Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 18.02 Billion |

| Market Size (2031) | USD 24.22 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Packaging Automation Market Analysis by Mordor Intelligence

The Europe packaging automation market size is estimated at USD 18.02 billion in 2026, and is expected to reach USD 24.22 billion by 2031, at a CAGR of 6.10% during the forecast period (2026-2031). Heightened regulatory demands, especially the EU Packaging and Packaging Waste Regulation (PPWR), converge with rising labor costs and rapid technological progress to reshape capital-spending priorities across European manufacturing. Companies are automating to ensure recyclability compliance, close labor gaps, and shield margins from energy price swings. Line-side digitization, from AI-enabled inspection to cobot palletizing, is creating new competitive baselines. Simultaneously, end-users are expanding their supplier pools to mitigate raw material volatility and cyber risk exposure, thereby raising expectations for integrated, secure, and upgradeable automation solutions. Intensifying buyer scrutiny around the total cost of ownership favors vendors that can bundle hardware, analytics, and lifecycle services into a single value proposition, accelerating consolidation among equipment makers and software specialists.

Key Report Takeaways

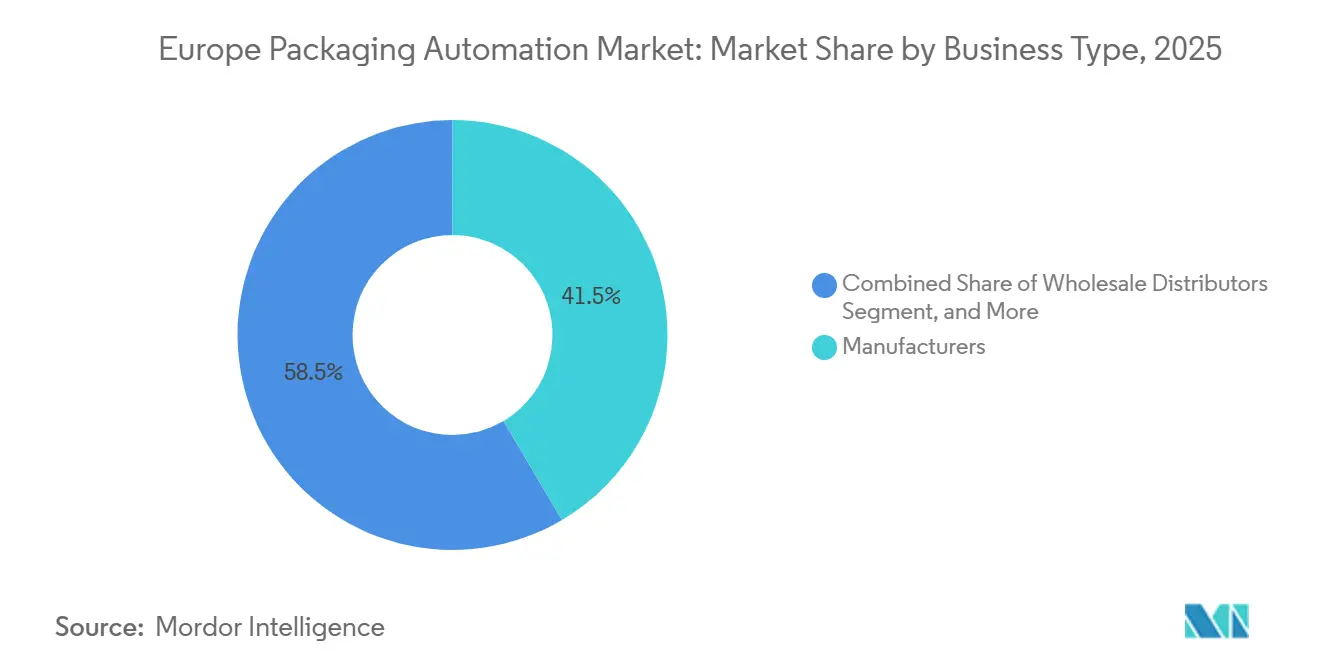

- By business type, manufacturers captured 41.5% of the Europe packaging automation market share in 2025.

- By end-user vertical, the Europe packaging automation market size for pharmaceuticals is projected to grow at a 8.3% CAGR between 2026–2031.

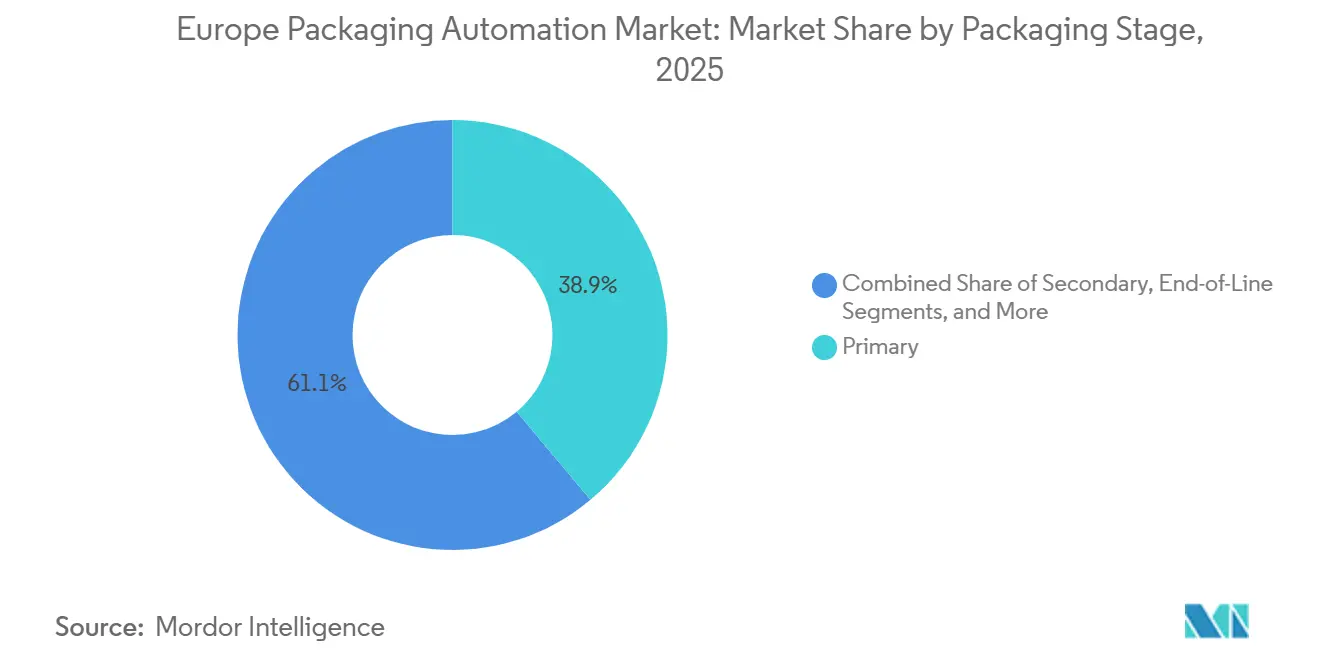

- By packaging stage, primary packaging captured 38.9% of the Europe packaging automation market share in 2025.

- By product type, the Europe packaging automation market size for palletizing and depalletizing systems is projected to grow at a 7.9% CAGR between 2026–2031.

- By geography, Germany captured 37.0% of the Europe packaging automation market share in 2025.

Europe Packaging Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pressure to reduce operating costs | +1.2% | Pan-European, strongest in Germany and France | Medium term (2-4 years) |

| Shrinking skilled-labour pool | +1.8% | Western Europe core | Long term (≥ 4 years) |

| EU packaging-waste and traceability mandates | +1.5% | EU-wide | Short term (≤ 2 years) |

| Mass-customisation and shorter SKUs | +0.9% | Western Europe and Nordics | Medium term (2-4 years) |

| AI-enabled predictive maintenance | +0.6% | Early adopters across Europe | Long term (≥ 4 years) |

| Plug-and-play modular cobots | +0.8% | Germany, France, UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pressure to Reduce Operating Costs

Packaging plants across Europe face sustained wage inflation and energy bills that remain well above 2022 levels, making automation the clearest path to offsetting operating pressure. ABB documented a 25% productivity gain at Striebel & John after deploying a multi-robot packaging island that also trimmed cardboard SKU counts from 15 to 9.[1]ABB, “Electrical Cabinets Packaged Quickly and Flexibly Thanks to ABB Robots,” abb.com Similar gains underpin Krones’ 10.1% 2024 EBITDA margin, despite persistently high polymer prices, signalling that early adopters are widening their cost gap over late movers.

Shrinking Skilled-Labour Pool

Manufacturing employment in the EU fell 2.1% in 2024, with packaging-line technicians among the hardest roles to fill. Bosch Rexroth’s battery-powered mobile cobot station lets one operator oversee tasks that previously needed a three-person team, freeing scarce labour for higher-value work.[2]Bosch Rexroth, “Mobile Cobot Station,” boschrexroth.com ABB’s OmniVance plug-and-play cells further lower the expertise barrier by shipping pre-configured and self-calibrating, enabling SMEs to deploy robots without in-house programmers.

EU Packaging-Waste and Traceability Mandates

The PPWR obliges producers to use fully recyclable packaging by 2030 and meet material-specific recycled-content thresholds. Compliance accelerates demand for high-precision sorting, vision inspection and digital coding capable of tracking every pack to its post-consumer destination.[3]European Parliament, “Packaging and Packaging Waste Regulation Texts Adopted,” europarl.europa.eu In pharmaceuticals, the Falsified Medicines Directive pushes adoption of automated serialization and aggregation suites such as Systech’s semi-automated solution, showcased at Pharmapack 2025.

Mass-Customisation and Shorter SKUs

SKU counts at many European consumer-goods plants have risen by roughly 15% year-on-year since 2023, forcing machinery to execute ultra-fast, tool-less changeovers. Beckhoff’s linear transport modules and B&R’s batch-of-one conveyor technology enable discrete pack handling without halting the line, protecting throughput even as variants proliferate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front capex | -1.4% | Most acute in Southern Europe SMEs | Short term (≤ 2 years) |

| Cyber-security vulnerabilities | -0.8% | EU-wide | Medium term (2-4 years) |

| Lack of interoperability standards | -0.7% | Legacy plants across Europe | Long term (≥ 4 years) |

| Raw-material supply volatility | -0.5% | All regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capex

Turn-key robotic lines can demand EUR 5-10 million, a figure that still deters many mid-sized converters even after grants and tax incentives. Vendors are responding with subscription models that shift spend from capital budgets to OPEX, though long payback windows remain a hurdle for family-owned firms.[4]Infosys Limited, “Modular Plant Automation for Smart Manufacturing,” infosys.com

Cyber-Security Vulnerabilities

The NIS2 directive classifies most packaging plants as “essential entities,” compelling adherence to stringent security protocols and incident-reporting rules. Integrators now embed network segmentation, real-time anomaly detection, and managed patching into new projects, adding cost and design complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Type: Manufacturers Extend Scale Advantage

Manufacturers captured 41.5% of Europe packaging automation market share in 2025 by tying automation spend to overall plant-wide efficiency programs. Their scale supports multi-line roll-outs that amortize software and maintenance across higher volumes. Wholesale distributors primarily adopt automation for palletizing and cross-docking, whereas omni-channel retailers integrate goods-to-person systems with automated bagging to accelerate fulfillment cycles. B2C e-commerce operators, buoyed by EUR 887 billion in regional online sales during 2024, will log an 8.7% CAGR to 2031, the fastest within the segment hierarchy. Investments gravitate toward smart sortation, auto-bagging, and dimensioning modules capable of processing thousands of individualized parcels per hour. Personal document shippers and contract packers remain a niche market but show steady uptake in track-and-trace capable printers and tamper-evident sealers.

A growing share of original manufacturers is revisiting make-versus-buy decisions, outsourcing secondary or tertiary packaging to co-packers yet retaining ownership of core filling and closing operations. That shift widens the addressable base for modular solutions that can be redeployed as order books fluctuate, ensuring vendors maintain recurring revenue from retrofits and line extensions.

By End-User Vertical: Food Dominate as Pharma Ramps Up

Food accounted for 32.18% of market share in the Europe packaging automation market, anchored by continuous-motion fillers, rotary cappers, and wrap-around case packers optimized for high-volume SKUs. Coca-Cola’s 2025 upgrades in Genshagen and Lüneburg feature 60,000-container-per-hour glass lines, underscoring the ongoing appetite for high-speed systems. Meanwhile, the pharmaceutical sector, driven by serialization and the demand for personalized medicines, is expected to expand at an 8.3% CAGR through 2031. Automated aggregation, inspection, and cold-chain compliant palletizing are top investment areas, with Systech and ABB piloting multi-camera vision suites that certify every bundle before release.

Cosmetics and personal care brands are adopting flexible cartoners and print-on-demand sleeve applicators to strike a balance between premium aesthetics and the increasing number of SKUs. Household chemical and detergent makers focus on leak-proof dosing and space-saving secondary packs to navigate tightening transportation emission rules. Confectionery and bakery outfits deploy gentle-handling delta robots and ultrasonic bag sealers to preserve fragile products at speed, while 3PL providers scale up automated mailers and label applicators for omnichannel clients.

By Packaging Stage: End-of-Line Gains Momentum

Primary operations retained a 38.9% share in 2025, thanks to entrenched demand for fillers, seamers, and vacuum sealers that protect product integrity at source. However, end-of-line solutions are outpacing all other stages at a 7.1% CAGR as plants chase labour elimination in palletizing, stretch-wrapping, and intralogistics. The Europe packaging automation market size for robotic palletizers alone is rising swiftly, supported by systems like AWL’s vision-guided unit capable of 800 parcels per hour. Secondary packaging maintains relevance through wrap-around and tray packers that consolidate retail-ready bundles, while tertiary and warehouse automation integrate AGVs with WMS platforms to optimize dock-to-dock cycle times.

Manufacturers increasingly specify holistic layouts where primary, secondary, and end-of-line assets share harmonized controls, enabling single-pane-of-glass monitoring and predictive maintenance. That architectural shift rewards suppliers capable of plug-and-produce interoperability via open protocols such as OPC UA PackML.

By Product Type: Filling Steady, Palletizing Surging

Filling machines account for 27.8% of Europe packaging automation market size, underpinned by sustained beverage and viscous-food throughput requirements. Servo-driven volumetric fillers and aseptic bloc systems remain core CAPEX items owing to their direct link with revenue capacity. Label-and-code equipment enjoys consistent pull from regulatory batch marking and sustainability logos, whereas form-fill-seal platforms cater to flexible pouches, gaining ground in snacks and nutraceuticals.

Palletizing and depalletizing units post the sharpest expansion at 7.9% CAGR. Vision-equipped cobots now handle mixed-height packs without custom grippers, reducing changeover time and floor space. Case packers are evolving toward delta-robot top-load architectures that manage multiple SKU patterns on a single frame. Bagging, capping, and stretch-wrapping hold incremental gains, while inline inspection and X-ray systems see heightened demand as producers tie food-safety KPIs to brand equity.

Geography Analysis

Germany led the European packaging automation market with a 37.0% revenue share in 2025, driven by its established machinery ecosystem and its status as an exporter. Flagship projects such as Krombacher’s EUR 100 million brewery modernization, which integrates advanced pattern formation and material-flow software, illustrate continued domestic reinvestment even amid a subdued macro backdrop. Germany also benefits from clustering effects around Bavaria and Baden-Württemberg, where engineering talent, component suppliers, and university research and development form dense networks that accelerate product cycles.

France is the fastest-growing national market, projected to grow at an 8.2% CAGR through 2031. Rapid adoption reflects the country’s aggressive stance on waste reduction, including plastic taxes and extended producer responsibility schemes that spur investment in traceable, recyclable packaging systems. Food manufacturers are expanding the use of cobots for palletizing, while pharmaceutical clusters in Lyon and Île-de-France are deploying next-generation inspection tunnels to meet export market compliance.

The United Kingdom remains a key adopter despite navigating post-Brexit customs complexity. Demand centers on serialized pharma packs, spirit bottling and specialty-chem drums. Italy leverages long-standing expertise in boutique machinery for luxury foods, wines and cosmetics, prompting above-average penetration of servo-driven cartoners and flow-wrappers. Spain emphasizes energy-efficient retrofits, increasingly coupling variable-speed drives with gas-phase sterilization to reconcile productivity with carbon caps.

Competitive Landscape

Industry structure is fragmented. ABB, Siemens, and Rockwell Automation apply cross-industry control and software expertise to win multi-line contracts that bundle SCADA, drives, and cybersecurity layers. Krones focuses squarely on the beverage and liquid-food sectors, posting 12.1% revenue growth in 2024 on the back of retrofit upgrades and Netstal’s acquisition of its injection-molding portfolio, which broadens coverage into preform production.

Strategic moves coalesce around three themes, which include platformization, ABB’s OmniVance cells ship pre-calibrated, lowering commissioning days by up to 70%; vertical integration, Krones’ Netstal deal pulls moulding in-house, capturing adjacent margin; and cyber-secure offerings, Siemens’ Industrial Edge embeds zero-trust frameworks to address NIS2 mandates. Consolidation is set to continue as mid-tier machine builders lacking software depth seek protective mergers or risk being sidelined when end-users source end-to-end solutions from a single vendor.

Emerging challengers target AI vision and predictive analytics. Several Germany-based start-ups offer edge-deployed quality-control models that self-train in hours, reducing false rejects. Partnerships with cloud providers extend these analytics to fleet-wide dashboards, creating service annuities for integrators while enabling users to shift toward condition-based maintenance. Vendors able to combine mechatronics with data-layer value are expected to outperform over the forecast horizon.

Europe Packaging Automation Industry Leaders

JLS Automation

Mitsubishi Corporation

Rockwell Automation

DESTACO

Swisslog Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Krones posted 12.1% 2024 revenue growth to EUR 5.29 billion and guided 7–9% expansion for 2025 on robust beverage automation demand.

- February 2025: Bosch Rexroth unveiled a 7-axis mobile cobot station capable of four-hour untethered operation, addressing labour deficits on packaging lines.

- January 2025: Systech showcased a semi-automated aggregation platform at Pharmapack to streamline EU serialization compliance.

- January 2025: Coca-Cola Europacific Partners Germany commissioned three high-speed Krones lines, including a 60,000-container-per-hour glass system in Lüneburg.

Europe Packaging Automation Market Report Scope

The Europe packaging automation market refers to the adoption of automated technologies and machinery across various stages of packaging processes, aimed at improving efficiency, reducing manual intervention, and ensuring consistency in packaging operations. This market encompasses a wide range of industries and applications, including food, beverages, pharmaceuticals, cosmetics, and logistics, among others.

Europe Packaging Automation Market Report is Segmented by Business Type (Manufacturers, Wholesale Distributors, Omni-Channel Retailers, B2B e-Commerce Retailers, B2C e-Commerce Retailers, Personal-Document Shippers, and Other Business Types), End-User Vertical (Food, Beverages, Pharmaceuticals, Cosmetics and Personal Care, Household and Detergents, Chemical, Warehousing and 3PL, and Other End-User Vertical), Packaging Stage (Primary, Secondary, End-of-Line, and Tertiary and Intralogistics), Product Type (Filling Machines, Labelling and Coding, Form-Fill-Seal, Bagging and Pouching, Palletizing and Depalletizing, and Other Product Types), and Country.

By Business Type

| Manufacturers |

| Wholesale Distributors |

| Omni-channel Retailers |

| B2B e-Commerce Retailers |

| B2C e-Commerce Retailers |

| Personal-Document Shippers |

| Other Business Types |

By End-User Vertical

| Food |

| Beverages |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Household and Detergents |

| Chemical |

| Warehousing and 3PL |

| Other End-User Verticals |

By Packaging Stage

| Primary (Filling/Sealing) |

| Secondary (Cartoning/Case-Packing) |

| End-of-Line (Palletising/Stretch-Wrap) |

| Tertiary and Intralogistics |

By Product Type

| Filling Machines |

| Labelling and Coding |

| Form-Fill-Seal (H/VFFS) |

| Bagging and Pouching |

| Palletising and Depalletising |

| Other Product Types |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Business Type | Manufacturers |

| Wholesale Distributors | |

| Omni-channel Retailers | |

| B2B e-Commerce Retailers | |

| B2C e-Commerce Retailers | |

| Personal-Document Shippers | |

| Other Business Types | |

| By End-User Vertical | Food |

| Beverages | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Household and Detergents | |

| Chemical | |

| Warehousing and 3PL | |

| Other End-User Verticals | |

| By Packaging Stage | Primary (Filling/Sealing) |

| Secondary (Cartoning/Case-Packing) | |

| End-of-Line (Palletising/Stretch-Wrap) | |

| Tertiary and Intralogistics | |

| By Product Type | Filling Machines |

| Labelling and Coding | |

| Form-Fill-Seal (H/VFFS) | |

| Bagging and Pouching | |

| Palletising and Depalletising | |

| Other Product Types | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe packaging automation market?

The Europe packaging automation market stands at USD 18.02 billion in 2026 and is forecast to hit USD 24.22 billion by 2031.

Which business-type segment is growing fastest?

B2C e-commerce retailers are projected to record a 8.7% CAGR between 2026 and 2031 as online shopping volumes lift demand for automated parcel packaging.

Why is end-of-line automation expanding more quickly than primary packaging?

Labour shortages and e-commerce fulfillment pressures make robotic palletizing and stretch-wrapping attractive, driving a 7.1% CAGR for end-of-line equipment through 2031.

How do EU regulations influence automation investment?

The PPWR and serialization mandates compel producers to add traceability, inspection and recyclable-material handling capabilities, turning automation into a compliance necessity rather than a discretionary upgrade.

Which country leads the market and which is growing fastest?

Germany leads with 37.0% revenue share in 2025, while France is the fastest-growing geography at an 8.2% CAGR over 2026-2031.

Page last updated on: