Gene Sequencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.82 Billion |

| Market Size (2031) | USD 14.17 Billion |

| Growth Rate (2026 - 2031) | 12.64% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gene Sequencing Market Analysis by Mordor Intelligence

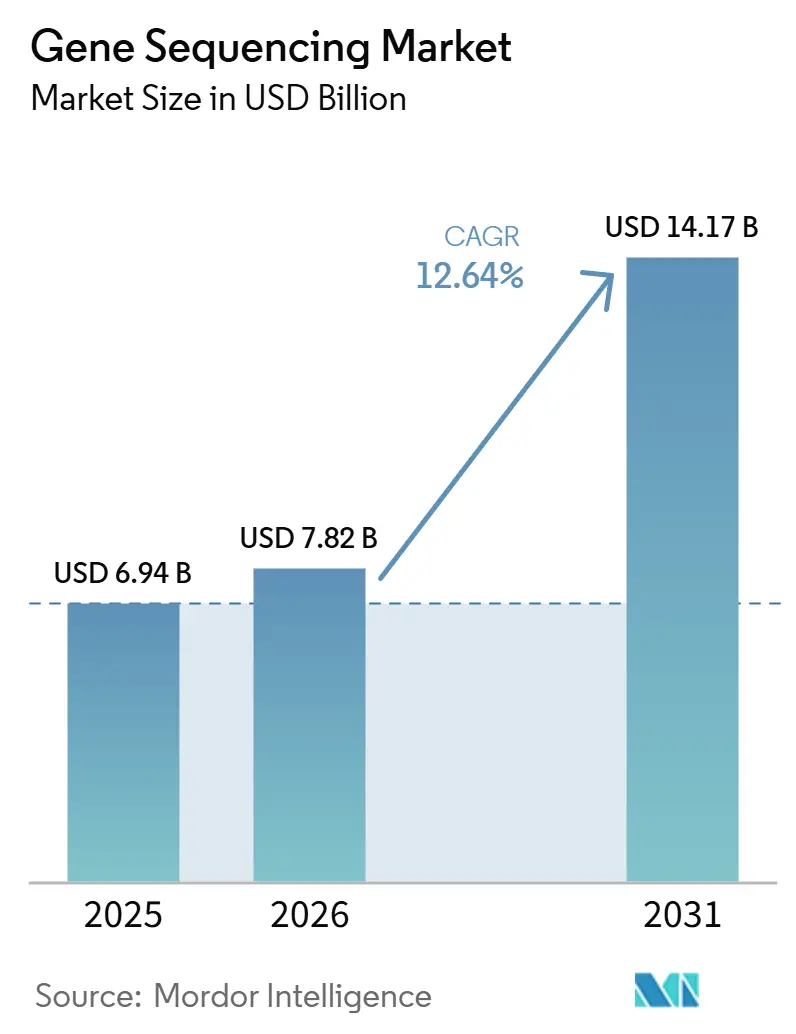

The Gene Sequencing Market size is projected to be USD 6.94 billion in 2025, USD 7.82 billion in 2026, and reach USD 14.17 billion by 2031, growing at a CAGR of 12.64% from 2026 to 2031.

The gene sequencing market is moving deeper into clinical use as precision oncology workflows expand, population genomics programs keep adding scale, and sequencing costs keep falling across high-volume platforms. The gap between research-grade and clinical-grade adoption is narrowing because hospitals, reference labs, and national genomics networks now have stronger reasons to standardize validated workflows and maintain faster turnaround times. The gene sequencing market also benefits from a durable installed-base model because every system placed in a clinical or research lab creates recurring demand for flow cells, reagent kits, and library preparation consumables over several years of operation. Reimbursement support in oncology, wider use of whole-genome sequencing in rare disease settings, and long-read advances in structural variant analysis are all improving the commercial case for new placements and higher test volumes. Competition in the gene sequencing market is also shifting beyond instrument performance because vendors now need tighter bioinformatics integration, clearer clinical validation, and stronger workflow support to keep customers on their platforms over time.

Key Report Takeaways

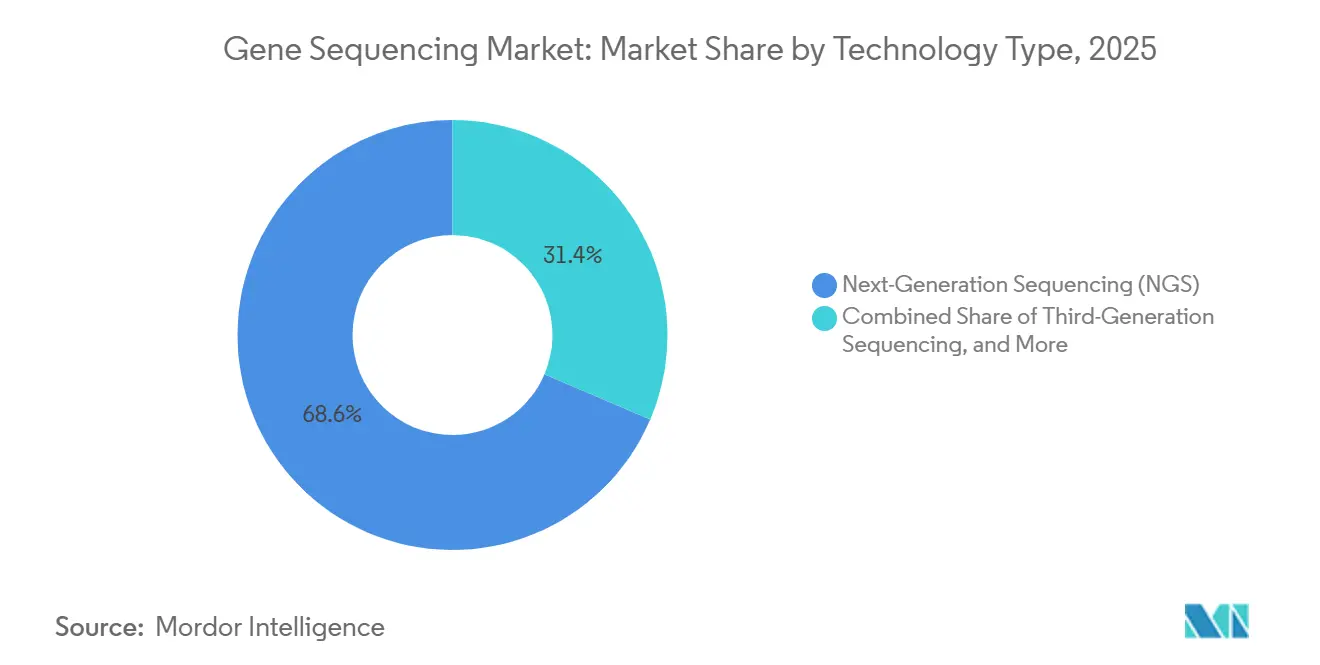

- By technology type, next-generation sequencing led with 68.57% revenue share in 2025, while third-generation sequencing is forecast to expand at 12.96% CAGR through 2031.

- By product, consumables held 52.79% share in 2025, while sequencing instruments are projected to grow at 13.52% CAGR through 2031 in the gene sequencing market.

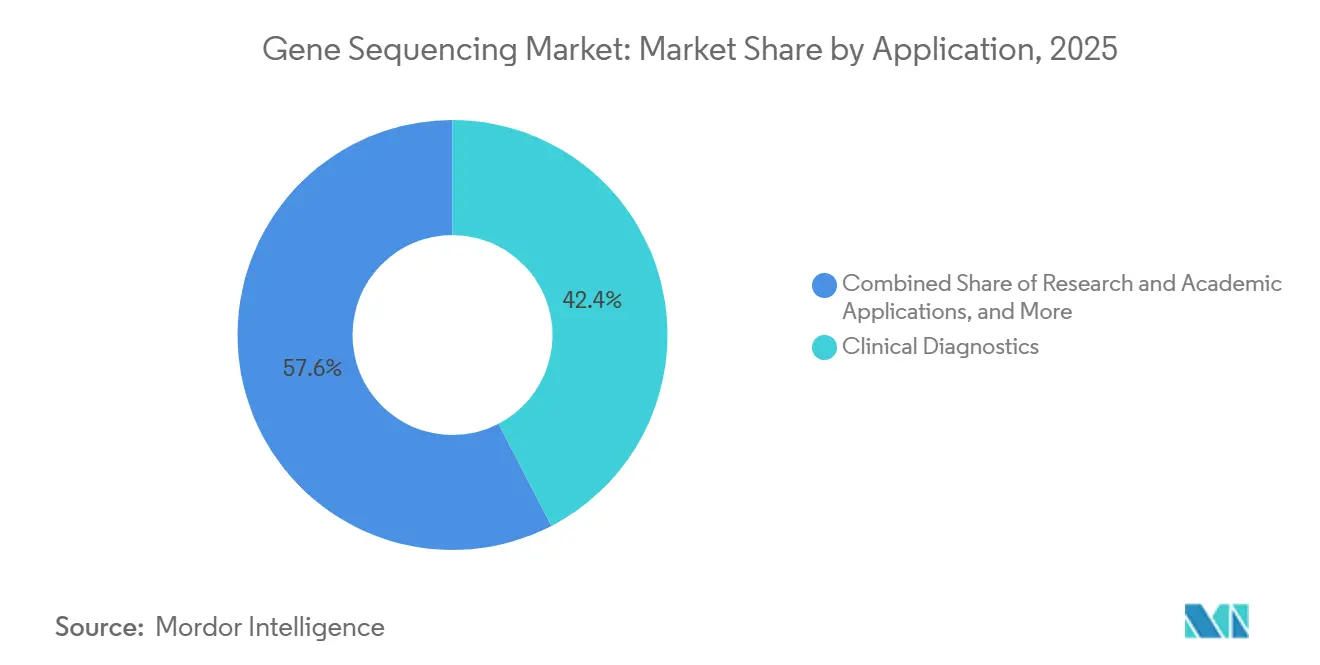

- By application, clinical diagnostics accounted for 42.39% revenue share in 2025, while research and academic applications are expected to advance at 14.38% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies represented 36.14% of spending in 2025, while hospitals and diagnostic laboratories are projected to grow at 15.63% CAGR through 2031 in the gene sequencing market.

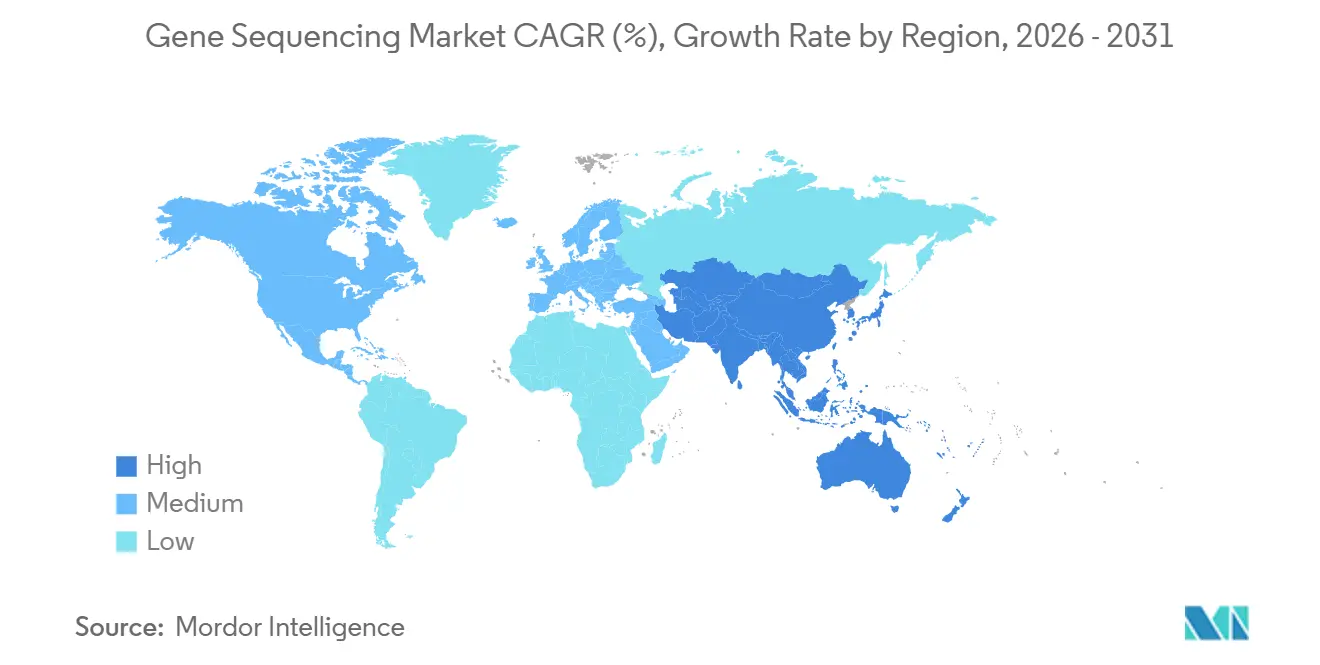

- By geography, North America captured 41.37% revenue share in 2025, while Asia-Pacific is forecast to expand at 14.53% CAGR through 2031 in the gene sequencing market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gene Sequencing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Clinical Adoption of Precision Oncology Panels | +3.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expansion of Rare Disease and Undiagnosed Disease Programs | +1.8% | North America, Europe, APAC | Medium term (2-4 years) |

| Falling Per-Base Sequencing Cost and Higher Throughput | +2.5% | Global | Short term (≤ 2 years) |

| Population-Scale Genomics and Biobank Expansion | +2.1% | Global, with spillover to MEA | Long term (≥ 4 years) |

| Shift Toward Long-Read Sequencing in Structural Variant Discovery | +1.4% | North America, Europe, East Asia | Medium term (2-4 years) |

| Growing Use of Sequencing in Decentralized, Near-Patient Workflows | +1.3% | Global, with early gains in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Clinical Adoption of Precision Oncology Panels

Clinical oncology remains the strongest demand engine in the gene sequencing market because comprehensive genomic profiling still has room to penetrate a larger eligible patient pool. The US Centers for Medicare & Medicaid Services continues to provide a reimbursement foundation through NCD 90.2 for advanced cancer patients when next-generation sequencing tests carry FDA approval or clearance as companion diagnostics, and that framework is supporting lab investment in validated platforms. The same gene sequencing market is also gaining support from minimal residual disease and molecular residual disease monitoring, where repeated liquid biopsy testing raises the need for high-sensitivity sequencing instead of legacy PCR workflows. That pattern matters because serial testing creates recurring run volumes rather than one-time diagnostic events, which improves utilization for installed instruments. As more targeted therapies require companion diagnostic support, labs without sequencing capability face a weaker competitive position and a harder path to clinical relevance. This is why the gene sequencing market is not only adding test volume, but it is also becoming more embedded in routine treatment-selection pathways.

Falling Per-Base Sequencing Cost and Higher Throughput

The gene sequencing market is benefiting from a faster cost reset as vendors push throughput gains and lower consumables expenses into commercial workflows. PacBio stated in 2026 that its SPRQ-Nx chemistry, together with SMRT cell reuse, enabled HiFi whole-genome sequencing below USD 300 per sample at scale, which moves long-read sequencing closer to budget levels that broader clinical programs can support.[1]PacBio SPRQ-Nx Chemistry Now Shipping Worldwide, Enabling Sub-300 HiFi Genomes for Large-Scale Projects and AI-Enhanced Sequencing Illumina also launched TruPath Genome in February 2026 at USD 395 per sample for consumables plus analysis on existing NovaSeq X infrastructure, which lowers adoption friction because labs do not need to buy a new instrument to access long-range genomic insight. These moves change buying behavior because lower per-sample costs make test volume and workflow fit more important than headline instrument pricing alone. In the gene sequencing market, that shift favors vendors that can hold customers through software, assay design, data interpretation, and quality assurance rather than through reagent pricing only. It also means that platforms with weaker workflow integration may struggle even when their raw sequencing performance is competitive.

Population-Scale Genomics and Biobank Expansion

Population genomics programs have become one of the most efficient volume builders in the gene sequencing market because they aggregate demand over many years and across large cohorts. The NIH All of Us Research Program reported in June 2026 that it held more than 535,000 whole genome sequences linked to nearly 482,000 electronic health records, making it the world’s largest integrated genomics and health database.[2]NIH’s All of Us Research Program Is Now the Largest Integrated Genomics and Health Database in the World Nature reported that the UK Biobank completed whole-genome sequencing of 490,640 participants at 32.5× average depth and identified nearly 1.5 billion genetic variants, which shows that national-scale sequencing is already operational rather than experimental. The same dataset also showed the continued limits of short-read whole-genome sequencing in insertions and repetitive regions, which keeps the door open for supplemental long-read work in future cohort phases.[3]Whole-Genome Sequencing of 490,640 UK Biobank Participants That matters because the gene sequencing market does not capture value from the initial cohort only; it also captures value from reanalysis, extension studies, and reference genome improvements that follow the first sequencing cycle. As more countries build similar programs, favored platform positions can last for years because the chosen workflow becomes embedded in procurement, informatics, and downstream analysis.

Shift Toward Long-Read Sequencing in Structural Variant Discovery

Long-read platforms are no longer a fringe option in the gene sequencing market because they are showing clinically relevant value in areas where short-read methods leave gaps. Genome Research reported in 2025 that HiFi long-read sequencing identified causal variants in 11.8% of previously unsolved rare disease families and candidate variants in another 5.4%, adding diagnostic yield that standard short-read exome or genome approaches had missed.[4]Unraveling Undiagnosed Rare Disease Cases by HiFi Long-Read Genome Sequencing That result is commercially important because a large residual pool of undiagnosed patients remains after first-line short-read testing, which creates a measurable demand base for long-read reanalysis. Korea’s Disease Control and Prevention Agency expanded its rare disease diagnostic support program in 2025 to cover 1,314 eligible diseases and 800 patients annually, with whole-genome sequencing central to the protocol. Even so, labs still face a practical transition challenge because long-read workflows require different sample preparation, bioinformatics pipelines, and clinical validation steps than established short-read programs. In the gene sequencing market, this slows full migration, but it does not weaken the demand case for long-read adoption in structural variant analysis, repeat expansion work, and difficult rare disease cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity of Sequencers and Automation | -1.2% | Global, especially low- and middle-income markets | Medium term (2-4 years) |

| Uneven Reimbursement for Clinical Sequencing Across Markets | -0.8% | APAC, South America, MEA | Long term (≥ 4 years) |

| Data Governance, Privacy, and Cross-Border Genomic Data Limits | -0.6% | EU, China, with spillover to North America | Medium term (2-4 years) |

| Shortage of Trained Bioinformatics and Clinical Interpretation Talent | -0.5% | Global, most acute in APAC and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity of Sequencers and Automation

The gene sequencing market still carries one of the heavier capital barriers in diagnostics because high-throughput instruments require large upfront spending and multi-year depreciation before labs can earn healthy margins. High-end systems remain difficult for many community hospitals and regional laboratories to justify without leasing options, shared-service models, or volume commitments. The problem extends beyond the sequencer because clinical-scale operation also needs liquid handling, automated library preparation, and secure informatics infrastructure. Falling reagent costs help, but they do not remove the burden of underused instruments in labs that lack consistent sample flow. This creates a two-tier structure in the gene sequencing market, where well-funded academic centers and reference labs can spread costs over larger volumes while smaller providers struggle to build a viable business case. It also delays wider geographic expansion because many low- and middle-income markets need lower-risk deployment models before local sequencing capacity can scale.

Data Governance, Privacy, and Cross-Border Genomic Data Limits

The gene sequencing market faces a structural barrier in data governance because genomic information is permanent, inheritable, and treated as highly sensitive personal data. The European Union’s General Data Protection Regulation classifies genetic data as a special category and places stricter conditions on consent and cross-border transfer, which adds compliance and infrastructure obligations for sequencing labs and vendors. China’s human genetic resources rules also limit the transfer of Chinese genomic data to foreign entities, which makes multinational sequencing workflows harder to design and scale across borders. Those differences fragment the gene sequencing market into more localized operating models and limit the full efficiency that could come from shared analysis environments. The burden is especially visible in multinational drug development because globally sequenced cohorts cannot always be combined in one hosted analysis setting without regulatory review. At the same time, the shortage of trained bioinformatics and clinical interpretation talent raises the cost of complying with these rules because labs need skilled teams to manage secure pipelines, interpretation, and reporting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Third-Generation Gains Reshape a Market NGS Built

Next-generation sequencing held 68.57% of the gene sequencing market share in 2025, reflecting years of clinical validation, a deep reagent ecosystem, and a large installed base across academic centers and reference laboratories. That leadership remains hard to displace because customers already have validated workflows, trained teams, and procurement relationships tied to short-read platforms. Sanger sequencing still retains a smaller but durable role in confirmation work, especially when labs need lower-throughput validation without running a full next-generation workflow. This keeps a practical place for older methods even as high-volume sequencing moves toward broader panel, exome, and genome use. The gene sequencing market therefore remains anchored by next-generation sequencing today, but that anchor is becoming less exclusive as long-read systems improve on cost and workflow readiness.

Third-generation sequencing is projected to expand at 12.96% CAGR through 2031, making it the fastest-growing technology category in the gene sequencing market. Demand is rising because structural variant detection, phased genome assembly, methylation analysis, and repeat region resolution are all areas where native long reads add value that short-read methods do not fully match. PacBio stated in 2026 that SPRQ-Nx chemistry allows SMRT cell reuse and supports HiFi whole-genome sequencing below USD 300 per sample at scale, which marks an important affordability threshold for broader program adoption. Illumina’s TruPath Genome also shows that short-read incumbents are trying to keep customers by adding long-range insight on existing hardware rather than surrendering that demand to long-read specialists. By 2031, the technology mix in the gene sequencing market is likely to look less one-sided because labs that need difficult variant resolution will have stronger reasons to adopt or add long-read capability.

By Product: Consumables Anchor Revenue While Instruments Drive Expansion

Consumables accounted for 52.79% of revenue in 2025, which shows how strongly the gene sequencing market depends on recurring purchases rather than one-time capital sales. Flow cells, reagent kits, and library preparation products are bought on every run, so revenue rises with throughput even when instrument placement slows. This pattern gives established vendors a more stable base because each active instrument becomes a repeat source of consumable demand over several years. It also means customer retention matters as much as new customer acquisition, since losing a platform account affects a recurring revenue stream rather than a single product sale. The gene sequencing industry, therefore, relies on installed-base durability, workflow convenience, and assay consistency to protect its largest product pool.

The gene sequencing market size for sequencing instruments is projected to expand at 13.52% CAGR from 2026 to 2031 as labs upgrade older benchtop systems and add higher-throughput platforms for clinical panels, exomes, and whole genomes. Instrument demand is also supported by the need to move testing closer to decentralized clinical settings, where turnaround time and sample control matter more. Even so, the long-run revenue mix is likely to lean further toward consumables because replacement cycles stretch across several years while run volumes can rise more continuously. This helps explain why vendors are pairing new instrument launches with chemistry, software, and automation changes that lift the value of each installed system rather than relying on placements alone. In the gene sequencing market, instruments open the door, but consumables still determine the durability of the revenue model.

By Application: Research Spending Rebounds While Clinical Diagnostics Consolidates

Clinical diagnostics represented 42.39% of the gene sequencing market share in 2025, making it the largest application area in the current revenue mix. Oncology remains the main center of gravity within this segment because targeted therapy selection, comprehensive genomic profiling, and residual disease monitoring all depend on reliable sequencing workflows. Clinical demand also tends to be more durable once reimbursement, validation, and reporting pathways are established in a hospital or reference lab setting. That gives this application a firmer operational base than project-funded research work, even when research demand is strong. The gene sequencing market, therefore, continues to draw much of its present revenue weight from clinical diagnostics, even as newer use cases broaden the application mix.

The gene sequencing market size for research and academic applications is projected to grow at 14.38% CAGR through 2031 as government-backed genomics programs and functional genomics work regain momentum. The NIH All of Us Research Program reported in June 2026 that it included more than 535,000 whole genomes, nearly 10,000 participants with proteomic data, and more than 14,500 participants with long-read whole-genome sequences, which reflects the scale now moving through public research networks. Population genomics is evolving especially quickly in data volume because cohort expansion, reanalysis, and multiomics layers all add new sequencing demand over time. Nature’s 2025 publication on UK Biobank whole-genome sequencing also showed that national health systems can now run sequencing at a scale that materially expands actionable genotype discovery when structural variants are included. In the gene sequencing market, this creates a favorable position for vendors that secure national program nodes early because those selections often shape platform use over a multi-year period.

By End User: Hospitals Accelerate Adoption as Pharma Deepens Integration

Pharmaceutical and biotechnology companies accounted for 36.14% of end-user spending in 2025, which reflects how deeply sequencing is embedded across target discovery, biomarker work, clinical trial stratification, and translational research. These buyers often adopt sequencing earlier than clinical providers because they can connect genomic data directly to pipeline decisions and development timelines. Their use of the gene sequencing market is also broad, spanning discovery science, trial operations, companion diagnostic work, and portfolio prioritization. That breadth keeps this group important even as clinical end users accelerate faster. It also gives vendors a reason to design offerings that align with regulated research and development workflows as well as clinical reporting needs.

The gene sequencing market size for hospitals and diagnostic laboratories is projected to rise at 15.63% CAGR through 2031 as testing moves from centralized reference settings into more in-house clinical workflows. Illumina and SPT Labtech announced in February 2026 that they would develop an automated sample preparation platform for decentralized healthcare settings around the MiSeq i100, which had reached its 1,000th shipment, showing how vendors are adapting products for faster local use SPTLABTECH.COM. This shift lets hospitals keep more of the diagnostic pathway and the associated economics, but it also forces them to build or buy bioinformatics and interpretation capacity. A 2025 workforce review reported that only 5,629 certified genetic counselors served the US population and that 41% of laboratories reported an inability to fill genomic technologist roles, which highlights a practical bottleneck in scaling in-house adoption DOI.ORG. In the gene sequencing market, vendors that package software, automation, and clinical decision support alongside instruments are better placed to help hospitals overcome this staffing constraint.

Geography Analysis

North America held 41.37% of gene sequencing market share in 2025, which kept it as the largest regional contributor. The United States continues to benefit from a stronger reimbursement base in oncology because CMS NCD 90.2 supports approved or cleared next-generation sequencing companion diagnostics for advanced cancer patients. That coverage structure supports investment in validated clinical sequencing workflows across cancer centers, hospital labs, and reference networks. Florida’s Medicaid program also activated reimbursement in 2025 for rapid whole-genome sequencing at USD 2,716.9 per test, which shows that clinical whole-genome sequencing is extending into neonatal and pediatric rare disease use cases at the state level. Canada and Mexico remain smaller contributors within the region, but lower cost thresholds and wider rare disease access are helping broaden the gene sequencing market beyond the United States.

Europe remained the second-largest regional block in 2025, with Germany, the United Kingdom, and France contributing most of the regional revenue. The United Kingdom has a working operational base through Genomics England and the NHS Genomic Medicine Service, which gives whole-genome sequencing a clearer pathway in rare disease and cancer care. Germany’s statutory health insurance system has also deepened support for comprehensive genomic profiling in oncology, which is helping sequencing move further beyond academic centers. The region’s growth is still moderated by GDPR-driven data residency and transfer requirements, which raise infrastructure costs and make it harder for smaller labs to match the operating resilience of large platform vendors.

Asia-Pacific is projected to expand at 14.53% CAGR through 2031, making it the fastest-growing geography in the gene sequencing market. China’s competitive environment is being reshaped by aggressive domestic platform positioning and stricter control over foreign genomic data participation. MGI Tech announced in March 2026 the acquisition of STOmics and CycloneSEQ, which broadened its coverage across short-read sequencing, long-read nanopore sequencing, and spatial omics under one portfolio. South Korea is also strengthening long-read and reference genome capability, while India’s genome mapping efforts are supporting sustained instrument and consumable demand over multiple years. The Middle East and Africa and South America remain at earlier stages, but genomics infrastructure spending in GCC markets and the expansion of clinical sequencing networks in Brazil are creating identifiable entry points for the gene sequencing market.

Competitive Landscape

The gene sequencing market remains oligopolistic in high-throughput clinical sequencing, even as adjacent niches are becoming more crowded. Illumina continues to hold an estimated share above 70% in high-throughput short-read sequencing, supported by its clinical validation depth, DRAGEN bioinformatics ecosystem, and large NovaSeq X installed base. That position gives the company a strong hold over existing workflows, but it also leaves it exposed to competitors that target lower per-run costs or differentiated data types. PacBio’s February 2026 sale of its short-read sequencing assets to Illumina for USD 48.1 million shows a clearer split in strategic direction, with PacBio concentrating on high-accuracy long-read sequencing while Illumina deepens its short-read and hybrid capabilities. In the gene sequencing market, this means the largest players are no longer competing only for throughput leadership; they are also deciding which data types and workflow positions they want to own.

The gene sequencing market is also opening competitive space in portable use cases, ultra-low-input sequencing, and multimodal workflows that combine sequencing with other omics layers. Illumina’s February 2026 launch of TruPath Genome is one example of a defensive move that protects its installed base by adding long-range genomic information on existing NovaSeq X systems instead of forcing customers into a new platform class. PacBio’s SPRQ-Nx chemistry is another example because it lowers long-read economics and makes the company’s proposition more practical for larger-scale clinical or population programs. MGI Tech’s 2026 acquisition of STOmics and CycloneSEQ points to a third strategy, where integrated short-read, nanopore, and spatial capabilities are used to make one vendor harder to displace across a broader omics stack. These moves show that the gene sequencing market is still concentrated at the core, but competition is widening around workflow breadth and the ability to combine data types within one customer relationship.

Gene Sequencing Industry Leaders

Agilent Technologies, Inc.

Becton, Dickinson and Company

Bio-Rad Laboratories, Inc.

Danaher Corporation

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Bifrost Biosystems signed a supply agreement with Illumina to access sequencing chemistry for its optical pooled screening platform, reflecting the growing role of application-specific sequencing partnerships in expanding the reach of established reagent ecosystems beyond core genomics labs.

- June 2026: The NIH All of Us Research Program became the world’s largest integrated genomics and health database, with data from more than 747,000 participants, including more than 535,000 whole genome sequences linked to electronic health records, available to researchers at no cost, alongside the program’s first multiomics data release, including RNA sequencing from nearly 9,000 participants and long-read whole-genome sequencing from more than 14,500 participants.

- April 2026: Illumina launched DRAGEN v4.5, expanding its bioinformatics software suite with improved variant calling in complex genomic regions, expanded pangenome representation, and native analytical support for TruPath Genome data.

- March 2026: MGI Tech announced the acquisition of STOmics and CycloneSEQ from BGI Group, positioning MGI as a manufacturer offering integrated short-read sequencing, long-read nanopore sequencing, generative lab intelligence, and spatial omics within one portfolio.

Global Gene Sequencing Market Report Scope

As per the scope of the report, gene sequencing is the laboratory process of determining the exact order of nucleotide bases within a specific gene, revealing its complete genetic blueprint. It uses technologies like Sanger sequencing and next‑generation sequencing (NGS) to decode DNA with high accuracy. This allows researchers and clinicians to identify mutations, disease‑associated variants, and functional regions within genes, supporting diagnostics, personalized medicine, and genetic research.

The gene sequencing market is segmented by technology type, product, application, end user, and geography. By technology type, the market is segmented into next-generation sequencing (NGS), sanger sequencing, third-generation sequencing, and others. By product, the market is segmented into sequencing instruments, consumables, and others. By application, the market is segmented into clinical diagnostics, research and academic applications, drug discovery and development, population genomics, and others. By end user, the market is segmented into hospitals and diagnostic laboratories, pharmaceutical and biotechnology companies, academic and research institutes, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Next-Generation Sequencing (NGS) |

| Sanger Sequencing |

| Third-Generation Sequencing |

| Others |

| Sequencing Instruments |

| Consumables |

| Others |

| Clinical Diagnostics |

| Research and Academic Applications |

| Drug Discovery and Development |

| Population Genomics |

| Others |

| Hospitals and Diagnostic Laboratories |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology Type | Next-Generation Sequencing (NGS) | |

| Sanger Sequencing | ||

| Third-Generation Sequencing | ||

| Others | ||

| By Product | Sequencing Instruments | |

| Consumables | ||

| Others | ||

| By Application | Clinical Diagnostics | |

| Research and Academic Applications | ||

| Drug Discovery and Development | ||

| Population Genomics | ||

| Others | ||

| By End User | Hospitals and Diagnostic Laboratories | |

| Pharmaceutical and Biotechnology Companies | ||

| Academic and Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for gene sequencing through 2031?

Next-generation sequencing led with 68.57% revenue share in 2025 because it has the deepest clinical validation, the broadest installed base, and the most established reagent ecosystem.

Which part of the business creates the most recurring revenue?

Consumables held 52.79% share in 2025, which shows that repeat purchases of flow cells, reagents, and library preparation kits remain the main revenue anchor.

Why is long-read sequencing gaining traction?

Long-read platforms are gaining adoption because they improve structural variant detection, repeat region analysis, and unsolved rare disease diagnosis, with third-generation sequencing projected to grow at 12.96% CAGR through 2031.

Which end users are expanding the fastest?

Hospitals and diagnostic laboratories are projected to grow at 15.63% CAGR through 2031 as sequencing moves into more in-house clinical workflows supported by automation and standardized panels.

Which region is growing the fastest?

Asia-Pacific is forecast to expand at 14.53% CAGR through 2031 as domestic platform development, national genome initiatives, and long-read reference projects add multi-year sequencing demand.

Page last updated on: