Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

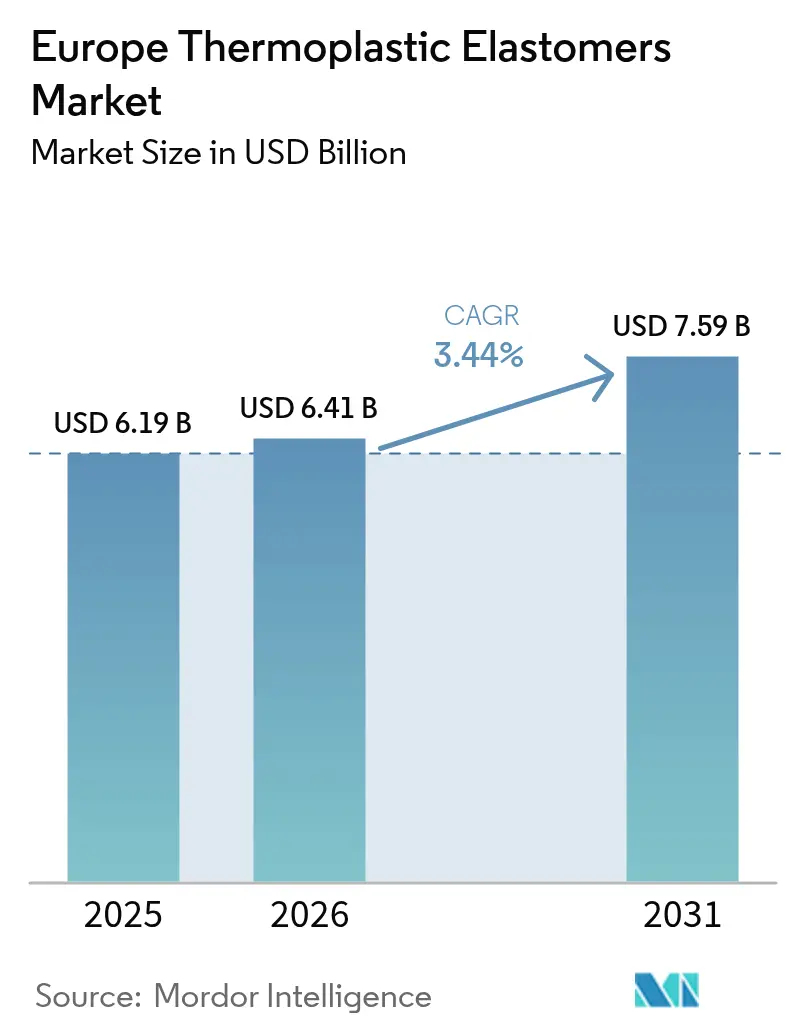

| Base Year Market Size (2025) | USD 6.19 Billion |

| Market Size (2026) | USD 6.41 Billion |

| Market Size (2031) | USD 7.59 Billion |

| Growth Rate (2026 - 2031) | 3.44% CAGR |

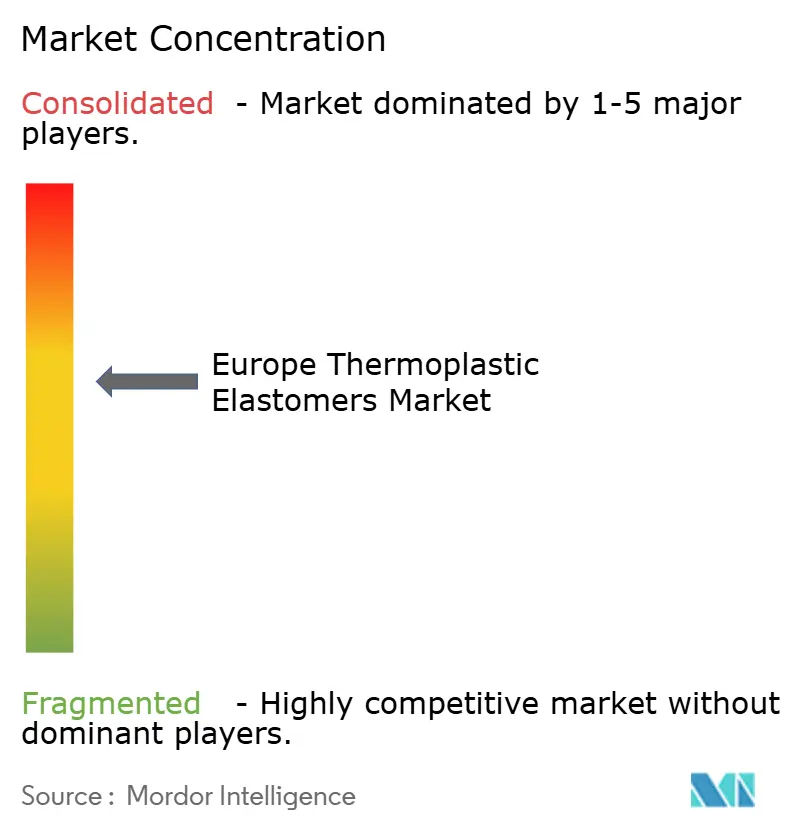

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Thermoplastic Elastomers Market Analysis by Mordor Intelligence

The Europe Thermoplastic Elastomers Market size was valued at USD 6.19 billion in 2025 and estimated to grow from USD 6.41 billion in 2026 to reach USD 7.59 billion by 2031, at a CAGR of 3.44% during the forecast period (2026-2031). Moderate expansion reflects a mature demand base in the automotive, construction, and consumer goods sectors, yet three structural catalysts continue to drive volumes upward. First, vehicle electrification is pushing OEMs to cut component weight and convert rubber and metal parts to recyclable TPEs. Second, green-building programs are rewarding halogen-free, low-VOC sealing products, tilting specifications away from PVC and EPDM. Third, closed-loop mandates under the revised End-of-Life Vehicles Directive are creating a defined premium for grades containing 50% or more post-consumer content. Integrated petrochemical producers maintain a cost edge through captive production of styrene and butadiene, but specialty compounders are winning orders in medical, electronics, and e-mobility niches where biocompatibility, flame retardancy, or high recycled content take precedence over price.

Key Report Takeaways

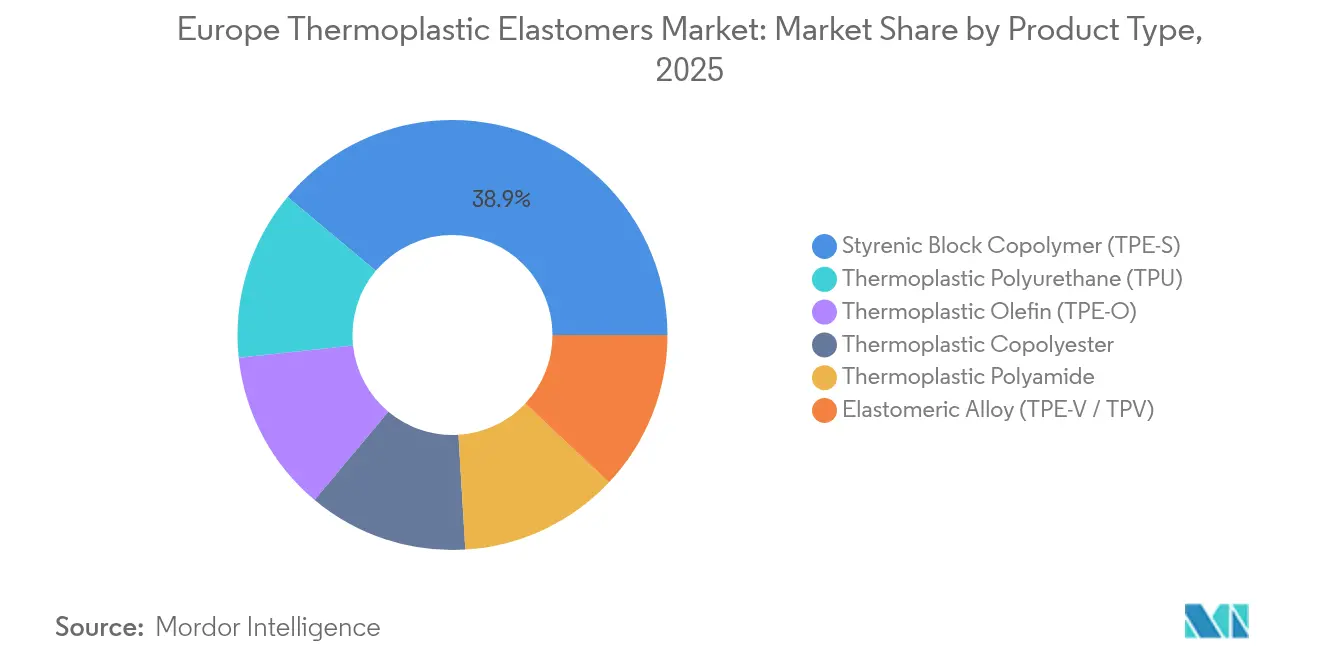

- By product type, styrenic block copolymers led with a 38.92% share of the Europe thermoplastic elastomers market in 2025. Thermoplastic polyurethanes are forecast to expand at a 3.56% CAGR through 2031, the fastest rate among product types.

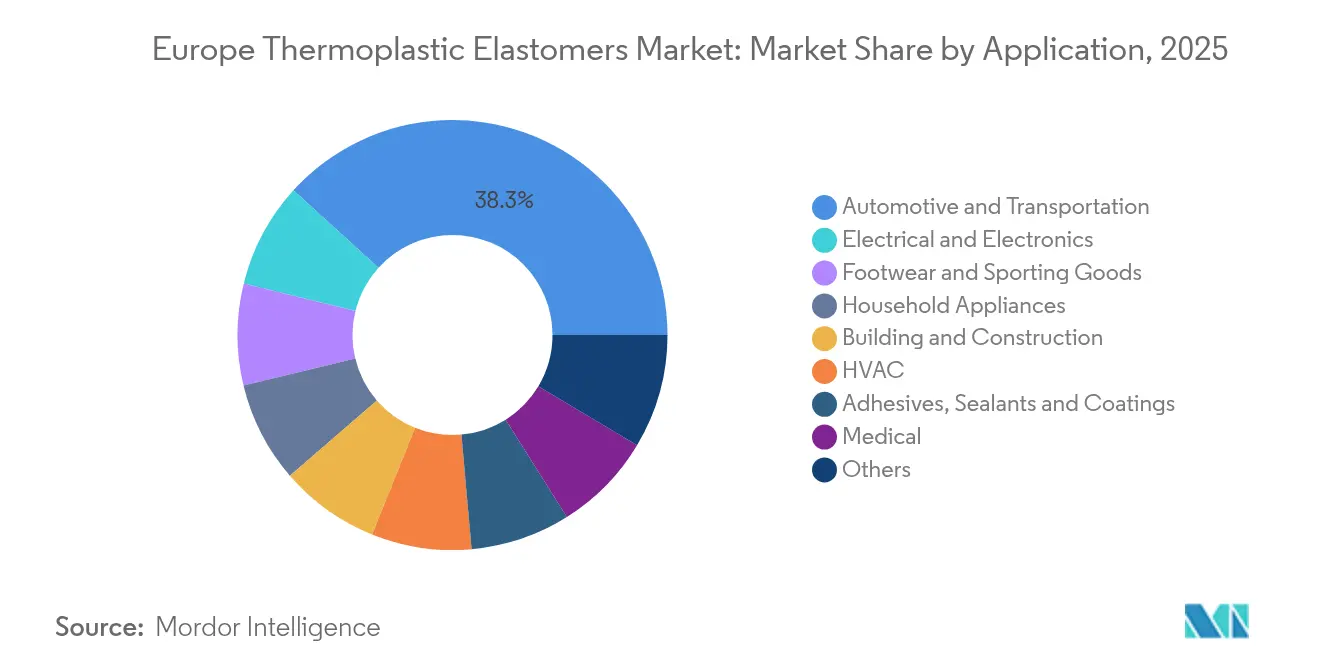

- By application, automotive and transportation accounted for 38.25% of demand in 2025, while electrical and electronics are projected to advance at a 3.66% CAGR through 2031.

- By geography, Germany held 44.10% of the Europe thermoplastic elastomers market size in 2025; the Rest of Europe cluster is predicted to grow at a 3.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Thermoplastic Elastomers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-driven lightweighting boom in European auto parts | +0.9% | Germany, France, Spain; spillover to Poland, Czech Republic | Medium term (2-4 years) |

| Rapid substitution of Polyvinyl Chloride and EPDM in building seals | +0.7% | Germany, UK, Nordic countries | Long term (≥ 4 years) |

| Medical-grade Thermoplastic-Urethane demand from catheter extruders | +0.5% | Germany, Ireland, Switzerland | Short term (≤ 2 years) |

| Foam-injection TPE for low-density interior trims | +0.4% | Germany, France, Italy | Medium term (2-4 years) |

| OEM take-back mandates fueling PCR-blend TPE usage | +0.6% | EU-wide, strongest in Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Driven Lightweighting Boom in European Auto Parts

Electric-vehicle architectures must shed 15-20% of their mass to counterbalance the weight of the battery, so OEMs are revising their material lists to favor recyclable thermoplastic elastomers over die-cast metal and vulcanized rubber. Volkswagen specifies Santoprene TPV engine covers that save 30% versus EPDM while handling 120°C oil exposure[1]ExxonMobil Chemical, “Santoprene TPV for electric vehicles,” exxonmobilchemical.com. Continental AG co-developed foam-injection TPE door seals, weighing 200 g less per vehicle. This seemingly small figure translates to 400 t of annual weight reduction at Wolfsburg volumes. In France and Spain, Stellantis and Renault source localized TPE gaskets to meet EU Battery Regulation carbon footprint thresholds of below 50 kg CO₂e/kWh by 2027. ISO 14040 life-cycle audits now influence sourcing decisions, prompting smaller compounders to consider mergers that can finance traceability systems.

Rapid Substitution of PVC and EPDM in Building Seals

Window and door makers across Germany and the Nordics are transitioning to TPE profiles to meet the requirements of DGNB Gold and BREEAM Excellent labels, which penalize the use of halogenated polymers. TPE-S and TPE-V retain elongation above 200% after 5,000 hours of xenon-arc testing per ISO 4892-2, matching the weatherability of PVC without plasticizer bleed. The UK Future Homes Standard, effective from 2025, requires airtightness of below 5 m³/h/m² at 50 Pa; co-extruded TPE corner keys meet this target while reducing installation time by 15 minutes per unit. Rehau and Deceuninck incorporate 40-50% post-industrial regrind, adding circularity that cushions EPDM price swings. The forthcoming EU Construction Products Regulation Annex ZA will require Environmental Product Declarations, thereby accelerating the uptake of TPE among facade contractors in Frankfurt and Amsterdam.

Medical-Grade TPU Demand from Catheter Extruders

European catheter manufacturers are transitioning away from plasticized PVC to comply with the EU MDR 2017/745 and ISO 10993 biocompatibility standards, which restrict the use of phthalates. Polycarbonate-based TPU offers kink resistance and thromboresistance that allow tubing downsizing from 7 Fr to 5 Fr without flow loss, a key benefit in pediatric cardiology. Ireland’s Galway cluster consumed 1,200 tons of medical TPU in 2024, favoring suppliers with ISO 13485-certified lines and full resin lot traceability for FDA 510(k) filings. The Commission’s plan to ban all phthalates in medical devices by 2026 will erase PVC’s last foothold in long-wear catheters, boosting TPU volumes by double digits in the near term.

Foam-Injection TPE for Low-Density Interior Trims

Foam-injection molding reduces TPE panel density to 0.5-0.7 g/cm³, resulting in a 25-30% mass reduction compared to solid parts, while maintaining Class-A finishes. Borealis and BASF codeveloped a nitrogen-foamed TPE-O that satisfies Volkswagen TL 52340 VOC limits below 50 µg/g at 65°C. Premium EVs, such as the BMW iX and Mercedes-Benz EQS, specify foamed TPE for armrests, shaving 1.5 kg per vehicle and adding kilometers to the driving range. Machine builders Arburg and Engel offer turnkey cells with closed-loop density control, letting Italian and Spanish tier-2s bid on local EV programs. ISO 3795 flammability compliance and micro-CT cell uniformity testing, as per ASTM D6226, are now standard quality gates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-linked styrene and isocyanate prices | -0.6% | EU-wide, acute in import-dependent markets (Italy, Spain) | Short term (≤ 2 years) |

| Tight EU REACH limits on phthalates and styrene monomer | -0.4% | Germany, France, Benelux | Medium term (2-4 years) |

| Competition from high-temp silicones in e-mobility | -0.3% | Germany, France, Sweden | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Linked Styrene and Isocyanate Prices

When Brent shifts more than USD 20/bbl inside a quarter, styrene and butadiene follow naphtha spreads almost in lockstep, driving feedstock costs that represent up to 60% of TPE-S production[2]ICIS, “Styrene monomer price trends,” icis.com. Spot styrene in Northwest Europe slid 21% from USD 1,400/t in January 2024 to USD 1,100/t by October, pinching margins for integrated players such as INEOS Styrolution, which idled lines at Antwerp during summer maintenance. A BASF force-majeure event on MDI in Q2 2024 inflated isocyanate prices by 18% and left TPU extruders with six-week lead times. Smaller compounders that lack hedge tools or captive feedstocks surrendered 200-300 bps margin, pushing more family-owned plants into private-equity roll-ups.

Tight EU REACH Limits on Phthalates and Styrene Monomer

ECHA restricted DEHP, DBP, BBP, and DIBP to concentrations above 0.1 wt% in consumer goods as of 2020; however, recyclate contamination still triggers costly GC-MS screening for inbound PCR streams. Draft Annex XVII rules would halve workplace styrene limits to 50 ppm, forcing closed-loop reactors with a EUR 5-10 million capital expenditure per line—out of reach for mid-tier Italian and Spanish TPE-S firms. Germany’s BAuA classified styrene as a suspected carcinogen in 2024, prompting enhanced PPE audits at supplier sites. OEMs are now auditing ventilation and emission systems as part of ISO 14001 supplier approvals, driving a flight to larger, better-capitalized compounders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Styrenic Base, Polyurethane Upswing

Styrenic block copolymers held 38.92% of the Europe thermoplastic elastomers market in 2025, underpinning formulations for adhesives, footwear, and soft-touch appliance parts. Thermoplastic polyurethanes are projected to post a 3.56% CAGR to 2031, increasing their share of the European thermoplastic elastomers market size as medical and premium automotive customers value abrasion and oil resistance at 80+ Shore A hardness levels. Thermoplastic olefins remain staples for exterior fascias due to their paintability without primers; however, Asian imports price them 10-15% below European output, thereby trimming margins for local producers.

Elastomeric alloys, positioned as TPVs, dominate under-hood seals that must limit oil swell to 15% per ASTM D471; however, silicone rivals are eroding their share in e-powertrain gaskets that require continuous use above 150 °C. Copolyesters and polyamide elastomers address high-temperature tubing niches, but they face hurdles related to moisture sensitivity and processing costs. ISO 1629 labeling has stripped away trade-name lock-in, letting procurement teams switch suppliers rapidly and sparking price pressure across the Europe thermoplastic elastomers market.

By Application: Automotive Foundation, Electronics Momentum

Automotive retained 38.25% share of the Europe thermoplastic elastomers market size in 2025 on the strength of weather seals, interior skins, and underbody shields that migrate well from combustion to electric platforms. Yet platform simplification and cost-down targets limit incremental growth to low single digits. Electrical and electronics, in contrast, is forecast to expand at a 3.66% CAGR through 2031 as data-center cable systems specify halogen-free, UL 94 V-0 TPE jackets that pass flame tests and release minimal toxic gas during fire events.

Building and construction applications benefit from green-building schemes that penalize halogenated materials, although sluggish new housing starts in Germany and France keep absolute volumes from surging. Medical devices, though still a small slice, command Europe thermoplastic elastomers market prices 2-3× higher than commodity grades; the segment enjoys a structural lift from PVC phase-out in long-term implantables. Footwear and sporting goods swing with consumer spending, while household appliances and HVAC absorb steady, policy-driven demand for gaskets and vibration dampers that support higher energy-efficiency ratings.

Geography Analysis

Germany anchored 44.10% of the Europe thermoplastic elastomers market in 2025, buoyed by Volkswagen Group, BMW, Mercedes-Benz, and Audi, and by integrated chemical hubs at Ludwigshafen, Leverkusen, and Marl. The country’s Mittelstand compounders—40-50 firms with EUR 20–200 million turnover—supply niche formulations for ski-boot liners, medical tubing, and bio-based automotive trim, leveraging rapid prototyping to outflank multinationals on service. France and the United Kingdom trail, supported by automotive production in Grand Est and the West Midlands, although customs frictions post-Brexit have triggered TPE capacity shifts to Poland and the Czech Republic to safeguard duty-free flows into EU vehicle plants.

Italy consumes sizable volumes in its Montebelluna footwear district and Lombardy appliance corridor, while Spain’s Valencia and Catalonia regions deploy TPE seals and trim in vehicles and white goods. The Rest-of-Europe cluster—comprising Poland, the Czech Republic, Hungary, Romania, and the Nordics—will grow at a 3.69% CAGR, as German OEMs onshore EV component lines in the East and wind farm build-outs in Denmark and Sweden demand low-temperature-rated cable jackets. Iberia’s emergence as a battery-cell hub adds localized demand for high-temperature gaskets, with PowerCo and Stellantis-TotalEnergies specifying locally compounded TPEs to cut logistics emissions and comply with EU taxonomy screens.

Value Chain Analysis

The Europe thermoplastic elastomers (TPE) value chain starts with feedstocks such as styrene, butadiene, propylene, and isocyanates sourced from European petrochemical hubs. These feedstocks flow into polymerization and compounding, where formulations are tuned for automotive seals and trims, building profiles, medical tubing, and electrical and electronics cable and connector applications. Integrated producers tend to preserve cost and supply advantages during crude-linked volatility, while specialty compounders differentiate through application engineering (VOC control, PP bonding, biocompatibility, flame retardancy) and through recycled-content compounding aligned with OEM circularity requirements.

Downstream, processors (injection molders, extruders, profile makers, and film/lamination specialists) convert TPEs into components that move through tier suppliers and distributors into OEM supply chains across automotive, construction, appliances, and medical devices. Trade bodies such as PlasticsEurope and EuPC operate alongside industry platforms such as the Circular Plastics Alliance, which coordinate workstreams including design-for-recyclability and recycled-content use and influence grade selection and qualification. The chain also reflects regional production and logistics choices, with established nodes in Western Europe and expanding compounding and converting capacity in Central and Eastern Europe to shorten lead times for vehicle and industrial customers and reduce logistics exposure.

Competitive Landscape

The European Thermoplastic Elastomer market is partially consolidated. Integrated giants exploit captive styrene, butadiene, and isocyanate to defend their margins against volatility, while mid-sized specialists carve out a share through high PCR content, color-match sampling in two weeks, and application engineering support that includes mold-flow simulation. Bio-based chemistries are the next frontier: Arkema and Evonik are piloting castor-oil and tall-oil TPEs that meet 50% renewable carbon thresholds, but these cost 20-30% more than their petro-variants.

Europe Thermoplastic Elastomers Industry Leaders

Covestro AG

KRATON CORPORATION

BASF

LyondellBasell Industries Holdings B.V.

Arkema

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory and OEM circularity requirements open room for high recycled-content and traceable TPE compounds in European automotive and transportation, where specifications increasingly favor thermoplastic, recyclable alternatives to thermoset rubbers for seals, gaskets, and interior skins. In February 2026, Council of the European Union documents on the End-of-Life Vehicles Regulation explicitly defined plastics to include elastomers that can be processed as thermoplastics, which clarifies the compliance pathway for TPE-based solutions and supports demand for PCR-ready formulations that can pass quality screening and lot traceability audits.

Opportunities also extend into specialty grades tied to electrification and electronics, including low-VOC interior materials and high-performance cable and film solutions. Capacity and go-to-market moves provide direct signals of positioning: ExxonMobil completed an expansion at Newport, Wales that doubled manufacturing capacity for specialty elastomers and lifted global Santoprene TPE capacity by 25%, and SK Chemicals appointed Omya Performance Polymer Distribution as a European distributor for its SKYPEL TPE-E in June 2026 to broaden reach in the UK, Ireland, Benelux, and Scandinavia. In parallel, EU-backed R&D supports next-generation recyclable elastomer chemistries, with the European Commission-funded REPurpose project active as of April 2026 to develop recyclable elastomeric polymers using biomass-derived building blocks and enzymatic degradation concepts that target end-of-life constraints limiting adoption in some applications.

Recent Industry Developments

- June 2026: Kraton published technical documentation describing a new SEBS-based solution for modifying engineering thermoplastics to improve impact resistance and stiffness. The work supports compounders seeking higher-performance TPE-S/SEBS formulations for durable goods and automotive-adjacent uses where mechanical property retention and processability affect material selection.

- September 2025: Kraiburg TPE introduced a sustainable Thermolast R range developed for e-bike handle applications in Germany. The launch broadened access to circularity-oriented TPE options for consumer mobility components, a segment where grip feel, durability, and sustainability claims matter.

- January 2025: Bjoern Thorsen A/S became a distributor for Celanese thermoplastic elastomers across Europe. The agreement strengthened Celanese grade channel access and increased support for customized solutions, which can shorten qualification cycles for converters and OEM suppliers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers thermoplastic elastomer materials sold in Europe, measured in value terms, and used across major end uses where flexible and rubber-like performance is needed with thermoplastic processing.

Scope exclusions: We exclude finished parts and assemblies made from these materials and only count the material market value at the point of sale of the resin or compound.

Segmentation Overview

- By Product Type

- Styrenic Block Copolymer (TPE-S)

- Thermoplastic Olefin (TPE-O)

- Elastomeric Alloy (TPE-V / TPV)

- Thermoplastic Polyurethane (TPU)

- Thermoplastic Copolyester

- Thermoplastic Polyamide

- By Application

- Automotive and Transportation

- Building and Construction

- Footwear and Sporting Goods

- Electrical and Electronics

- Medical

- Household Appliances

- HVAC

- Adhesives, Sealants and Coatings

- Others

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public datasets that help anchor the plastics and elastomers value chain in Europe, and then we narrowed down to thermoplastic elastomer specific signals. We reviewed sources such as Eurostat for industrial output and trade direction, customs and tariff chapter statistics where polymers and compounds are visible, and European Chemicals Agency materials that clarify compliance pressure and substitution trends.

To keep inputs grounded, we also used industry association releases and technical papers, such as those from plastics and rubber federations, peer reviewed polymer journals, and publicly available recycling and end of life policy documents. Company filings, investor presentations, and reputable press were used to validate capacity additions, product mix comments, and any plant related changes. Where needed, we referenced paid subscriptions for company financials and intelligence, patent databases, and shipment level import and export checks to confirm directionally whether volume and price movements were consistent. These examples are not exhaustive, and many other public sources were used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on conversations and structured surveys with material producers, compounders, distributors, and large end users across automotive, building and construction, medical, and electrical applications in Europe. We used this step to confirm what buyers are actually sourcing as TPE in local procurement, to stress test price ranges, and to align the demand outlook by country clusters and end use.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | |

| Mid tier: 60% | Functional/Unit leaders: 32% | |

| Smaller Players: 15% | Managers: 54% |

Market-Sizing & Forecasting

The core sizing logic was built using a top-down approach where polymer demand in Europe is reconstructed by end use industries and then translated into thermoplastic elastomer consumption using penetration rates and substitution patterns for each application. Where the data was less clean, the numbers were corroborated with selective bottom-up checks, such as sampled supplier and distributor revenue splits, typical ASP by chemistry, and estimated volume by major end uses before totals were adjusted.

Key inputs that guided the model included automotive and transportation production trends, lightweighting and recyclability adoption signals, construction activity indicators tied to sealing and insulation demand, and medical and electronics output direction where specialty grades are used. We also tracked mix shifts across common material families, including styrenic block copolymers, thermoplastic olefins, and thermoplastic polyurethanes, since pricing and growth can differ by chemistry. Forecasts were prepared using scenario analysis, where the base case was aligned to expert expectations on vehicle build plans, renovation intensity, and compliance driven material changeovers, and then stress tested for energy cost swings and slower industrial output.

When a bottom-up roll up could not cover all countries or channels, gaps were handled by applying validated ratios from comparable markets in Europe, followed by a reconciliation back to the total demand pool so the final numbers stayed realistic.

Data Validation & Update Cycle

Validation was done in layers so that major errors can be caught early and small drifts can be corrected before sign off. Model outputs were checked against independent signals like trade direction, plant utilization commentary, and pricing movement seen across common polymer benchmarks, and then outliers were reviewed to understand whether they came from scope, timing, or unit conversion issues.

If a variance remained material after internal review, the assumptions were taken back to select interviewees for a quick re check and clarification. Reports are refreshed annually, and interim updates are made when there are material events such as major capacity starts, regulatory changes affecting materials, or sudden price shocks in the polymer feedstock cycle. Before delivery, we do a final pass so the latest public developments are reflected in the numbers and narrative.

Mordor Intelligence's Europe Thermoplastic Elastomers Market Market Sizing Compared With Other Published Estimates

Published market sizes for Europe thermoplastic elastomers can differ even when the year is the same, because each publisher draws the scope line differently and then uses different price and volume assumptions. The spread usually comes from what is counted as the market, how mixed compounds and related elastomer families are treated, and how currency timing and inflation are applied.

The main gap comes from whether adjacent elastomer materials and finished component value are blended into the number, because Mordor Intelligence counts only the thermoplastic elastomer material market in Europe and keeps the value at the resin or compound sale level, which avoids double counting parts made from TPEs. Differences also show up when one estimate assumes faster ASP progression across TPU and other higher priced grades, or when country coverage and update timing do not reflect the same industrial slowdown or rebound signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.19 B (2025) | |

| Regional Consultancy A | USD 6.34 B (2025) | Uses a broader type list and may include more compounded and specialty elastomer blends under the TPE label, which can lift the total slightly when mixed compounds are priced at higher averages. |

| Trade Journal B | USD 6.25 B (2025) | Applies a different price deck by chemistry and may smooth pricing using longer averaging windows, which can shift a single-year market value when feedstock and energy costs move quickly. |

The table shows a tight range for 2025, which is expected in a mature regional materials market, yet the small differences still trace back to what is included and how price is refreshed. By keeping scope tied to material revenue and then cross checking totals with end use demand signals and price realism, the estimate remains easy to follow and repeat when assumptions are updated.

Key Questions Answered in the Report

How large is the Europe thermoplastic elastomers market in 2026?

The Europe thermoplastic elastomers market size stands at USD 6.41 billion in 2026, and it is projected to reach USD 7.59 billion by 2031 at a 3.44% CAGR.

Which product segment grows fastest through 2031?

Thermoplastic polyurethanes post the strongest forecast, advancing at a 3.56% CAGR on the back of medical and premium automotive demand.

Why are recycled-content TPE grades gaining traction?

The 2024 revision of the End-of-Life Vehicles Directive forces OEMs to hit 85% material recovery and 95% recyclability, incentivizing 50%-plus PCR blends in seals and interior skins.

Which country dominates regional consumption?

Germany commands 44.10% of demand, leveraging its extensive automotive and chemical production ecosystem.

How do feedstock price swings affect producers?

Styrene and butadiene costs can run 50–60% of TPE-S cash costs; a steep crude decline or spike compresses margins, forcing non-integrated compounders to renegotiate contracts or idle capacity.

Page last updated on: