Automated Mining Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

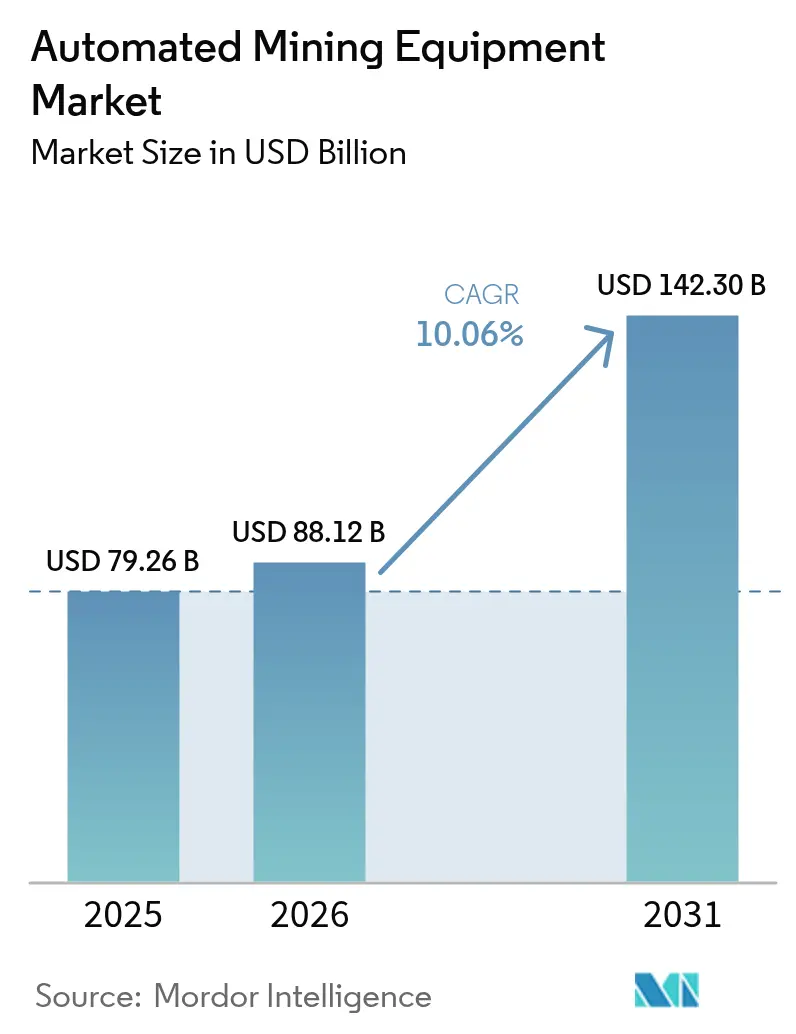

| Market Size (2026) | USD 88.12 Billion |

| Market Size (2031) | USD 142.30 Billion |

| Growth Rate (2026 - 2031) | 10.06% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Mining Equipment Market Analysis by Mordor Intelligence

The automated mining equipment market size is expected to grow from USD 79.26 billion in 2025 to USD 88.12 billion in 2026 and is forecast to reach USD 142.3 billion by 2031 at a 10.06% CAGR over 2026-2031. Continued investment in sensor-rich haulage fleets, strict safety rules in mature mining hubs, and aggressive productivity targets in high-volume iron-ore, copper, and coal basins anchor demand for connected autonomy. Capital is shifting toward edge-enabled fleet-management software because remote supervision keeps trucks moving through shift changes, meals, and blasting windows. High-bandwidth private-LTE and 5G-Advanced networks are now standard at new greenfield pits, reducing latency for obstacle detection and enabling mixed-vendor fleets. Autonomous underground loaders let mines recover deeper orebodies without exposing crews to heat, ground-fall, or diesel-particulate hazards, aligning with regulators’ zero-harm mandates. Competitive positioning is moving away from ultra-class truck payloads toward software moats built on perception algorithms and predictive-maintenance datasets, fragmenting the value chain and lowering switching costs for mid-tier operators.

Key Report Takeaways

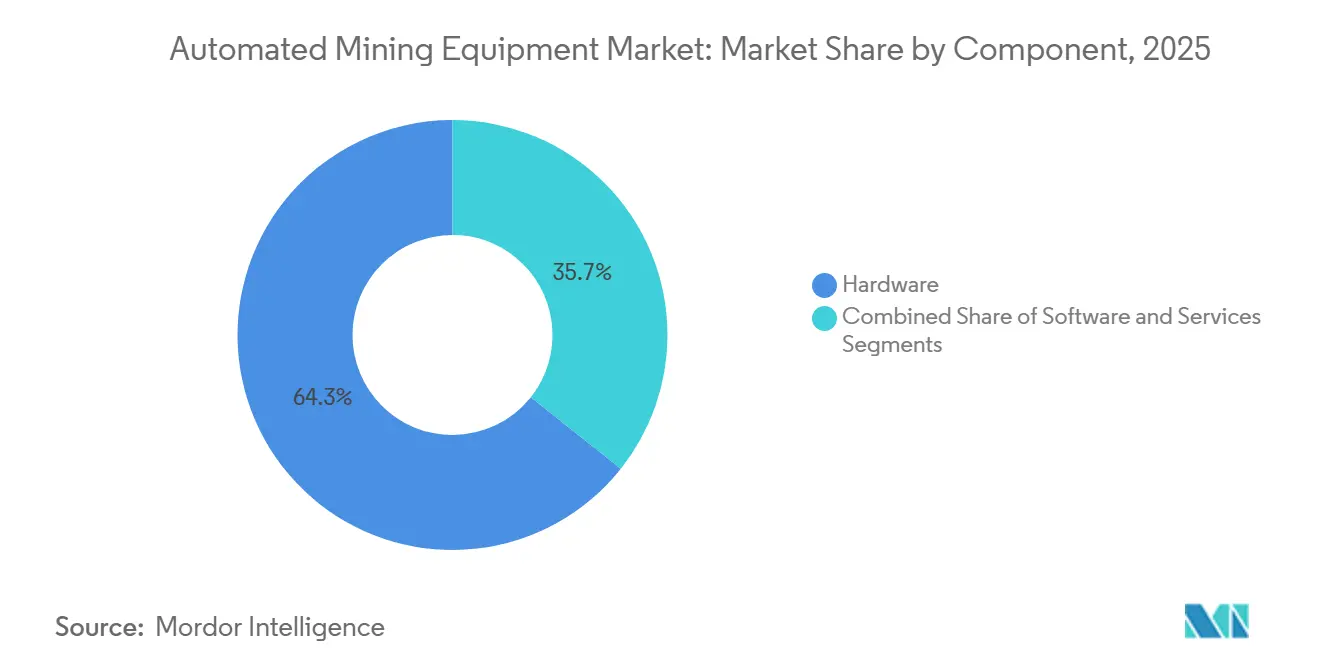

- By component, hardware led with 64.32% of 2025 revenue, while software is expanding at an 11.07% CAGR through 2031.

- By mining technique, surface mining held 68.71% of 2025 revenue; underground mining is advancing at a 10.59% CAGR over 2026-2031.

- By autonomy level, Level 2 systems accounted for 43.38% of 2025 deployments, yet Level 4 platforms are growing at a 10.91% CAGR.

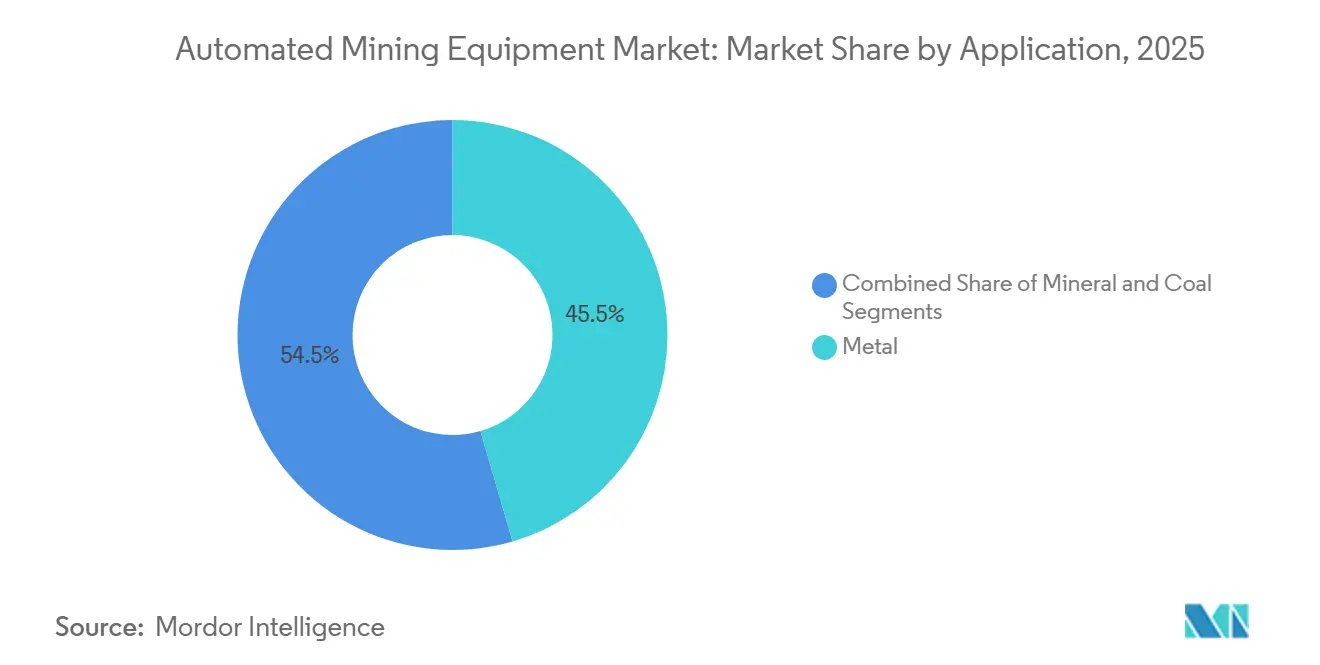

- By application, metal mining captured 45.49% of 2025 demand, whereas coal mining is accelerating at a 10.96% CAGR through the forecast horizon.

- By fleet size, mid-scale groups of 25-99 units represented 40.51% of 2025 installations, but small-scale fleets under 25 units are rising at an 11.07% CAGR.

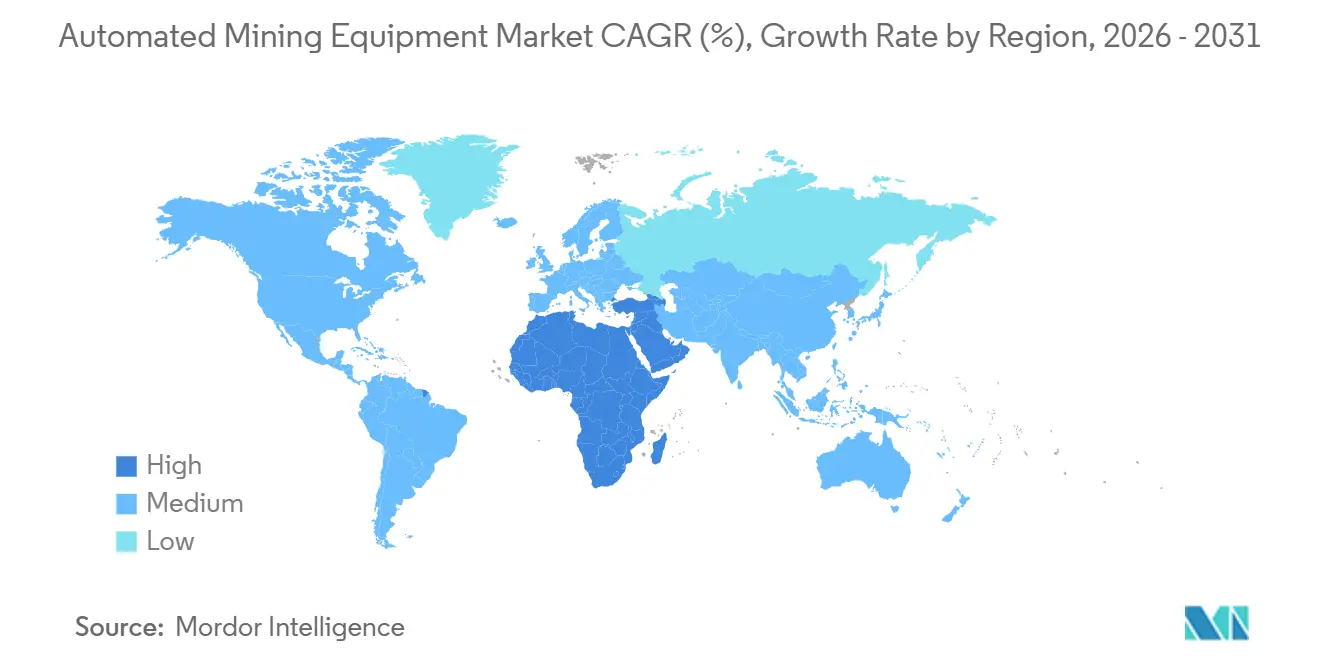

- By geography, Asia-Pacific commanded 39.86% of 2025 revenue, while the Middle East and Africa region is pacing the field at an 11.22% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automated Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Productivity and Worker Safety | +2.80% | Global, with concentration in Australia, Canada, Chile, South Africa | Medium term (2-4 years) |

| Rising Labor Shortages in Mature Mining Regions | +2.30% | North America, Australia, Europe | Long term (≥ 4 years) |

| Cost-Reduction Initiatives via Automation | +1.90% | Global, particularly Asia-Pacific and South America | Short term (≤ 2 years) |

| Advancements in Sensor and AI Integration for Autonomous Haulage | +1.60% | Global, early adoption in Australia, North America | Medium term (2-4 years) |

| ESG-Driven Shift to Remote Zero-Harm Mines | +1.20% | Global, regulatory pressure strongest in Europe, Australia | Long term (≥ 4 years) |

| Surge in Autonomous Underground LHD Retrofits at Mid-Tier Sites | +0.90% | Australia, Canada, South Africa, Sweden | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Productivity and Worker Safety

Fatality rates in global mining averaged 0.03 per million hours worked in 2024, yet underground sites still logged injury frequencies three to four times higher than surface operations. Western Australian and Ontario regulators now require risk-mitigation plans that favour remote operation rather than human entry into haulage drifts. Autonomous load-haul-dump machines have already lowered lost-time injuries by 31% at South African platinum mines using Sandvik’s AutoMine platform, and autonomous truck fleets in Australia’s Pilbara corridor consistently run through shift changeovers, lifting asset utilization by about 15% compared with crewed fleets,[1]Jacob Blomqvist, “AutoMine Raises Underground Safety,” Sandvik Mining and Rock Solutions, SANDVIK.COM Capital budgets therefore allocate up to 18% of sustaining spend to automation retrofits, reversing a century-old preference for labour expansion.

Rising Labor Shortages in Mature Mining Regions

Canada faced a shortfall of 80,000 mining workers by 2025, while Australia projected a 24,000-person deficit for technical roles by 2027. Nevada Gold Mines illustrates the new operating model: Komatsu’s FrontRunner Level 4 fleet enables one remote supervisor to oversee fifteen trucks, trimming the local driver roster from 45 to 7.[2]“FrontRunner Autonomous Haulage System,” Komatsu Ltd., KOMATSU.COM Without such automation, mines in aging labour pools would curtail output or pay unsustainable wage premiums, making autonomy a production-continuity imperative rather than a discretionary cost-saving tool.

Cost-Reduction Initiatives via Automation

Vale’s Carajás complex scaled an autonomous Cat MineStar fleet from 30 to 90 trucks, harvesting 15% productivity gains and 7.5% diesel savings thanks to optimized speed profiles and predictive-maintenance alerts.[3]“Vale Autonomous Fleet Expansion,” Vale S.A., VALE.COM Retrofit economics break even within two years when iron ore trades above USD 60 per metric ton or copper above USD 3.50 per pound, because each USD 0.8-1.2 million truck upgrade replaces three full-time drivers, lengthens tire life, and trims idle fuel burn. Modular autonomy kits also let junior miners adopt driverless haulage without the balance-sheet strain of buying new equipment.

Advancements in Sensor and AI Integration for Autonomous Haulage

Komatsu fuses lidar, millimeter-wave radar, and stereo cameras to detect objects as small as 0.3 m at 200 m, allowing trucks to pass through active blast zones safely. Caterpillar’s MineStar Edge, released in December 2025, pushes perception processing to on-board edge computers, cutting control-loop latency from 150 ms to under 20 ms. China’s Yimin coal mine demonstrates that high-density sensor payloads and 5G-Advanced links now scale beyond Western majors, signalling a shift from rule-based to learning-based autonomy capable of coping with weekly pit-geometry changes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX and Complex Integration | -1.40% | Global, acute in South America, Africa, smaller operators | Short term (≤ 2 years) |

| Cyber-Security Vulnerabilities in Connected Fleets | -0.90% | Global, highest risk in remote sites with limited IT infrastructure | Medium term (2-4 years) |

| Legacy Fleet Heterogeneity Hampers Interoperability | -0.70% | North America, Australia, Europe (mature mining regions) | Medium term (2-4 years) |

| Limited High-Bandwidth Connectivity in Deep-Underground Mines | -0.50% | Underground operations globally, particularly in Canada, Australia, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Complex Integration

Full-fleet conversions cost more than USD 5 million per truck once vehicle replacement, dispatch-system upgrades, and remote-operations centers are included. Mixed-vendor fleets raise middleware spend by an extra USD 2 million because dispatch logic must synchronize autonomous and manual units at intersections, extending payback timelines and discouraging mid-tier miners from immediate adoption.

Cyber-Security Vulnerabilities in Connected Fleets

Ransomware incidents climbed 47% between 2024 and 2025, forcing temporary suspensions when attackers encrypted autonomous-fleet databases. A 2024 GPS-spoofing attack in Western Australia stopped production for 12 hours, proving that even air-gapped networks are exposed if satellite receivers accept unauthenticated signals. With fewer than ten ISO 27001-certified mine sites worldwide, most autonomous operations remain susceptible to malicious commands that could override braking or steering systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Outpaces Hardware on Margin Expansion

Software revenue in the automated mining equipment market is scaling at the highest rate, advancing at an 11.07% CAGR through 2031 as fleet-management platforms shift from perpetual licenses to per-hour subscriptions. That model delivers gross margins above 70%, far exceeding the 25-35% margins earned on steel-intensive trucks and loaders. Services such as training and remote monitoring complement software by offloading expertise from miners to vendors, deepening lock-in, and smoothing recurring revenue streams.

Hardware still underpins the automated mining equipment market, with robotic trucks, loaders, and drillers accounting for 64.32% of 2025 turnover. Original-equipment manufacturers are embedding over-the-air update capability, so their equipment becomes the physical node for value-adding analytics, letting them defend share against pure-play software firms. Sandvik’s battery-electric concept loader illustrates the convergence: an emissions-free chassis bundled with autonomous navigation, delivered as an integrated performance contract rather than a one-time sale.

By Mining Technique: Underground Automation Closes the Surface Gap

Surface operations hold the majority revenue share because open pits allow reliable GPS coverage, straightforward haul roads, and high-payload trucks. Even so, underground mines are growing faster at a 10.59% CAGR because automation solves acute safety problems linked to ground-falls and poor ventilation. LiDAR-based simultaneous-localization and mapping now replaces satellite navigation, letting loaders operate 750 m below surface and achieve round-the-clock cycles.

The automated mining equipment market size attached to underground projects, therefore, expands every time deeper orebodies move into production. Autonomous loaders deployed at Finland’s Kittilä gold mine run through blasting and re-entry delays, adding three to four extra productive hours daily. As a result, mine planners are revising cut-off grades, converting marginal resources to reserves because labour exposure is no longer the primary constraint.

By Autonomy Level: Level 4 High Automation Leapfrogs Incremental Steps

Level 2 partial-automation solutions still dominate the automated mining equipment market share at 43.38% in 2025, mainly via collision-avoidance and auto-dump functions. However, miners moving directly to Level 4 gain larger productivity jumps because a single control-room operator can supervise multiple trucks. Nevada Gold Mines’ 2025 rollout shows fifteen-to-one supervision ratios are practical, reshaping labour economics.

Level 5 remains experimental due to regulatory caution over removing all human override, but continuous improvement in perception algorithms and edge compute suggests limited-use-case pilots could reach commercial readiness after 2031. For now, the fast uptake of Level 4 fleets is widening a performance gap between early adopters and laggards, reinforcing a two-speed automated mining equipment market.

By Application: Coal Mining Automation Accelerates on Labor Attrition

Metal mining generated 45.49% of 2025 spending because copper and iron-ore megaprojects possess the scale to absorb high initial automation costs. Coal producers, however, are adopting autonomy at a quicker 10.96% CAGR because younger workers shun underground coal jobs. China’s Yimin mine demonstrates that coupling battery-electric trucks with 5G-Advanced links can eliminate diesel-particulate penalties and cut ventilation loads, making autonomy doubly attractive.

The automated mining equipment market size tied to coal is also supported by trolley-assist systems that slash diesel burn by up to 50% on uphill hauls. With thermal-coal margins squeezed by carbon policies, those savings often mark the difference between continued operation or closure, driving aggressive automation rollouts in Appalachia, Inner Mongolia, and the Bowen Basin.

By Fleet Size: Small-Scale Deployments Democratize Autonomy Access

Mid-scale deployments (25-99 units) currently dominate installations, but modular kits now let small-scale fleets under 25 units post the fastest 11.07% CAGR. Heidelberg Materials’ German quarry proves five-truck fleets can break even in 18 months when open-architecture control stacks avoid proprietary lock-in.

This democratization is altering automated mining equipment industry dynamics: nimble contractors that master autonomy can under-bid incumbents on haulage and loading tenders. Original-equipment vendors therefore court small customers with subscription bundles combining hardware, software, and training to preserve share as the automated mining equipment market expands down the size curve.

Geography Analysis

Asia-Pacific anchors the automated mining equipment market with 39.86% of 2025 revenue, led by Australia’s Pilbara corridor where more than 880 autonomous trucks haul iron ore. China’s state-owned coal and metals firms added 326 driverless units by mid-2024 after deploying private-5G networks that provide sub-10 ms vehicle-to-infrastructure links. India is piloting systems at Coal India subsidiaries but waits for liability clarity before mass rollout. Japan and South Korea export technology rather than deploy fleets domestically, while Singapore hosts regional software hubs that support mines across Southeast Asia and Oceania.

Middle East and Africa is the fastest-growing region at an 11.22% CAGR because Saudi Arabia and South Africa link mining licenses to zero-harm and local-content targets achievable only with remote operations. South Africa already fields about 180 smart mines, and Siemens forecasts that 30-40% of the nation’s mobile equipment could become autonomous by 2040. Ghana, Botswana, and the Democratic Republic of Congo are running pilot projects but must first expand fiber or 5G coverage to deep-pit and underground zones.

South America outpaces the global automated mining equipment market rate as Chile’s USD 83.1 billion project pipeline mandates autonomy in new copper projects, while Brazil’s iron-ore expansions incorporate driverless haulage into 60% of environmental-impact filings. Vale’s ramp-up from 30 to 150 autonomous trucks illustrates scale economics, and Argentina’s lithium salars are choosing small retrofit fleets to overcome workforce scarcity at 4,000-m elevations. North America remains the second-largest region by value, with Alberta’s oil-sands trucks and Nevada’s gold mines leading adoption, and Europe remains smaller but influential thanks to Sweden’s Arctic installations that validate equipment in extreme cold.

Competitive Landscape

Roughly 60% of autonomous-hardware shipments in 2025 came from the top five vendors Caterpillar, Komatsu, Sandvik, Epiroc, and Hitachi Construction Machinery yet software-only specialists such as Wenco, RPMGlobal, and Autonomous Solutions fragment the stack by licensing fleet-management layers that run mixed brands. Incumbents answer with vertical integration: Komatsu and Epiroc formed a joint venture in January 2026 to co-develop underground autonomy, pooling perception patents and accelerating Level 4 releases.

Technology is the decisive lever. Caterpillar’s MineStar Edge slashes control-loop latency to under 20 ms by pushing compute to the truck edge, while Sandvik’s battery-electric loader removes diesel particulates in confined stopes, giving early adopters a compliance advantage. Chinese manufacturers XCMG and Sany undercut Western vendors by up to 40% on sticker price and include autonomy modules as standard, targeting cost-sensitive coal operators.

Value capture is therefore tilting toward data: vendors that own predictive-maintenance datasets and sensor-fusion algorithms lock customers into decade-long support contracts. This dynamic encourages multi-year service level agreements over outright equipment sales, raising switching costs even as interoperable software theoretically lowers them. The automated mining equipment market consequently balances moderate hardware concentration with increasing software fragmentation.

Automated Mining Equipment Industry Leaders

Rockwell Automation Inc.

ABB Ltd.

Autonomous Solutions Inc. (ASI Mining)

Hexagon AB

Trimble Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Nevada Gold Mines partnered with Komatsu and Nokia to deploy FrontRunner AHS across 300- and 230-tonne trucks, illustrating a strategy to marry fleet expansion with ultra-low-latency 5G for real-time optimization

- May 2025: Sandvik launched AutoMine Surface Fleet to extend its underground automation franchise into drill-and-blast surface rigs, aiming to capture adjacent revenue streams while leveraging existing software assets

- April 2025: Epiroc secured its largest-ever autonomous and electric equipment contract, signaling confidence in bundled zero-emission plus autonomy offerings that address both ESG and productivity goals

- February 2025: Deswik enhanced its ORB Live module to integrate autonomous dispatch with cave monitoring, positioning the firm as a one-stop software orchestrator for underground digital twins

Global Automated Mining Equipment Market Report Scope

The Automated Mining Equipment Market Report is Segmented by Component (Hardware including Excavators, Load Haul Dump, Robotic Truck, Drillers and Breakers, and Other Equipment; Software; Services), Mining Technique (Surface Mining, Underground Mining), Application (Metal, Mineral, Coal), Autonomy Level (Level 1 to Level 5), Fleet Size (Small-Scale, Mid-Scale, Large-Scale), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Excavators |

| Load Haul Dump | |

| Robotic Truck | |

| Drillers and Breakers | |

| Other Equipment | |

| Software | |

| Services |

| Surface Mining |

| Underground Mining |

| Metal |

| Mineral |

| Coal |

| Level 1 - Operator Assist |

| Level 2 - Partial Automation |

| Level 3 - Conditional Automation |

| Level 4 - High Automation |

| Level 5 - Full Automation |

| Small-Scale (Less Than 25 Units) |

| Mid-Scale (25-99 Units) |

| Large-Scale (More Than Equal to 100 Units) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Singapore | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Hardware | Excavators |

| Load Haul Dump | ||

| Robotic Truck | ||

| Drillers and Breakers | ||

| Other Equipment | ||

| Software | ||

| Services | ||

| By Mining Technique | Surface Mining | |

| Underground Mining | ||

| By Application | Metal | |

| Mineral | ||

| Coal | ||

| By Autonomy Level | Level 1 - Operator Assist | |

| Level 2 - Partial Automation | ||

| Level 3 - Conditional Automation | ||

| Level 4 - High Automation | ||

| Level 5 - Full Automation | ||

| By Fleet Size | Small-Scale (Less Than 25 Units) | |

| Mid-Scale (25-99 Units) | ||

| Large-Scale (More Than Equal to 100 Units) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Singapore | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What revenue is automated mining equipment projected to generate by 2031?

Global sales are forecast to reach USD 142.3 billion by 2031, up from USD 88.12 billion in 2026 at a 10.06% CAGR.

Which product area is expanding the fastest?

Fleet-management and predictive-maintenance software is growing at 11.07% CAGR, outpacing hardware and services.

Why are operators moving directly to Level 4 autonomy?

Level 4 lets one remote supervisor oversee up to 15 trucks, removing in-cab labor and lifting truck utilization by roughly 15%.

What is the biggest hurdle for smaller miners?

Upfront capital of more than USD 5 million per truck and complex mixed-fleet integration can delay payback and deter adoption.

Which region is likely to post the highest growth through 2031?

Middle East and Africa is advancing at an 11.22% CAGR, driven by zero-harm mandates in Saudi Arabia and South Africa.

How does autonomy improve on-site safety and productivity?

Driverless loaders and trucks cut lost-time injuries by about 31% in underground mines and keep hauling through shift changes, boosting output without adding crews.

Page last updated on: