Size and Share of Conveyor Belt Market In Mining Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

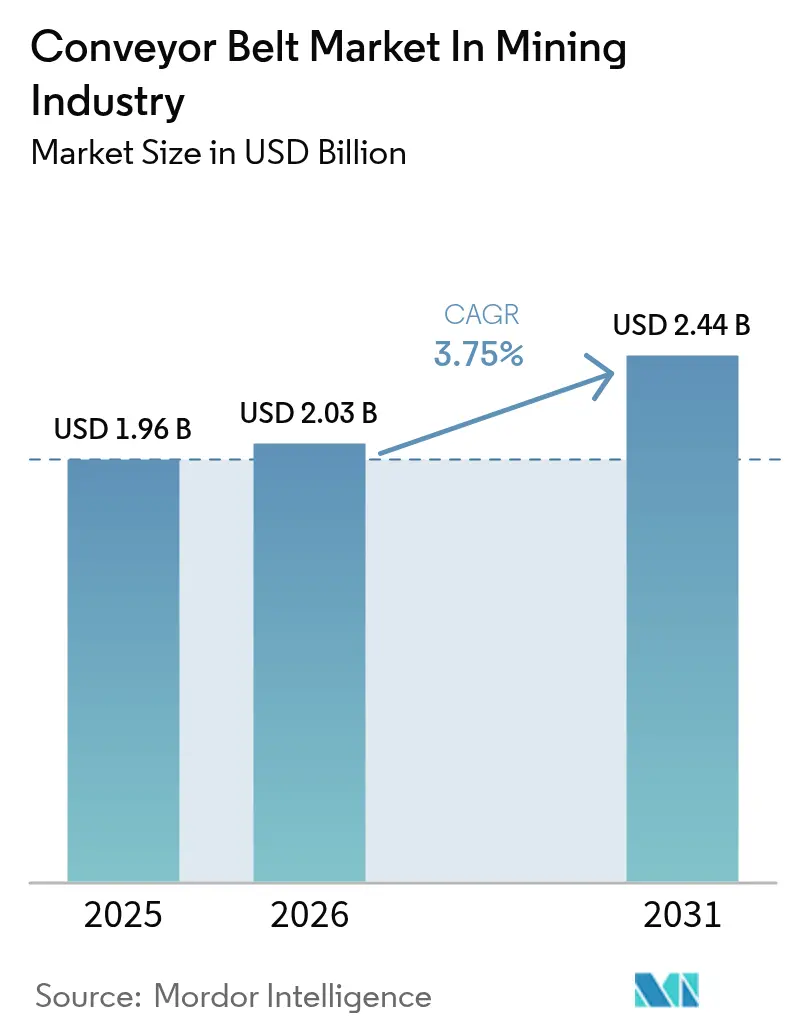

| Market Size (2026) | USD 2.03 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

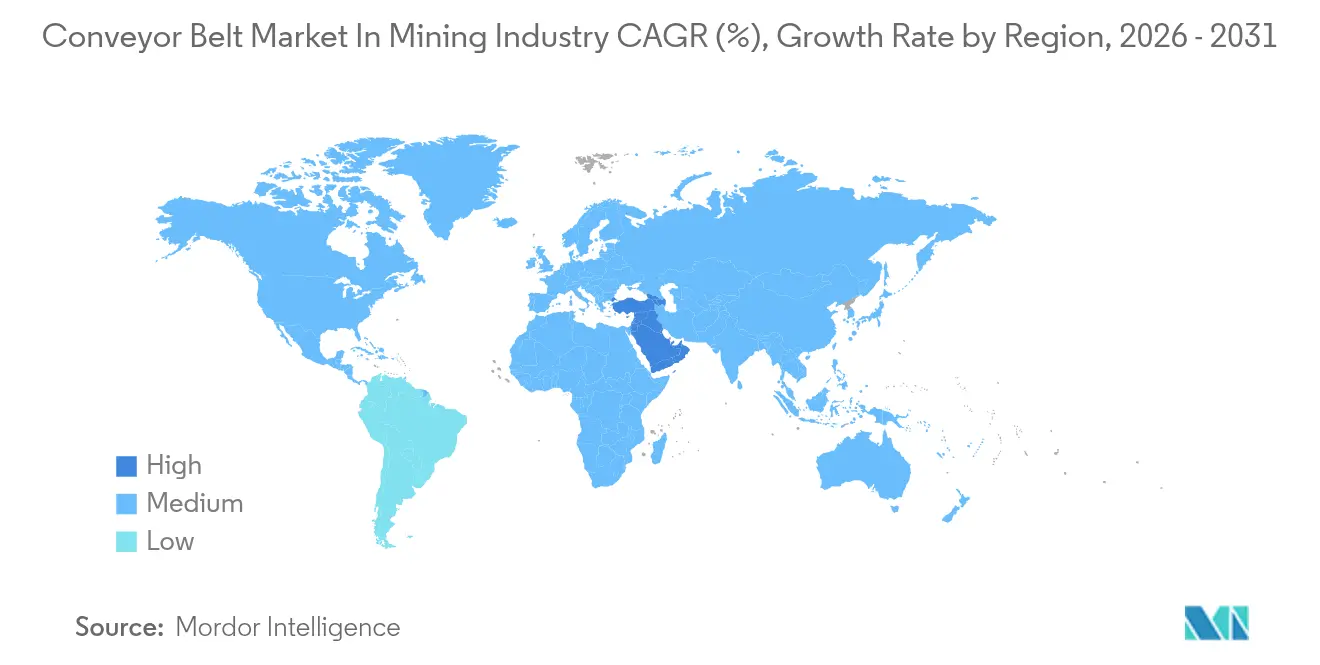

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Conveyor Belt Market In Mining Industry by Mordor Intelligence

The conveyor belt market size in mining industry size is projected to be USD 1.95 billion in 2025, USD 2.03 billion in 2026, and reach USD 2.44 billion by 2031, growing at a CAGR of 3.75% from 2026 to 2031. Mines are reallocating capital from diesel-truck haulage toward electrified in-pit crushing and conveying, yet cash-flow pressure and lengthy payback periods slow wholesale conversion. Rising demand for battery metals is translating into bigger throughput requirements that favour long overland belts, while national regulators are tightening fire-safety and proximity-detection rules that mandate higher-grade compounds. Raw-material volatility, especially in steel and aramid fiber, injects cost uncertainty just as lenders attach ESG clauses to project finance, prompting operators to scrutinize lifecycle costs rather than headline prices. Suppliers able to bundle belts, digital monitoring, and field service into turnkey solutions are capturing wallet share as mines seek to hedge technician shortages and commissioning risk.

Key Report Takeaways

- By geography, Asia-Pacific led with 38.64% revenue share in 2025, while Africa is forecast to expand at a 4.19% CAGR through 2031.

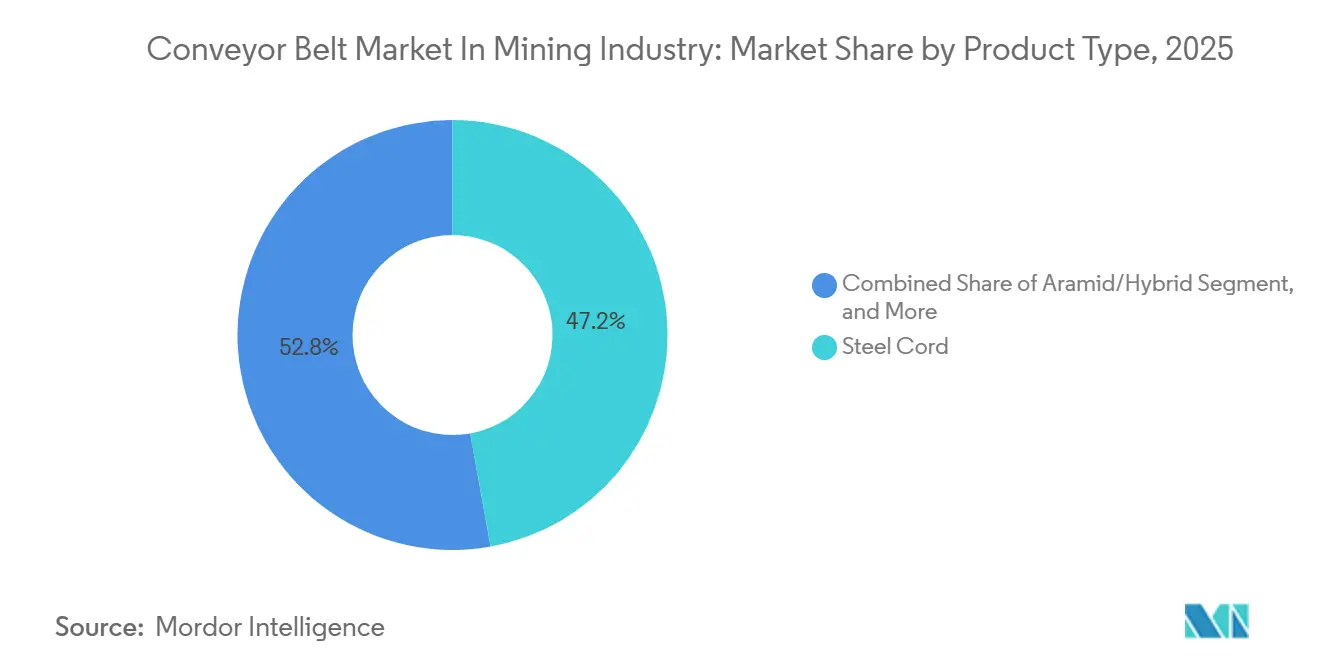

- By product type, steel cord belts held 47.17% of the conveyor belt market share in 2025, whereas aramid and hybrid belts are advancing at a 4.22% CAGR to 2031.

- By drive type, geared systems accounted for 72.84% of installations in 2025, but gearless drives are projected to grow at a 4.51% CAGR to 2031.

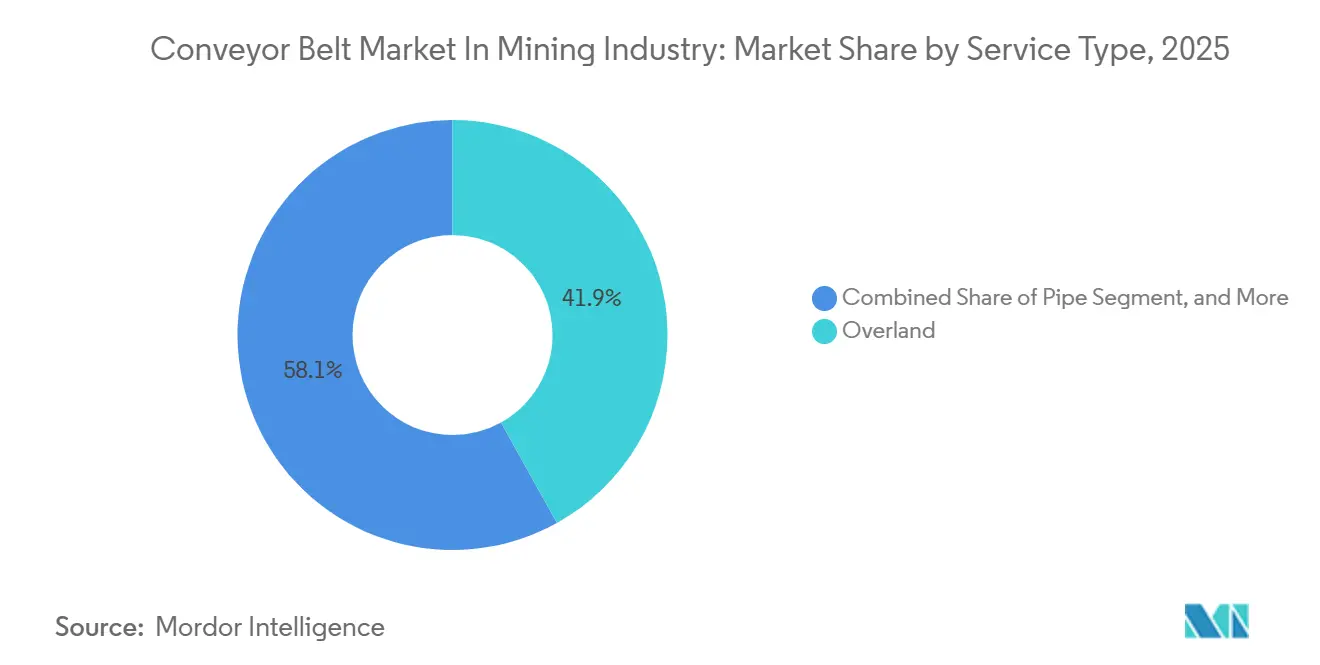

- By service type, overland conveyors commanded 41.92% share of the conveyor belt market size in 2025, yet pipe conveyors are set to post a 4.28% CAGR between 2026-2031.

- By application, open-pit operations captured 63.11% demand in 2025, while underground installations are progressing at a 4.96% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Conveyor Belt Market In Mining Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy Expansion of Surface and Underground Mining CAPEX (2025-2030) | +1.20% | Global, with concentration in Asia-Pacific (China, India, Australia), Africa (South Africa, DRC, Egypt), South America (Brazil, Chile, Argentina) | Medium term (2-4 years) |

| Surge in Bulk-Material Throughput Requirements of Autonomous Haulage Systems | +0.80% | North America, Australia, Chile (early adopters); spillover to Southern Africa | Medium term (2-4 years) |

| Tighter Occupational-Safety Mandates in High-Risk Mining Zones | +0.60% | Global, led by North America (MSHA), Europe (EU directives), Asia-Pacific (national regulators) | Long term (≥ 4 years) |

| Growing Demand for Energy-Efficient Abrasion-Resistant Belts | +0.50% | Global, strongest in regions with high electricity costs (Europe, Japan, Australia) | Long term (≥ 4 years) |

| On-Conveyor Ore-Grade Sensing Driving Adoption of Low-Vibration Belt Designs | +0.40% | North America, Australia, Chile, South Africa (advanced mining operations) | Medium term (2-4 years) |

| ESG-Linked Financing Tied to Low-Noise, Recyclable Belt Materials | +0.30% | Europe, North America, Australia; emerging in South America and Africa for international-financed projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heavy Expansion of Surface and Underground Mining CAPEX

Global mining capital expenditure aligned to conveyor installations is entering a multi-year surge, with USD 406 billion in active and planned projects logged for 2025. Flagship developments in the Pilbara and Atacama are shifting more than 10 kilometers of material per flight, confirming a scale at which conveyors outcompete diesel trucks on unit cost. Underground transitions at deep copper and gold deposits are ordering steel cord belts with breaking strengths surpassing 6,000 kN m⁻¹ to lift ore more than 1,000 meters without transfer points. Multinational miners such as Rio Tinto and BHP locked in 2025 procurement budgets for belt upgrades that stretch through 2030, signalling sustained order pipelines. Smaller producers still face financing gaps, yet their project feasibility studies increasingly benchmark conveyors as the long-run cost baseline.

Surge In Bulk-Material Throughput Requirements of Autonomous Haulage Systems

Autonomous truck networks rely on steady feed rates, pushing mines to designate conveyors as the fixed spine of material flow. Inline ore-grade analysers that require belt-speed stability within ±2% now influence rubber compound selection because vibration dampening secures sensor accuracy. Gearless drives commissioned at Codelco’s Chuquicamata in 2025 run 20 MW on a single flight, delivering 11,000 t h⁻¹ while trimming vibration by 30% versus geared sets.[1]ABB Communications, “ABB gearless drives for TAKRAF’s most powerful mining conveyors in Chile,” abb.com Early adopters in Australia and Chile report that the sensor-ready belts improve mill scheduling and reduce over-grinding losses, reinforcing the business case for higher-spec platforms.

Tighter Occupational-Safety Mandates in High-Risk Mining Zones

The United States Mine Safety and Health Administration finalized a proximity-detection rule in 2024, forcing retrofits of guard logic and emergency-stop circuits on legacy belts.[2]United States Mine Safety and Health Administration, “Proximity Detection Final Rule,” msha.gov Parallel updates to belt-air-course standards require flame-retardant covers, accelerating demand for neoprene and halogen-free formulations in underground coal. International Labour Organization guidelines published the same year are cascading into national codes from Indonesia to Peru, staging a multi-regional compliance cycle that lengthens the aftermarket tail for replacement belts.[3]United States Mine Safety and Health Administration, “Proximity Detection Final Rule,” msha.gov Mines that lag on upgrades now face insurance premium surcharges that often exceed the incremental cost of compliant belting.

Growing Demand for Energy-Efficient Abrasion-Resistant Belts

Electricity makes up as much as 25% of conveyor operating cost in high-tariff regions. Operators therefore specify low-rolling-resistance covers and lighter carcasses that shave kilowatt draw. Continental’s ContiClean demonstrated a 95% carry back reduction at a U.S. cement plant, doubling belt life and trimming scraper maintenance.[4]Continental AG, “Project Insight: ContiClean,” continental-industry.com DuPont aramid reinforcements cut belt mass by 40%, translating into 3-5% energy savings on overland routes that exceed 8 kilometers. Payback often falls below three years in Australia, Japan, and Germany, incentivizing mines to finance premium constructions even amid volatile commodity prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX and Long Payback Periods | -0.90% | Global, most acute in emerging markets (Africa, Southeast Asia, South America) with limited project finance | Medium term (2-4 years) |

| Persistent Shortage of Trained Belt-Maintenance Technicians | -0.60% | Global, severe in remote mining regions (Australia outback, Canadian Arctic, Sub-Saharan Africa) | Long term (≥ 4 years) |

| Belt Fire-Risk Clauses Raising Insurance Premiums | -0.40% | Underground coal and metal mines globally, particularly North America, Australia, South Africa | Short term (≤ 2 years) |

| Volatile Raw-Material (Steel and Aramid) Supply Due to Geo-Political Shocks | -0.50% | Global, with acute exposure in regions dependent on imports (Europe, Southeast Asia, South America) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX And Long Payback Periods

Overland or pipe conveyors can cost USD 5-15 million per kilometer, with multi-flight systems topping USD 300 million. Finance committees for mid-tier producers prefer shorter-cycle truck fleets, despite higher long-run operating expense, because loan covenants emphasize near-term cash flow. Currency swings and steel price spikes during the 2024-2025 window eroded contingency budgets on several African copper projects, leading to schedule slippage. Digital-twin software marketed by FLSmidth now models lifecycle savings to de-risk decisions, yet adoption is still confined to tier-1 miners with robust engineering departments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aramid Hybrids Challenge Steel Cord Dominance

Steel cord belts accounted for 47.17% of the conveyor belt market share in 2025 because their tensile capacity fits high-load, long-distance haulage. The conveyor belt market in mining industry is witnessing a 4.22% CAGR tilt toward aramid and hybrid belts that trim weight and energy demand without compromising breaking strength. Underground copper and gold mines opt for these lighter carcasses to ease installation in confined declines, while overland routes with compound curves appreciate the higher fatigue resistance. Suppliers are responding with modular platforms that pair aramid warp layers with sensor loops, an architecture that supports on-belt grade analyzers.

Fenner’s delivery of an ST6300 steel cord unit to a New South Wales gold mine illustrates ongoing demand for extreme-strength belts where vertical lifts exceed 1,000 meters. Continental’s Brazil plant expansion adds heavy-duty capacity to cut lead times for South American copper projects. Specialty textiles and solid-woven belts retain footholds in short in-plant circuits, but their share edges down as mines consolidate material-handling routes into fewer, more powerful flights. The conveyor belt market in mining industry therefore reflects a coexistence model in which steel cord remains the backbone of ultra-high-tension duties while aramid gains share in energy-sensitive or space-constrained installations.

By Drive Type: Gearless Systems Gain Traction in Ultra-High-Power Installations

Geared drives still held 72.84% share of the 2025 installed base thanks to price advantage and widespread maintenance know-how. However, gearless drives are expanding at a 4.51% CAGR as mines push beyond the 15-MW threshold where gearbox life-cycle economics deteriorate. The conveyor belt market in mining industry increasingly favours synchronous-motor designs paired with variable-frequency control that eliminate oil-bath gearboxes, cut vibration, and surface live torque data for predictive analytics. ABB’s 20-MW system at Chuquicamata set a new benchmark for single-flight capacity, reducing gearbox downtime risk and slashing CO₂ by 70% relative to diesel haulage.

In regions with reliable grids and OEM service depots, gearless penetration accelerates as procurement teams internalize lower spares inventories and extended maintenance intervals. Smaller mines in Africa and Southeast Asia still specify geared units because initial capital outlay for gearless can run 20-30% higher. As digital-twin commissioning shortens ramp-up time and warranty clauses extend to ten years, gearless value propositions strengthen, but technician reskilling remains a gating factor for widespread uptake.

By Service Type: Pipe Conveyors Expand in Environmentally Sensitive Corridors

Overland conveyors captured 41.92% of the conveyor belt market size in 2025 by offering the lowest cost per tonne over long horizontal hauls. Yet pipe conveyors, advancing at 4.28% CAGR, solve dust and spillage concerns where routes cross water sources, urban settlements, or indigenous lands. Enclosed belts satisfy stricter environmental-impact assessments, thereby accelerating permitting of greenfield mines in Canada, Scandinavia, and Eastern Australia. Relocatable overland modules rolled out by Metso cut stranded-asset risk as open pits widen, appealing to lithium and phosphorus deposits that evolve in phased benches.

Capital premiums of 30-50% over trough designs limit pipe adoption to regions with litigation exposure or community pushback. Where regulators fine dust exceedances, mines calculate that an up-front premium offsets multi-year legal fees and schedule delays. The conveyor belt market in mining industry thus shows a two-track future: standardized overland modules for bulk tonnage and enclosed pipe variants for high-visibility corridors.

By Application: Underground Segments Accelerate as Ore Bodies Deepen

Open-pit mines accounted for 63.11% of demand in 2025 because surface coal, iron ore, and copper deposits still dominate global tonnage. The conveyor belt market in mining industry is nonetheless shifting underground at a 4.96% CAGR as near-surface reserves deplete, and deeper orebodies sustain long-term grades. Underground belts must clear stricter flame-resistance and vibration criteria, prompting uptake of neoprene covers and sensor-instrumented idlers that monitor belt slip and methane accumulation.

Hybrid surface-to-underground systems emerge in transition pits, creating demand for belts certified against both surface abrasion and underground flame standards. Premium pricing attached to those cross-certified belts boosts supplier margins even as volume gradually tilts underground. Over the forecast horizon, belt demand growth concentrates in expansion shafts across Chile, Canada, and South Africa, underscoring the need for light yet high-tension carcasses compatible with vertical lifts.

Geography Analysis

Asia-Pacific remained the epicentre of conveyor investment in 2025, accounting for 38.64% of global revenue. Chinese coal producers fitted overland conveyors in Inner Mongolia to meet stricter truck-emission caps, while Indian iron-ore miners upgraded aging belts with ISO 340-compliant fire-resistant covers ahead of tighter national codes. Australian iron-ore majors integrated gearless drives and low-rolling-resistance belts that shave diesel burn, aligning with net-zero targets. Japan and South Korea, though smaller in tonnage, export high-spec belts to Southeast Asian nickel projects, cementing the region’s technology incubator role.

Africa records the fastest regional CAGR at 4.19%, lifted by copper projects in the Democratic Republic of Congo, phosphate expansions in Egypt, and gold shafts in South Africa. Simandou’s in-pit crushing and conveying complex headlines West Africa’s greenfield boom, while retrofit cycles in South Africa upgrade 1990s-era belts with digital monitoring to reduce unplanned downtime. The region’s challenges, notably grid instability and technician shortages, temper gearless penetration but also open opportunities for modular, quick-splice textile belts that tolerate variable loading.

North America and Europe exhibit replacement-driven demand as mines retire 20-year-old belts and retrofit safety systems. Continental’s USD 85 million compounding expansion in Iowa underscores a stable, high-performance aftermarket for abrasion-resistant covers. South America continues to pivot toward underground copper and lithium, with Brazil and Chile adding local steel cord capacity to shorten import lead times. The Middle East shows limited near-term influence, though Saudi Arabia’s Vision 2030 mining diversification may unlock sizable conveyor contracts post-2030.

Competitive Landscape

Top suppliers capture roughly 45% of global sales, indicating moderate concentration. Multinationals such as ContiTech, Bridgestone, Fenner Dunlop, and Phoenix leverage regional factories to shorten lead times and embed field-service teams that mitigate technician scarcity. Brand differentiation hinges on compound science, sensor integration, and the ability to finance turnkey packages. ContiTech’s Total Conveyance platform bundles belts, digital monitoring, and maintenance contracts, emulating Fenner’s one-stop-shop model launched after its 2022 acquisition of Conveyor Products and Solutions.

Chinese manufacturers expand export share by undercutting price; however, limited after-sales reach and gaps in MSHA or ISO certifications restrict entry into highly regulated mines. Technology partnerships flourish as belt makers team with ABB, FLSmidth, and Metso to co-engineer gearless drives and predictive-maintenance dashboards. The conveyor belt market in mining industry also sees digital-native entrants offering analytics-as-a-service, monetizing belt-health data through subscription platforms that compete with OEM monitoring suites.

Raw-material volatility remains a wild card. Steel and aramid price spikes in 2024-2025 squeezed margins, pushing suppliers to hedge with multiyear procurement contracts and explore recycled-polymer blends. Insurance carriers elevate fire-risk deductibles, rewarding suppliers whose compounds pass the latest flame-testing protocols. Accordingly, compliance portfolios now influence tender awards as much as headline price, reinforcing incumbents’ certification advantage.

Leaders of Conveyor Belt Market In Mining Industry

Semperit AG Holding

Fenner Dunlop Australia Pty Ltd (Michelin Group)

Oriental Rubber Industries Pvt Ltd

Bridgestone Corporation

Zhejiang Double Arrow Rubber Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TAKRAF secured an overland conveying contract for the Collahuasi copper mine in Chile, underscoring surging capital flows into South American energy-transition minerals and reinforcing TAKRAF’s expertise in high-capacity belt design.

- January 2025: Freeport-McMoRan finalized infrastructure for the Bagdad autonomous truck rollout, which mandates synchronized high-throughput conveyors to accommodate continuous ore flow and validate autonomous-haul economics.

- September 2024: Flexco opened a conveyor accessory plant in Namibia, extending localized supply and maintenance support across southern African mines to cut lead times and strengthen aftermarket sales.

- August 2024: Bridgestone invested USD 167 million to modernize its Kitakyushu facility, expanding production of premium compounds and embedding smart-sensor mold lines that feed data into its Smart On-Site analytics suite.

- August 2024: BEUMER Group won a contract for a long-distance overland conveyor at Warrior Met Coal in Alabama, a strategic U.S. reference that highlights demand for energy-efficient belts in replacement projects.

Scope of Report on Conveyor Belt Market In Mining Industry

The Conveyor Belt Market in Mining Industry Report is Segmented by Product Type (Steel Cord, Textile Reinforced, Aramid/Hybrid, Bucket and Side Wall, Others), Drive Type (Geared, Gearless), Service Type (In-Pit, In-Plant, Overland, Pipe, Stackers, Feed Conveyors), Application (Open-Pit, Underground), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Steel Cord |

| Textile Reinforced |

| Aramid/Hybrid |

| Bucket and Side Wall |

| Others Product Type |

| Geared |

| Gearless |

| In-Pit |

| In-Plant |

| Overland |

| Pipe |

| Stackers |

| Feed Conveyors |

| Open-Pit |

| Underground |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Singapore | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Steel Cord | |

| Textile Reinforced | ||

| Aramid/Hybrid | ||

| Bucket and Side Wall | ||

| Others Product Type | ||

| By Drive Type | Geared | |

| Gearless | ||

| By Service Type | In-Pit | |

| In-Plant | ||

| Overland | ||

| Pipe | ||

| Stackers | ||

| Feed Conveyors | ||

| By Application | Open-Pit | |

| Underground | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Singapore | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the expected value of the conveyor belt market in mining by 2031?

It is forecast to reach USD 2.44 billion by 2031.

Which region is projected to grow fastest for mining conveyor belts?

Africa is expected to post the quickest CAGR at 4.19% through 2031.

Which product type currently dominates belt demand in mines?

Steel cord belts lead with 47.17% share of 2025 revenue.

Why are gearless drives gaining popularity on conveyors?

They cut gearbox maintenance, lower vibration, and can handle ultra-high power above 15 MW.

What is the main barrier for smaller miners adopting long conveyors?

High upfront capital and payback periods extending beyond five years deter investment.

How are safety regulations influencing belt specifications?

Stricter fire-resistance and proximity-detection rules are driving demand for flame-retardant covers and automated shutdown sensors.

Page last updated on: