Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 7.73 Billion |

| Market Size (2031) | USD 10.85 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Coolant Market Analysis by Mordor Intelligence

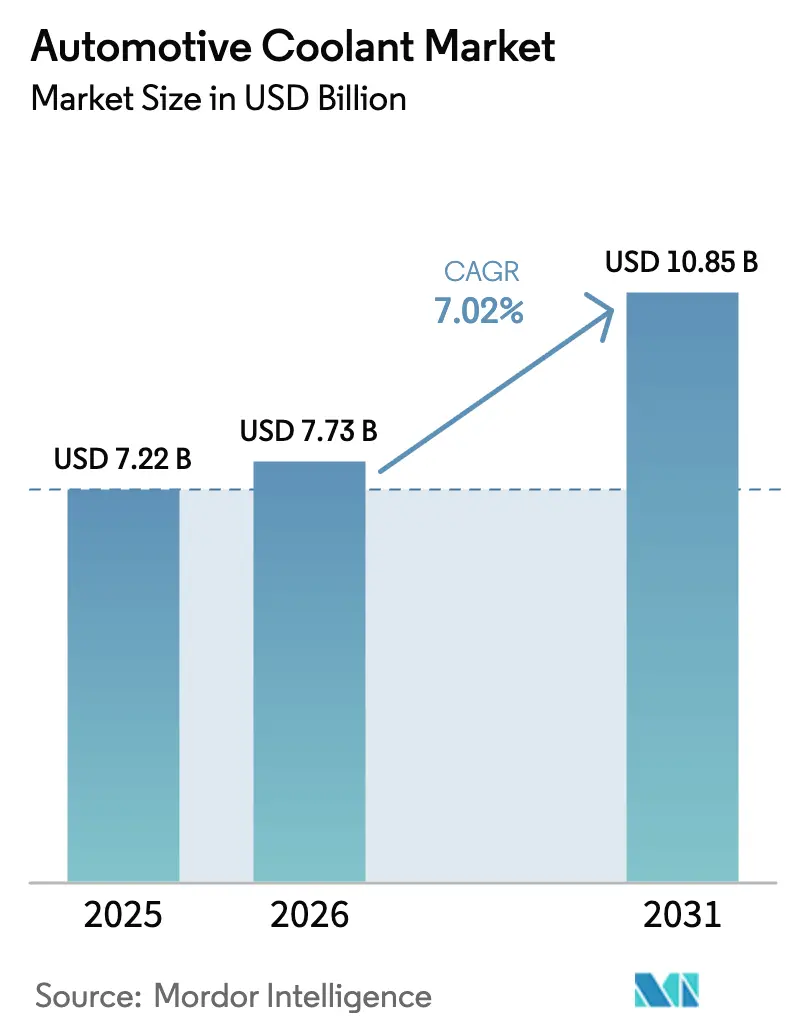

The automotive coolant market size is expected to grow from USD 7.22 billion in 2025 to USD 7.73 billion in 2026 and is forecast to reach USD 10.85 billion by 2031 at a 7.02% CAGR over 2026-2031. Rising electric-vehicle production, aging internal-combustion fleets that require frequent fluid changes, and stricter thermal-management regulations are driving the steady expansion of the automotive coolant market. Suppliers gain from value-added chemistry that lengthens drain intervals, while fleet operators reduce downtime costs through premium formulations. Electrification reshapes product needs by pushing low-conductivity, dielectric coolants into volume production, creating a fresh revenue layer atop traditional ethylene-glycol lines.

Key Report Takeaways

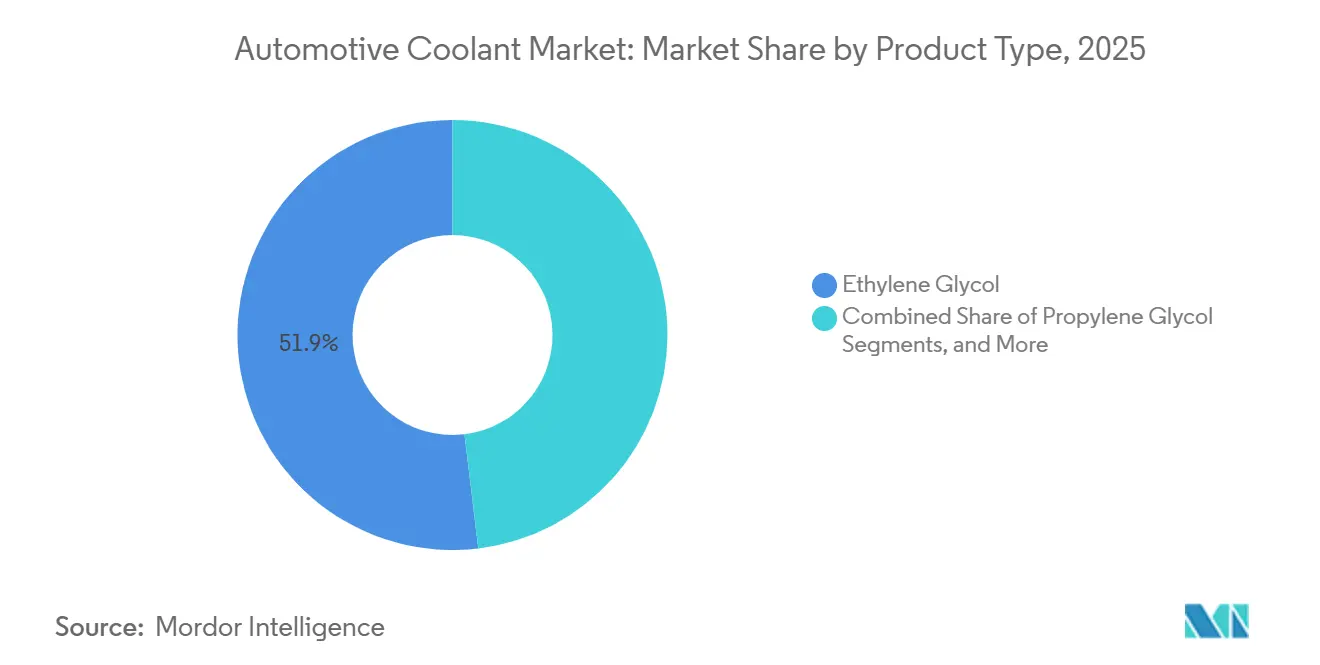

- By product type, Ethylene glycol held 51.92% of the automotive coolant market share in 2025, while glycerin-based coolants are forecast to post a 9.01% CAGR through 2031.

- By vehicle type, Passenger cars accounted for 45.52% of the automotive coolant market size in 2025, and light commercial vehicles are projected to advance at a 7.12% CAGR through 2031.

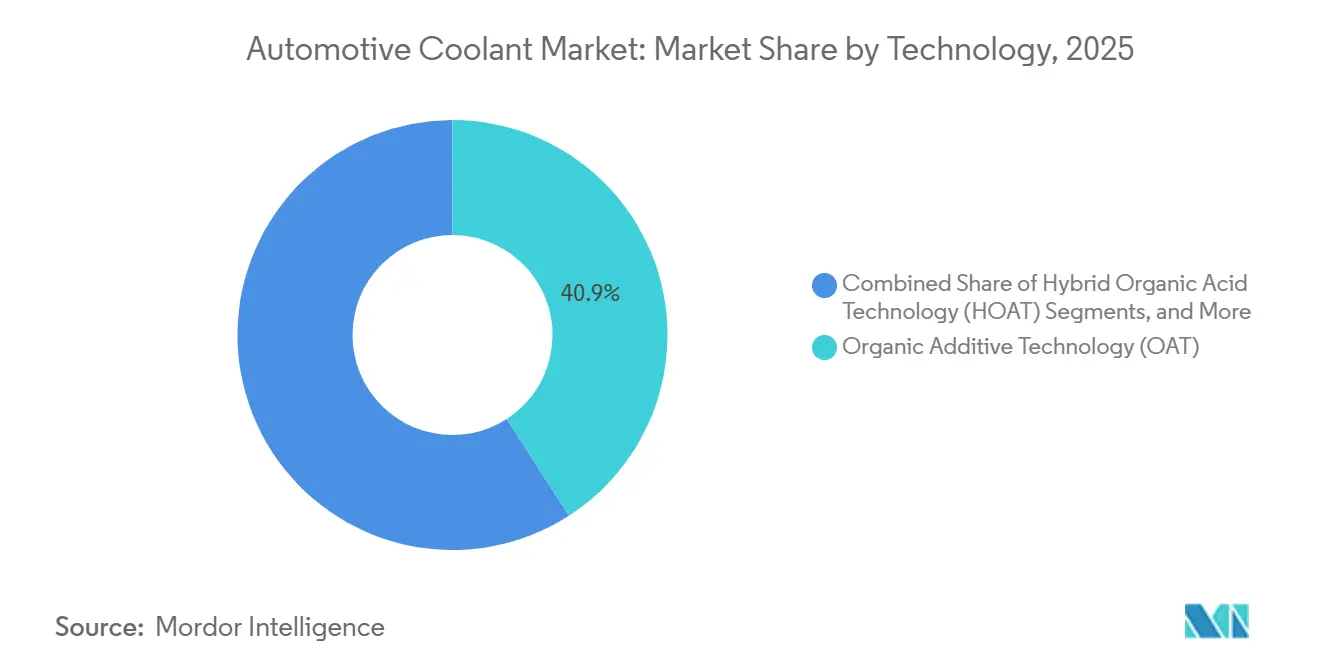

- By technology, Organic Additive Technology captured 40.88% of the automotive coolant market revenue share in 2025, whereas Hybrid Organic Acid Technology is set to grow at a 7.91% CAGR through 2031.

- By end user, the aftermarket segment accounted for 66.94% of the automotive coolant market size in 2025, while OEM fill is projected to expand at a 5.49% CAGR during the forecast period.

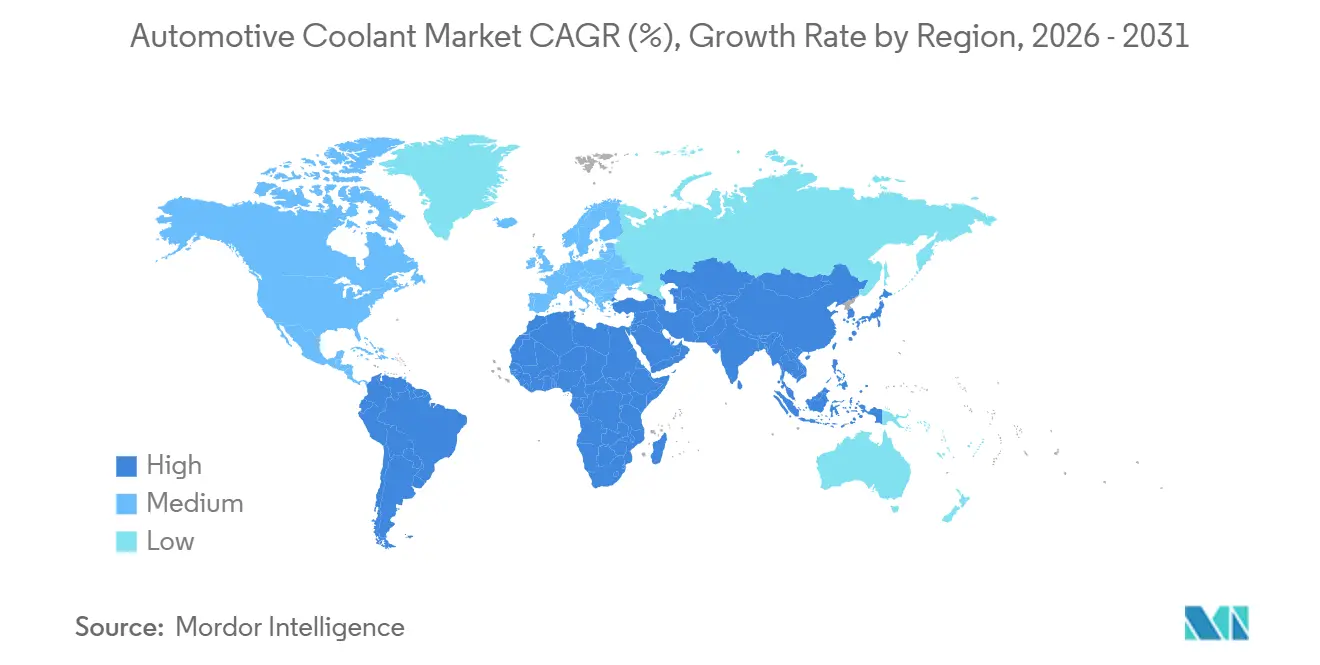

- By geography, the Asia-Pacific region commanded 34.53% of the automotive coolant market share in 2025, and South America is projected to register a 6.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Coolant Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Vehicle Parc and Aging Fleet | +1.8% | Global, with concentration in North America and Europe | Long Term (≥ 4 Years) |

| OEM Push for Long-Life OAT/HOAT Coolants | +1.5% | Global, Led by North America and Asia-Pacific | Medium Term (2–4 Years) |

| Growth of Emerging-Market Vehicle Production | +1.2% | Asia-Pacific Core, Spill-Over to South America | Medium Term (2–4 Years) |

| Adoption of High-Performance ICE Designs | +0.9% | Global, Emphasis on Europe and North America | Short Term (≤ 2 Years) |

| Demand for Dielectric Thermal-Management Fluids in EVs | +0.7% | Asia-Pacific and Europe, Expanding to North America | Medium Term (2–4 Years) |

| Environmental Shift Toward Bio-Based Glycerin Coolants | +0.6% | Europe and North America, Regulatory-Driven | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Rising Global Vehicle Parc and Aging Fleet

Fleet aging trends are driving consistent demand in the automotive coolant aftermarket, as older vehicles require more frequent coolant replacements compared with modern extended-life formulations. The expansion of the global vehicle parc, particularly in emerging markets, is generating replacement demand that outpaces new-vehicle sales growth. In India, the automotive aftermarket is expected to scale significantly, supported by government initiatives such as PLI and PM E-DRIVE, which promote domestic vehicle production while sustaining a substantial internal combustion engine fleet. This trend benefits aftermarket coolant suppliers, as aging fleets in North America and Europe gradually shift from conventional to long-life coolant systems during major service intervals. The effect is especially pronounced in heavy-duty commercial vehicles, where fleet operators adopt extended-life coolants to reduce maintenance frequency, lower operational costs, and efficiently manage larger vehicle populations.

OEM Push for Long-Life OAT/HOAT Coolants

Original equipment manufacturers are standardizing on organic acid technology and hybrid formulations to achieve service intervals exceeding 150,000 miles, fundamentally altering coolant demand patterns from volume-based to value-based consumption. General Motors' DexCool adoption established the template, with service life extending to 150,000 miles compared to conventional coolants' 30,000-mile intervals[1]"Late-Model Cooling System Cautions," MOTOR, motor.com. This shift reduces total coolant volume consumption per vehicle over its lifetime while increasing per-unit coolant value and complexity. European OEMs, such as Mercedes-Benz, specify 15-year service intervals for certain applications, creating demand for premium coolant chemistries with enhanced stability and corrosion protection. The transition challenges aftermarket suppliers to stock multiple chemistry types while educating service technicians on compatibility requirements, as mixing incompatible coolant types accelerates component failures.

Growth of Emerging-Market Vehicle Production

Emerging-market expansion, led by India's 66% year-over-year growth in luxury EV registrations and China's thermal management regulations, drives both ICE and EV coolant demand through localized production requirements[2]"Electric Vehicle Industry in India: Growth, Policy & Market Trends," IBEF, ibef.org. India's automotive production growth, supported by government manufacturing incentives, creates demand for both conventional and EV-specific coolant formulations as domestic OEMs establish thermal management supply chains. China's GB standards for EV thermal management mandate specific coolant properties for battery and power electronics cooling, creating regulatory barriers that favor established coolant suppliers with technical expertise. South American markets, particularly Brazil and Argentina, benefit from automotive integration agreements that streamline vehicle homologation and component approval processes, thereby reducing market-entry barriers for coolant suppliers serving both countries [3]"Resolution 114/2024," MINISTRY OF INDUSTRY AND COMMERCE, Argentina.gob.ar .

Demand for Dielectric Thermal-Management Fluids in EVs

Electric vehicle thermal management requirements fundamentally differ from those in ICE applications, creating new market segments for low-conductivity coolants and immersion-cooling fluids that protect high-voltage battery and power electronics systems. China's regulatory framework mandates specific electrical conductivity limits for EV coolants, driving demand for specialized formulations that balance thermal performance with electrical safety. Prestone's recent patent developments in low-conductivity coolant technology demonstrate industry innovation in this space, addressing the dual requirements of thermal efficiency and electrical isolation. The market opportunity extends beyond automotive applications, as coolant manufacturers like PETRONAS diversify into data center immersion cooling, leveraging their expertise in EV thermal management for high-density computing applications. Advanced nanofluids incorporating graphene oxide and nanodiamond particles achieve up to 40% improvements in thermal conductivity while maintaining the electrical isolation required for battery-cooling circuits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material (Glycol) Price Volatility | −1.4% | Global, Acute in Asia-Pacific Manufacturing Hubs | Short Term (≤ 2 Years) |

| Extended Drain Intervals Cutting Aftermarket Volume | −1.2% | North America and Europe, Spreading to Asia-Pacific | Medium Term (2–4 Years) |

| Sealed Cooling Loops in Next-Gen EV Platforms | −0.7% | Asia-Pacific and Europe, Increasingly Common in Premium EVs | Long Term (≥ 4 Years) |

| Toxicity-Driven Ethylene-Glycol Restrictions | −0.5% | Europe and North America, Regulatory-Driven | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Raw-Material (Glycol) Price Volatility

Ethylene glycol price volatility continues to directly affect automotive coolant manufacturing costs, putting pressure on margins and potentially limiting growth in price-sensitive segments. Fluctuations in global ethylene glycol markets challenge manufacturers’ ability to maintain stable retail pricing, particularly in emerging markets where cost sensitivity remains high. The adoption of bio-based glycerin alternatives, though environmentally advantageous, introduces additional cost pressures from premium pricing, thereby restricting uptake among budget-conscious aftermarket customers. Strengthening supply chain resilience is therefore critical, with manufacturers such as Arteco investing in local production facilities in China to reduce import dependency and mitigate currency risks. Smaller coolant producers lacking vertical integration or long-term supply contracts are especially vulnerable to raw material shortages, which may accelerate industry consolidation and favor larger, integrated players over the coming years.

Extended Drain Intervals Cutting Aftermarket Volume

The adoption of long-life coolants reduces total aftermarket volume consumption as service intervals extend from 30,000 miles to 150,000+ miles, fundamentally altering demand patterns from frequent replacement to infrequent, premium purchases. The transition creates a volume-to-value shift, requiring coolant suppliers to capture higher margins per unit to offset reduced replacement frequency. Heavy-duty applications demonstrate this impact most clearly, where Perkins Extended Life Coolant reduces coolant and additive costs by up to 80% through 3,000-hour service intervals compared to conventional formulations. The challenge compounds as sealed cooling systems in next-generation EV platforms eliminate traditional service points, potentially reducing aftermarket coolant demand for battery electric vehicles. Fleet operators increasingly adopt extended-life coolants to reduce maintenance costs, creating a structural headwind for aftermarket volume growth while benefiting OEM fill applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ethylene Glycol Dominance Faces Bio-Based Challenge

Ethylene glycol maintains its market leadership with a 51.92% of the automotive coolant market share in 2025, driven by its proven performance characteristics and established supply chains. Meanwhile, glycerin emerges as the fastest-growing segment, with a 9.01% CAGR through 2031, reflecting environmental sustainability mandates and the adoption of bio-based chemistry. The ethylene glycol segment benefits from mature manufacturing infrastructure and cost advantages, particularly in Asia-Pacific production hubs where scale economies support competitive pricing.

The segment dynamics reflect a broader industry transformation, in which traditional chemical leadership is being disrupted by sustainability-driven innovation, creating opportunities for suppliers with bio-based capabilities while challenging established ethylene glycol producers to develop renewable alternatives or risk erosion of their market share.

By Vehicle Type: Commercial Vehicles Drive Growth Despite Passenger Car Leadership

Passenger cars maintain a 45.52% of the automotive coolant market share in 2025, as e-commerce expansion and last-mile delivery electrification create specialized thermal management requirements. Light commercial vehicles represent the fastest-growing segment, with a 7.12% CAGR through 2031. The passenger car segment benefits from volume production and standardized coolant specifications; however, growth moderates as extended-life coolants reduce the need for replacement. Commercial vehicle applications require higher-performance coolants that can support extended service intervals and severe-duty operation. The heavy-duty segments are increasingly adopting OAT formulations to achieve a 1,000,000-mile service life. Medium- and heavy-duty commercial vehicles benefit from the purchasing power of fleets and professional maintenance practices that favor premium coolant formulations over conventional alternatives.

The segment transformation reflects broader transportation electrification trends, in which commercial fleets lead EV adoption due to total cost of ownership benefits, driving demand for specialized battery thermal management coolants. EPA regulations mandating substantial PEV penetration through 2032 particularly impact medium-duty delivery vehicles, where fleet purchasers like Amazon and FedEx drive early adoption of electric powertrains requiring dedicated thermal management solutions.

By Technology: OAT Leadership Challenged by HOAT Innovation

Organic Additive Technology holds 40.88% of the automotive coolant market share in 2025, as OEMs seek optimized corrosion protection combining organic acids with targeted inorganic additives. Hybrid Organic Acid Technology (HOAT) is projected to be the fastest-growing segment, with a 7.91% CAGR through 2031. OAT formulations maintain leadership through proven extended-life performance and broad OEM adoption, particularly in North American applications where General Motors' DexCool established the technology standard. HOAT represents the evolution of technology that addresses OAT limitations in specific applications, incorporating silicate or phosphate additives to enhance immediate corrosion protection while maintaining extended service-life characteristics. Inorganic Additive Technology (IAT) serves legacy applications and cost-sensitive segments, though market share declines as OEMs transition to extended-life formulations.

The technology segmentation reflects industry maturation, where chemistry optimization drives competitive differentiation rather than fundamental innovation. European OEMs, in particular, favor HOAT formulations that combine OAT longevity with enhanced aluminum protection, creating regional specification differences that challenge global coolant suppliers to maintain multiple chemistry platforms while achieving scale economies.

By End User: Aftermarket Dominance Faces OEM Growth Challenge

The aftermarket segment commands a 66.94% share of the automotive coolant market in 2025, reflecting the ongoing service requirements of the installed vehicle base. Meanwhile, OEM channels are expected to experience accelerated growth of 5.49% through 2031, as manufacturers increasingly specify premium coolant formulations at the factory fill. Aftermarket dominance stems from the replacement cycle, where aging vehicle fleets require coolant service multiple times throughout the vehicle's lifetime, creating sustained demand independent of fluctuations in new-vehicle sales. The segment faces structural challenges as extended-life coolants reduce service frequency, shifting demand from volume-based to value-based consumption patterns.

OEM growth acceleration reflects manufacturers' strategic focus on extended-life coolants, which reduce warranty costs while differentiating their service offerings. The channel shift creates opportunities for coolant suppliers with OEM relationships while challenging traditional aftermarket distributors to adapt to lower throughput volumes. Regulatory compliance factors increasingly influence OEM coolant selection as emission durability requirements extend to 160,000 kilometers under EU6d standards, creating demand for coolants that maintain thermal management performance over extended vehicle lifecycles.

Geography Analysis

The Asia-Pacific region maintains the largest regional market share, accounting for 34.53% of the automotive coolant market in 2025. This is driven by China's stringent EV thermal management regulations and India's rapid expansion of automotive production, which is supported by government manufacturing incentives. China's GB standards mandate specific electrical conductivity limits for EV coolants, creating demand for specialized formulations that balance thermal performance with electrical safety requirements. India's automotive aftermarket growth, supported by PLI and PM E-DRIVE policies, generates sustained demand for both conventional and EV-specific coolant formulations as domestic OEMs establish thermal management supply chains. Japan and South Korea contribute to the development of advanced EV technology, which requires specialized dielectric coolants for battery and power-electronics cooling applications.

South America emerges as the fastest-growing region, with a 6.67% CAGR through 2031, benefiting from Argentina-Brazil automotive integration policies that streamline vehicle homologation and component approval processes, while expanding commercial vehicle production to meet growing e-commerce demand. The region's growth acceleration stems from mutual recognition agreements that reduce regulatory barriers for coolant suppliers serving both major markets, creating economies of scale for regional operations.

North America and Europe represent mature markets with moderate growth rates, as the adoption of extended-life coolants reduces replacement frequency, while regulatory requirements drive specification upgrades toward premium formulations. European markets are facing particular transformation pressure from REACH regulations and PFAS restrictions, which favor bio-based coolant alternatives, creating opportunities for suppliers with sustainable chemistry capabilities. North American fleet operators increasingly adopt extended-life coolants to reduce maintenance costs, creating structural headwinds for aftermarket volume growth while benefiting OEM fill applications.

Competitive Landscape

Established players like BASF, Chevron, and ExxonMobil dominate the automotive coolant market, leveraging advanced chemistry platforms and global distribution networks. In contrast, emerging disruptors are carving a niche with EV-specific dielectric coolants and applications in data center cooling. These market leaders, through vertical integration, regulatory compliance expertise, and enduring relationships with OEMs, have strengthened their competitive edge, making it difficult for smaller suppliers to enter the fray.

White-space opportunities emerge in EV thermal management applications, where traditional coolant suppliers are diversifying into battery cooling and immersion cooling for data centers, as demonstrated by PETRONAS's partnership with Iceotope for precision liquid cooling solutions. Technology adoption patterns favor suppliers with patent portfolios in nanofluids and low-conductivity formulations, as companies like Prestone develop specialized solutions for EV applications that require electrical isolation.

Competitive intensity increases in emerging markets, where local production capabilities and regulatory compliance create advantages for established players with regional manufacturing footprints. This is evidenced by Arteco's facility establishment in China, which serves the local automotive and electronics cooling markets.

Automotive Coolant Industry Leaders

-

ExxonMobil Corp.

-

Chevron Corporation

-

TotalEnergies SE

-

Saudi Aramco Group

-

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Automotive Research Association of India (ARAI), under the Ministry of Heavy Industries, signed an MoU with Hindustan Petroleum Corporation Limited (HPCL) Green R&D Centre. The partnership focuses on joint research in lubricants, coolants, fuels, additives, and energy solutions to develop advanced engines and vehicles while enhancing indigenous technologies.

- September 2024: Bosch Rexroth partnered with Modine to integrate EVantage liquid-cooled thermal management systems into the eLION portfolio for electrified off-highway machinery, thereby expanding thermal management applications beyond the automotive sector into industrial mobile equipment.

- June 2024: PETRONAS Lubricants International forged a partnership with Iceotope to co-develop sustainable thermal management solutions for data centers, introducing PETRONAS Iona Tera liquid coolant as an expansion beyond automotive applications.

Global Automotive Coolant Market Report Scope

Automotive coolants are liquid coolants used to dissipate heat in automotive internal combustion engines. The coolant prevents corrosion in the cooling system by removing excess heat from the engine and limiting long-term damage.

The scope of the report covers segmentation based on vehicle type, chemical type, and geography.

The Automotive Coolant Market Report is Segmented by Product Type (Ethylene Glycol, Propylene Glycol, Glycerin, Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Technology (IAT, OAT, HOAT), End User (OEM, and Aftermarket), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Ethylene Glycol |

| Propylene Glycol |

| Glycerin |

| Others |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Bus and Coaches |

By Technology

| Inorganic Additive Technology (IAT) |

| Organic Additive Technology (OAT) |

| Hybrid Organic Acid Technology (HOAT) |

By End User

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Ethylene Glycol | |

| Propylene Glycol | ||

| Glycerin | ||

| Others | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Bus and Coaches | ||

| By Technology | Inorganic Additive Technology (IAT) | |

| Organic Additive Technology (OAT) | ||

| Hybrid Organic Acid Technology (HOAT) | ||

| By End User | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What will be the market size of automotive coolant market?

The automotive coolant market is expected to grow from USD 7.22 billion in 2025 to USD 7.73 billion in 2026 and is forecast to reach USD 10.85 billion by 2031 at 7.02% CAGR over 2026-2031.

Why is South America the fastest growing region through 2031?

Argentina-Brazil integration policies streamline homologation, lifting vehicle production and coolant demand.

How do electric vehicles influence coolant formulations in 2026?

EVs require low-conductivity dielectric fluids that protect battery packs and power electronics from electrical shorts.

What factor most constrains aftermarket coolant volume in 2026?

Extended drain-interval technologies lengthen service life to 150,000 miles or more, reducing replacement frequency.

Which technology segment shows the highest growth rate through 2031?

Hybrid Organic Acid Technology is advancing at an 7.91% CAGR as OEMs seek balanced corrosion protection.

Page last updated on: