Automated Microbiology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.07 Billion |

| Market Size (2031) | USD 14.12 Billion |

| Growth Rate (2026 - 2031) | 9.25% CAGR |

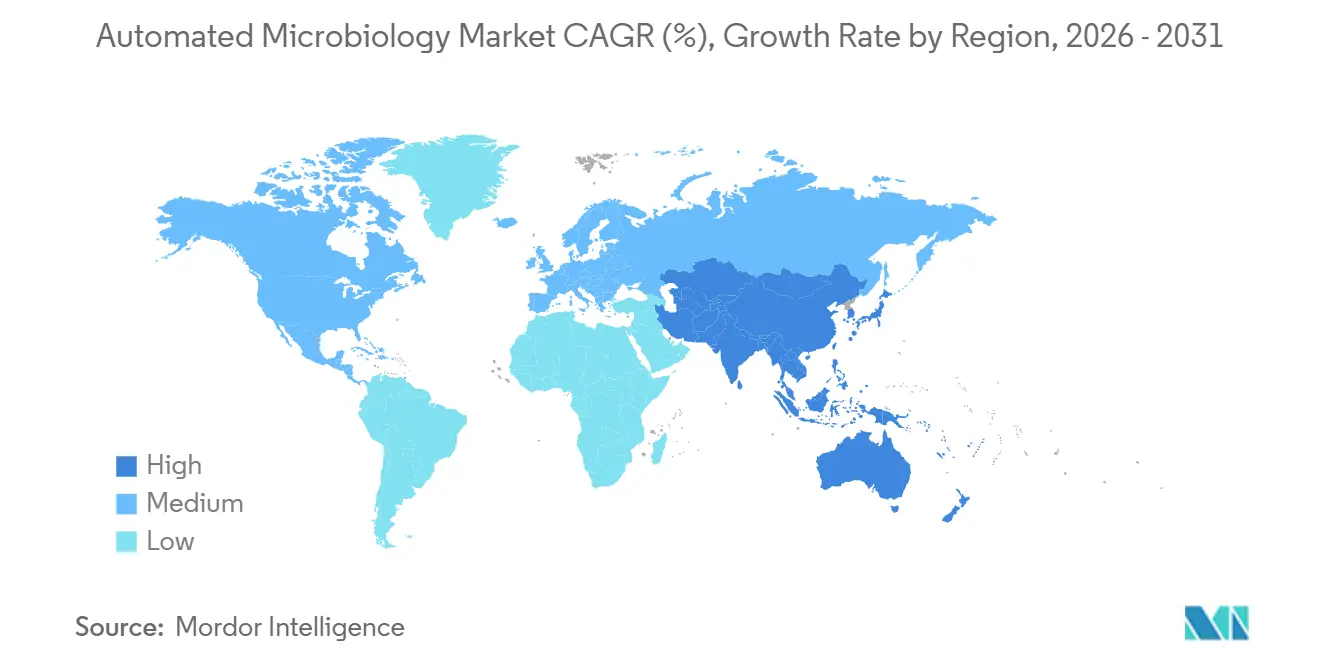

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

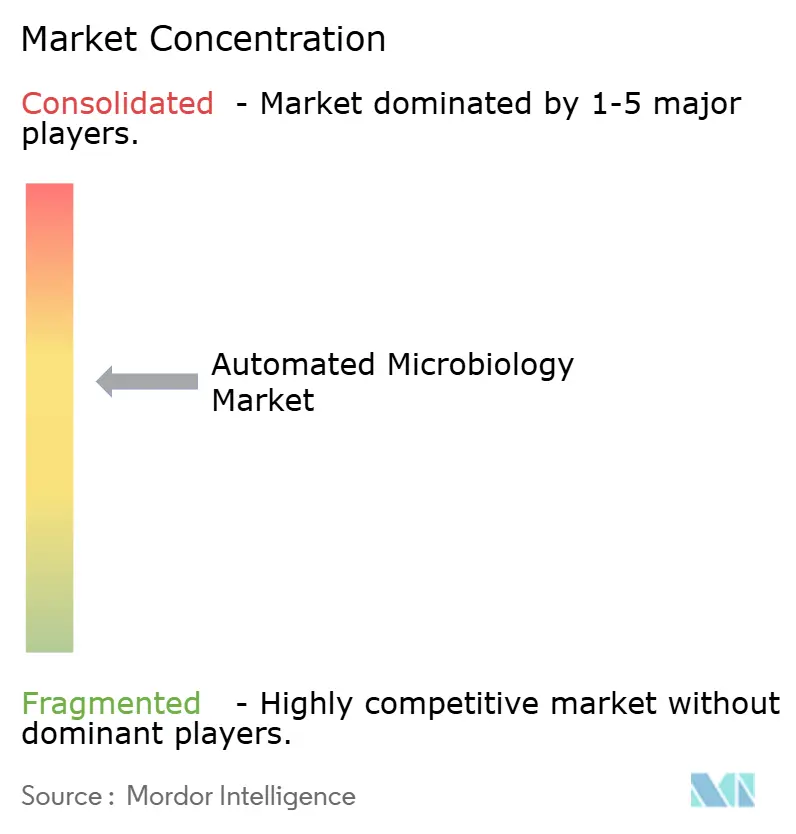

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Microbiology Market Analysis by Mordor Intelligence

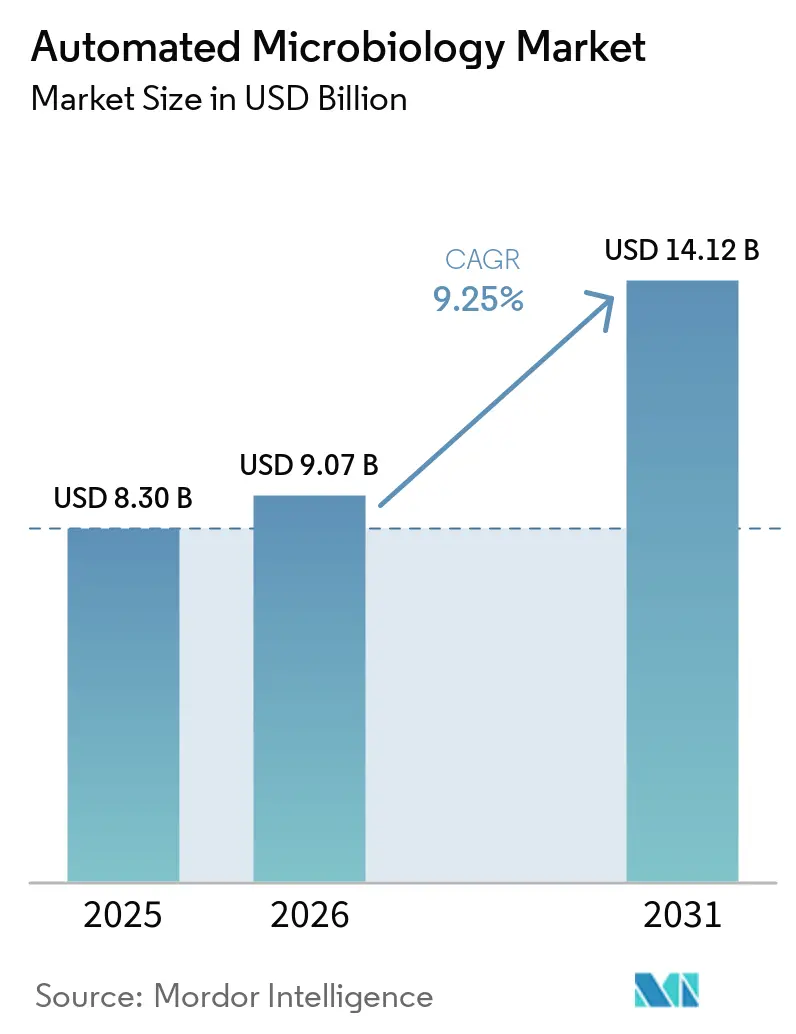

The Automated Microbiology Market size is expected to grow from USD 8.30 billion in 2025 to USD 9.07 billion in 2026 and is forecast to reach USD 14.12 billion by 2031 at 9.25% CAGR over 2026-2031.

The market is moving into a different demand cycle because antimicrobial resistance surveillance, laboratory staffing shortages, and tighter quality control requirements are now pushing automation at the same time, which makes adoption less discretionary than it was in earlier periods. WHO GLASS already draws standardized resistance data from 110 countries, and that scale supports sustained demand for automated identification and susceptibility workflows that can deliver consistent, machine-readable outputs across large testing networks. Turnaround time pressure is also becoming a direct purchasing factor because high-volume laboratories need faster blood culture and urine culture processing without adding headcount, and validated total laboratory automation systems have already shown major reductions in reporting time in routine practice. The automated microbiology market is also benefiting from regulated pharmaceutical and biopharmaceutical quality control demand, where audit-ready data capture, software validation, and connected workflows are becoming more important in day-to-day laboratory operations, especially as vendors expand AI-assisted imaging and middleware capabilities. Competition remains moderate to high, and current strategy is centered on portfolio reshaping, workflow integration, and software lock-in, while pressure points remain visible in China and in hospital systems that continue to defer large capital purchases.

Key Report Takeaways

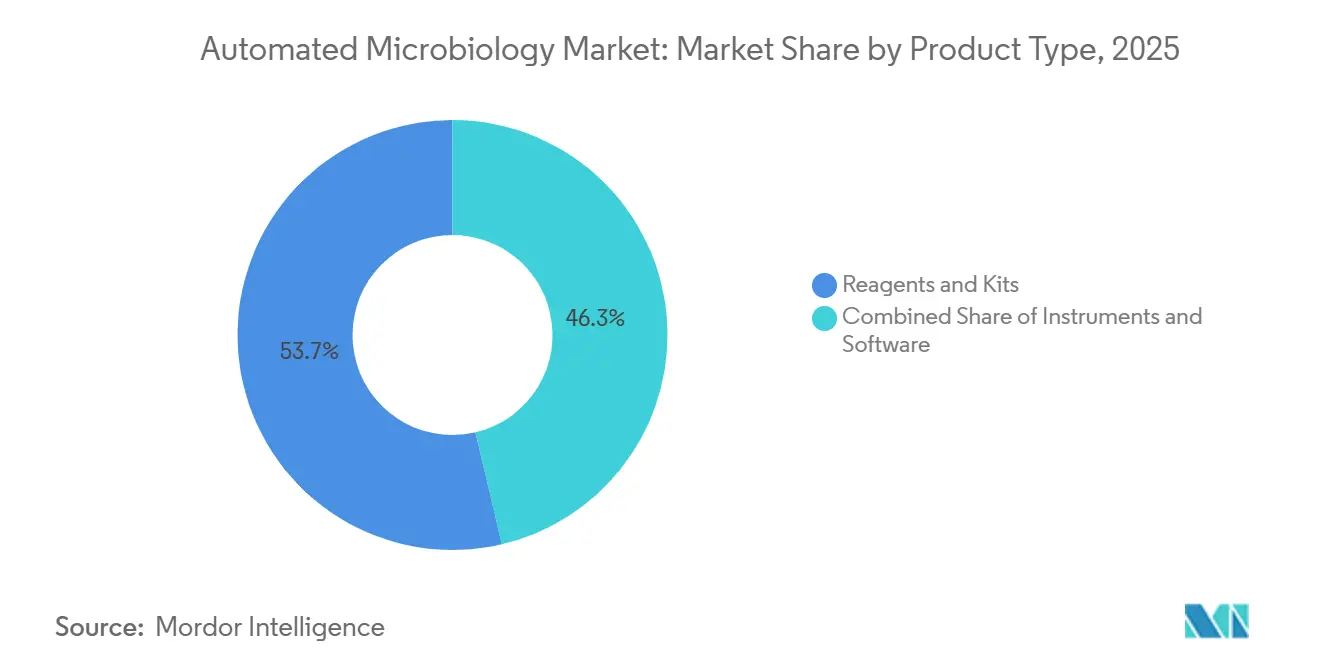

- By product type, reagents and kits led with 48.31% revenue share in 2025, while instruments are projected to grow at 11.38% CAGR through 2031.

- By automation type, fully automated systems held 75.24% revenue share in 2025 and is expected to record a 10.52 CAGR through 2031.

- By application, clinical diagnostics accounted for 54.52% revenue share in 2025, while biopharmaceutical production is forecast to grow at 11.25% CAGR through 2031.

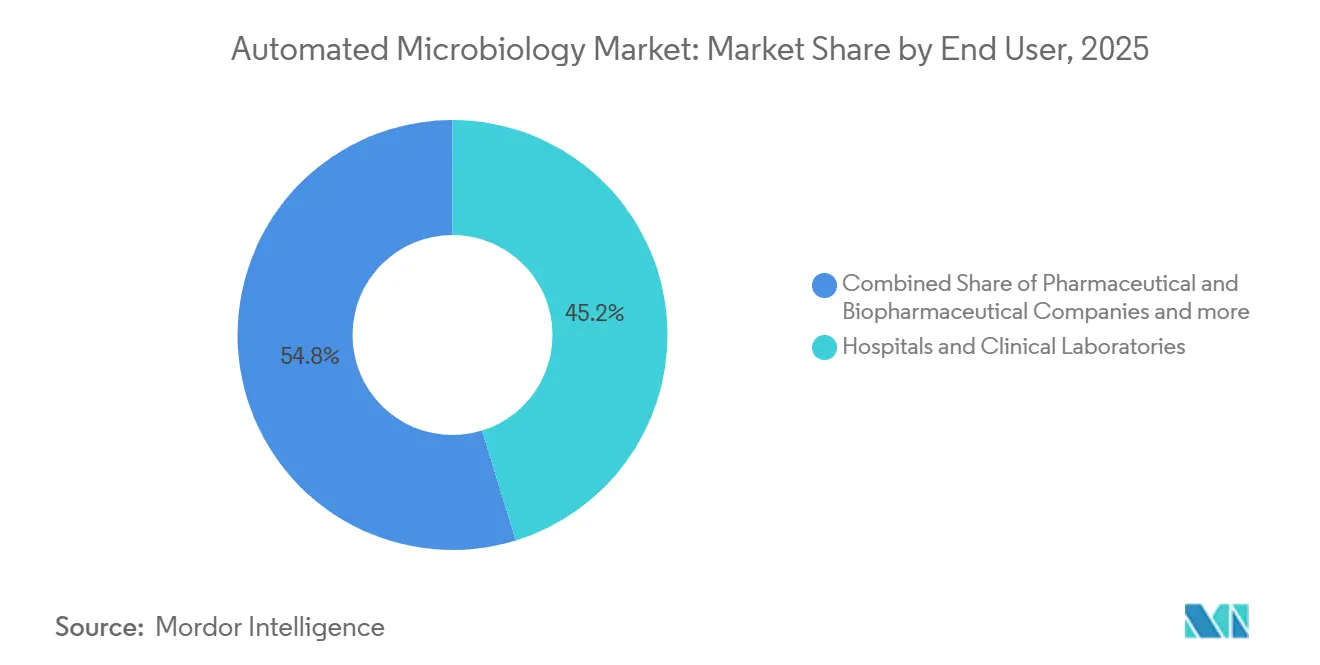

- By end user, hospitals and clinical laboratories held 45.22% revenue share in 2025, while pharmaceutical and biopharmaceutical companies are projected to expand at 11.65% CAGR through 2031.

- By diagnostic technology, molecular diagnostics held 45.31% share in 2025, while automated imaging and digital microscopy is projected to advance at 12.38% CAGR through 2031.

- By sample type, blood accounted for 62.24% share in 2025, while urine is forecast to grow at 11.52% CAGR through 2031.

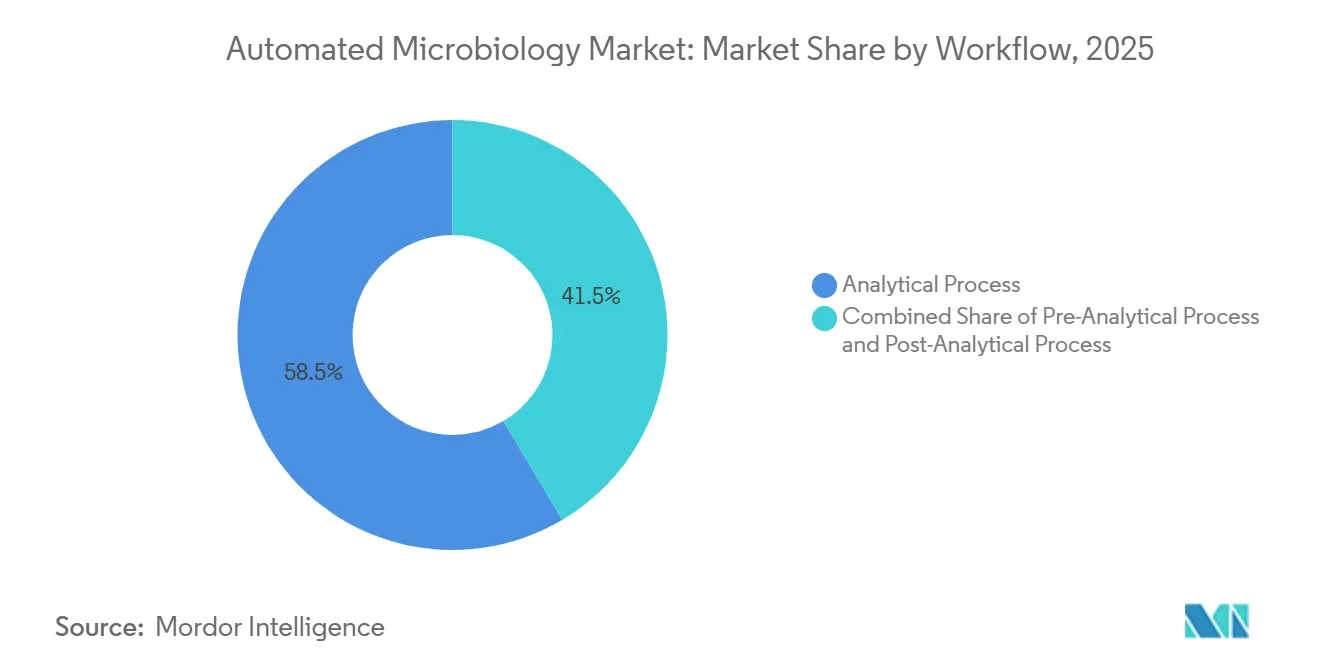

- By workflow, the analytical process held 58.52% share in 2025, while the pre-analytical process is projected to expand at 10.25% CAGR through 2031.

- By geography, North America held 42.22% global revenue share in 2025, while Asia-Pacific is projected to record the highest CAGR at 12.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automated Microbiology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Rapid Pathogen Identification in High-Volume Labs | +2.8% | Global, with highest intensity in North America and EMEA | Short term (≤ 2 years) |

| Expanding AMR Surveillance and Stewardship Programs | +1.9% | Global, with APAC and MEA scaling infrastructure rapidly | Medium term (2-4 years) |

| Automation Demand Driven by Technician Shortages and Turnaround-Time Pressure | +1.5% | North America, Western Europe, Japan | Short term (≤ 2 years), Medium term (2-4 years) |

| Increasing QC Requirements in Pharma, Food, and Water Testing | +1.2% | North America and EU, with spillover to APAC biopharma hubs | Medium term (2-4 years) |

| Cloud-Connected Workflow Standardization Across Multi-Site Lab Networks | +0.8% | North America and EU, with early gains in APAC centralized networks | Medium term (2-4 years), Long term (≥ 4 years) |

| Cybersecure AI-Ready Middleware as a Differentiator for Regulated Labs | +0.6% | Global, with strongest pull in the EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Rapid Pathogen Identification in High-Volume Labs

The automated microbiology market is seeing stronger demand from core laboratories that now process very high daily specimen volumes with limited ability to add staff or extend manual review steps. Northwell Health’s core laboratory was reported to process more than 2,400 urine cultures each day on a total laboratory automation platform, and that scale makes walk-away microbiology systems an operational requirement rather than a discretionary upgrade. Clinical urgency is reinforcing that demand because sepsis treatment outcomes worsen when appropriate therapy is delayed, which keeps blood culture detection speed and result reporting time at the center of laboratory purchasing decisions. In validated settings, total laboratory automation reduced blood culture turnaround time from 97 hours to 53.5 hours and reduced urine culture negative reporting time from 52.1 hours to 28.3 hours, which shows that time compression is now measurable and not just a workflow claim. Waters announced in June 2026 that the BD BACTEC FXI system received FDA 510(k) clearance and reduced mean time to bloodstream infection detection by 3 hours, or 15%, compared with its predecessor, which shows that product upgrades are still producing clinically relevant gains even in an established category.

Expanding AMR Surveillance and Stewardship Programs

The automated microbiology market is also being supported by surveillance frameworks that require standardized susceptibility data and wider interoperability across national and global reporting systems. The CDC Antimicrobial Resistance Laboratory Network had conducted more than 1.5 million tests through the end of 2025, including more than 520,000 isolate characterizations, 530,000 colonization screenings, and 664,000 whole-genome sequences, which illustrates the scale that automated microbiology platforms must support[1]Centers for Disease Control and Prevention, “About the AR Lab Network,” CDC, cdc.gov. A related shift is visible in the move toward molecular resistance detection because laboratories that rely only on conventional culture workflows face wider data gaps when surveillance programs increasingly need standardized and machine-readable resistance markers. A 2025 study in Infection Control & Hospital Epidemiology noted that wide adoption of rapid molecular AMR detection from blood cultures has direct implications for national surveillance comparability, which supports demand for platforms that can combine phenotypic and molecular outputs in one workflow. WHO’s 2025 report drew on more than 23 million bacteriologically confirmed infections from 110 countries, and that breadth continues to support investment in automated laboratory infrastructure across both mature and scaling testing networks.

Automation Demand Driven by Technician Shortages and Turnaround-Time Pressure

The automated microbiology market is being pushed forward by a structural staffing gap that laboratories cannot close quickly through normal recruitment and training cycles. ASCP reported more than 24,000 annual laboratory position openings in the United States against only 8,800 graduates from training programs, which leaves many laboratories with persistent vacancies and limited room to sustain manual microbiology workloads. This labor imbalance matters more in microbiology than in some adjacent disciplines because manual specimen handling, plate reading, and susceptibility workflows still consume large amounts of skilled staff time unless they are automated. A 2026 review in Frontiers in Cellular and Infection Microbiology reported that leading institutions now process up to 97% of amenable specimen types through total laboratory automation, while fully automated disk diffusion AST achieved 99.3% categorical agreement for Enterobacterales and 99.4% for Staphylococcus spp., which reduces earlier concerns that walk-away systems may compromise performance. As that evidence base grows, procurement decisions are shifting from whether automation is justified to which workflows should be automated first to protect turnaround time and staff productivity in the automated microbiology market.

Increasing QC Requirements in Pharma, Food, and Water Testing

The automated microbiology market is gaining support from regulated quality control settings where contamination monitoring, audit trails, and validated electronic workflows now matter as much as raw test throughput. bioMérieux’s Industrial Applications segment, which includes pharmaceutical quality control, recorded 14% organic sales growth in 2025, and that was the highest rate across its business lines, which shows that compliance-led demand is already feeding into purchasing activity. The same pattern is spreading beyond pharma because food and water testing laboratories also face stronger expectations around standardized methods, traceability, and dependable reporting cycles in export and regulated environments. HTWK Leipzig is running the EU-funded μQuant project from January 2025 through December 2026, and that project is focused on robotics and AI-based automated microbial image analysis to reduce cycle times across laboratory applications. As more regulated laboratories connect microbiology data to broader quality systems, automation becomes easier to justify because it supports compliance, throughput, and documentation in one investment cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost and Ongoing Service Contract Burden | -1.5% | Global, with the greatest pressure in smaller hospital systems and emerging markets | Short term (≤ 2 years), Medium term (2-4 years) |

| Complex Validation, Interoperability, and LIMS Integration | -1.2% | Global, with highest friction in Asia-Pacific secondary laboratories and MEA | Medium term (2-4 years) |

| Limited Skilled Workforce for Instrument Uptime and Advanced Assay Interpretation | -0.8% | Global, particularly constrained in South America and MEA | Long term (≥ 4 years) |

| Data Integrity, Cybersecurity, and AI Governance Concerns in Connected Laboratories | -0.6% | North America and EU regulated environments | Medium term (2-4 years), Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Ongoing Service Contract Burden

The automated microbiology market still faces a meaningful adoption barrier because fully automated systems require large upfront spending, dedicated space, and long service commitments that many smaller laboratories struggle to absorb. A 2026 multi-institutional review in Frontiers in Cellular and Infection Microbiology identified high capital investment, dependence on specialized consumables, the need for dedicated laboratory space, and exposure to downtime as the main constraints on total laboratory automation adoption. The cost issue is not limited to instrument purchase because vendor-specific consumables and support contracts turn the system into a long-term recurring expense structure that often compares poorly with more distributed manual alternatives in hospital budgeting reviews. The burden is even heavier in emerging markets because local service engineering capacity may be limited, and delays in repairs can quickly turn a single equipment issue into a testing backlog. That combination keeps the most advanced automation concentrated in higher-volume hospital systems, reference laboratories, and well-funded pharmaceutical facilities within the automated microbiology market.

Complex Validation, Interoperability, and LIMS Integration

The automated microbiology market also faces slower adoption when laboratories cannot connect new analyzers cleanly to existing LIMS, HIS, and stewardship reporting systems. A 2024 PLOS One study of clinical microbiology laboratories in Thailand found that poor connectivity between microbiology LIMS and automated instruments was common, which forced manual data re-entry and increased both workload and transcription risk. A separate 2024 review in PLOS Global Public Health showed that multiple non-interoperable digital systems continue to limit data quality in AMR surveillance work, which makes the automation case harder when downstream integration remains weak. The burden continues after installation because software updates and instrument reconfiguration can trigger fresh validation work under regulated laboratory settings, which slows refresh cycles and can delay wider rollout of AI-assisted modules. These constraints are more visible in secondary laboratories across Asia-Pacific, the Middle East, and Africa, where instrument acquisition sometimes moves faster than the supporting digital standardization needed to use automation fully.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reagents Sustain Revenue; Instruments Lead the Next Upgrade Cycle

Reagents and kits held 48.31% of the automated microbiology market share in 2025, which reflects the recurring demand for culture media, identification panels, and susceptibility cards across a growing installed base. This revenue stream is structurally different from instrument sales because consumables continue to move once an analyzer is placed and a laboratory enters a supply relationship. That recurring profile helps stabilize vendor revenue even when capital ordering becomes uneven across hospital systems. It also gives leading suppliers room to support software updates, menu expansion, and field service through a more predictable cash flow base.

The automated microbiology market will see faster expansion in instruments, which are forecast to grow at 11.38% CAGR from 2026 to 2031 as laboratories replace partial automation with more integrated pre-analytical, analytical, and post-analytical set-ups. Software is becoming more strategically important within the automated microbiology industry because AI-assisted image analysis now influences workflow speed, consistency, and customer retention after the initial hardware placement. Copan stated in February 2026 that PhenoMATRIX received broad intended-use FDA 510(k) clearance for AI-assisted colony plate sorting across multiple culture media types, which reflects the direction of product development in higher-value software layers. As a result, instruments and software are now the main innovation battleground, while reagents continue to anchor the commercial model.

By Automation Type: Full Walk-Away Dominance Reflects Laboratory Workforce Economics

Fully automated systems held 75.24% of market revenue in 2025, which shows that the dominant purchasing logic is no longer limited to analytical performance and is now closely tied to labor substitution. The staffing gap in laboratory medicine has made it harder for administrators to defend workflows that depend on frequent manual intervention or long training periods for specialized microbiology staff. In that setting, full walk-away systems offer value not only through throughput gains but also through lower exposure to open staffing positions and repeated turnaround delays. This is why fully automated platforms have become the preferred format in larger hospital and reference laboratory networks.

Semi-automated systems still retain a role in lower-volume laboratories and in testing settings where uncommon morphologies or polymicrobial specimens continue to need closer human review. The automated microbiology market is not transitioning at the same speed everywhere because many mid-tier hospitals in China, South Asia, and Southeast Asia are still moving from semi-automated to fully automated configurations. A 2026 study in the European Journal of Clinical Microbiology & Infectious Diseases highlighted Chinese MALDI-TOF systems such as Autof MS2600 and EXS3000, both with databases exceeding 5,189 species, which shows that domestic vendors are becoming more credible options in mid-market segments. That means the next wave of share shifts may come not from whether laboratories automate, but from which suppliers capture the replacement cycle as full automation spreads.

By Application: Clinical Diagnostics Dominates; Biopharma Scales Fastest

Clinical diagnostics accounted for 54.52% of the automated microbiology market size in 2025, which confirms that hospital-associated testing remains the largest demand center by routine volume. Bloodstream infection, urinary tract infection, and respiratory pathogen work continue to generate daily testing demand that is hard to defer and difficult to centralize completely. That gives the clinical segment a durable base even when capital spending pauses because the underlying testing need remains steady. The breadth of antimicrobial stewardship programs also supports continued demand because each clinical episode is increasingly tied to more standardized microbiology data requirements.

Biopharmaceutical production is forecast to expand at 11.25% CAGR from 2026 to 2031, which makes it the fastest-growing application in the automated microbiology market. This segment is being strengthened by cell and gene therapy scale-up, higher sterility expectations, and more frequent use of rapid and automated bioburden monitoring in critical production steps. bioMérieux completed the acquisition of Accellix in January 2026, and the deal supports its position in rapid automated flow cytometry for cell and gene therapy quality control, which signals the strategic value attached to this area[2]bioMérieux SA, “bioMérieux Acquires Accellix,” bioMérieux, biomerieux.com. Environmental and water testing, along with food and beverage testing, remain smaller but stable niches that help vendors diversify beyond hospital cycles within the automated microbiology industry.

By End User: Hospitals Hold Volume Leadership; Pharma/Biopharma Companies Set the Growth Pace

Hospitals and clinical laboratories held 45.22% of end-user revenue in 2025, and that leadership still reflects the scale and regularity of routine blood, urine, wound, and related microbiological testing. These buyers remain central to vendor sales efforts because they combine predictable specimen volume with a continuing need to improve turnaround time and staff utilization. Their position is reinforced by the fact that microbiology workloads are difficult to postpone, especially in acute care settings where result speed influences treatment decisions. Large hospital systems also tend to be the first to adopt integrated laboratory automation because they can justify multi-workflow platforms across a broader testing base.

Pharmaceutical and biopharmaceutical companies are forecast to grow at 11.65% CAGR from 2026 to 2031, which makes them the fastest-growing end-user group in the automated microbiology market. Their momentum comes from biologics manufacturing expansion, advanced therapy production, and stricter quality control expectations in regulated environments. Contract research organizations sit close to this demand pocket because outsourced bioburden and biosafety testing often requires the same validated and audit-ready platforms used in internal pharma laboratories. That overlap gives vendors a clear expansion path from direct pharma accounts into CRO demand, which keeps this part of the automated microbiology industry commercially attractive even when hospital budgets tighten.

By Diagnostic Technology: Molecular Diagnostics Leads Share; Imaging-AI Drives the Growth Frontier

Molecular diagnostics held 45.31% share in 2025, which reflects the established position of PCR-based and multiplex panel systems in higher-income laboratory networks. These systems already fit well with antimicrobial resistance workflows because they can generate rapid and standardized outputs that are useful in both patient care and surveillance reporting. Their installed base also gives vendors a strong platform for cross-selling adjacent automation and informatics modules. Even so, molecular systems do not eliminate demand for culture-based workflows because phenotypic confirmation and susceptibility testing remain essential in many routine laboratory pathways.

Automated imaging and digital microscopy is forecast to advance at 12.38% CAGR from 2026 to 2031, which makes it the fastest-growing technology area in the automated microbiology market. A June 2026 paper in npj Digital Medicine described a deep learning system for bacterial identification and resistance prediction from MALDI-TOF data, and that work points to a broader move toward richer interpretation from existing analytical data sets. Bruker announced workflow expansions for its MALDI Biotyper and IR Biotyper portfolio at ESCMID Global 2026, including MBT PrepMatic and MBT SepsiMatic, which shows that vendors are still investing heavily in automated sample preparation and blood culture to MALDI pathways. Mass spectrometry remains important, but the next competitive frontier is shifting toward image analysis, AI-supported interpretation, and broader decision support within the automated microbiology industry.

By Sample Type: Blood Anchors Clinical Revenue; Urine's Automation Wave Signals a Structural Shift

Blood held 62.24% share of sample type revenue in 2025, which reflects the high clinical priority and strong capital intensity attached to bloodstream infection diagnostics. Blood culture platforms sit near the center of many microbiology automation investments because faster detection directly supports earlier treatment action in severe infections. This sample category also tends to carry higher system importance because hospitals rely on it across emergency, inpatient, and critical care pathways. That keeps blood-based automation commercially important even when laboratories delay broader platform upgrades.

Urine is projected to expand at 11.52% CAGR from 2026 to 2031, which makes it the fastest-growing sample type in the automated microbiology market. The growth comes from a large testing base and from the fact that urine workflows contain several repetitive manual steps, including decapping, barcoding, plating, and volume measurement, that are well suited to automation. Waters announced in June 2026 that BD BACTEC FXI received FDA 510(k) clearance, CE Mark under EU IVDR, and Japan PMDA approval, which keeps blood culture innovation visible, but the larger structural shift in routine workflow efficiency is increasingly tied to how laboratories automate high-volume urine processing. Tissue and other non-liquid sample types will continue to grow more gradually because automated pre-processing remains harder to standardize across more variable specimen formats.

By Workflow: Analytical Processes Remain Core; Pre-Analytical Automation Unlocks Total Throughput

The analytical process held 58.52% share in 2025, which reflects the long-established role of automation in incubation, imaging, identification, and AST workflows. These steps have attracted the most product development over the past two decades, which explains why the installed base is deepest here. They also carry the clearest clinical value because they are directly tied to organism detection, characterization, and result release. For many laboratories, this remains the first layer of automation and the starting point for broader platform integration.

Pre-analytical process automation is forecast to grow at 10.25% CAGR from 2026 to 2031, which shows that the automated microbiology market is now giving more weight to specimen handling quality before culture interpretation begins. A 2026 review in Frontiers in Cellular and Infection Microbiology argued that specimen processing variability remains the largest controllable source of culture false negatives, which is why more buyers are shifting attention upstream to reception, sorting, aliquoting, and plating. Copan, Waters/BD, and Bruker now compete across this earlier stage of the workflow, and that means the automated microbiology industry is moving toward unified platforms that connect pre-analytical, analytical, and post-analytical steps under one middleware layer. As these platforms mature, post-analytical automation and software validation will carry more strategic weight because result interpretation and release are becoming harder to separate from the hardware itself.

Geography Analysis

North America held 42.22% of the automated microbiology market size in 2025, and that position reflects high clinical testing intensity, a large pharmaceutical manufacturing base, and a laboratory environment that increasingly favors documented automation in regulated settings. The United States remains the center of regional demand because workforce shortages are especially visible there, with ASCP reporting more than 24,000 annual openings against 8,800 graduates from training programs. Product approvals have also supported a steady replacement and upgrade cycle, including BD Phoenix M50 in April 2025, bioMérieux VITEK COMPACT PRO in March 2025, Copan PhenoMATRIX in February 2026, and BD BACTEC FXI in June 2026[3]Becton, Dickinson and Company, “BD Receives FDA 510(k) Clearance for Advanced Microbiology Solution,” BD News, news.bd.com. Canada and Mexico remain smaller contributors, but consolidation in Canadian laboratory services and the expansion of Mexico’s private hospital base continue to add incremental demand to the automated microbiology market.

Europe’s position in the automated microbiology market is shaped by public hospital procurement cycles and by the region’s strong pharmaceutical quality control base. Growth is steadier than in Asia-Pacific, but the demand mix is broad because hospital laboratories, reference centers, and industrial users all contribute to equipment and consumables demand. bioMérieux reported 4.6% organic sales growth in EMEA in 2025, and industrial applications led the improvement across the region, which supports the view that pharmaceutical quality control is an important growth contributor. Spain and Italy continue to add demand through laboratory modernization and health system investment, which gives Europe a balanced growth profile even without the faster expansion rates seen in Asia-Pacific.

Asia-Pacific will record the highest CAGR at 12.65% from 2026 to 2031 in the automated microbiology market, but the drivers differ widely across the region. India still has a long runway for adoption because many district and tertiary hospitals are moving from manual AST methods to automated phenotypic systems, which leaves substantial room for first-time instrument placement. Japan is a more mature automation market and is now in an upgrade phase, which is reflected in the April 2026 PMDA approval for BD BACTEC FXI alongside its other regulatory clearances. China presents a mixed picture because bioMérieux reported a double-digit organic decline in microbiology revenue there in 2025, while adoption in mid-tier hospitals continues to expand as purchasing shifts beyond the top hospital tier. South Korea is benefiting from biopharma export growth, which is creating additional quality control automation demand. Middle East and Africa and South America remain earlier-stage opportunities, where GCC healthcare infrastructure programs and Brazil’s private laboratory base provide demand anchors, while limited local validation and service capacity still slows broader adoption.

Competitive Landscape

The automated microbiology market remains moderately concentrated, with a small group of global diagnostics and life sciences companies controlling much of the installed base, premium consumables stream, and higher-value software layer. Competition is now less about stand-alone instruments and more about who can combine sample preparation, analytical performance, result interpretation, and validated digital workflows in one commercial offering. This matters because once a laboratory configures middleware, reporting rules, and informatics around a specific platform, switching to another vendor becomes more difficult and can require fresh validation under regulated settings. The automated microbiology market therefore rewards vendors that can expand customer lock-in through integrated workflow design rather than through hardware performance alone.

One clear strategic move came in April 2026, when Thermo Fisher Scientific signed an agreement to sell its microbiology business to Astorg for USD 1.075 billion, with the divested unit having generated USD 645 million in 2025 revenue, which points to active portfolio reshaping and the emergence of a more focused platform in this space. Another came in January 2026, when bioMérieux acquired Accellix to strengthen its position in rapid automated flow cytometry for cell and gene therapy quality control, which aligns with the faster growth seen in regulated biopharma testing. Roche added a broader diagnostics and AI signal in May 2026 through its agreement to acquire PathAI, which shows that larger diagnostics groups continue to deepen algorithmic capability around image interpretation and workflow support. These moves show that acquisition strategy is being used to add software, automation depth, and specialized regulated testing capability rather than only more instrument volume.

The product road map also remains active. BD received FDA 510(k) clearance for the Phoenix automated microbiology system update in April 2025, and the filing included a Predetermined Change Control Plan authorization, which is relevant because it points to a more flexible regulatory path for future AI-related model updates. Bruker’s 2026 announcements around MALDI workflow expansion and Copan’s 2026 FDA clearance for PhenoMATRIX show that software-assisted interpretation and pre-analytical automation are becoming more important in vendor differentiation. Smaller players continue to defend narrower positions in rapid phenotypic AST, digital colony imaging, and pharmaceutical bioburden testing, but their scale remains limited next to the broader commercial reach of the largest suppliers. At the same time, the mid-market remains less fully served, especially in emerging regions where buyers need compact, validated systems with lower service complexity. That leaves room for additional consolidation, partnerships, and region-specific product formats over the next few years in the automated microbiology market.

Automated Microbiology Industry Leaders

Becton, Dickinson and Company

bioMérieux SA

Thermo Fisher Scientific Inc.

Danaher Corporation

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Roche entered into a definitive merger agreement to acquire PathAI, a US-based AI-powered digital pathology and laboratory diagnostics company. The acquisition, expected to close in H2 2026, integrates PathAI's algorithmic diagnostics capabilities into Roche's Diagnostics division, directly strengthening its position in AI-driven imaging and interpretation for clinical microbiology and adjacent workflows.

- April 2026: Thermo Fisher Scientific signed a definitive agreement to sell its microbiology business, spanning antimicrobial susceptibility testing, culture media, and pharma/food safety solutions, to pan-European private equity firm Astorg for USD 1.075 billion. The divested unit generated USD 645 million in revenue in 2025. Astorg intends to operate the business as an independent platform with an active M&A mandate, and transaction close is expected in H2 2026, subject to regulatory approval.

Global Automated Microbiology Market Report Scope

As per the scope of the report, automated microbiology refers to the use of automated systems and technologies to perform microbiological testing, identification, and analysis of microorganisms. These systems enhance efficiency, accuracy, and speed in detecting bacteria, viruses, fungi, and other microbes in clinical, environmental, or industrial samples.

The segmentation of the automated microbiology market is categorized by product type, automation type, application, end user, diagnostic technology, sample type, workflow, and geography. By product type, the market includes instruments such as automated microbial identification systems, automated blood culture systems, automated colony counters, automated sample preparation systems, automated antibiotic susceptibility testing systems, automated microbiology analyzers, automated incubators, and automated media preparation systems. It also includes reagents and kits, as well as software. By automation type, the market is divided into fully automated and semi-automated systems. By application, the market covers clinical diagnostics, biopharmaceutical production, environmental and water testing, food and beverage testing, and other applications.

By end user, the market is segmented into hospitals and clinical laboratories, pharmaceutical and biopharmaceutical companies, food and beverage manufacturers, contract research organizations, and other end users. By diagnostic technology, the market includes molecular diagnostics, mass spectrometry, automated imaging and digital microscopy, flow cytometry, and other technologies. By sample type, the market is segmented into blood, urine, tissue, and other sample types. By workflow, the market is categorized into pre-analytical process, analytical process, and post-analytical process. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Instruments | Automated Microbial Identification Systems |

| Automated Blood Culture Systems | |

| Automated Colony Counters | |

| Automated Sample Preparation Systems | |

| Automated Antibiotic Susceptibility Testing Systems | |

| Automated Microbiology Analyzers | |

| Automated Incubators | |

| Automated Media Preparation Systems | |

| Reagents and Kits | |

| Software |

| Fully Automated |

| Semi-Automated |

| Clinical Diagnostics |

| Biopharmaceutical Production |

| Environmental and Water Testing |

| Food and Beverage Testing |

| Other Applications |

| Hospitals and Clinical Laboratories |

| Pharmaceutical and Biopharmaceutical Companies |

| Food and Beverage Manufacturers |

| Contract Research Organizations |

| Other End Users |

| Molecular Diagnostics |

| Mass Spectrometry |

| Automated Imaging and Digital Microscopy |

| Flow Cytometry |

| Other Technologies |

| Blood |

| Urine |

| Tissue |

| Other Sample Types |

| Pre-Analytical Process |

| Analytical Process |

| Post-Analytical Process |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Instruments | Automated Microbial Identification Systems |

| Automated Blood Culture Systems | ||

| Automated Colony Counters | ||

| Automated Sample Preparation Systems | ||

| Automated Antibiotic Susceptibility Testing Systems | ||

| Automated Microbiology Analyzers | ||

| Automated Incubators | ||

| Automated Media Preparation Systems | ||

| Reagents and Kits | ||

| Software | ||

| By Automation Type | Fully Automated | |

| Semi-Automated | ||

| By Application | Clinical Diagnostics | |

| Biopharmaceutical Production | ||

| Environmental and Water Testing | ||

| Food and Beverage Testing | ||

| Other Applications | ||

| By End User | Hospitals and Clinical Laboratories | |

| Pharmaceutical and Biopharmaceutical Companies | ||

| Food and Beverage Manufacturers | ||

| Contract Research Organizations | ||

| Other End Users | ||

| By Diagnostic Technology | Molecular Diagnostics | |

| Mass Spectrometry | ||

| Automated Imaging and Digital Microscopy | ||

| Flow Cytometry | ||

| Other Technologies | ||

| By Sample Type | Blood | |

| Urine | ||

| Tissue | ||

| Other Sample Types | ||

| By Workflow | Pre-Analytical Process | |

| Analytical Process | ||

| Post-Analytical Process | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the automated microbiology market by 2031?

The automated microbiology market is forecast to reach USD 14.12 billion by 2031, up from USD 9.07 billion in 2026, at a 9.25% CAGR over 2026-2031.

Which product category leads revenue in automated microbiology?

Reagents and kits led product revenue with a 48.31% share in 2025, supported by recurring demand tied to installed instrument bases.

What is driving faster adoption of automated microbiology systems in hospitals?

The main factors are antimicrobial resistance surveillance, laboratory staffing shortages, and the need to shorten turnaround times in high-volume clinical settings.

Which application is growing the fastest through 2031?

Biopharmaceutical production is the fastest-growing application, with an 11.25% CAGR from 2026 to 2031, supported by stricter quality control needs and growth in advanced therapies.

Which region is expanding the fastest in automated microbiology?

Asia-Pacific is expected to post the highest growth rate, with a 12.65% CAGR from 2026 to 2031, driven by hospital upgrades, biopharma expansion, and broader first-time automation adoption.

What is the biggest barrier to wider deployment of automated microbiology platforms?

The largest barrier remains the combined burden of high capital cost, service contracts, space requirements, and integration complexity, especially for smaller hospitals and emerging markets.

Page last updated on: