Market Overview

| Study Period | 2020 - 2031 |

|---|---|

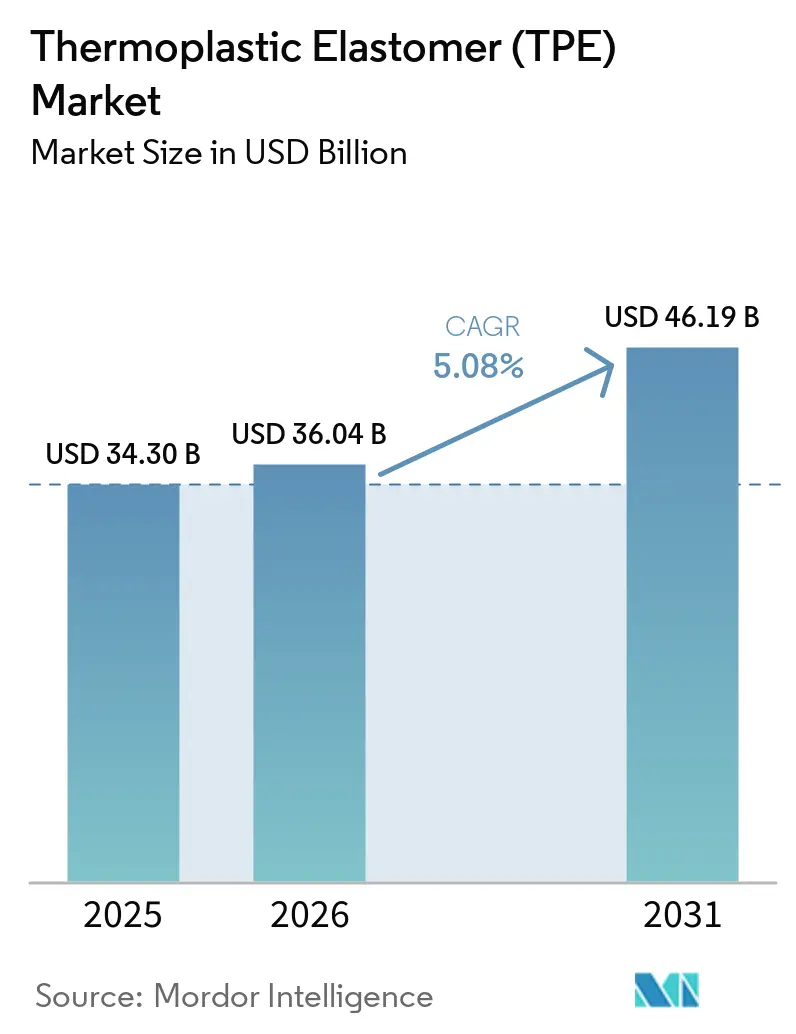

| Market Size (2026) | USD 36.04 Billion |

| Market Size (2031) | USD 46.19 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoplastic Elastomer (TPE) Market Analysis by Mordor Intelligence

The Thermoplastic Elastomer Market size in 2026 is estimated at USD 36.04 billion, growing from 2025 value of USD 34.30 billion with 2031 projections showing USD 46.19 billion, growing at 5.08% CAGR over 2026-2031. This advance highlights the material’s ability to combine rubber-like flexibility with thermoplastic processing efficiency, a combination now integral to vehicle electrification, next-generation medical devices, and circular manufacturing mandates. Producers are expanding regional capacity and introducing low-carbon, recycled-content grades to satisfy sustainability regulations and corporate net-zero targets. Asia-Pacific continues to anchor production and consumption thanks to its extensive automotive and electronics supply chains, healthcare investment, and policy support for electric vehicles. Healthcare modernization and the ongoing replacement of PVC and latex with biocompatible alternatives add another layer of momentum, while lighter wire harnesses and charging hardware in battery-electric cars further pull demand into high-margin formulations. Despite adipic-acid volatility and elevated machinery costs acting as brakes, the thermoplastic elastomers market retains a resilient growth profile as industries seek lighter, recyclable, and more design-flexible materials.

Key Report Takeaways

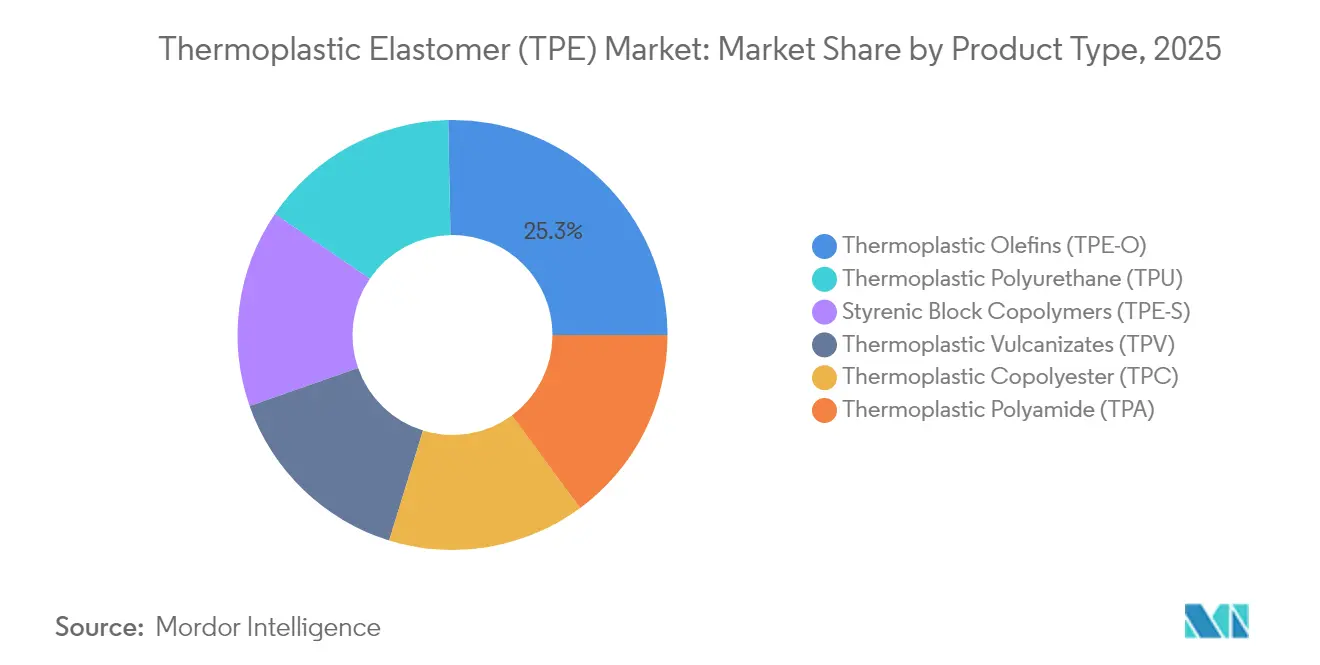

- By product type, thermoplastic olefins held 25.32% of the thermoplastic elastomers market share in 2025 and are set to advance at a 7.24% CAGR through 2031.

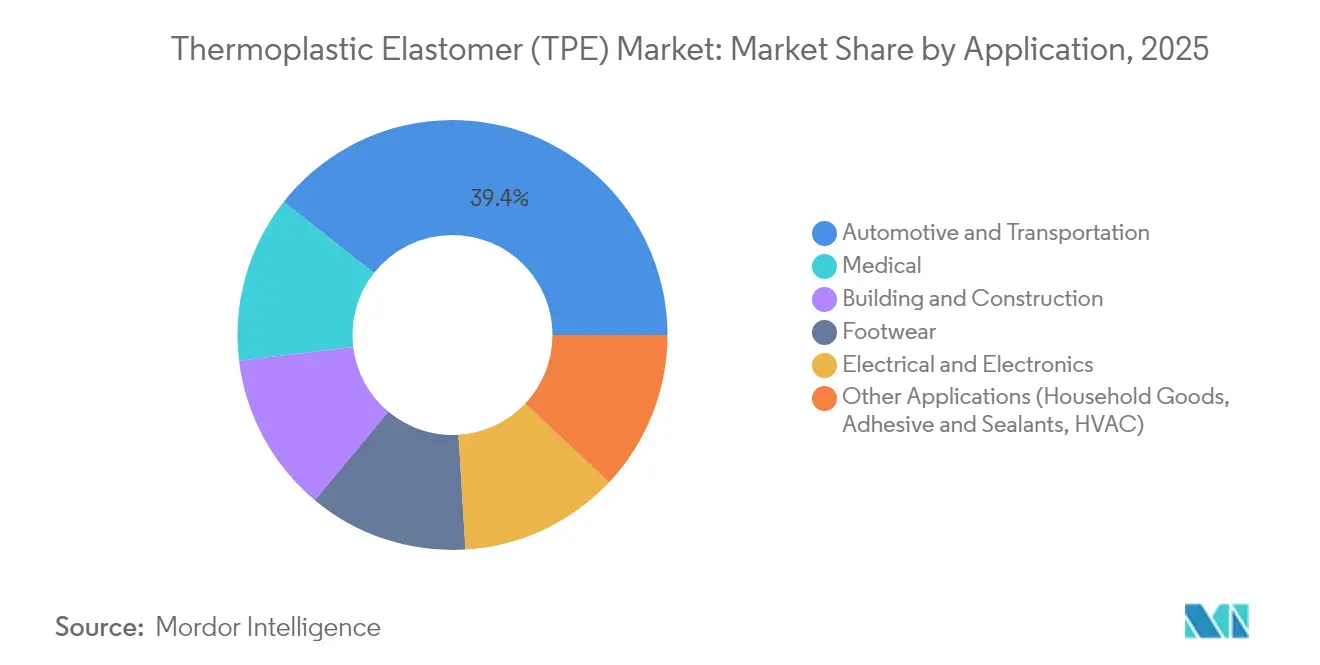

- By application, automotive and transportation commanded 39.38% of 2025 revenue, while medical devices are projected to expand at a 5.75% CAGR to 2031.

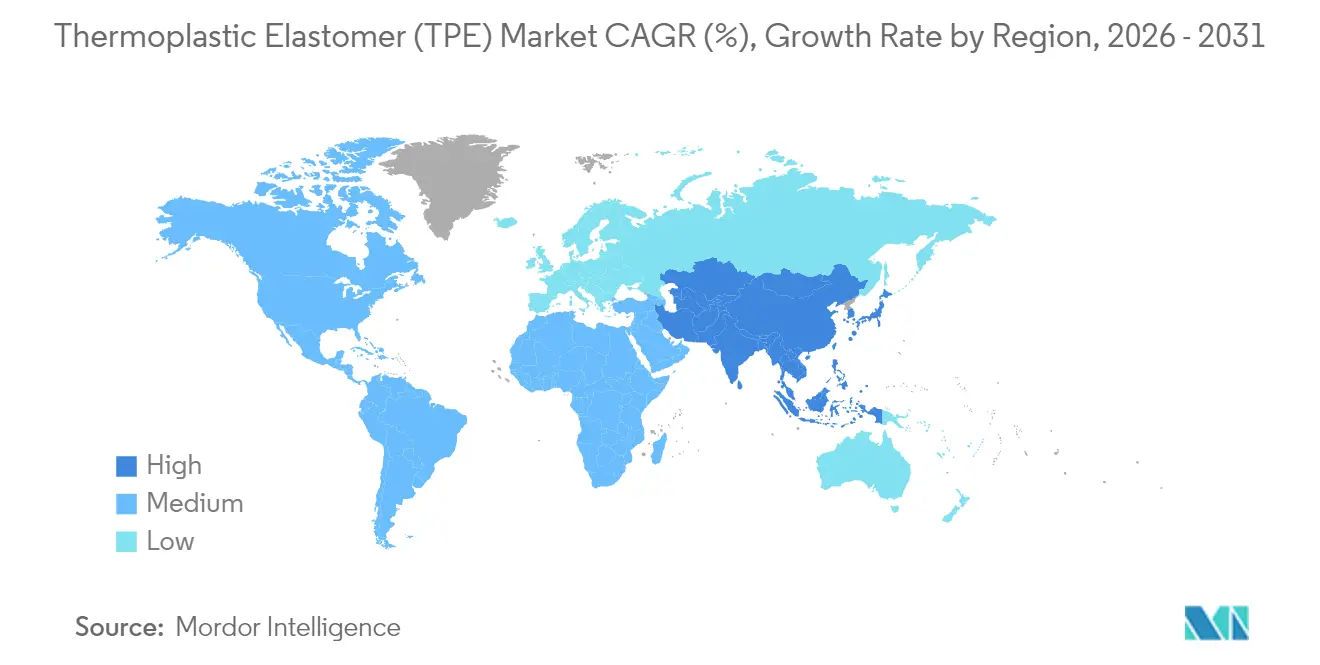

- By geography, Asia-Pacific TPE Market contributed 46.25% of the 2025 value and is forecast to progress at a 6.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermoplastic Elastomer (TPE) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Lightweighting Push in Automotive Wire and Cable | +1.2% | Global; China, Europe, North America focus | Medium term (2-4 years) |

| Growing Application in the Heating, Ventilation, and Air Conditioning (HVAC) Industry | +0.8% | North America & EU; expanding to APAC | Long term (≥ 4 years) |

| Increasing Utilization in Consumer Electronics | +0.9% | APAC core; spill-over worldwide | Short term (≤ 2 years) |

| Increasing Demand from Healthcare Industry | +1.1% | Global; premium markets | Medium term (2-4 years) |

| Substantial Demand from Footwear and Sports Equipment | +0.7% | Global; production in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Light Weighting Push in Automotive Wire and Cable

The electric vehicle revolution is fundamentally reshaping wire and cable specifications, with thermoplastic elastomers emerging as critical enablers of weight reduction and performance optimization. Celanese’s Hytrel TPC-LCF delivers a 50% carbon-footprint cut while enduring −40 °C to 130 °C, illustrating how polymeric jacketing helps reduce harness weight in electric vehicles[1]Celanese Corporation, “Hytrel TPC-LCF Material Launch,” celanese.com. Cross-linked polyolefins now displace silicone in high-voltage lines, providing abrasion resistance that shortens routing paths and trims copper usage. Asia-Pacific, led by Chinese OEMs, dominates EV output, so local compounders secure volume growth first. TPE jacketing is also moving into onboard charging pads and coolant tubes, lifting average polymer content per vehicle and magnifying revenue inside the thermoplastic elastomers market.

Growing Application in the Heating, Ventilation, and Air Conditioning (HVAC) Industry

Heat-pump adoption and new refrigerants intensify sealing and vibration requirements. TE Connectivity cites lifetime reliability as a procurement benchmark, spurring substitution of EPDM with higher-temperature TPEs in gaskets and hose liners. DSM’s Arnitel HT permits single-piece hot-air ducts, cutting weight 40% and part cost 50%, a direct gain for installers targeting energy-efficient retrofits. Digitally controlled compressors also need flexible mounts that dampen noise while hosting sensors, a niche well served by specialty TPE compounds in the thermoplastic elastomers market.

Increasing Utilization in Consumer Electronics

Device brands value soft-touch aesthetics, drop resistance, and tight tolerances. SABIC and Lubrizol’s LNP-ESTANE ECO blends embed bio-based content yet remain color stable during over-molding of laptop lids. KRAIBURG TPE’s Light Effect line allows uniform ambient back-lighting for premium earbuds and watches without UV yellowing. As form factors shrink, gasket walls thin to sub-0.5 mm, motivating designers to choose grades with high flow and low compression set. Asia-Pacific fabs capture first-mover volume, reinforcing the thermoplastic elastomers market’s regional skew.

Increasing Demand from Healthcare Industry

Biocompatibility rules drive hospitals away from phthalates and latex. Teknor Apex tubing grades resist spallation, support gamma, EtO, and steam sterilization, and extend pump life in infusion systems. KRAIBURG TPE’s THERMOLAST M range, Shore 00 30–50, mimics human tissue, increasing wearer comfort in prosthetics. Single-use diagnostics and advanced wound care further expand volumes, securing medical’s role as the fastest-growing slice of the thermoplastic elastomers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermoplastic Polyurethane (TPU) Price Volatility Due to Adipic Acid Supply | −0.9% | Global; import-dependent regions harder hit | Short term (≤ 2 years) |

| High Manufacturing and Equipment Cost | −0.7% | Global; emerging markets sharper impact | Medium term (2-4 years) |

| Challenges of 3D Printing with Soft Thermoplastics | −0.4% | Developed manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Thermoplastic Polyurethane (TPU) Price Volatility Due to Adipic Acid Supply

Raw material cost inflation is creating significant margin pressure across the Thermoplastic Polyurethane (TPU) value chain, with adipic acid supply constraints representing a critical bottleneck that affects pricing stability and production planning. BASF raised butanediol derivative prices, amplifying cost swings for TPU makers [2]BASF, “Price Adjustments for BDO and Derivatives,” basf.com. Kraton implemented a USD 330 t increase on SIS, signifying parallel inflation across block copolymers. When petroleum feedstocks spike and logistics falter, converters face slimmer spreads, prompting some Original Equipment Manufacturers (OEMs) to defer non-critical projects that rely on TPU inside the thermoplastic elastomers market.

High Manufacturing and Equipment Cost

Capital equipment investments required for Thermoplastic Elastomer (TPE) production are creating barriers to market entry and constraining capacity expansion, particularly as manufacturers face elevated interest rates and uncertain demand conditions. Two-component injection presses and precision twin-screw extruders can top USD 5 million, stretching payback periods. A survey of North American processors shows 66% intend machinery upgrades but many favor retrofits to curb outlay. Skilled labor shortages raise commissioning risk, especially in Southeast Asia, thereby slowing new-capacity rollouts in the thermoplastic elastomers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: TPE-O Dominates Through Versatility

Thermoplastic olefins led with 25.32% 2025 revenue and are forecast to post the segment-best 7.24% CAGR through 2031, sustaining the largest slice of the thermoplastic elastomers market size at segment level. Automakers rely on TPE-O for bumper fascia, air-dam seals, and under-body panels because the blends bond readily with polypropylene substrates and resist weathering. Construction profiles and consumer goods add volume, especially where cost targets favor PP-based alloys.

TPU holds the number-two spot by value, favored for abrasion-critical uses in athletic shoes, conveyor belts, and catheter jacketing. Growth momentum remains tempered by adipic-acid price instability, yet high value-added niches preserve margins. TPV follows closely in under-hood air-management parts that must tolerate 140 °C peaks. Styrenic block copolymers keep share in adhesives and disposable razors, while TPC and TPA extend reach into drive belts, pneumatic tubing, and charge-air ducts. Specialty compounding, such as Teknor Apex’s Sarlink TPV for EV battery seals, demonstrates how formulation know-how unlocks premium pricing within the thermoplastic elastomers market.

By Application: Medical Growth Outpaces Automotive Leadership

Automotive and transportation accounted for 39.38% of 2025 sales, anchoring the thermoplastic elastomers market size by end use. Battery-electric cars intensify demand for low-density vibration isolators, cable jackets, and flexible cooling hoses. Sensor housings for advanced driver-assistance systems also deploy UV-stable TPE over-molds to shield electronics from road debris.

Medical is projected to grow at 5.75% CAGR through 2031, the fastest pace among segments. Disposable IV sets, syringe plungers, and dialysis tubing all pivot toward clear, PVC-free TPE grades as hospitals target safer material profiles. Building and construction relies on TPE flashing tape and insulated window seals, adding resilience to an otherwise cyclical sector. Electrical and electronics exploit dielectric strength and colorability to streamline smart-device assembly. Footwear brands pursue high-rebound, low-density midsoles that enable weight-neutral design. Small but lucrative niches, such as soft-grip toothbrush handles, round out a diversified demand map that stabilizes earnings across the thermoplastic elastomers market.

Geography Analysis

Asia-Pacific claimed 46.25% of 2025 value, the highest thermoplastic elastomers market share among regions, and is on course for a 6.34% CAGR to 2031. China represents the fulcrum, producing nearly one in three vehicles globally and hosting expansive smartphone and appliance clusters. INVISTA’s move to double Nylon 6,6 capacity to 400,000 t/y in Shanghai underscores raw-material self-sufficiency that underpins compounder growth. South Korea supplies display and battery components, while India escalates wire-and-cable builds for renewable energy, sustaining intra-regional trade.

North America remains innovation-heavy in the TPE Market. Detroit OEMs specify bio-based TPV window seals, and Boston-area medical device startups pilot new catheter coatings, locking in profitable niches. Celanese’s Hytrel TPC-LCF, launched at Chinaplas yet developed in Texas, achieves a 50% carbon-footprint cut, aligning with US Inflation Reduction Act incentives. Tariffs on petrochemical imports, effective 2025, could add 12-20% to resin costs, nudging compounders to reshore intermediate production and potentially opening capacity for domestic TPU lines.

Europe’s environmental directives accelerate uptake of recycled-content TPEs such as Avient’s reSound REC GP 7820, which contains 60% post-consumer feedstock . German Tier 1s test TPV radiator hoses that meet Euro 7 cold-start requirements. Meanwhile, Spain and Italy deploy heat-pump retrofits that use Arnitel HT ducting to meet decarbonization targets. South America and the Middle East & Africa are smaller today yet offer long-run upside as infrastructure expands. Mexico is now the world’s fourth-largest polyurethane market, reflecting near-shoring of US automotive supply chains and drawing TPU injection molders closer to OEMs. Gulf Cooperation Council countries invest in specialty elastomer hubs to diversify away from crude exports, hinting at localized downstream demand within the thermoplastic elastomers market.

Competitive Landscape

The thermoplastic elastomers market is moderately consolidated. Exxon Mobil Corporation, Kraton Corporation, and LG Chem leverage integrated feedstock positions to buffer price swings and ensure allocation priority. Exxon Mobil’s Vistamaxx line keeps visibility in hygiene films, while Kraton optimizes hydrogenated styrene-isoprene block copolymers for adhesive tack. LG Chem channels naphtha crackers into metallocene-catalyzed TPO grades that court OEMs seeking low-VOC interiors.

Thermoplastic Elastomer (TPE) Industry Leaders

Exxon Mobil Corporation

Arkema

LG Chem

LyondellBasell Industries Holdings B.V.

Kraton Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Teknor Apex expanded its partnership with Nexeo Plastics to enhance material offerings in the EMEA (Europe, the Middle East, and Africa) region, including advanced thermoplastic elastomers like Monprene TPE and Sarlink TPV.

- October 2024: Avient Corporation launched new recycled-content thermoplastic elastomers at Fakuma 2024, featuring up to 60% post-consumer recycled content in the reSound REC GP 7820 TPEs (Thermoplastic Elastomers), aimed at reducing carbon footprints compared to virgin thermoplastic elastomers.

Global Thermoplastic Elastomer (TPE) Market Report Scope

Thermoplastic elastomers are a class of copolymers or a physical mix of polymers consisting of materials with both thermoplastic and elastomeric properties. TPE is used for mobile phone components, cables, plugs, and sockets due to its electrical resistance and ability to be molded. TPE is used for shoe soles, scuba flippers, and ski pole handles due to its flexibility, wear resistance, and UV stability. Product type, applications, and geography segment the thermoplastic elastomer market. By product type, the market is segmented into a styrene block copolymer, thermoplastic olefin, elastomeric alloy, thermoplastic polyurethane, thermoplastic copolyester, and thermoplastic polyamide. By application, the market is segmented into automotive & transportation, building & construction, footwear, electrical & electronics, medical and other applications. The report also covers the market size and forecasts for the TPE market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (kilo tons).

By Product Type

| Styrenic Block Copolymers (TPE-S) |

| Thermoplastic Olefins (TPE-O) |

| Thermoplastic Vulcanizates (TPV) |

| Thermoplastic Polyurethane (TPU) |

| Thermoplastic Copolyester (TPC) |

| Thermoplastic Polyamide (TPA) |

By Application

| Automotive and Transportation |

| Building and Construction |

| Footwear |

| Electrical and Electronics |

| Medical |

| Other Applications (Household Goods, Adhesive and Sealants, HVAC) |

By Geography

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Styrenic Block Copolymers (TPE-S) | |

| Thermoplastic Olefins (TPE-O) | ||

| Thermoplastic Vulcanizates (TPV) | ||

| Thermoplastic Polyurethane (TPU) | ||

| Thermoplastic Copolyester (TPC) | ||

| Thermoplastic Polyamide (TPA) | ||

| By Application | Automotive and Transportation | |

| Building and Construction | ||

| Footwear | ||

| Electrical and Electronics | ||

| Medical | ||

| Other Applications (Household Goods, Adhesive and Sealants, HVAC) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the thermoplastic elastomers market?

The market is valued at USD 36.04 billion in 2026 and is projected to reach USD 46.19 billion by 2031.

Which product type leads the thermoplastic elastomers market?

Thermoplastic olefins hold 25.32% 2025 revenue and register the fastest 7.24% CAGR through 2031.

Why are thermoplastic elastomers gaining traction in electric vehicles?

They enable lightweight wire jackets and flexible battery seals while offering lower carbon footprints than legacy rubber alternatives.

Which application is growing fastest?

Medical devices post the highest 5.75% CAGR as hospitals shift from PVC and latex to sterilizable, biocompatible TPE solutions.

How dominant is Asia-Pacific in this market?

Asia-Pacific accounts for 46.25% of 2025 revenue and is forecast to expand at a 6.34% CAGR to 2031, powered by automotive and electronics manufacturing.

Page last updated on: