Mining Laboratory Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

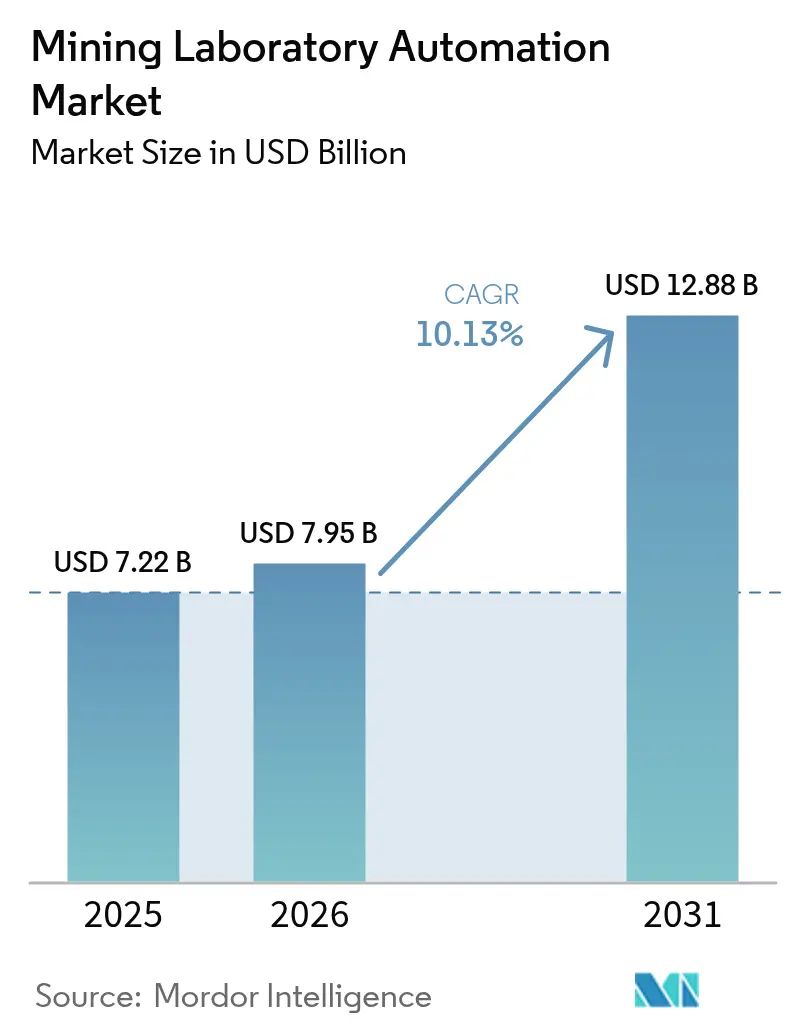

| Market Size (2026) | USD 7.95 Billion |

| Market Size (2031) | USD 12.88 Billion |

| Growth Rate (2026 - 2031) | 10.13% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mining Laboratory Automation Market Analysis by Mordor Intelligence

Mining Laboratory Automation market size in 2026 is estimated at USD 7.95 billion, growing from 2025 value of USD 7.22 billion with 2031 projections showing USD 12.88 billion, growing at 10.13% CAGR over 2026-2031. Robust demand stems from mine-site digitalization programs that seek faster turn-around of assays, tighter grade control, and lower human-exposure to hazardous environments. Autonomous sampling systems now link directly with cloud-hosted LIMS platforms, enabling pit-to-port traceability that boosts ore recovery, trims re-handling costs, and strengthens ESG compliance. Mid- and large-scale miners are digitizing laboratories to counter scarce skilled labor, while containerized labs shorten development timelines for green-field projects. Convergence of robotics, AI, and modular instrumentation is creating scalable ecosystems that lower total cost of ownership and give early adopters 18–24-month payback horizons. Investment momentum is reinforced by regional policy pushes, particularly in Australia, Chile, Saudi Arabia, and Ghana, where regulators and sovereign funds are steering capital toward automated mining value chains.

Key Report Takeaways

- By product category, robotics led with 33.60% revenue share in 2025; LIMS is forecast to expand at a 12.15% CAGR through 2031.

- By automation level, modular systems held 50.20% of the Mining Laboratory Automation market share in 2025, while total lab automation is projected to grow at 14.51% CAGR to 2031.

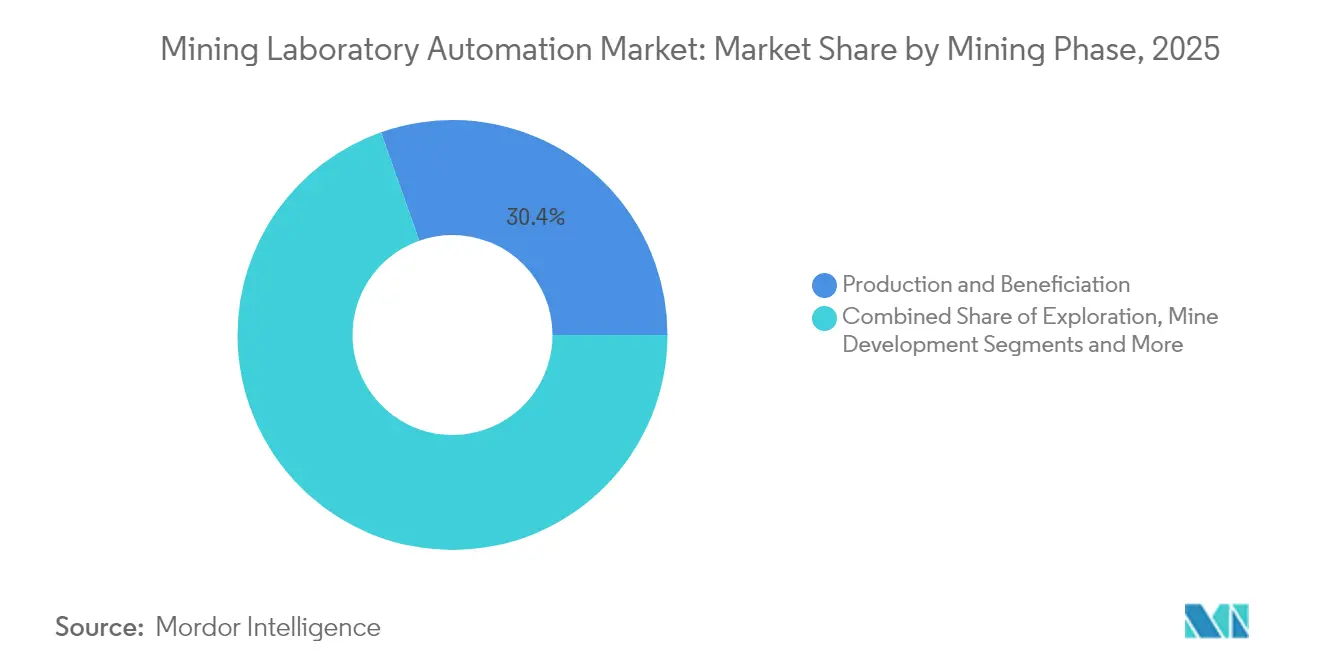

- By mining phase, production and beneficiation accounted for 30.40% share of the Mining Laboratory Automation market size in 2025; exploration and grade control is advancing at a 12.98% CAGR through 2031.

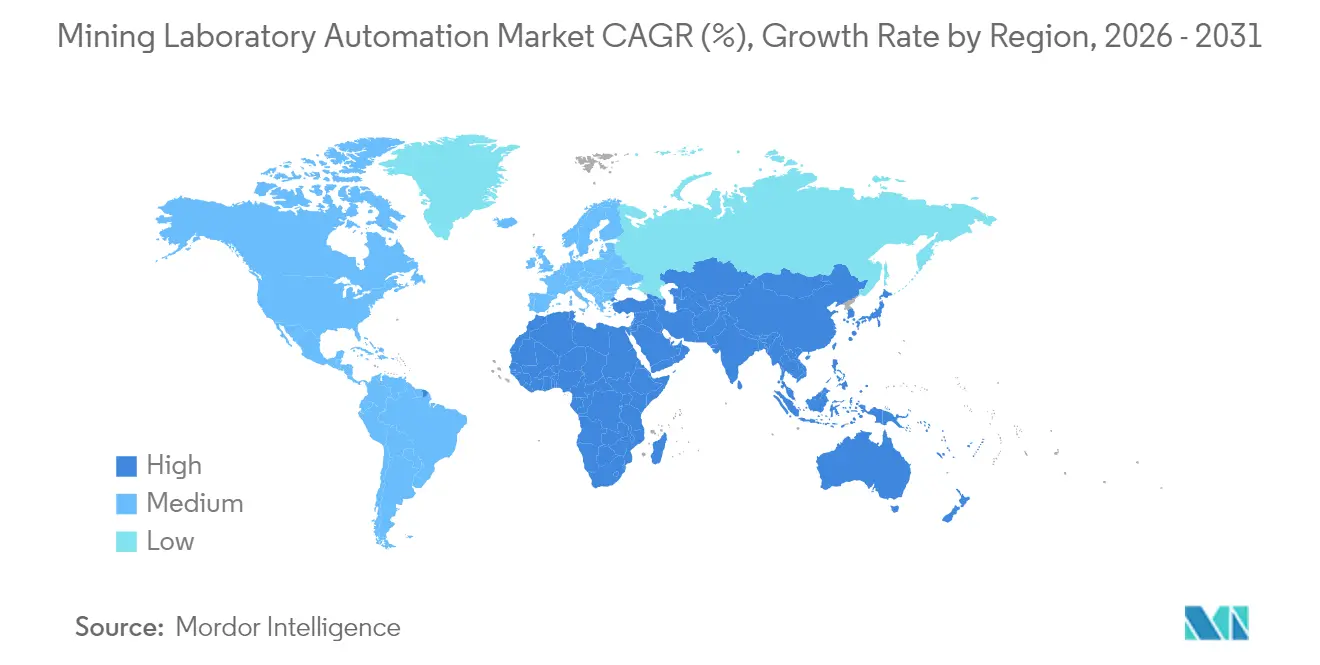

- By geography, Asia-Pacific commanded 31.20% share in 2025, whereas Middle East & Africa posts the fastest 14.86% CAGR to 2031.

- By end-user, large enterprises captured 57.10% of the Mining Laboratory Automation market size in 2025; mid-tier and junior miners represent the fastest-growing user group at 13.88% CAGR.

- FLSmidth, Thermo Fisher Scientific, and Bruker collectively held 25.60% Mining Laboratory Automation market share in 2025, reflecting a moderately fragmented landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mining Laboratory Automation Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Digital-first "Pit-to-Port" Sampling Initiatives in Australia | 1.8% | Australia, with spillover to Canada and Brazil | Medium term (2-4 years) |

| Mandatory On-site Assay Turn-around in Chilean Copper Mines | 1.5% | Chile, Peru, with adoption in APAC copper operations | Short term (≤ 2 years) |

| Rapid Grade-Control Needs in West African Gold Super-Pits | 1.2% | West Africa, expanding to East Africa and South America | Medium term (2-4 years) |

| Stricter Tailings-Dam Monitoring Rules in Brazil | 0.9% | Brazil, with regulatory spillover to global operations | Long term (≥ 4 years) |

| Rise of Containerized "Hub-and-Spoke" Labs Across the Nordics | 0.7% | Nordic countries, expanding to remote mining regions globally | Long term (≥ 4 years) |

| AI-Enabled Predictive Maintenance for Robotic Sample Prep | 1.4% | Global, with early adoption in Australia and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-first “Pit-to-Port” Sampling Initiatives in Australia

Mining majors now integrate autonomous drills, automated crushers, and robotic fire-assay lines into unified data backbones that push geochemical results into planning software within minutes. Rio Tinto reports annual savings of USD 200 million after deploying predictive maintenance on robotic lab assets, while BHP’s Spence mine in Chile logged three months of full autonomy with zero safety incidents in 2024. Continuous data flow removes manual choke points, cuts contamination risk by 40%, and lifts ore recovery 3–5% in large iron-ore operations.[1]BHP Editorial Team, “Artificial Intelligence is unearthing a smarter future,” bhp.com

Mandatory On-site Assay Turn-around in Chilean Copper Mines

Four-hour regulatory limits for grade-control assays have forced Chilean sites to adopt automated sample preparation and portable XRF units capable of 90-minute results. Codelco’s USD 2.5 billion agreement with ABB bundles electrification and laboratory automation, giving early movers 2–3-point boosts in copper recovery and shaping similar mandates in Peru.[2]Mining Digital Staff, “ABB and Codelco Partner on Chilean Mine Decarbonisation,” miningdigital.com

Rapid Grade-Control Needs in West African Gold Super-Pits

Gold mega-pits have introduced high-throughput robotic labs that process 500+ samples per day. AngloGold Ashanti gained a 650% ROI at Iduapriem by pairing blast-movement monitoring with automated assay workflows, which raised gold recovery 4–6%. Success is spurring similar investments across Ghana, Mali, and Suriname.

AI-Enabled Predictive Maintenance for Robotic Sample Prep

Machine-learning models review vibration and thermal signals to forecast failures 72–96 hours in advance. Gecko Robotics documented 35% less unplanned downtime and 8–12% higher equipment availability at pilot mine sites. Lower maintenance costs accelerate project paybacks and encourage bundled hardware-and-software contracts.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| CAPEX Pay-back > 3 Years for Mid-Tier Mines | -1.6% | Global, particularly affecting junior and mid-tier operations | Short term (≤ 2 years) |

| Limited Inter-operability Between Legacy Assay Hardware | -1.2% | North America and Europe with aging infrastructure | Medium term (2-4 years) |

| Scarcity of Robotics Technicians in Africa & Caribbeans | -0.8% | Sub-Saharan Africa and Caribbean mining regions | Long term (≥ 4 years) |

| Data-sovereignty Barriers to Cloud-Hosted LIMS in EU | -0.7% | European Union, with potential spillover to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CAPEX Pay-back > 3 Years for Mid-Tier Mines

Mid-tier mining operations face significant financial constraints when evaluating laboratory automation investments, as extended payback periods often exceed acceptable risk thresholds for companies with limited capital resources. SRK Consulting's analysis of mining operational costs reveals that automation projects requiring initial investments above USD 5 million typically face scrutiny from boards when payback periods extend beyond 36 months. The challenge is compounded by volatile commodity prices that make long-term ROI calculations unreliable, particularly for gold and base metal operations where price fluctuations can exceed 20% annually. Teck Resources' Quebrada Blanca II project exemplifies this challenge, with development costs escalating to USD 8.5-9 billion significantly above initial estimates, highlighting the risk of cost overruns in major automation initiatives. Equipment financing options and leasing arrangements are emerging as potential solutions, but adoption remains limited due to concerns about technology obsolescence and maintenance responsibilities.

Limited Inter-operability Between Legacy Assay Hardware

The mining industry's substantial installed base of legacy analytical equipment creates significant integration challenges when implementing modern automation systems, as many instruments lack standardized communication protocols required for seamless data exchange. Laboratory information management systems must accommodate dozens of different instrument interfaces, with some facilities operating equipment from 15+ different manufacturers spanning 20+ years of technology evolution. The complexity increases exponentially when attempting to integrate fire assay furnaces, X-ray fluorescence spectrometers, and atomic absorption systems from different eras into unified automated workflows. Retrofit solutions can cost 40-60% of new equipment purchases while delivering only partial functionality, creating difficult capital allocation decisions for mining companies. The emergence of universal communication standards and middleware solutions offers potential relief, but implementation requires significant technical expertise that many mining operations lack internally.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Robotics Accelerate Hazard Reduction

Robotics generated the largest 33.60% slice of the Mining Laboratory Automation market in 2025, underpinned by the need to shield personnel from high-temperature furnaces and carcinogenic dust. Scott Automation’s turnkey cells now deliver crushing, milling, weighing, and fire-assay pouring in sealed environments, lifting throughput and repeatability. LIMS, while smaller, is the fastest climber at 12.15% CAGR, as executives value data integrity and regulatory traceability more than incremental hardware speed. Container labs meet exploration campaigns that require rapid mobilization; one 40-foot module can be on-line within three weeks. Automated analyzers adopt AI-assisted calibration, trimming reagent use and boosting precision.

By Automation Level: Modular Dominates but TLA Gains Traction

Firms prefer modular islands that replace discrete tasks—crushing, splitting, or fusion—without destabilizing whole workflows. Such systems accounted for 50.20% of the Mining Laboratory Automation market share in 2025. As payback proof accumulates, total lab automation grows 14.51% per year, particularly in iron-ore and copper hubs where sample volumes are extreme. ABB’s alliance with Agilent to provide integrated robotic-chemistry islands signals a shift toward vendor ecosystems that deliver cradle-to-gate solutions.

By Mining Phase: Production Dominates, Exploration Races Ahead

Production and beneficiation stages consumed 30.40% of 2025 revenue as operators demand real-time process control to meet contract specs. Exploration and grade control, however, post the 12.98% CAGR headline because complex ore bodies require rapid drill-core analytics. Giant Mining’s deployment of AI-powered geomet modeling before its 2025 drill campaign shows how early geochemical intelligence de-risks later capex.

By End-User: Large Enterprises Still Rule

Major diversified miners held 57.10% of the Mining Laboratory Automation market size in 2025 because they can fund multi-site roll-outs and sustain in-house R&D. Cost declines and leasing models let mid-tier players grow their outlay at 13.88% CAGR. Orexplore’s pay-per-sample gold detection service proves attractive for juniors seeking capital-light exploration.

Geography Analysis

Asia-Pacific anchored 31.20% of global revenue in 2025, with Australia’s autonomous iron-ore chain and China’s vast base-metal capacity driving demand. Australian robotics spending in mining stood at USD 63 billion in 2022 and is projected to jump to USD 218 billion by 2030, a trend mirrored in laboratory settings. Japan and South Korea supply precision sensors and AI chips that sharpen assay accuracy.

Middle East & Africa records the quickest 14.86% CAGR, catalyzed by sovereign funds. Saudi miner Ma’aden’s tie-up with Hexagon to open the region’s first digital mine—budgeted at USD 2 billion—sets a template for lab automation across phosphate, gold, and copper assets. African deployments lean heavily on container labs and remote monitoring to sidestep weak infrastructure and scarce technicians.

North America shows steady replacement demand as legacy uranium, potash, and precious-metal labs age. Vendors must navigate inter-operability retrofits and unionized labor environments. Europe’s picture is mixed: Nordic iron-ore producers pioneer hub-and-spoke automated labs that support numerous satellite mines, but the wider EU struggles with data-sovereignty hurdles that complicate cloud-based LIMS models. South America benefits from Chile’s assay-turn-around law and Peru’s lithium boom.

Competitive Landscape

The Mining Laboratory Automation market balances between scale incumbents and nimble disrupters. FLSmidth, Bruker, and Thermo Fisher wield global service fleets, integrated analytics suites, and robust after-sales contracts—together capturing 26% share. They solidify positions through retrofit packages that bolt robotics onto legacy instruments. Challenger firms like Chrysos (PhotonAssay) and GeologicAI deliver game-changing non-destructive analysis and AI-core scanning that compress assay lead-times from hours to minutes. Partnership webs multiply: ABB joins Agilent for robotic wet-chemistry cells; ABB also links with Mettler-Toledo’s LabX to overlay weight data onto LIMS, responding to laboratories starved of skilled technicians.

Automation-as-a-service emerges as a battleground. Scott Technology and Intertek pilot outcome-based contracts where miners pay per analyzed sample rather than own equipment outright. Meanwhile, equipment OEMs embed AI-driven predictive maintenance to slash unplanned downtime—a differentiator highlighted by Gecko Robotics’ field results. Sustainability imperatives push vendors to design low-energy fusion furnaces and smart ventilation, addressing stricter tailings analytics and decarbonization metrics.

Mining Laboratory Automation Industry Leaders

FLSmidth A/S

Thermo Fisher Scientific

SGS SA

Intertek Group PLC

Rocklabs (Scott Technology)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sandvik introduced a new autonomous surface drilling solution that shapes the future of drilling operations by improving efficiency and safety in mining environments, representing a significant advancement in surface automation technology.

- May 2025: Chrysos Corporation signed its first PhotonAssay unit contract with Newmont, marking a significant milestone in the deployment of advanced analytical technology that promises to revolutionize gold analysis in mining laboratories.

- February 2025: ABB and Codelco partnered to implement digital technologies, automation systems, and electrification solutions across Codelco's mining operations in Chile, representing a multi-billion dollar investment in mine decarbonization and laboratory automation.

- January 2025: ABB Robotics and Agilent Technologies entered a collaboration to develop automated laboratory solutions that enhance efficiency and flexibility in laboratory operations across various sectors, including mining and mineral processing.

Global Mining Laboratory Automation Market Report Scope

Laboratory automation automates the routine laboratory procedures and the use of dedicated workstations and software, and program instruments, which allows the associate scientists and technicians to deploy their resources and innovations towards experimentation and designing of useful follow-up projects, instead of spending their days performing tasks of tedious repetition. The scope of the study is limited to the deployment of laboratory automation solutions in the mining industry.

| Robotics |

| Laboratory Information Management Systems (LIMS) |

| Container Laboratory |

| Automated Analyzers and Sample Preparation Equipment |

| Total Lab Automation (TLA) |

| Modular / Island Automation |

| Exploration and Grade Control |

| Mine Development and Planning |

| Production and Beneficiation |

| Closure and Environmental Monitoring |

| Iron Ore |

| Copper |

| Gold |

| Coal and Battery Minerals (Ni, Li, Co) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Robotics | |

| Laboratory Information Management Systems (LIMS) | ||

| Container Laboratory | ||

| Automated Analyzers and Sample Preparation Equipment | ||

| By Automation Level | Total Lab Automation (TLA) | |

| Modular / Island Automation | ||

| By Mining Phase | Exploration and Grade Control | |

| Mine Development and Planning | ||

| Production and Beneficiation | ||

| Closure and Environmental Monitoring | ||

| By Commodity Processed | Iron Ore | |

| Copper | ||

| Gold | ||

| Coal and Battery Minerals (Ni, Li, Co) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Mining Laboratory Automation market?

The market is valued at USD 7.95 billion in 2026 and is forecast to reach USD 12.88 billion by 2031.

Which product segment leads spending today?

Robotics holds the largest 33.60% share, driven by the need to automate hazardous sample-preparation tasks.

Why are containerized laboratories gaining interest?

They offer fully equipped analytical capabilities that can be deployed on-site within weeks, ideal for remote exploration and fast-tracked green-field projects.

Which region is growing fastest?

Middle East & Africa posts the highest 14.86% CAGR, propelled by sovereign wealth fund investments and new digital mines.

How long is the typical payback period for automation projects?

Large operations report 18–24-month paybacks, while mid-tier mines often face periods longer than 3 years unless leasing or service-based models are used.

What role does AI play in laboratory automation?

AI underpins predictive maintenance, real-time data analytics, and advanced image-based ore characterization, reducing downtime and enhancing decision accuracy.

Page last updated on: