Automotive On-board Charger Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

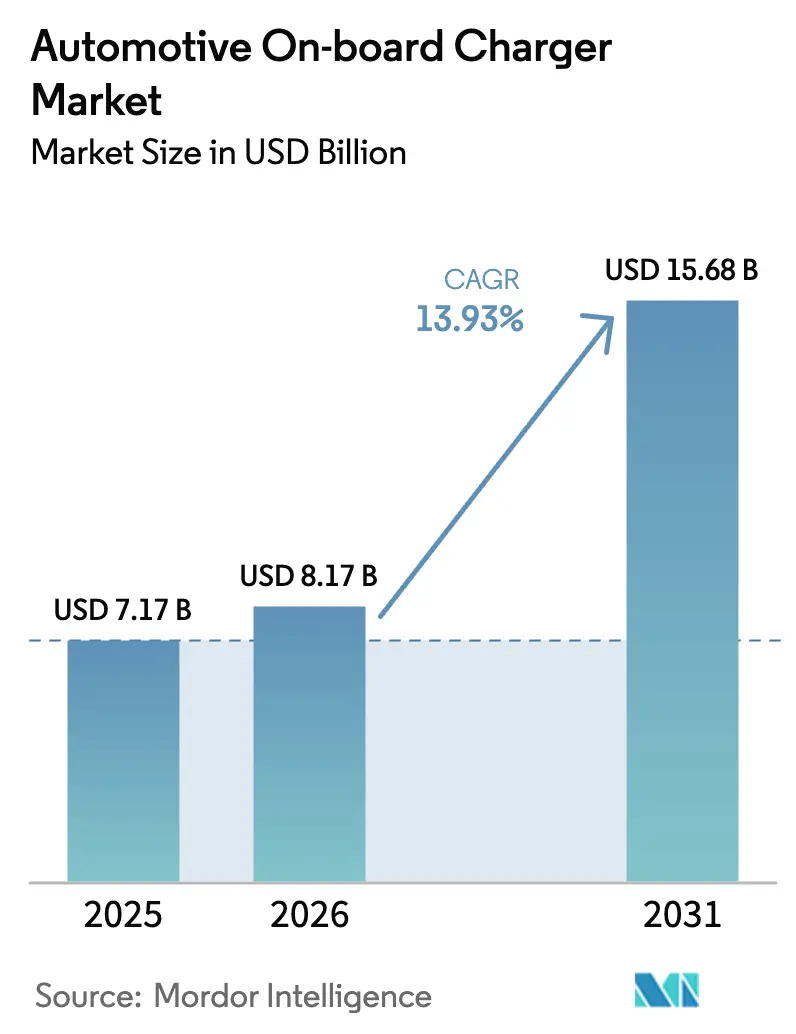

| Market Size (2026) | USD 8.17 Billion |

| Market Size (2031) | USD 15.68 Billion |

| Growth Rate (2026 - 2031) | 13.93% CAGR |

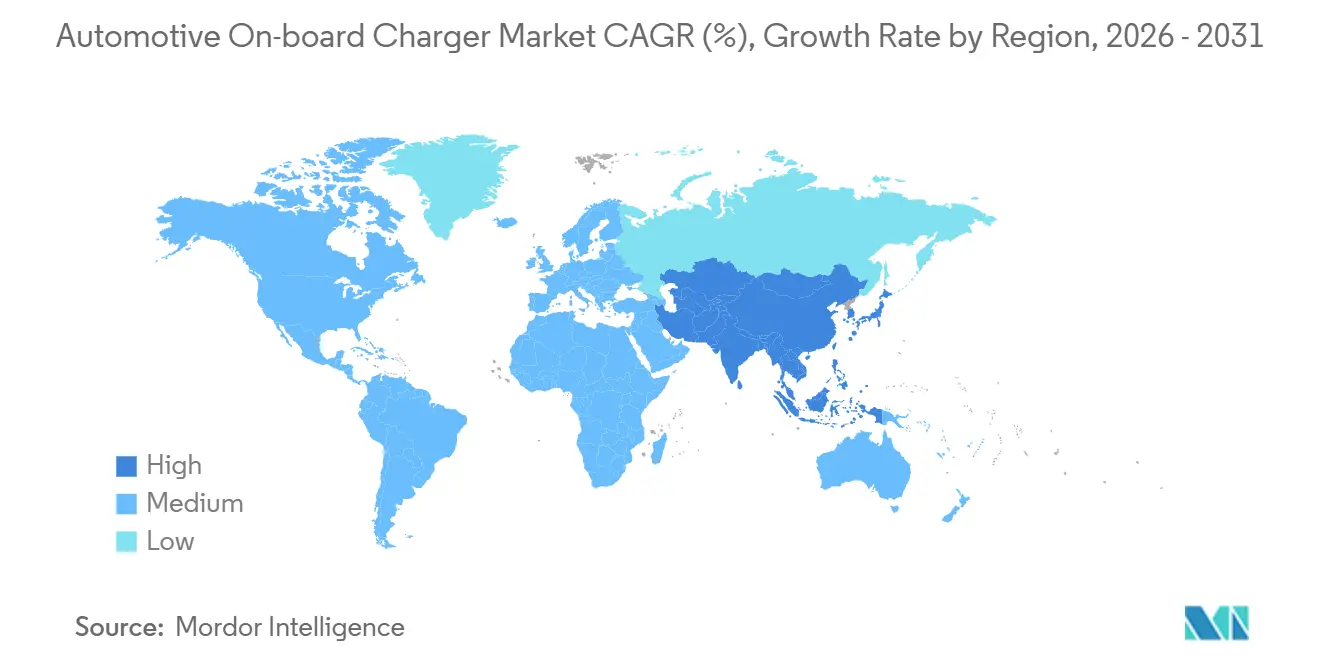

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

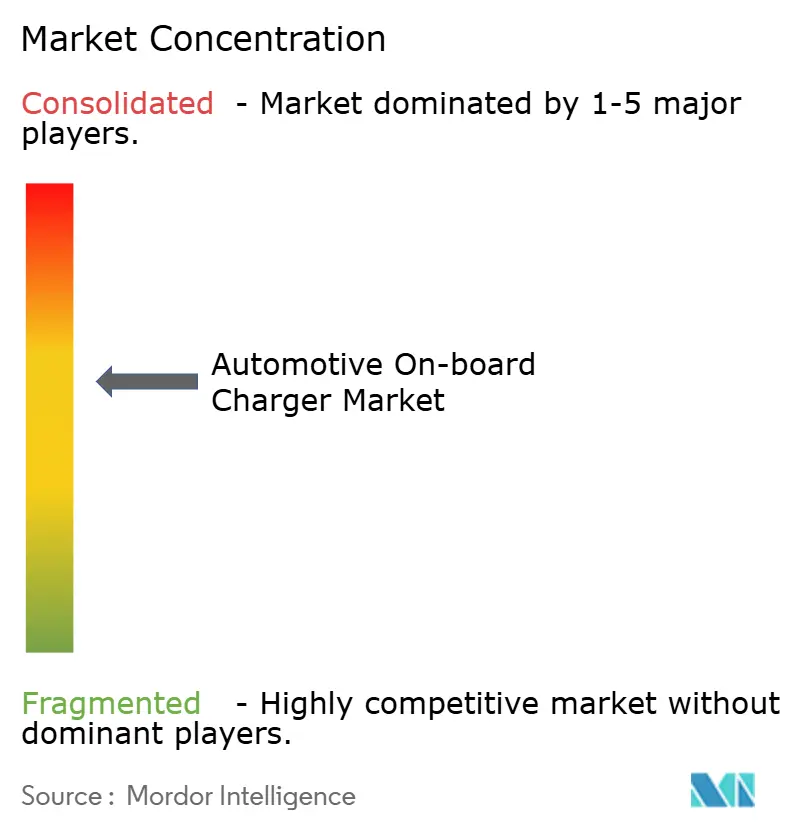

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive On-board Charger Market Analysis by Mordor Intelligence

The automotive on-board charger market size is expected to grow from USD 7.17 billion in 2025 to USD 8.17 billion in 2026 and is forecast to reach USD 15.68 billion by 2031 at 13.93% CAGR over 2026-2031. Growing preference for higher-power AC charging, wider adoption of bidirectional functionality, and falling wide-band-gap semiconductor costs are aligning vehicle architectures and grid-integration roadmaps worldwide. Battery-electric models dominate demand, three-phase residential connections in Europe and parts of Asia are accelerating the shift toward 22 kW charging, and regulators on three continents now embed vehicle-to-grid readiness into funding rules. Silicon-carbide and gallium-nitride devices are squeezing inverter and charger footprints, enabling Tier-1 suppliers to fold 22 kW capability into 3-in-1 e-axles sold to both passenger and commercial OEM programs. At the same time, depot-based AC charging strategies among bus and delivery fleets are spurring specification upgrades that keep overnight charging windows under six hours without the demand-charge penalties associated with ultra-fast DC hubs.

Key Report Takeaways

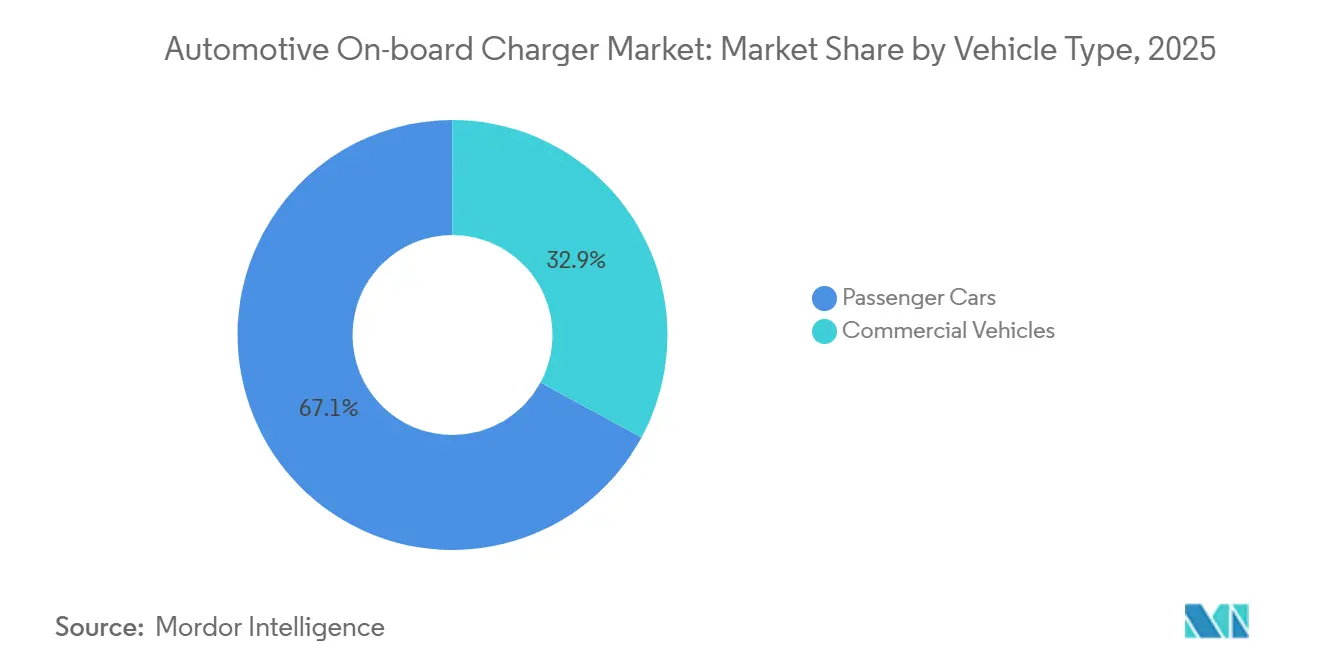

- By vehicle type, passenger cars accounted for 67.10% of the automotive on-board charger market share in 2025, whereas commercial vehicles are forecast to expand at 14.42% CAGR to 2031.

- By powertrain type, battery-electric vehicles led with 75.33% revenue share in 2025, and are advancing at a 15.48% CAGR through 2031.

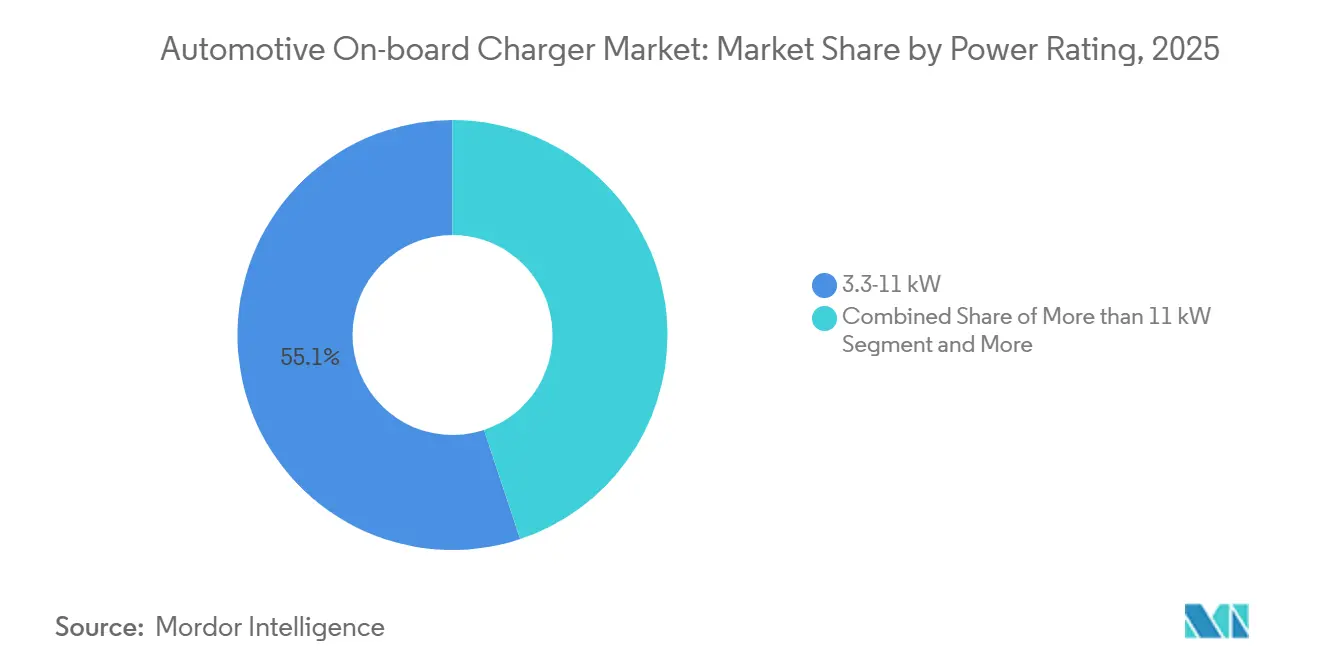

- By power rating, the 3.3-11 kW band captured 55.12% of 2025 revenue, but chargers above 11 kW are projected to grow at 14.71% CAGR over the same period.

- By sales channel, OEM-installed units represented 84.25% of 2025 shipments, yet the aftermarket is rising at 15.75% CAGR on retrofit demand across early-generation EVs.

- By geography, Asia-Pacific held 39.05% share in 2025 and is set to record the fastest regional growth at 15.02% CAGR to 2031, propelled by China’s localization mandates and India’s FAME-II incentives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive On-board Charger Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Adoption and Purchase Incentives | +3.2% | China, Europe, California | Medium term (2-4 years) |

| Switch to 800 V Architectures | +2.8% | Europe, China, North America premium | Medium term (2-4 years) |

| Declining SiC/GaN Prices | +2.1% | Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Plug-&-Charge and V2G Readiness | +1.9% | Europe, United States, Asia-Pacific export platforms | Long term (≥ 4 years) |

| Traction-Integrated and Bidirectional OBCs | +1.7% | Global premium and commercial | Long term (≥ 4 years) |

| PV-Integrator Channel in Emerging Markets | +1.4% | India, Southeast Asia, Brazil, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aggressive Global EV Adoption Targets and Purchase Incentives

Governments are front-loading subsidy budgets and tightening fleet CO₂ rules, forcing automakers to standardize 11 kW or higher chargers so vehicles qualify for evolving incentive tiers. The EU’s 2035 internal-combustion ban spurred volume brands to future-proof models with bidirectional-ready hardware [1]“Alternative Fuels Infrastructure Regulation,” European Commission, europa.eu. China kept its New Energy Vehicle rebates through 2025 and excludes 3.3 kW designs from higher rebate brackets, while California’s Advanced Clean Cars II regulation is nudging several other United States states toward a de facto nationwide zero-emission sales mandate. India’s FAME-II extension channels significant investment into vehicles that embed domestic, bidirectional-capable chargers. Together, these policies compress product-cycle timelines and shift demand toward power-dense, protocol-rich chargers that accommodate future grid-services revenue streams.

Rapid Switch to 800 V Vehicle Architectures Enabling 11-22 kW OBCs

High-voltage platforms decouple AC charge time from battery size, letting 90 kWh packs add 22 kW home charging without oversizing cables or cooling loops. Porsche’s Taycan validated consumer appetite for premium AC performance, and Hyundai’s 2024 E-GMP rollout pushed 22 kW chargers into mid-segment sedans. GM’s Ultium migration to 800 V from 2027 aligns pickup and SUV families around 19.2 kW AC capability, while BYD’s e-Platform 3.0 integrates an 11 kW bidirectional charger inside the drive inverter, trimming underbody space and lowering parts count. Europe reaps the most benefit because three-phase 400 V home service is standard; North America’s single-phase limits keep adoption to 11 kW, yet premium fleets still value the reduced thermal losses of 800 V silicon-carbide designs.

Declining SIC/GAN Device Prices Lifting OBC Power Density

Wide-band-gap transistor prices fell significantly from 2024-2025, pushing SiC cost parity with silicon when cooling and passives are counted. Infineon’s CoolSiC line doubled shipments, ON Semiconductor monolithically integrated gate drivers, and Wolfspeed forecasts a significant wafer-price drop by 2027. GaN devices trail in cost yet lead in sub-11 kW form factors where 500 kHz switching shrinks magnetics. Automakers that once reserved SiC for halo trims now plan single-supply chains that amortize qualification costs across volume models, reinforcing the learning curve that further compresses price gaps.

Mandatory ISO 15118 / Plug-&-Charge and V2G Readiness Clauses in EU and US Funding Schemes

The European Alternative Fuels Infrastructure Regulation locks in ISO 15118-20 for all public AC posts by 2025, embedding secure authentication and bidirectional negotiation at the protocol layer. The U.S. National Electric Vehicle Infrastructure program requires bidirectional readiness for grant-funded chargers by 2025. These mandates ripple into vehicle bills-of-materials because incompatibility strands investment. OEMs are therefore synchronizing charger firmware and cybersecurity stacks in parallel with hardware upgrades, pulling forward development programs that had once been slated for the 2030 model year.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wide-Band-Gap Substrate Costs | −1.8% | Global cost-sensitive segments | Medium term (2-4 years) |

| Hesitancy to Up-Spec AC Chargers | −1.5% | North America, Europe, China tier-1 cities | Short term (≤ 2 years) |

| Bottlenecks for Residential Upgrades | −1.1% | Europe urban centers, Japan, Korea, United States Northeast | Medium term (2-4 years) |

| Scrap-Recycling Regulation in China | −0.9% | China, potential Asia-Pacific spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistently High Wide-Band-Gap Substrate Costs in 22 kW Three-Phase OBCs

In early 2026, six-inch SiC wafers were significantly more expensive than their silicon counterparts, leading to a notable cost premium for each 22 kW charger. While projections for 200 mm lines suggest a reduction in substrate costs by 2028, the current price gap confines high-power AC hardware to premium models. Meanwhile, Chinese Tier-2 suppliers explored low-frequency silicon solutions, but these resulted in a density drop below acceptable thresholds, making them unsuitable for compact platforms.

OEM Hesitancy to Up-Spec AC Chargers as DC Ultra-Fast (≥350 kW) Roll-Outs Accelerate

With Electrify America, Tesla, and IONITY saturating corridors with 350 kW posts, consumers are increasingly favoring en-route charging over home charging. A 2025 survey by the U.S. DOE revealed that buyers prioritize DC availability over Level 2 speed. In response, OEMs have halted upgrades to 11 kW specs and are channeling capital expenditures towards 800 V battery packs. This shift highlights the growing importance of ultra-fast charging infrastructure in shaping consumer behavior and influencing OEM strategies. Additionally, the increasing adoption of electric vehicles (EVs) is driving demand for faster and more efficient charging solutions, further accelerating the transition to DC ultra-fast chargers. As a result, the automotive on-board charger market is undergoing significant changes to align with evolving industry trends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Specification Upgrades

Passenger cars held 67.10% of 2025 shipments due to higher unit volumes, yet fleet procurement policies are tilting the momentum. Electric buses and last-mile vans equip 22 kW chargers to trim pack sizes by 100 kWh, saving significantly in battery cost per vehicle. Commercial vehicles are set to expand with the fastest growth at a 14.42% CAGR through 2031. Depot operators such as Amazon have validated 11 kW as their optimum trade-off between panel upgrade expense and overnight availability, influencing van OEMs to offer dual ratings. This interplay keeps the automotive on-board charger market diversified across duty cycles.

Ride-hail operators in Europe increasingly specify 11 kW-capable sedans so drivers can top up during shift changes; Tesla reports that a notable share of its 2025 European Model 3 sales went to such fleets. In heavy commercial, Proterra’s 19.2 kW AC solution allows midday top-ups without megawatt-scale infrastructure, an approach now mirrored by BYD’s eBus line in Latin America. These cases show how operational cost modeling, not just regulatory pressure, is reshaping charger choices.

By Powertrain Type: BEVs Anchor Demand, PHEVs Stabilize

Battery-electric vehicles represented 75.33% of 2025 revenue and will rise at 15.48% CAGR through 2031, underscoring their role as the core value pool of the automotive on-board charger market. Carmakers are converging on 11 kW as the baseline, with Tesla, Volkswagen, and GM overlaying software packages that later activate bidirectional functions for grid-services compensation. Plug-in hybrids retain a separate supply chain around 3.3-7.4 kW silicon designs that meet overnight charging needs for 20 kWh batteries, and updated EU CO₂ credits now push plug-in hybrid electric vehicle packs toward 30 kWh, nudging charger ratings up to 7.4 kW. Yet the incremental cost of 11 kW hardware still outweighs fleet-tax incentives in many markets, so the automotive on-board charger industry maintains dual product tiers to balance affordability and regulatory compliance.

A second dynamic shaping this segment is residual-value retention. Leasing companies in Germany report that BEVs equipped with 22 kW chargers command higher resale than 11 kW peers after four years, accelerating adoption among corporate fleets that optimize total cost of ownership. In contrast, North American suburban buyers show price sensitivity above 11 kW because single-phase home circuits seldom benefit, reinforcing regional divergence in charger specifications. As a result, the automotive on-board charger market size for plug-in hybrids is forecast to expand by 2031, whereas BEVs could grow further, keeping program volumes high enough for suppliers to amortize SiC qualification costs across both sectors.

By Power Rating: Above-11 kW Segment Gains Traction

The 3.3-11 kW category dominated 55.12% of global shipments in 2025, yet chargers above 11 kW are on track for 14.71% CAGR, reflecting the pull from European three-phase grids and Chinese premium sport utility vehicles. Mercedes-Benz offers 22 kW standard across its EVA2 platform, and Polestar’s 3 SUV positions fast home charging as a core brand differentiator. This evolution is also visible in commercial deployments where buses and depot-based vans adopt 22 kW to halve turnaround time without incurring demand charges from 150 kW DC units. The automotive on-board charger market share thus migrates toward high-power tiers in jurisdictions with grid capacity and incentive alignment.

Conversely, the United States caps residential level-2 at 11 kW, and Canada’s winterized garages rarely upgrade beyond 7.4 kW because ambient cold moderates battery degradation. Automakers therefore modularize designs: Ford’s Lightning pickup uses a common PCB that supports either 11 kW or 19.2 kW, activated by a different component population. For suppliers, this structure increases SKU complexity but preserves production scale, supporting broader dispersion of SiC device costs.

By Sales Channel: Aftermarket Gains as Retrofit Demand Builds

OEM sales dominated 84.25% in 2025, but the aftermarket is climbing 15.75% CAGR because early 3.3 kW EVs no longer satisfy consumer expectations once local utilities approve 7.4 kW or 11 kW home circuits. European subsidy programs reimburse for charger upgrades, triggering brisk demand for Delta Electronics’ 7.4 kW retrofit module that reuses the factory wiring harness. The automotive on-board charger market size for upgrades could grow further by 2031, but deeper integration in new vehicles threatens the long-term ceiling.

Valeo’s 3-in-1 e-axle, which embeds the charger, displaces discrete modules starting in 2026, raising the entry barrier for independent retrofit specialists. Consequently, firms such as Delta-Q pivot to add-on bidirectional kits rather than pure power-rating boosts, monetizing the regulatory push in California and the EU for emergency micro-grid capability. Suppliers that fail to invest in firmware and cybersecurity may exit the segment as compliance costs escalate, tightening channel competition and lifting margins for qualified players.

Geography Analysis

Asia-Pacific captured 39.05% of 2025 revenue and will expand at 15.02% CAGR through 2031. China alone produced 16.6 million New Energy Vehicles in 2025, leveraging local SiC supply chains and “Made in China 2025” rules that keep domestic charger content above 50%. India’s FAME-II ties per-vehicle payouts to indigenous OBC procurement, pushing Tata Motors and Mahindra to dual-source from Varroc and Sona BLW plants in Pune. Japan and South Korea remain cautious on home-wiring upgrades, capping chargers at 6 kW, which slows SiC diffusion despite subsidies. Southeast Asian rooftop-solar bundling, however, is opening a path for 7.4 kW bidirectional designs that store daytime generation for evening air-conditioning loads.

In 2025, Europe, led by three-phase residential grids in Germany, France, and the Nordics, captured a significant portion of the global turnover. By 2025, the Alternative Fuels Infrastructure Regulation mandates the integration of ISO 15118-20 into every public AC plug. This push has prompted Volkswagen to align its MEB platform with the 11 kW bidirectional hardware standard for the 2027 model year. In the Nordics, utilities are already compensating exported kilowatt-hours at spot prices. As a result, vehicle-to-grid trials are expanding beyond initial pilots, rewarding households with 22 kW chargers that can modulate their feed-in. The United Kingdom is echoing this sentiment with its 2025 smart-charging rule, promoting a similar demand-response approach and piquing supplier interest in mid-power OBCs rich in firmware.

North America, contributing significantly in 2025, sees its automotive on-board charger market driven by the Inflation Reduction Act's credit and investments from the National Electric Vehicle Infrastructure[2]“NEVI Final Guidance,” U.S. Department of Transportation, transportation.gov. Federal guidelines stipulate that hardware funded by grants must have bidirectional capabilities after 2026. Ford and GM have already pledged full compliance for their pickups and SUVs by 2027. In California, vehicle-to-grid pilots are incentivizing owners with reimbursements during peak stress events. This makes the bidirectional 11 kW chargers a financially appealing choice. On the other hand, Canada's colder climate leans towards block-heater circuits. Consequently, utilities are opting to subsidize 7.4 kW upgrades over the 11 kW, which is moderating the penetration rates of SiC. Latin America and the Middle East, while currently representing a smaller share, are witnessing significant growth. This surge is fueled by announcements of new plants in Brazil's Rota 2030 and the UAE's fee-waiver initiative. Both programs stipulate that to avail fiscal benefits, chargers above 7 kW must be locally assembled.

Competitive Landscape

Market concentration is moderate: the top five suppliers—BorgWarner, Hyundai Mobis, LG Electronics, Valeo, and DENSO—held a notable share in 2025. All these players now target 800 V SiC designs with sealed-coolant jackets that allow 22 kW continuous operation at ambient 40 °C. Intellectual-property filings around ISO 15118-20 Plug & Charge rose last year, with Infineon, STMicroelectronics, and ON Semiconductor defending algorithmic authentication stacks. The competitive axis has shifted from basic efficiency claims to holistic system integration: software-defined chargers that can unlock vehicle-to-grid via over-the-air update without altering copper harnesses.

Specialists are carving niches. VisIC Technologies’ GaN platform won a 2025 order from a European premium marque for a 22 kW module, besting SiC density in the same envelope[3]“GaN OBC Contract Announcement,” VisIC Technologies, visic-tech.com . Delta Electronics, through co-marketing with independent service chains, secured a modest foothold in Europe's aftermarket, pricing its 7.4 kW kits at an affordable rate installed. Meanwhile, driven by component-level economics, STMicroelectronics eyes a target for 200 mm SiC wafers by 2027, aiming to reduce die costs. This ambitious timeline puts pressure on smaller fabs, nudging them towards technology licensing or an exit from the market.

As 3-in-1 e-axle penetration deepens, propulsion specialists—BorgWarner, Valeo, Hyundai Mobis—gain advantage because they can spread SiC dies across traction and charging duties. Pure-play charger firms risk relegation to retrofit niches unless they pair with inverter vendors or pivot to energy-storage systems. Software and cybersecurity capabilities are now must-have assets as regulators treat chargers as network nodes, lifting compliance costs and narrowing the viable competitive field.

Automotive On-board Charger Industry Leaders

BorgWarner Inc.

Hyundai Mobis Co., Ltd.

LG Electronics

Ficosa International S.A

Valeo SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: FORVIA HELLA and Tau Motors unveiled a transformer-less “viOBC” targeting series production within three years, promising higher density and efficiency.

- September 2025: Sterling Gtake E-Mobility partnered with Landworld Technology to manufacture on-board chargers in Faridabad, forecasting revenue of INR 450 crore (~USD 53 million) by FY 2030.

- August 2025: BRUSA HyPower launched its OBC7 family certified for automotive use, supporting up to 19.2 kW single-phase and 22 kW three-phase across 400 V and 800 V systems.

- February 2025: Changan Automobile integrated Navitas GaN devices into the Qiyuan E07, claiming the first commercial GaN-based on-board charger platform worldwide.

Global Automotive On-board Charger Market Report Scope

The scope includes segmentation by vehicle type (passenger cars and commercial vehicles), powertrain type (battery electric vehicles and plug-in hybrid electric vehicles), power rating (less than 3.3 kW, 3.3-11 kW, and more than 11 kW), and sales channel (OEM-installed and aftermarket). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, the Middle East, and Africa. Market size and growth forecasts are presented by value in USD and by volume in units.

| Passenger Cars |

| Commercial Vehicles |

| Battery Electric Vehicles (BEVs) |

| Plug-in Hybrid Electric Vehicles (PHEVs) |

| Less than 3.3 kW |

| 3.3-11 kW |

| More than 11 kW |

| OEM-installed |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Powertrain Type | Battery Electric Vehicles (BEVs) | |

| Plug-in Hybrid Electric Vehicles (PHEVs) | ||

| By Power Rating | Less than 3.3 kW | |

| 3.3-11 kW | ||

| More than 11 kW | ||

| By Sales Channel | OEM-installed | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the automotive on-board charger market be by 2031?

It is projected to reach USD 15.68 billion by 2031, accelerating at 13.93% CAGR since 2026.

Which vehicle segment is growing fastest for on-board chargers?

Commercial vehicles, especially buses and delivery vans, are forecast to expand charger demand at 14.42% CAGR through 2031.

What role do SiC and GaN play in charger design?

Falling SiC and GaN prices enable lighter, more efficient chargers that fit inside 3-in-1 e-axles and support bidirectional energy flows.

Is retrofit demand expected to stay strong?

Yes, aftermarket revenue is growing 15.75% CAGR as early EV owners upgrade 3.3 kW units to 7.4 kW or 11 kW and add vehicle-to-load features.

Page last updated on: