Hybrid Automation Solutions For Packaging Machinery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

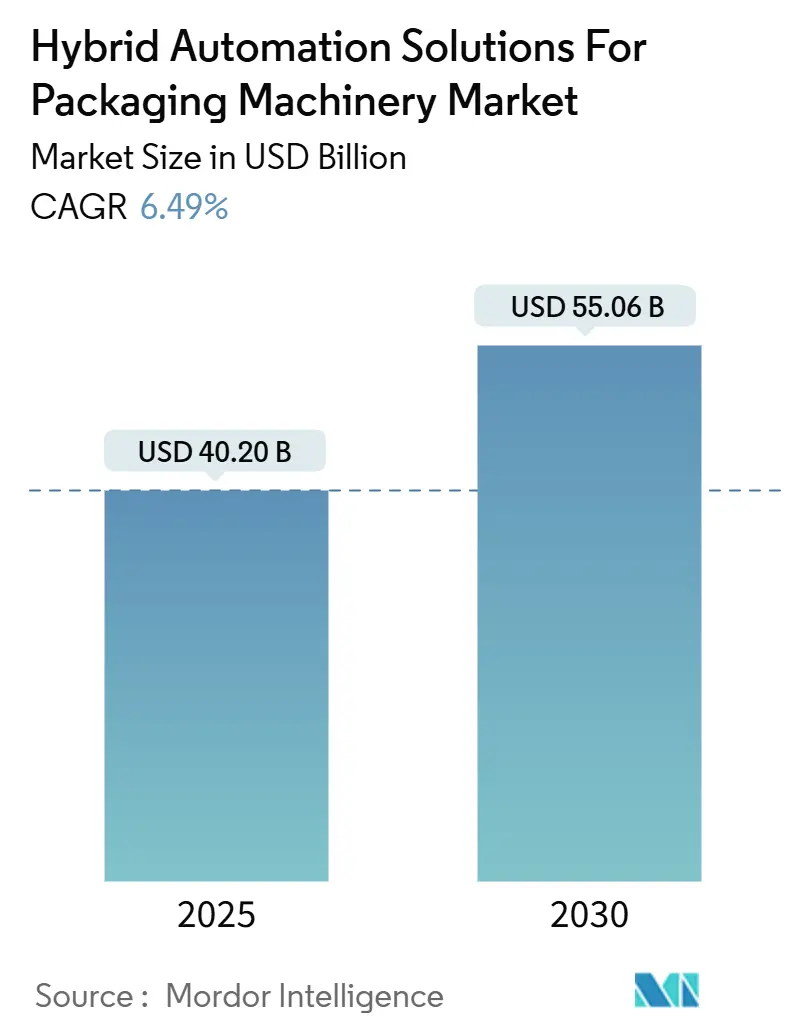

| Market Size (2025) | USD 40.20 Billion |

| Market Size (2030) | USD 55.06 Billion |

| Growth Rate (2025 - 2030) | 6.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Automation Solutions For Packaging Machinery Market Analysis by Mordor Intelligence

The hybrid automation solutions market for packaging machinery is projected to reach USD 40.2 billion by 2025 and is forecasted to increase to USD 55.06 billion by 2030, expanding at a 6.49% CAGR. Inflexible legacy lines are steadily giving way to modular cells that merge programmable logic controllers with artificial intelligence, collaborative robots, and cloud analytics. Manufacturers see these technologies as the fastest path to smaller lot sizes, faster changeovers, and real-time traceability. Capital inflows remain strong in North America, where brownfield retrofits dominate; however, the Asia-Pacific region is drawing the most incremental investment as governments push digital manufacturing initiatives and brand owners localize production closer to e-commerce demand centers.[1]Siemens AG, “Digital Factory Solutions,” siemens.com Consolidation among automation, software, and traditional machinery suppliers is accelerating, sharpening the focus on outcome-based service models and predictive maintenance platforms that can guarantee uptime.

Key Report Takeaways

- By component, the hardware segment captured 48.33% of the hybrid automation solutions for packaging machinery market share in 2024.

- By packaging machinery type, the hybrid automation solutions for packaging machinery market size for labeling and coding equipment are projected to grow at an 8.53% CAGR between 2025–2030.

- By end-user industry, the food and beverage segment captured 37.91% of the hybrid automation solutions for packaging machinery market share in 2024.

- By geography, the hybrid automation solutions for packaging machinery market size for Asia-Pacific is projected to grow at an 8.13% CAGR between 2025–2030.

Global Hybrid Automation Solutions For Packaging Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for flexible smaller-lot packaging | +1.2% | Global with concentration in North America and Europe | Medium term (2–4 years) |

| Growth of e-commerce driven SKUs | +1.5% | Global led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Labor shortages accelerating automation investments | +1.8% | North America and Europe expanding to Asia-Pacific | Long term (≥ 4 years) |

| Adoption of Industry 4.0 and IIoT architectures | +1.3% | Global with early adoption in developed markets | Medium term (2–4 years) |

| Energy-efficiency regulations favouring hybrid drives | +0.7% | Europe and North America, spreading globally | Long term (≥ 4 years) |

| OEM subscription models enabling cap-ex to op-ex shift | +0.9% | Global, led by developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising demand for flexible smaller-lot packaging

Personalized products and limited-edition releases force packaging lines to perform dozens of changeovers per shift without sacrificing throughput. Hybrid automation enables electronic recipe swaps, reducing format change time from hours to minutes, allowing brand owners to target niche segments that carry 15-20% price premiums. Pharmaceutical plants now package orphan drugs in micro-batches of fewer than 100 units while maintaining compliance. Manufacturers that adopted modular cells reported double-digit improvements in overall equipment effectiveness as idle time during changeovers vanished. Investment momentum remains strongest in the United States and Germany, where agile packaging has become a strategic differentiator in crowded consumer categories.

Growth of e-commerce driven SKUs

Online marketplaces have inflated SKU counts ten-fold over the past decade, driving demand for adaptive grippers and vision systems that auto-tune parameters for each item on the fly. Machine-learning algorithms now choose the smallest viable carton, cutting corrugate use by up to 30% and lowering dimensional-weight shipping charges. Direct-to-consumer lines must switch between bulk club packs and single-item parcels, requiring software-defined conveyors and dynamic print-and-apply labelers. Asia-Pacific contract packers have become early adopters because they serve multiple brand owners with highly variable daily order profiles. The payoff is faster fulfillment and lower material waste, which directly improves e-commerce profit margins.

Labor shortages accelerating automation investments

Packaging operator vacancies exceed 40% at many U.S. facilities, forcing plants to run fewer lines or shorter shifts. Collaborative robots take over repetitive pick-and-place tasks, while augmented-reality work instructions enable remaining staff to execute complex changeovers with minimal training. Rising wages shorten payback periods to 18-24 months, shifting automation from a long-term ambition to an immediate necessity. European food processors report a 15% decrease in lost-time injuries after deploying cobots, which improves both safety and retention. As Asia-Pacific wages climb, the region is expected to mirror Western automation intensity within five years.

Adoption of Industry 4.0 and IIoT architectures

Edge sensors and cloud analytics provide real-time feedback, boosting line availability by up to 25% through predictive maintenance alerts. Digital twins simulate new package designs virtually, reducing physical trial runs and cutting the time-to-market in half. Interoperable OPC UA frameworks enable legacy PLCs to feed data into enterprise dashboards, providing executives with a plant-wide view of performance. Early adopters in Japan and the United States now tie bonus targets to overall equipment effectiveness metrics generated from IIoT platforms. The resulting culture shift embeds continuous improvement into daily routines, rather than relying on periodic kaizen events.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital outlay | -1.1% | Global, particularly impacting SMEs | Short term (≤ 2 years) |

| Integration complexity across brownfield lines | -0.8% | North America and Europe with aging infrastructure | Medium term (2–4 years) |

| Cybersecurity vulnerabilities in converged OT/IT | -0.6% | Global with heightened concern in critical sectors | Long term (≥ 4 years) |

| Interoperability gaps with legacy PLC protocols | -0.5% | Global, concentrated in mature manufacturing regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High initial capital outlay

Full hybrid upgrades can cost USD 2-5 million per mid-scale line, a figure that overwhelms many small manufacturers. Traditional ROI models often undervalue speed, flexibility, and SKU responsiveness, making business cases appear weaker than they actually are. Although leasing and pay-per-use schemes exist, auditors often flag the long-term liabilities these contracts create. Economic slowdowns further restrict access to affordable credit, prompting firms to extend the life of aging equipment instead of modernizing. Without creative financing or government incentives, adoption among small and medium enterprises is likely to lag.

Integration complexity across brownfield lines

Legacy conveyors, case packers, and proprietary PLC networks require custom gateways that inflate project costs by 25-40% and add multiple months to validation cycles.[2]Rockwell Automation, “Packaging Solutions,” rockwellautomation.com Each additional vendor protocol multiplies the testing permutations, thereby increasing the risk of unforeseen downtime after go-live. Pharmaceutical plants face even stricter software change controls, which increase documentation costs. A shortage of skilled system integrators lengthens project queues, forcing manufacturers to prioritize the most critical lines first. The result is fragmented modernization that dilutes the full benefits of hybrid automation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Transformation

Services are projected to grow at the fastest 8.95% CAGR as vendors shift to predictive maintenance subscriptions, which can reduce unplanned downtime by up to 40%. Hardware remains the revenue anchor because robotics, drives, and vision systems still account for the majority of spending in hybrid automation solutions for the packaging machinery market. Yet margins are migrating to value-added analytics, and vendors that combine edge controllers with cloud dashboards are signing multi-year performance contracts.

Software’s steady advance reflects rising demand for AI-enabled scheduling, digital twins, and cybersecurity monitoring. Remote support gained momentum during pandemic travel restrictions and now underpins nearly every new service agreement. As a result, hardware suppliers embed secure gateways, allowing service teams to diagnose anomalies in real-time, thereby turning every installed base into a recurring-revenue opportunity.

By Packaging Machinery Type: Labeling Leads Innovation

Filling and dosing equipment dominated the hybrid automation solutions for packaging machinery market share at 32.75% in 2024, as high-volume beverage and pharmaceutical lines still require high-speed volumetric accuracy. However, serialization laws have made labeling and coding the most dynamic category with an 8.53% CAGR, driving upgrades to inkjet and laser coders that integrate directly with enterprise resource planning systems.

Collaborative palletizers are also gaining traction as vision systems identify mixed-case layouts, cutting end-of-line labor. Meanwhile, AI-assisted inspection across all machine types delivers statistical quality control and automated rejection, raising first-pass yield and minimizing recalls

By End-user Industry: Personal Care Accelerates

Food and beverage led spending at 37.91% thanks to its broad SKU mix and strict hygiene codes. Personal care and cosmetics exhibit the strongest 9.55% CAGR as brands race to biodegradable pouches and refill systems, pressuring converters to handle thin-wall laminates and plant-based films without sacrificing throughput.

Life-science producers maintain steady upgrades to satisfy traceability mandates, while consumer electronics adopters seek anti-counterfeit markers in tamper-evident seals. Direct-to-consumer channels are pushing every vertical toward dual-format capability, with both bulk retail packs and single-item e-commerce shipments on the same line. Hybrid cells satisfy both requirements, supported by cloud configuration libraries that load the correct motion profile with a single scan.

Geography Analysis

North America’s early embrace of Industry 4.0 anchors its 33.26% share, and brownfield retrofits continue as food and drug processors modernize batch records and energy-efficient drives. Canada’s carbon-reduction targets spur demand for servo-driven case packers, while Mexican near-shoring funnels capital to flexible lines that serve U.S. retailers without border delays.

The Asia-Pacific region is the momentum story, with an 8.13% CAGR through 2030. Chinese policy incentives and India’s consumer boom stimulate investments in scalable robotics and AI inspection, making the region the largest install base for mid-range collaborative robots.[3]State Council of China, “Manufacturing Policy Updates,” english.www.gov.cn Japan and South Korea contribute technology leadership, exporting high-precision actuation and deep-learning vision modules across the region.

Europe advances on the strength of circular economy mandates and energy efficiency legislation. German machine builders integrate servo-hybrid drives to cut power consumption by 30%, while French packaged-food exporters deploy digital twins to simulate recyclable material runs before purchasing film. South America, the Middle East, and Africa remain nascent but attractive markets, with rising urban incomes and the spread of organized retail creating step-change demand, although adoption lags due to financing constraints.

Competitive Landscape

Competition is moderately fragmented as automation giants collide with packaging specialists. ABB, Rockwell Automation, and Siemens bundle robots, drives, and MES platforms, while Krones, Tetra Pak, and Syntegon retrofit smart sensors onto mechanical assets. Cloud analytics and machine learning differentiate the leaders. Rockwell’s FactoryTalk and Siemens’ MindSphere anchor multi-year outcome guarantees, while ABB embeds vision-guided picking to shorten integration times.

Mergers and acquisitions reflect the shift from hardware to solutions. Siemens’ 2024 purchase of Opcenter Advanced Planning added AI scheduling, and Omron’s 2024 acquisition of IMA Group’s robotics division bolstered European market share. Patent filings in collaborative robotics increased by 20% year-over-year, signaling a technology arms race.

White-space lies in mid-market manufacturers that lack in-house OT expertise. Vendors offering pre-engineered cells with pay-per-use pricing can capture this cohort, particularly in the Asia-Pacific region, where greenfield factories often bypass legacy PLC stages. Cybersecurity credentials are a new tender requirement, as evidenced by Schneider Electric’s 2025 ISO 27001 certification, which reassures pharmaceutical buyers.

Hybrid Automation Solutions For Packaging Machinery Industry Leaders

ABB Ltd.

Rockwell Automation, Inc.

Siemens AG

Schneider Electric SE

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Rockwell Automation announced a USD 150 million investment to expand its packaging robotics research center in Wisconsin.

- December 2024: Siemens acquired Opcenter Advanced Planning for USD 280 million to strengthen digital factory scheduling capabilities.

- September 2024: Bosch Rexroth and Microsoft agreed to co-develop cloud predictive-maintenance solutions for packaging machines.

- August 2024: Omron bought IMA Group’s robotics unit for USD 120 million to broaden collaborative robot portfolios.

Global Hybrid Automation Solutions For Packaging Machinery Market Report Scope

| Hardware |

| Software |

| Services |

| Filling and Dosing Machines |

| Labeling and Coding Machines |

| Palletizing/Depalletizing Systems |

| Wrapping and Bundling Machines |

| Cartoning and Case-packing Machines |

| Food and Beverage |

| Pharmaceutical and Life Sciences |

| Personal Care and Cosmetics |

| Consumer Electronics |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Packaging Machinery Type | Filling and Dosing Machines | ||

| Labeling and Coding Machines | |||

| Palletizing/Depalletizing Systems | |||

| Wrapping and Bundling Machines | |||

| Cartoning and Case-packing Machines | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceutical and Life Sciences | |||

| Personal Care and Cosmetics | |||

| Consumer Electronics | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the hybrid automation solutions for packaging machinery market in 2025?

The market is expected to reach USD 40.2 billion in 2025 and is forecasted to expand at a 6.49% CAGR through 2030.

Which region will grow the fastest through 2030?

Asia-Pacific posts the highest 8.13% CAGR, propelled by China’s manufacturing upgrade policies and India’s rising consumer demand.

Which packaging machine category is expected to lead growth?

Labeling and coding machines record an 8.53% CAGR due to serialization and track-and-trace mandates.

Why are services outpacing hardware growth?

Outcome-based contracts and predictive maintenance reduce unplanned downtime, propelling services to an 8.95% CAGR compared to hardware’s slower pace.

What is the primary barrier to adoption for small manufacturers?

High capital outlays, often USD 2-5 million per line, remain the biggest hurdle, despite new leasing and subscription models.

How are labor shortages influencing investment decisions?

Turnover rates above 40% in some regions accelerate collaborative robot adoption, reducing payback periods to under two years.

Page last updated on: