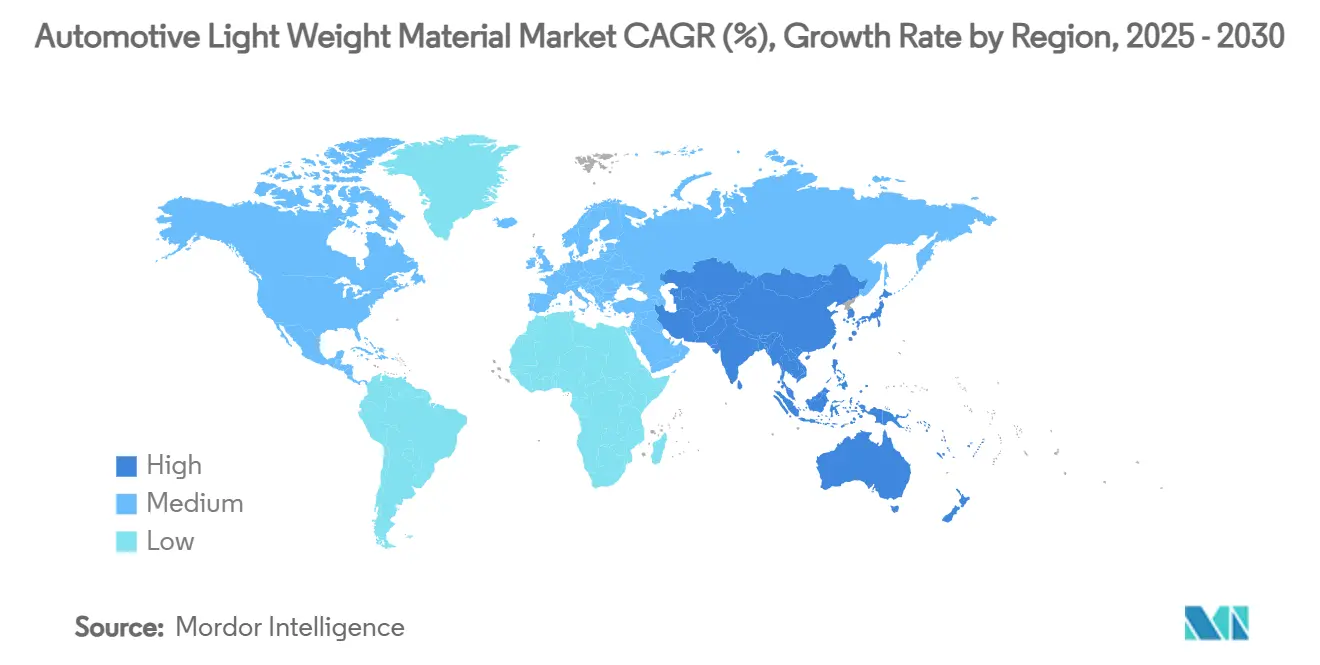

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

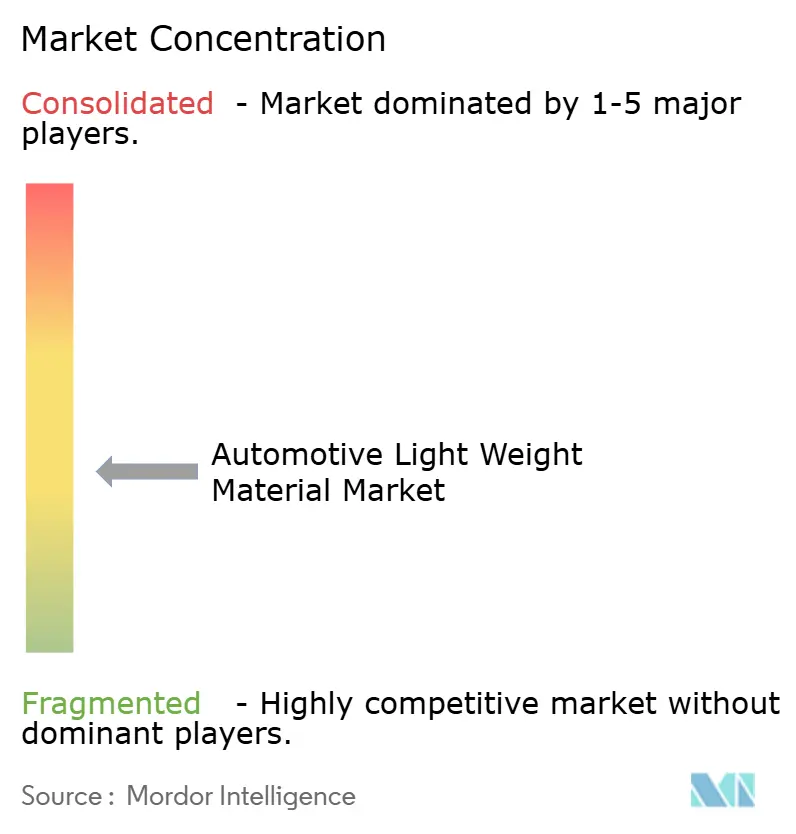

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Light Weight Material Market Analysis by Mordor Intelligence

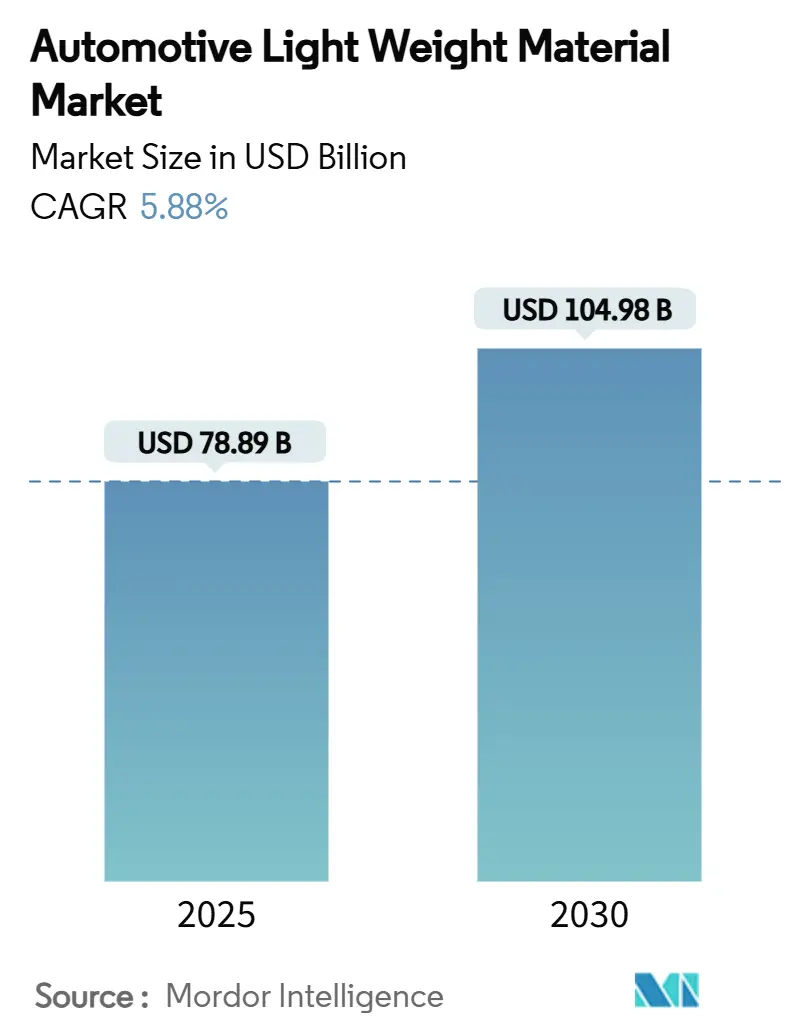

The Automotive Light Weight Material Market size is estimated at USD 78.89 billion in 2025, and is expected to reach USD 104.98 billion by 2030, at a CAGR of 5.88% during the forecast period (2025-2030). Volume expansion comes from regulatory pressure to cut fleet emissions, the requirement to offset the 300-500 kg battery mass in electric vehicles, and the rising need to package AI-sensor payloads without eroding performance. Polymers and composites already dominate the material mix, yet advanced high-strength steels remain relevant where crash performance and cost efficiency intersect. Multi-material architectures are becoming mainstream, so suppliers that master joining, corrosion control, and recyclability gain an advantage. Supply-chain volatility in magnesium and titanium persists, but recycling-driven circular models, especially in Europe and North America, are beginning to mitigate critical-mineral risk.

Key Report Takeaways

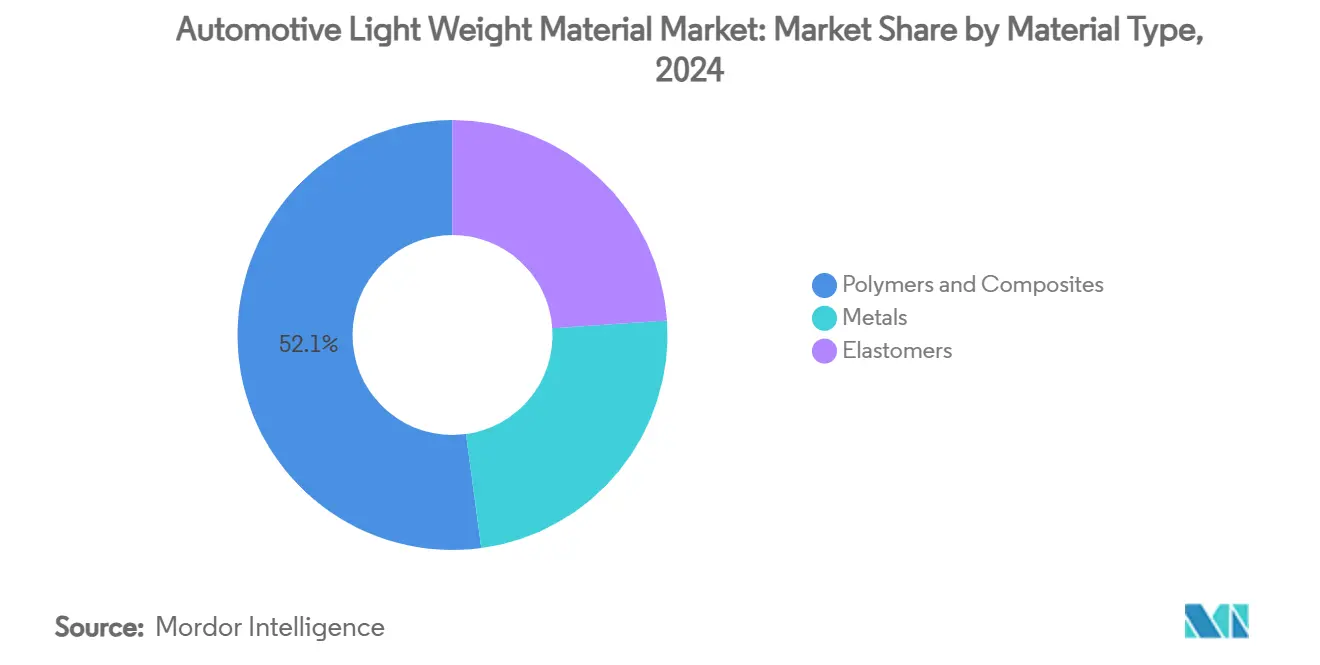

- By material type, polymers and composites held 52.14% of the automotive lightweight material market share in 2024 while registering the fastest CAGR at 6.23% to 2030.

- By vehicle type, light commercial vehicles posted the highest projected CAGR at 6.56% through 2030, whereas passenger cars retained a 62.23% share of the automotive lightweight material market in 2024.

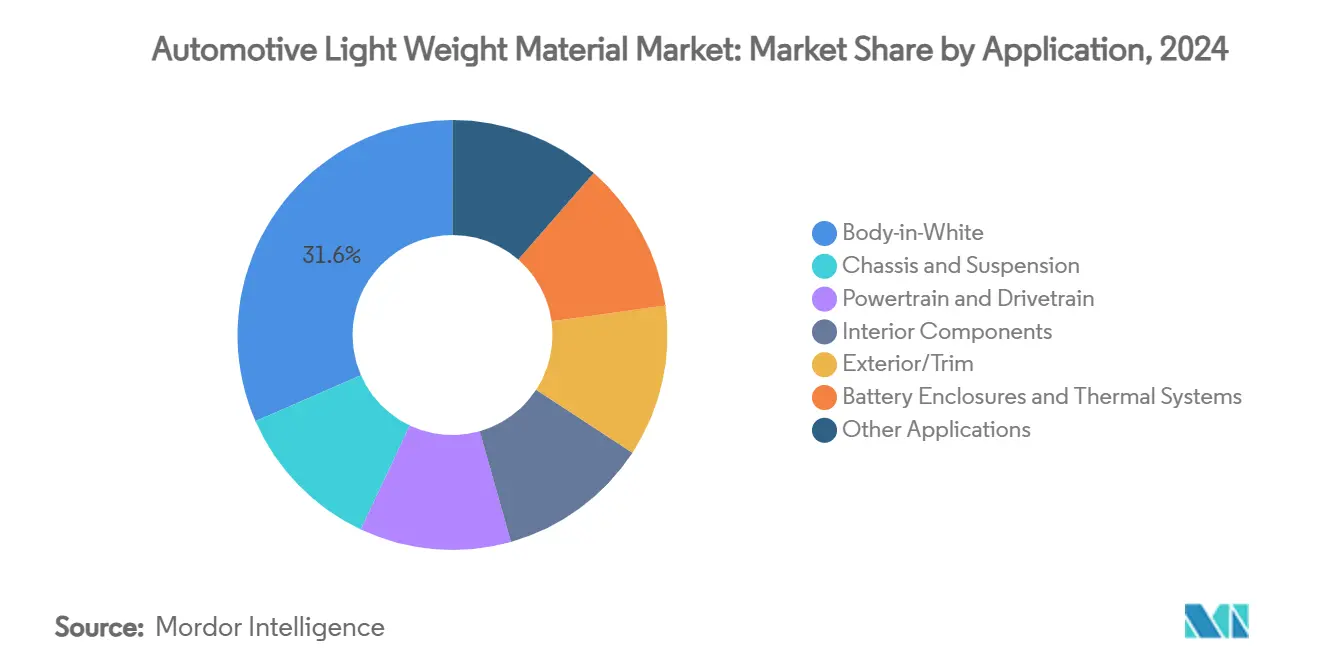

- By application, body-in-white accounted for 31.56% of the automotive lightweight material market size in 2024 and is advancing at a 6.12% CAGR through 2030.

- By geography, Europe held the largest share with 35.78% of the market in 2024, while Asia-Pacific is the fastest growing with a CAGR of 7.12%.

Global Automotive Light Weight Material Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for fuel efficiency and CO₂-reduction | +1.8% | Global with strongest effect in North America and EU | Medium term (2-4 years) |

| Rising adoption of electric and hybrid vehicles | +1.5% | Global led by China and Europe | Long term (≥ 4 years) |

| Stringent global and regional vehicle-weight legislation | +1.2% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Lightweighting for AI-sensor payload in autonomous cars | +0.8% | North America and EU, pilot projects in APAC | Long term (≥ 4 years) |

| Circular-economy credits for embedded carbon reduction | +0.5% | EU leading, adoption spreading to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Fuel Efficiency and CO₂-Reduction

Corporate Average Fuel Economy rules and parallel EU targets force automakers to seek mass savings that cannot be met by power-train tweaks alone. The American Chemistry Council calculated that reverting to heavier materials would add 89 million gallons of fuel over vehicle lifetimes, an outcome regulators will not accept. Advanced high-strength steels enable 25% weight cuts while raising crash safety, which keeps them in vehicle structures even as aluminum and composites expand. Lifecycle assessment now shapes procurement decisions, so recycled aluminum and bio-based composites gain traction where embedded carbon matters more than absolute weight. Weight-adjusted tax incentives in the United States and Europe further reinforce this shift, creating predictable demand visibility for the automotive lightweight material market.

Rising Adoption of Electric and Hybrid Vehicles

Battery packs increase curb weight by 300-500 kg, compelling OEMs to erase mass in every other subsystem just to preserve range. Tesla’s gigacasting consolidates more than 70 parts into a single aluminum component, trimming both weight and complexity at scale. Research at Chalmers University confirms that carbon-fiber structural batteries could raise EV range by 70% once commercialized. Thermoplastic composites are moving into battery enclosures for their thermal-management and weight advantages over steel. As automakers bundle LIDAR, radar, and compute hardware, even modest mass savings translate into real-world range extension, thereby intensifying demand for advanced materials. Novelis anticipates 20-25% regional aluminum growth in Asia purely from the EV build-out.

Stringent Global and Regional Vehicle-Weight Legislation

The 2024 CAFE amendment in the United States and the EU’s forthcoming Euro 7 rules impose steep penalty costs for non-compliance, making lightweight materials economically justified despite higher unit prices. Euro 7 also caps brake particulate emissions, encouraging additive-manufactured disc designs that simultaneously lower weight and particulate output. Regional disparities influence material strategies; European automakers lead in composite uptake, while Asian OEMs emphasize cost-optimized multi-material blends. Lifecycle carbon accounting in new regulations favors integrated suppliers that can document low-carbon material footprints from cradle to gate.

Lightweighting for AI-Sensor Payload in Autonomous Cars

Sensor suites and onboard computing add up to 100 kg to autonomous vehicles, so engineers must recoup mass in structural areas. Higher utilization rates shrink payback periods, allowing fleets to justify carbon fiber and titanium where they once failed cost-benefit tests. Premium vehicle pricing also eases adoption barriers, giving suppliers with composite and advanced alloy portfolios a first-mover edge. Thermal management for CPUs and GPUs pushes aluminum and magnesium demand, while vibration-sensitive sensor mounts increasingly shift to carbon-fiber composites for dimensional stability. Long development timelines for autonomy pipeline signal durable demand in the automotive lightweight material market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced composites and alloys | -1.4% | Global with strongest pressure in price-sensitive segments | Medium term (2-4 years) |

| Manufacturing and repair complexity | -0.9% | Global with variations by technical capability | Short term (≤ 2 years) |

| Supply-chain volatility in critical minerals (Mg, Ti) | -1.1% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Manufacturing and Repair Complexity

Joining aluminum to steel requires isolation layers to curb galvanic corrosion, which adds both grams and dollars. Composite repair often mandates full panel replacement rather than localized fixes, inflating insurance costs in mainstream segments. Suppliers without multi-material expertise struggle to clear qualification hurdles, slowing broad adoption. Additive manufacturing can handle complex geometries but remains throughput-limited for high-volume car programs, leaving most series production to conventional forming or casting methods.

Supply-Chain Volatility in Critical Minerals (Mg, Ti)

Magnesium extraction is geographically concentrated, and ongoing geopolitical tensions threaten steady supply. Titanium sponge capacity is limited outside a handful of producers, creating price shocks when aerospace demand spikes. Hyundai’s USD 5.8 billion recycling heavy complex in Louisiana illustrates one mitigation path: capture scrap streams to reduce virgin-critical-metal exposure. Longer term, localized recycling may soften volatility but will not eliminate it.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Composites Drive Innovation

Polymers and composites contributed 52.14% to the automotive lightweight material market share in 2024, and their 6.23% CAGR to 2030 underscores an expanding role in structural and semi-structural parts. Carbon fiber reinforced plastics cut weight by 60% versus steel while holding stiffness, suiting performance-critical zones such as roof bows and battery trays. Glass fiber composites provide economical mass savings for door modules and hatch covers, whereas engineering plastics extend heat tolerance in power-electronic housings. This growth underscores why the automotive lightweight material market attracts sustained research and development in resin chemistry and fiber architecture.

Aluminum retains relevance through its mature recycling ecosystem and OEM familiarity. Magnesium promises even greater mass reduction for die-cast transmission cases, though supply-chain fragility tempers large-scale penetration. Titanium alloys inhabit niche exhaust and suspension parts because corrosion resistance justifies cost in high-temperature or salt-spray environments; the USD 867 million Cumberland County plant signals anticipated long-term demand[1]Cumberland County TN, “Titanium Project Announcement,” Cumberland County Government, cumberlandcountync.gov.

By Vehicle Type: Commercial Vehicles Accelerate

Light commercial vehicles show a 6.56% CAGR to 2030, the highest within the automotive lightweight material market, driven by electrified last-mile fleets under urban emissions caps. Weight savings translate directly into payload capacity and route efficiency, making premium materials economically sound. Passenger cars kept 62.23% share in 2024 but now treat lightweighting as table stakes rather than market differentiation. Heavy commercial trucks seek aluminum frame rails and composite roof panels that add freight space without exceeding axle limits. Chinese OEMs expanding in ASEAN are porting lightweight design rules into regional assembly plants, deepening material-demand diversity.

By Application: Body-in-White Leads Transformation

Body-in-white captured 31.56% of the automotive lightweight material market size in 2024 and is expanding at a 6.12% CAGR as OEMs front-load mass-reduction in primary structures. Tesla’s gigacasting strategy swaps 70 stamped parts for one aluminum casting, removing hundreds of welds and trimming curb weight. Chassis and suspension systems now adopt magnesium cross-members to cut unsprung mass, enhancing ride and range. Power-train subsystems increasingly feature composite heat shields that thrive in 900 °C zones without adding grams.

Interiors shift to natural-fiber and recyclate blends; BMW uses recycled PA6 in windscreen crossbeams to combine lightness with circular goals. Exterior skins benefit from thermoplastic olefin composites that allow Class-A paint finishes while permitting complex shapes. Battery enclosures provide the fastest emerging sub-segment because they demand fire resistance, electromagnetic shielding, and minimal weight, all under one roof of requirements.

Geography Analysis

Europe controlled 35.78% of the automotive lightweight material market in 2024, anchored by Germany’s vertically integrated carbon-fiber value chains. BMW’s single-source mandate on recycled carbon fiber enforces supply-quality discipline and cost compression. European carbon accounting assigns monetary value to embedded emissions, so recycled aluminum billets enjoy preferential procurement. The Euro 7 particulate cap on brake discs amplifies additive-manufactured gray-iron substitutes, which combine weight reduction with emissions control.

Asia-Pacific posts the fastest 7.12% CAGR, led by China’s EV output surge and Southeast Asia’s new assembly corridors. Government subsidies for local carbon-fiber plants in Jiangsu Province are scaling domestic capability, reducing import reliance[2]International Fiber Journal, “China Accelerates Carbon Fiber Production,” International Fiber Journal, fiberjournal.com. Japanese firms commercialize cellulose nanofiber composites compatible with mass-production cycle times, giving automakers a renewable option at a tolerable cost premium. Korean metallurgy labs deliver high-temperature alloys mitigating battery-thermal fatigue, reinforcing regional supply resilience. The automotive lightweight material market therefore advances quickly where policy, scale, and innovation intersect.

North America leverages its established recycling infrastructure: Novelis’s USD 4.1 billion Alabama plant will dedicate significant hot-mill capacity to automotive grades. Truck-centric model mixes reward lightweighting because every saved kilogram lifts payload and bottom-line revenue. CAFE tightening after 2024 adds contractual clauses requiring material suppliers to document Scope 1-3 emissions, nudging OEMs to align with circular-economy partners. Domestic titanium sponge projects, such as the Cumberland County facility, begin to insulate U.S. producers from external shocks.

Competitive Landscape

The automotive lightweight material market displays moderate fragmentation. Advanced high-strength steel remains concentrated among a handful of producers; Novelis, Alcoa, and Hydro dominate aluminum sheet. Composites, however, are distributed across many regional specialists, keeping barriers to entry moderate. Start-ups exploit white space in nano-architected lattices and structural battery casings, filing patents that fuse energy storage with load-bearing functionality. Traditional chemical groups position high-temperature resins with fast cure cycles, bridging the gap between lab success and line-speed reality.

Automotive Light Weight Material Industry Leaders

ArcelorMittal

Constellium group

Novelis

Thyssenkrupp AG

TORAY INDUSTRIES, INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: LyondellBasell unveiled its latest Schulamid ET100 product line, a lightweight polyamide tailored for automotive interior structural applications.

- April 2024: Hyundai Motor Group inked a deal with TORAY INDUSTRIES INC., to harness advanced materials, focusing on lightweight and high-strength attributes, for its eco-friendly, high-performance vehicles.

Global Automotive Light Weight Material Market Report Scope

| Metals | Aluminum |

| High-Strength Steel | |

| Magnesium Alloys | |

| Titanium Alloys | |

| Polymers and Composites | CFRP |

| GFRP | |

| Engineering Plastics | |

| Elastomers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Electric and Hybrid Vehicles |

| Body-in-White |

| Chassis and Suspension |

| Powertrain and Drivetrain |

| Interior Components |

| Exterior/Trim |

| Battery Enclosures and Thermal Systems |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Metals | Aluminum |

| High-Strength Steel | ||

| Magnesium Alloys | ||

| Titanium Alloys | ||

| Polymers and Composites | CFRP | |

| GFRP | ||

| Engineering Plastics | ||

| Elastomers | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Electric and Hybrid Vehicles | ||

| By Application | Body-in-White | |

| Chassis and Suspension | ||

| Powertrain and Drivetrain | ||

| Interior Components | ||

| Exterior/Trim | ||

| Battery Enclosures and Thermal Systems | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive lightweight material market?

The automotive lightweight material market size is USD 78.89 billion in 2025.

How fast is the automotive lightweight material market expected to grow?

It is projected to register a 5.88% CAGR and reach USD 104.98 billion by 2030.

Which material segment leads the automotive lightweight material market?

Polymers and composites lead with 52.14% share in 2024 and the fastest 6.23% CAGR through 2030.

Which region is growing quickest in the automotive lightweight material market?

Asia-Pacific is the fastest, expanding at a 7.12% CAGR due to rapid EV production scaling.

What application area commands the largest demand for lightweight materials?

Body-in-white structures hold 31.56% of demand and continue to grow at 6.12% CAGR.

Page last updated on: