Bioprocess Analyzers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 5.51 Billion |

| Growth Rate (2026 - 2031) | 15.54% CAGR |

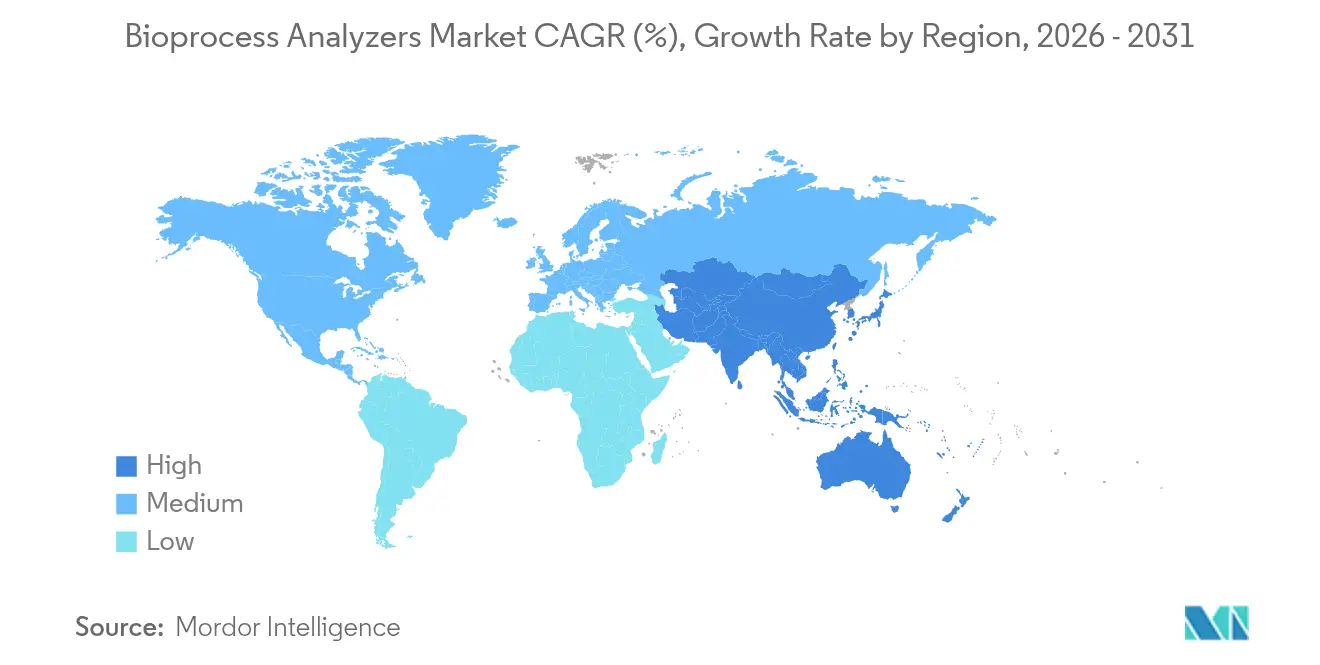

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioprocess Analyzers Market Analysis by Mordor Intelligence

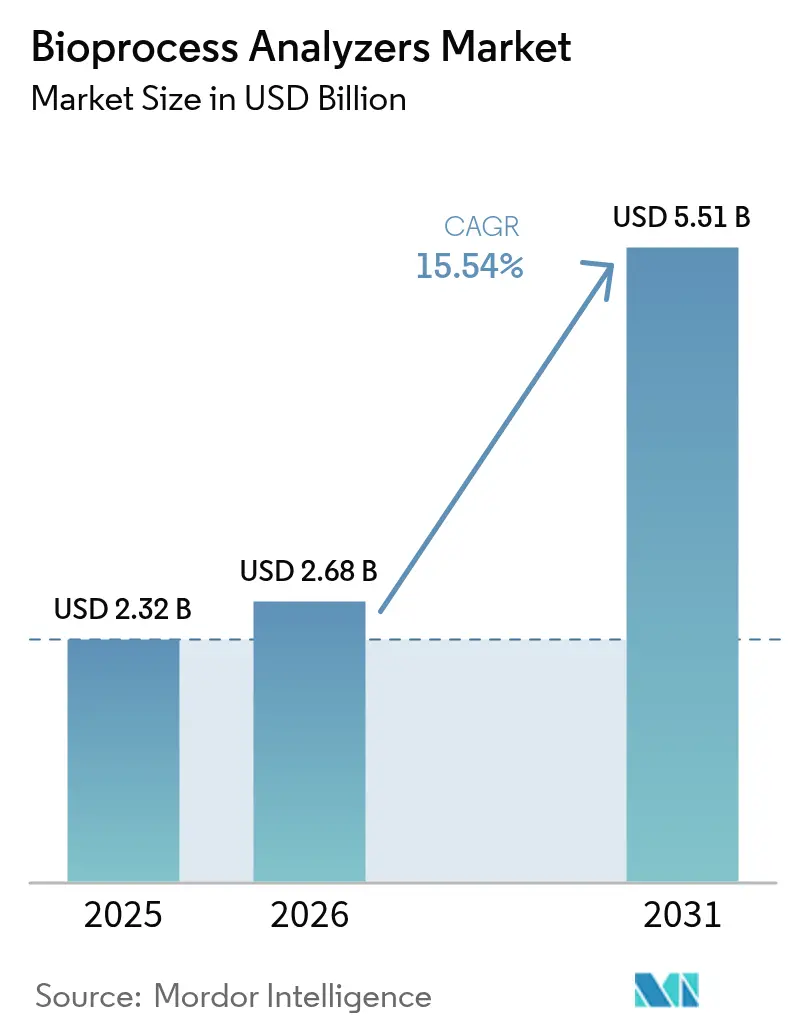

The bioprocess analyzers market size was valued at USD 2.32 billion in 2025 and estimated to grow from USD 2.68 billion in 2026 to reach USD 5.51 billion by 2031, at a CAGR of 15.54% during the forecast period (2026-2031). Demand accelerates as manufacturers abandon retrospective batch testing in favor of real-time optimization, spurred by regulatory preference for continuous manufacturing and the pandemic-era proof of concept delivered during rapid COVID-19 vaccine scale-up. Growth links directly to expanded global biomanufacturing capacity, aggressive investment in single-use technology, and the maturing digital-twin ecosystem that fuses spectroscopy with AI-driven models for predictive quality control. Instruments remain the backbone of monitoring workflows, yet software and analytics capture disproportionate incremental dollars as factories deploy closed-loop control strategies. Regionally, North America retains a dominant installed base, while Asia-Pacific’s surge in green-field plants drives the highest incremental volume. M&A continues at a measured pace, with leading suppliers consolidating to offer vertically integrated hardware-software-service stacks that help end-users navigate validation, data integrity, and workforce shortages.

Key Report Takeaways

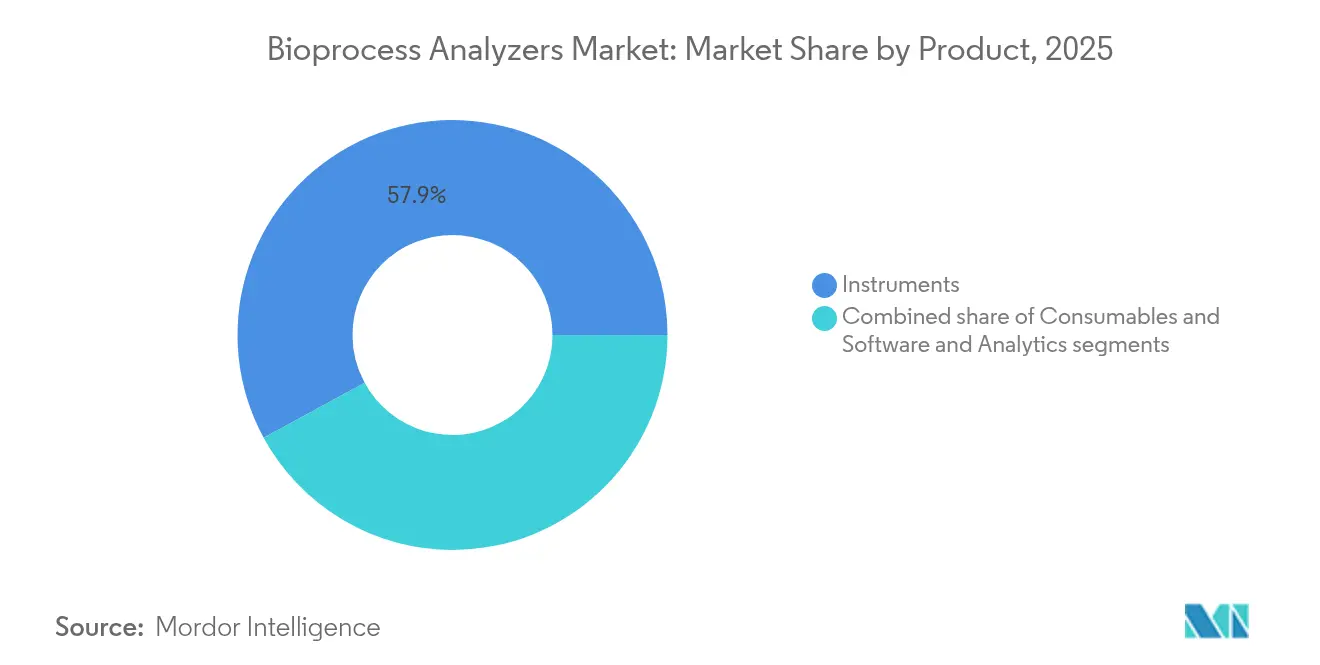

- By product category, instruments led with 57.93% revenue share in 2025; software and analytics are projected to expand at a 17.34% CAGR to 2031.

- By measurement principle, Raman spectroscopy secured 42.02% of the bioprocess analyzers market share in 2025, while mass spectrometry records the highest projected CAGR at 17.38% through 2031.

- By type, substrate analysis accounted for 46.09% share of the bioprocess analyzers market size in 2025 and physicochemical parameter monitoring is advancing at a 17.22% CAGR through 2031.

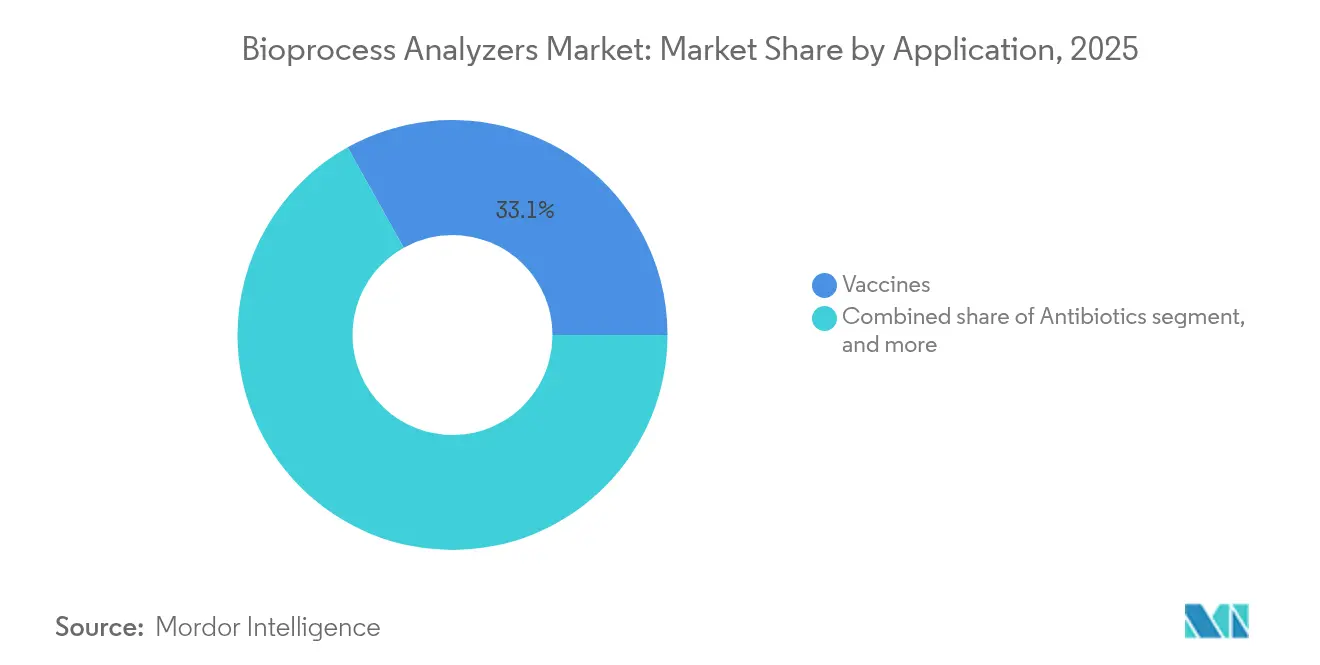

- By application, vaccines captured 33.11% share in 2025 and biosimilars are forecast to grow at an 18.63% CAGR to 2031.

- By end-user, biopharmaceutical companies held 58.21% revenue share in 2025, whereas contract manufacturers are poised for an 18.31% CAGR through 2031.

- By geography, North America commanded 39.84% share in 2025; Asia-Pacific is on track for a 16.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioprocess Analyzers Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of biopharmaceutical manufacturing capacity | +3.2% | Global; North America & Asia-Pacific hubs | Medium term (2-4 years) |

| Rising adoption of process analytical technology (PAT) | +2.8% | North America & EU leading; APAC accelerating | Short term (≤2 years) |

| Increasing R&D expenditure in life sciences | +2.1% | Global; emphasis on developed markets | Long term (≥4 years) |

| Surge in demand for personalized medicine | +1.9% | North America & EU core; spillover to APAC | Medium term (2-4 years) |

| Expansion of contract manufacturing organizations (CMOs) | +2.4% | Global; fastest in Asia-Pacific | Short term (≤2 years) |

| Favorable regulatory support for continuous manufacturing | +1.7% | North America & EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growth of Biopharmaceutical Manufacturing Capacity

Rapid green-field and brown-field expansion pushes global installed capacity above 16.5 million L across more than 1,500 facilities, each new bioreactor requiring its own analytical suite. Samsung Biologics’ Plant 5 alone adds 180,000 L, bringing the campus total to 784,000 L and catalyzing orders for spectroscopy, mass-spectrometry, and electrochemical sensors. Similar momentum is visible in North Carolina, where Fujifilm is building eight additional 20,000 L reactors, creating downstream pull for in-line Raman probes. Developing regions amplify demand because regulators mandate equivalency with ICH-compliant processes, forcing local manufacturers to buy validated systems from global vendors. Larger vessels intensify sample throughput requirements, nudging buyers toward multiplexed solutions that monitor metabolite, nutrient, and physicochemical indicators simultaneously. Collectively these projects raise the bioprocess analyzers market baseline and extend replacement cycles as firms standardize on platform technologies.

Rising Adoption of Process Analytical Technology (PAT)

The FDA’s January 2025 draft guidance endorses real-time release testing, clarifying validation pathways and unfreezing capex that had been on hold. Manufacturers fast-track “Process Analytics 4.0,” integrating Raman, NIR, and MS with machine-learning models that hit R² > 0.9 for glucose, lactate, and IgG prediction in small-scale runs. Digital twins compare live data against mechanistic simulations, enabling feed-rate adjustments within seconds instead of hours. These closed-loop architectures cut deviations and shorten batch-review cycles, providing CFO-level ROI that accelerates budget approvals. Early adopters report 25% reductions in product-release timelines, reinforcing the business case for enterprise-wide roll-outs. Vendors respond by bundling software subscriptions with hardware to lock in long-term annuity revenue and differentiate against low-cost sensor entrants.

Increasing R&D Expenditure in Life Sciences

Global life-sciences R&D outlays are projected to reach USD 516.79 billion in 2024, with biologics capturing the lion’s share. Early-stage pipelines increasingly feature cell, gene, and mRNA modalities that require more nuanced process monitoring than classical monoclonal antibodies. Beckman Coulter’s CytoFLEX mosaic, capable of detecting 80 nm particles, addresses nanoparticle analytics central to gene-therapy vectors. Specialized HPLC methods for in-vitro transcription elevate the need for multi-attribute analytical platforms that correlate upstream RNA quality with downstream potency. R&D groups adopt benchtop mass spectrometry for rapid metabolomics, shortening clone-selection cycles. Collectively, these activities funnel a steady stream of demand into the bioprocess analyzers market well before commercial scale, creating a structural tailwind that extends through the product life cycle.

Surge in Demand for Personalized Medicine

Shift toward patient-specific therapies compresses production runs and raises the premium on flexibility. Automated, modular analyzers that can be redeployed within hours gain traction because production lines must pivot between indications. Decentralized factories—sometimes colocated with hospitals—demand compact systems with remote-operation capability for sites lacking advanced instrumentation staff[1]International Society for Pharmaceutical Engineering, “Decentralized Manufacturing White Paper,” ispe.org. AI engines that self-calibrate to each donor’s cell-growth profile enable tighter process control, fueling double-digit software revenue growth. In gene-modified cell therapy, inline spectroscopy tracks vector copy number and transduction efficiency in real time, improving batch acceptance rates. Suppliers that provide integrated hardware, consumables, and SaaS analytics become strategic partners rather than commodity vendors, deepening switching costs and fortifying recurring revenue.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating costs | -2.1% | Global; smaller and emerging biotech firms most affected | Short term (≤2 years) |

| Stringent validation and compliance requirements | -1.8% | North America & EU; extending to APAC | Medium term (2-4 years) |

| Shortage of skilled bioprocessing professionals | -1.5% | Global; acute in rapidly expanding APAC markets | Medium term (2-4 years) |

| Data integration and interoperability challenges | -1.3% | Global; multi-site manufacturers | Short–medium term (≤3 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs

An integrated PAT workstation can top USD 100,000, discouraging adoption among seed-stage biotech firms and academic labs[2]bioRxiv, “Cost Analysis of PAT Adoption in Academic Labs,” biorxiv.org. Even when capital is secured, ongoing expenses for reagents, calibration standards, and service contracts erode budgets. Attempts to create DIY or open-hardware solutions lower entry barriers but lack the GMP pedigree required for licensed production. Cost-sensitive buyers delay upgrades, extending the use of legacy off-line assays despite productivity penalties. Vendors counter by offering leasing, pay-per-sample, and cloud-based analytics to smooth cash outflows. Still, sticker shock remains a tangible drag on short-term growth, particularly in regions where grant funding cycles dictate purchasing capacity.

Stringent Validation and Compliance Requirements

Qualification of AI-enabled analyzers is a moving target because adaptive algorithms fall outside classical validation templates[3]Parenteral Drug Association, “Validation of AI Systems in GMP Environments,” pda.org. Sponsors often run dual workflows—traditional assays in parallel with real-time systems—to satisfy auditors, effectively doubling workload and dampening ROI. Divergent regional rules force multinationals to tailor validation packages, prolonging tech-transfer timelines. Skilled compliance engineers are scarce, inflating labor costs and creating project bottlenecks. Vendors are investing in pre-validated libraries and turnkey documentation to accelerate deployment, but uncertainty persists, muting the pace at which the bioprocess analyzers market converts early adopters into mainstream buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Instruments Dominate Despite Software Surge

Hardware remained essential, with the instruments segment contributing 57.93% of 2025 revenue. That share reflects a baseline need for tangible sensors, spectroscopy units, and samplers that physically interact with bioreactors. Demand for single-use compatible probes expands the consumables annuity, particularly where disposable bags represent 85% of upstream workflows. The bioprocess analyzers market size for instruments is projected to scale in tandem with mega-plant roll-outs, but growth rates moderate as installed bases mature in legacy geographies.

Software and analytics, although just 14.1% of 2025 spending, deliver a 17.34% CAGR as factories transition to fully digital twins. AI-enabled platforms extend beyond data logging to predictive maintenance and automatic parameter correction, raising overall equipment effectiveness by double digits. The swelling data footprint encourages cloud-native architectures, driving partnerships between instrument vendors and hyperscale providers. This interplay shifts wallet share toward recurring licenses, reshaping vendor P&L and introducing SaaS valuation multiples into the traditionally hardware-centric bioprocess analyzers industry.

By Measurement Principle: Raman Leads While Mass Spectrometry Accelerates

Raman spectroscopy captured 42.02% revenue in 2025 by offering non-destructive, water-tolerant insight into metabolite profiles without sample preparation. Inline fiber optics allow continuous tracking of glucose, lactate, and amino-acid pools, underpinning closed-loop nutrient feeds. Model libraries developed in mini-bioreactors transfer seamlessly to manufacturing scale, lowering calibration costs.

Mass spectrometry, however, edges into mainstream acceptance with a 17.38% CAGR. Microfluidic interfaces now permit online sampling at sub-milliliter volumes, enabling real-time titer and impurity maps previously possible only off-line. Vendors emphasize high-resolution, low-maintenance designs to dispel perceptions of complexity. NIR retains traction for biomass estimation, while electrochemical sensors offer low-cost redundancy for critical-quality attributes, rounding out a diversified measurement portfolio that sustains the bioprocess analyzers market.

By Type: Substrate Analysis Dominates Amid Physicochemical Growth

Nutrient availability dictates cell-culture performance, so substrate analysis owned 46.09% market revenue in 2025, tracking variables like glucose, glutamine, and key minerals. High-density perfusion cultures intensify consumption dynamics, renewing demand for multichannel analyzers that monitor substrates alongside waste products. Continuous production elevates the value of concentration detectors that validate steady-state conditions.

Physicochemical monitoring enjoys a 17.22% CAGR, reflecting broader adoption of automated pH, DO, and CO₂ probes linked to plant-wide control systems. As operators pursue real-time release testing, inline confirmation of viscosity and osmolality gains favor. The convergence of substrate, metabolite, and physicochemical data inside unified dashboards reinforces vendor propositions around holistic process visibility, ensuring sustainable expansion of the bioprocess analyzers market size for integrated solutions.

By Application: Vaccines Lead While Biosimilars Surge

Vaccines retained 33.11% of revenue in 2025 thanks to global pandemic-preparedness spending and mRNA platform proliferation. Viral-vector and lipid-nanoparticle processes pose stringent requirements for particle-size, RNA-encapsulation, and potency control, each dependent on high-frequency analyte readings. Regulatory expectations for rapid lot-release further embed real-time analytics.

Biosimilars clock the fastest trajectory at an 18.63% CAGR because demonstrating analytical similarity demands deeper characterization than innovator products. High-resolution mass spectrometry paired with LC techniques forms a multi-attribute method that enables simultaneous monitoring of glycosylation, oxidation, and deamidation. As blockbuster biologics face patent expiry, producers scale capacity in Asia while deploying state-of-the-art analyzers to comply with EMA and FDA comparability guidelines, buoying the bioprocess analyzers market share for advanced instruments.

By End-User: Biopharma Companies Lead CMO Growth

Originator biopharma retained 58.21% revenue share in 2025, reflecting decades of internal manufacturing investment. Even so, internal facilities increasingly resemble commercial CMOs, standardizing on flexible, single-use lines empowered by PAT.

Contract manufacturing and research organizations sprint ahead at an 18.31% CAGR, driven by small biotech outsourcing and big-pharma hedging capacity risk. CMOs operationalize economies of scale in analytical assets by servicing multiple molecules concurrently. Standardized calibration protocols and automated sampling cut changeover to hours, translating instrumentation into revenue faster than in single-product plants. The resulting spending boom provides a diversified revenue stream for vendors, further expanding the global bioprocess analyzers market.

Geography Analysis

North America held 39.84% of 2025 revenue due to a dense concentration of GMP facilities, proactive FDA policy on PAT, and more than USD 160 billion in announced pharmaceutical capex across 2025 projects. Mega-acquisitions such as Lonza’s purchase of Roche’s Vacaville site—housing 330,000 L of reactors—underscore continued maturation of the local supply chain. Meanwhile, draft BIOSECURE legislation could redirect USD 2.1 billion worth of biologics production contracts away from Chinese entities, further stimulating domestic instrument demand. In Canada, government co-investment grants expedite vaccine analytics expansion, offering additional runway for hardware sales.

Asia-Pacific posts a 16.23% CAGR as regional champions execute multi-billion-dollar builds. Samsung Biologics targets 964,000 L of capacity upon completion of Plant 6, generating downstream pull for spectroscopy, chromatography, and data-management systems. Japan’s Five-Year Startup Plan allocates tax incentives for biotech, pushing smaller firms to equip pilot plants with scalable analytics. China’s pursuit of CGMP parity anchors demand for FDA-validated instrumentation, while India’s bioeconomy roadmap pushes indigenous companies to source high-spec measuring tools to tap western outsourcing flows. Southeast Asia emerges as a secondary hub, where CDMOs erect smaller yet sophisticated suites designed to export therapies under stringent ICH standards.

Europe maintains steady, low-double-digit growth underpinned by strong regulatory emphasis on data integrity and single-use innovation, epitomized by Sartorius’ BioPAT Spectro Raman platform. Germany and Switzerland remain pillars for equipment design and application support, while Ireland leverages a skilled workforce and tax regimes to attract U.S. biologics projects. Elsewhere, Middle East & Africa and South America represent nascent opportunities: local governments fund technology-transfer consortia to secure vaccine self-sufficiency, creating pilot orders that seed future adoption. Together these regional dynamics maintain an upward trajectory for the global bioprocess analyzers market.

Regulatory Landscape

Regulatory expectations for bioprocess analyzers are shaped largely by pharmaceutical GMP frameworks and the Process Analytical Technology (PAT) paradigm, which links in-process measurement to Quality by Design and risk-based control. Method lifecycle requirements have tightened through ICH Q14 (Analytical Procedure Development) and ICH Q2 (Validation of Analytical Procedures) updates finalized in March 2024, increasing expectations on suppliers and end users to show method robustness, transferability, and ongoing performance monitoring for in-line and at-line analyzers.

In the United States, FDA has continued to formalize its posture toward innovative and continuous manufacturing, including a strategy document published via the Federal Register in December 2025 that keeps real-time monitoring and modernization of manufacturing technologies in focus. In Europe, EMA updated biological-medicinal-product guidance in December 2025 with added emphasis on critical in-process controls and reference standard qualification, while also providing pathways such as Qualification of Novel Methodologies (QoNM) for new analytical approaches used in development and manufacturing. Across regions, compliance programs increasingly intersect with data integrity expectations, and for certain analyzer configurations, quality-system standards such as ISO 13485, which creates a dual-track validation and documentation requirement for global deployments.

Competitive Landscape

The market shows moderate concentration: no single vendor surpasses a 20% revenue slice, yet the top five collectively exceed 60%, placing the sector at a middle-ground oligopoly. Thermo Fisher enlarges its portfolio via in-house innovation, exemplified by the Stellar mass spectrometer delivering 10× sensitivity gains for bioprocess omics. Agilent’s USD 925 million BIOVECTRA buy expands CDMO analytics reach, integrating small-molecule LC expertise with biologics titer quantification, thereby blurring historical product lines. Sartorius couples hardware with data analytics through BioPAT modules that slot seamlessly into its single-use ecosystem, locking customers into an end-to-end workflow.

Bruker’s acquisition of Optimal Group adds synTQ PAT knowledge-management software, enabling instrument-agnostic data unification that appeals to multi-vendor plants. Advanced Instruments merged with Nova Biomedical to build a USD 621 million revenue platform focused on cell-culture media osmolality and metabolite analyzers, signaling renewed consolidation among mid-tier specialists. Waters emphasizes chromatographic innovations such as BioResolve Protein A columns with MaxPeak surface chemistry for 7× sensitivity enhancements in antibody titer assays.

Competitive differentiation shifts toward software prowess and turnkey validation kits. Vendors race to embed machine-learning engines, remote-support sensors, and on-demand training portals. Intellectual-property filings highlight automated sampling robots and AI-based spectral deconvolution, underscoring a pivot from hardware performance to integrated workflow management. As factories digitize, supplier relationships evolve into multiyear service agreements that bundle upgrades, thereby smoothing revenue cycles and reinforcing the upward momentum of the bioprocess analyzers market.

Bioprocess Analyzers Industry Leaders

F. Hoffmann-La Roche AG

Nova Biomedical Corporation

Sartorious AG

YSI, Inc.

Kaiser Optical Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is emerging around higher-sensitivity, in-line spectroscopy and multi-attribute analysis that can shift more quality decisions upstream into the process and reduce reliance on retrospective testing. A concrete signal is the June 2026 announcement by Fujifilm and HORIBA to co-develop a high-sensitivity inline Raman measurement system for real-time monitoring of cell culture and purification processes, positioned around yield improvement versus UV-Vis methods. Programs like this reinforce demand for Raman-centered workflows already used in bioprocess monitoring, while also raising the bar for model governance, calibration transfer, and audit-ready data pipelines.

A second opportunity band involves packaging analyzers with software and digital-manufacturing layers to simplify closed-loop control adoption and enable enterprise rollouts across multi-site biomanufacturing networks, particularly among fast-scaling CMOs. Partnerships and platformization efforts that connect instruments to operations applications and use standardized data models target persistent interoperability and workforce constraints cited by manufacturers, and they align with regulatory momentum toward real-time release testing and continuous process verification. As new capacity comes online in both legacy and greenfield hubs, vendors offering validated, single-use compatible sensors alongside pre-built analytics libraries and documentation kits should be able to shorten qualification timelines and expand from point deployments to site standards.

Recent Industry Developments

- June 2026: Sartorius expanded its longstanding partnership with LFB Biomanufacturing, extending collaboration toward end-to-end cell line development across multiple modalities. The move reinforces integrated upstream-to-downstream development workflows, increasing demand for standardized PAT data capture and analyzer-compatible digital toolchains across partner networks.

- November 2025: Aber Instruments and Sartorius Stedim Biotech unveiled the BioPAT Viamass single-use biomass sensor designed for integration into Ambr 250 high-throughput bioreactors. By pushing disposable biomass measurement deeper into small-scale screening, the launch supports faster model-building and smoother scale-up, which increases pull-through for compatible analyzers and software workflows.

- May 2024: Sartorius and Sanofi collaborated to commercialize an integrated and continuous biomanufacturing (ICB) platform for downstream process intensification. This initiative points to the shift toward continuous operations where rapid, high-frequency analytics are required to maintain control and support real-time decision-making in intensified downstream steps.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers instruments, consumables, and related software used to measure and track critical parameters during bioprocess development and manufacturing, so process performance and product quality can be monitored and adjusted.

Scope exclusions: routine clinical diagnostic analyzers that are not used for bioprocess monitoring and control are excluded.

Segmentation Overview

- By Product

- Instruments

- Consumables

- Software & Analytics

- By Measurement Principle

- Raman Spectroscopy

- Near-Infrared (NIR)

- Mass Spectrometry

- Electrochemical Sensors

- By Type

- Substrate Analysis

- Metabolite Analysis

- Concentration Detection

- Physicochemical Parameter Monitoring

- By Application

- Vaccines

- Antibiotics

- Recombinant Proteins

- Biosimilars

- Other Applications

- By End-User

- Biopharmaceutical & Pharmaceutical Companies

- Contract Manufacturing/Research Organizations

- Academic & Research Institutes

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the fact base for the model and to lock the market definition before we size and forecast. We review public sources such as US FDA databases and guidance pages, European Medicines Agency product information, WHO vaccine and biologics updates, OECD science indicators, and the World Bank macro series to understand activity levels across regions.

To translate activity into likely analyzer demand, secondary information is also taken from annual reports, earnings decks, and product literature of suppliers, along with reputable press and industry association websites focused on biomanufacturing. When a cross-check is needed, paid subscriptions for company financials and news intelligence, patent databases, and shipment-level import and export records are used to confirm product launches, supply trends, and regional availability. The sources listed here are illustrative only, and additional public references were also used to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary inputs come from interviews and structured surveys with bioprocess tool suppliers, biomanufacturing operations teams, and quality and process development users, so we can validate how analyzers are selected and how frequently they are replaced or expanded. Because this is a global market, discussions were balanced across APAC, EMEA, and the Americas, then used to confirm adoption by workflow stage (process development versus commercial manufacturing) and monitoring mode (in-line, at-line, and off-line).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 48% |

| Mid tier: 47% | Functional/Unit leaders: 42% | EMEA: 33% |

| Smaller Players: 16% | Managers: 45% | Americas: 19% |

Market-Sizing & Forecasting

Market size is first reconstructed using a top-down approach where the demand pool is built from biomanufacturing activity signals, and then analyzer intensity is applied by workflow and by monitoring mode. Once that view is formed, the totals are corroborated with selective bottom-up approximations using sampled price points, channel feedback, and supplier revenue splits where disclosures are available, and then the country totals are adjusted when the checks do not line up.

In this market, key inputs include the number of active biologics and vaccine manufacturing sites by region, the pace of capacity additions, the share of single-use adoption (which shifts sensor and consumable pulls), typical calibration and replacement cycles, and pricing progression for instruments and consumables. Where data is thin for smaller countries, gaps are handled by using analog markets with similar biologics output and adjusting for import dependence and scale.

For forecasting, scenario analysis is used with a base case shaped by expert consensus from interviews, followed by sensitivity bands linked to facility ramp timing and process monitoring requirements. The model stays practical because each assumption is tied to a measurable indicator that can be refreshed without relying on internal customer systems.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including biomanufacturing capacity announcements, observable shipment patterns for relevant analyzer categories, and the timing of biologics and vaccine pipeline progress that feeds into production planning. Any sharp variance is reviewed, and assumptions are rechecked when the mismatch cannot be explained by timing effects, currency conversion, or definitional differences.

Before sign-off, the model goes through multiple analyst reviews where outliers are challenged and calculations are verified at the country and regional level before rolling up to the global total. The report is refreshed annually, and interim updates are triggered when material events occur, such as major approvals, large facility ramps, or supply constraints that change near-term purchasing behavior. Right before delivery, a final pass is completed so clients receive the latest updated view available to us.

Mordor Intelligence's Bioprocess Analyzers Market Size Compared With Other Published Estimates

Published market sizes for bioprocess analyzers can diverge even when they look similar at first glance, because the included items, base-year choices, and growth inputs are not always aligned. The differences usually show up around what is counted as part of bioprocess monitoring, and how fast recurring demand is expected to scale.

The main gap comes from whether recurring consumables and software tied to process monitoring are counted together with analyzer hardware, where Mordor Intelligence includes these only when they are used for bioprocess measurement and then anchors growth to capacity additions and replacement cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.32 B (2025) | |

| Global Consultancy A | USD 2.33 B (2025) | Uses a similar global scope year, but growth is moderated by assuming slower shifts toward in-line monitoring and longer refresh cycles for installed analyzer systems. |

| Industry Publisher B | USD 2.88 B (2025) | Appears to apply broader inclusion of adjacent process analytics and higher attach rates per manufacturing site, which can lift the 2025 level even if the long-term direction is similar. |

Overall, the table shows that scope around consumables, software tie-ins, and what is treated as adjacent analytics explains most of the spread, followed by different assumptions on adoption speed and price movement. With the model linked to site counts, monitoring intensity, and replacement behavior, the output remains traceable and can be rechecked as new capacity comes online.

Key Questions Answered in the Report

What is the current bioprocess analyzers market size?

The bioprocess analyzers market size reached USD 2.68 billion in 2026 and is projected to climb to USD 5.51 billion by 2031.

What CAGR is expected for the bioprocess analyzers market through 2031?

The market is forecast to grow at a robust 15.54% CAGR from 2026 to 2031.

Which product segment leads the bioprocess analyzers market?

Instruments dominate, accounting for 57.93% of 2025 revenue, though software and analytics are the fastest-growing category.

Which region is growing fastest in the bioprocess analyzers market?

Asia-Pacific is expected to post a 16.23% CAGR through 2031, outpacing all other regions.

Why are biosimilars important for future demand?

Biosimilars require intricate analytical proof of similarity, pushing demand for high-resolution, multi-attribute analyzers and driving an 18.63% CAGR in this application segment.

How are contract manufacturers influencing market dynamics?

Contract manufacturing organizations are scaling capacity rapidly, adopting standardized analytical platforms at an 18.31% CAGR, and thereby expanding the customer base for instrument and software vendors.

Page last updated on: