Bacterial and Viral Specimen Collection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

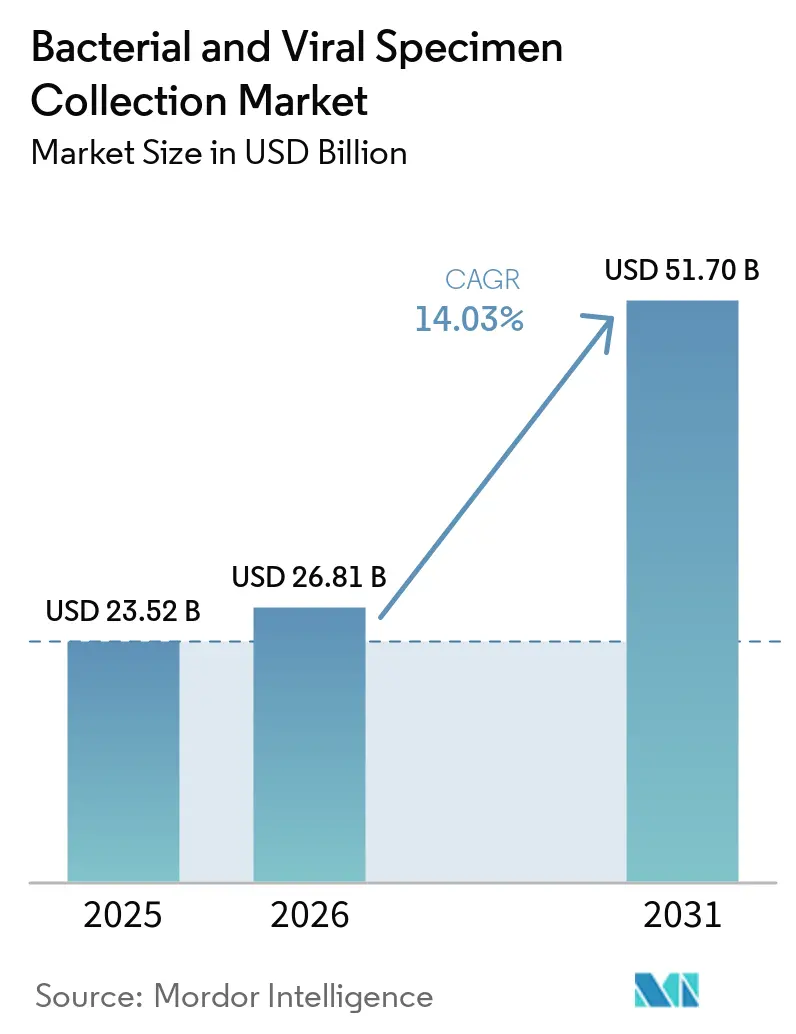

| Market Size (2026) | USD 26.81 Billion |

| Market Size (2031) | USD 51.70 Billion |

| Growth Rate (2026 - 2031) | 14.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

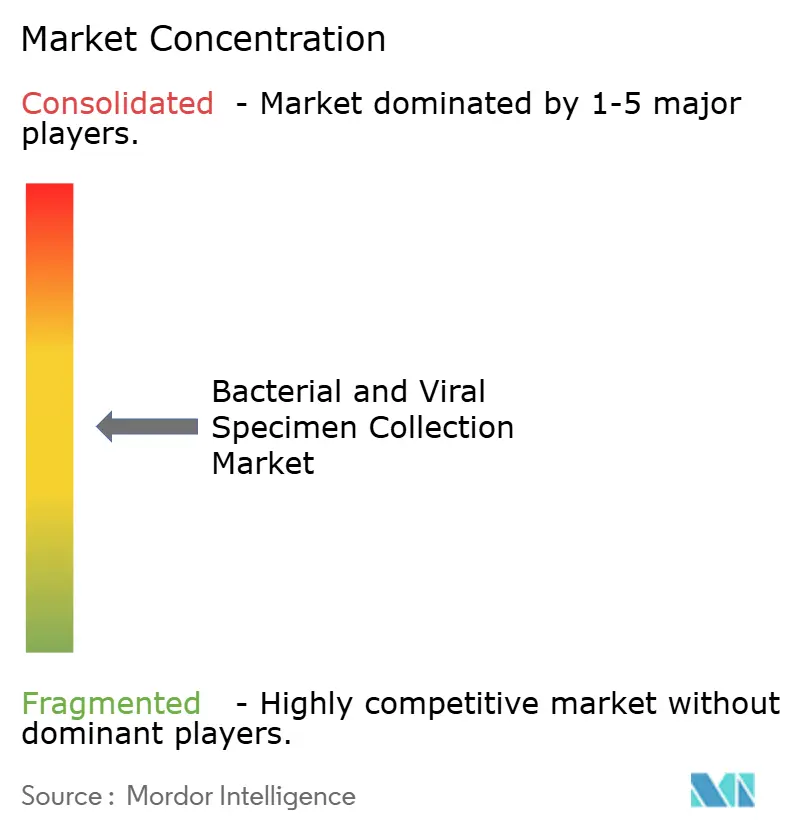

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bacterial and Viral Specimen Collection Market Analysis by Mordor Intelligence

The Bacterial And Viral Specimen Collection Market size was valued at USD 23.52 billion in 2025 and is estimated to grow from USD 26.81 billion in 2026 to reach USD 51.70 billion by 2031, at a CAGR of 14.03% during the forecast period (2026-2031).

The bacterial and viral specimen collection market is experiencing growth due to the rising adoption of molecular diagnostics, where collection quality significantly impacts test reliability. The market is further supported by global antimicrobial resistance surveillance programs that require routine and standardized bacteriological sampling across hospitals, laboratories, and public health networks. Decentralized and self-administered testing is driving additional demand, with ambient-stable formats and user-friendly kit designs enabling expansion beyond traditional clinical settings. Regulatory pressures on specimen integrity and transport are encouraging healthcare systems to replace outdated consumables with validated alternatives, fostering repeat purchases in the market.

Key Report Takeaways

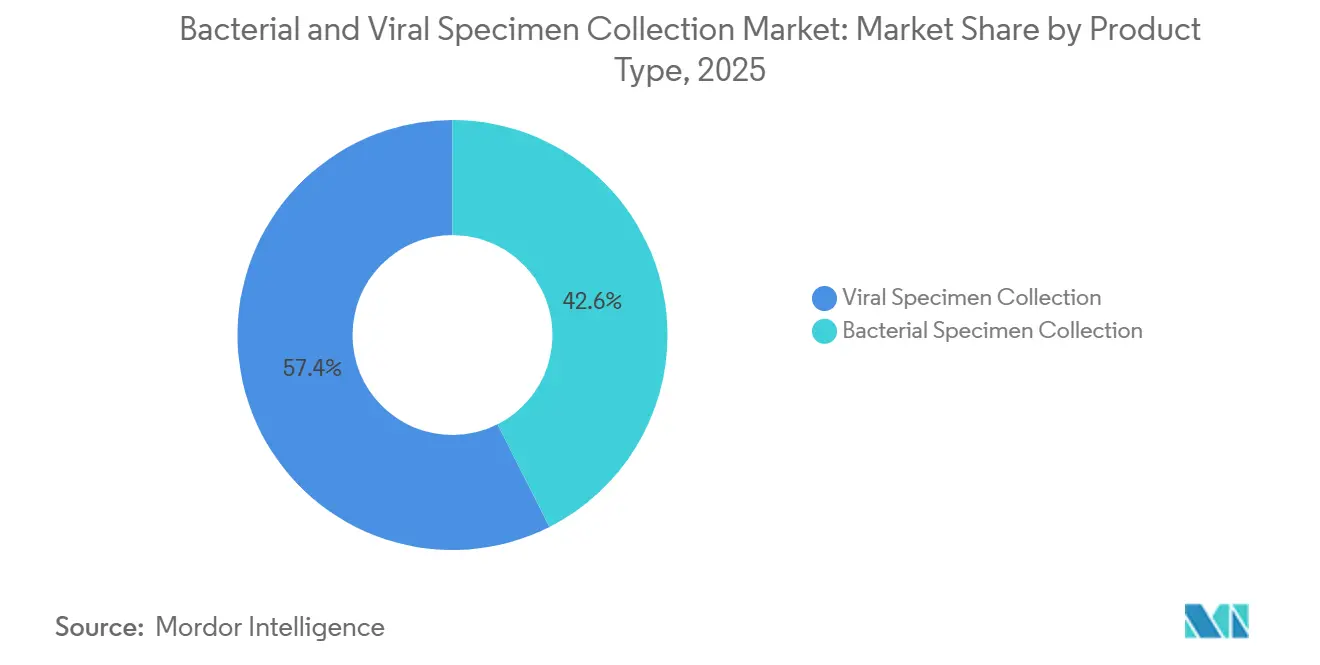

- By product type, viral specimen collection held 57.45% of revenue in 2025, while bacterial specimen collection is projected to record the highest CAGR at 15.99% through 2031.

- By specimen type, respiratory specimens accounted for 42.35% of revenue in 2025, while saliva specimens are forecast to expand at a 17.95% CAGR through 2031.

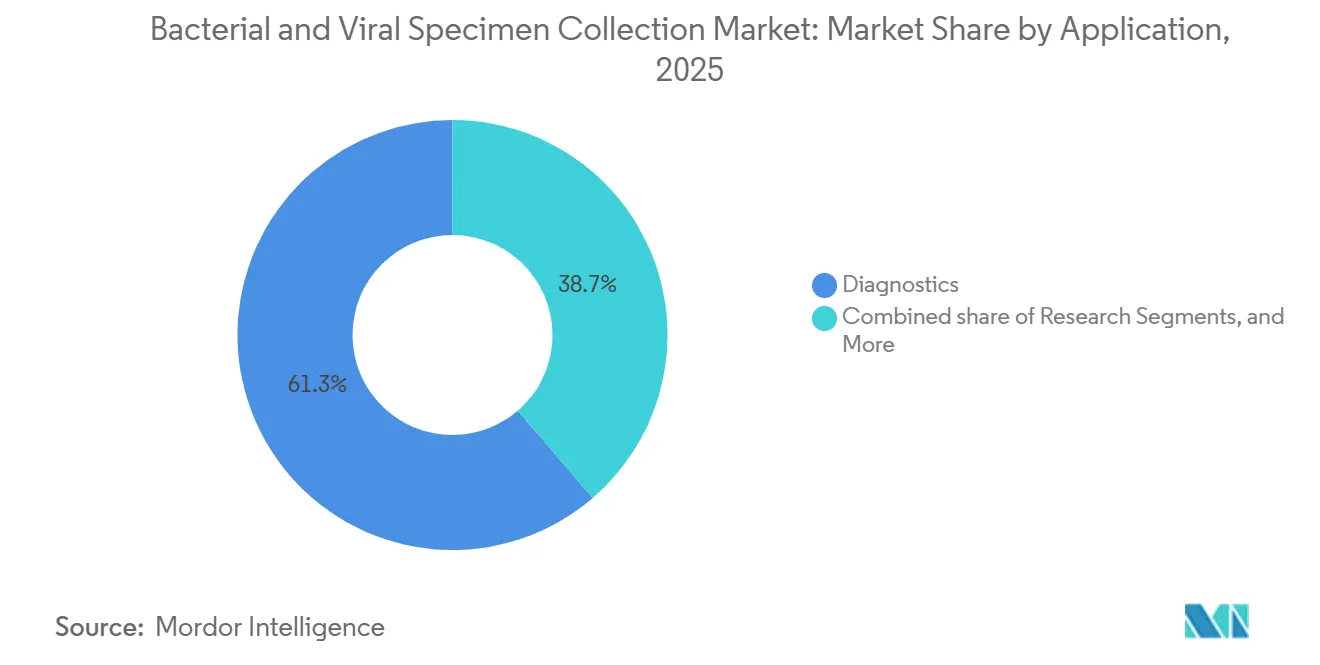

- By application, diagnostics captured 61.27% of revenue in 2025, while research is projected to grow at a 16.55% CAGR through 2031.

- By end user, hospitals and clinics held 39.76% of revenue in 2025, while diagnostic laboratories are projected to advance at a 15.45% CAGR through 2031.

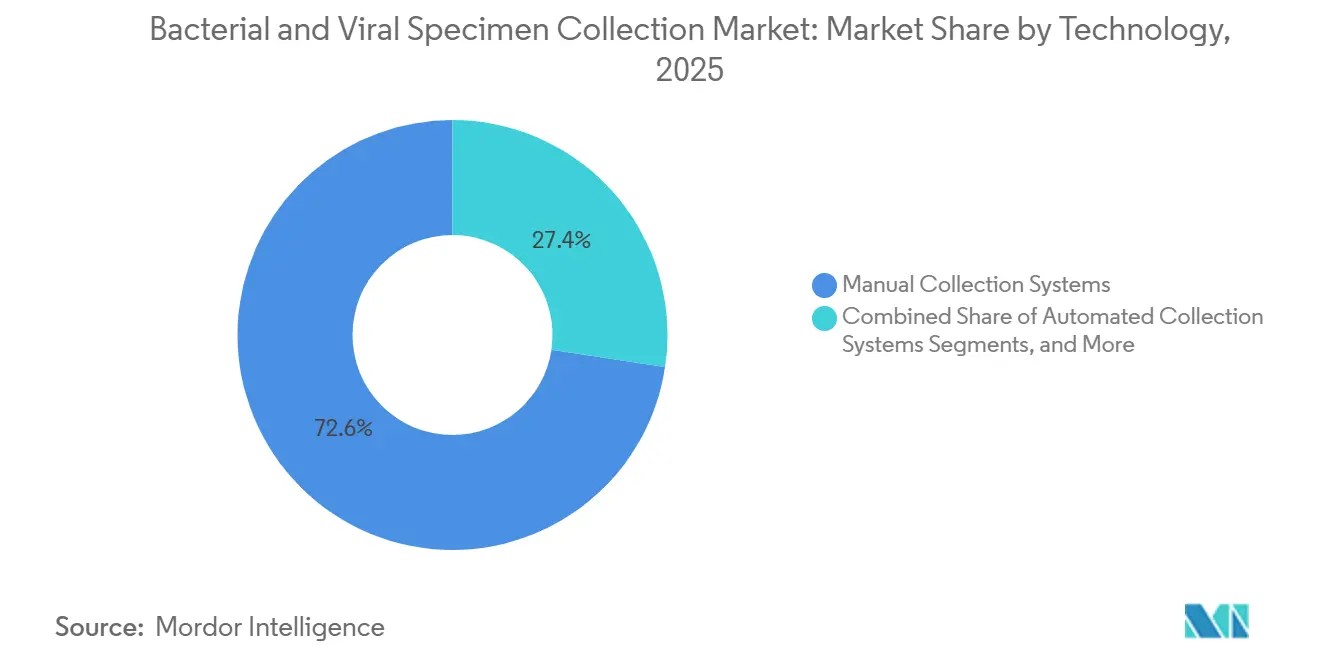

- By technology, manual collection systems accounted for 72.65% of revenue in 2025, while automated collection systems are projected to grow at a 17.66% CAGR through 2031.

- By geography, North America represented 42.55% of revenue in 2025, while Asia-Pacific is forecast to expand at a 16.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bacterial and Viral Specimen Collection Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising infectious disease testing volume | +3.5% | Global, with concentrated effect in Sub-Saharan Africa, South Asia, and Southeast Asia | Long term (≥ 4 years) |

| Expanding molecular diagnostics and PCR adoption | +2.8% | North America and Europe core, with spillover to Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Stringent specimen integrity and transport standards | +1.2% | Global, strongest in North America and the European Union | Short term (≤ 2 years) |

| Decentralized testing, home collection, and DTC sampling | +2.0% | North America and Europe, with early adoption in urban Asia-Pacific markets | Medium term (2-4 years) |

| Ambient-stable transport media adoption in remote and low-cost settings | +1.6% | Sub-Saharan Africa, South Asia, and Latin America | Long term (≥ 4 years) |

| Sustainability pressure on plastic-intensive single-use collection devices | +0.7% | European Union and North America, with emerging relevance in Australia and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Infectious Disease Testing Volume Sustains Structural Demand

The market for bacterial and viral specimen collection is thriving, driven by an uptick in testing for infectious diseases. This surge spans respiratory pathogens, bloodstream infections, and extensive surveillance initiatives. Routine care sees elevated specimen volumes due to endemic respiratory infections. Meanwhile, heightened demand for standardized bacterial collection arises from bacteremia surveillance and antimicrobial resistance programs. As national surveillance frameworks become more structured, there's a noticeable shift in procurement: a move towards certified kits, distancing from generic low-cost products. This shift is significant; once protocols for collection are standardized, replacements tend to adhere to these approved formats rather than being subject to discretionary purchases.

Expanding Molecular Diagnostics And PCR Adoption Elevates Collection Standards

The market for bacterial and viral specimen collection is on the rise, propelled by the adoption of RT-PCR, multiplex PCR, and next-generation sequencing in clinical labs. These advanced platforms necessitate stringent control over pre-analytical variables. As a result, factors like swab material, transport media composition, and storage conditions have gained prominence compared to older testing methodologies. This evolution amplifies the value of molecularly compatible collection products, diminishing the relevance of basic commodity formats in sophisticated labs. Furthermore, it bolsters suppliers capable of validating the entire workflow, from collection to assay performance. BD expanded its BD MAX System menu in December 2025 with IVDR-certified VIASURE assays through its collaboration with Certest Biotec.

Decentralized Testing, Home Collection, And DTC Sampling Reshape Collection Economics

The bacterial and viral specimen collection market is evolving as testing shifts away from hospitals and central clinics. Direct-to-consumer kits, employer screening programs, and telehealth-linked sampling are driving demand for user-friendly collection formats. These products require clear instructions, tamper-evident packaging, and reliable transport performance, increasing their commercial value. Saliva collection is gaining traction due to its convenience for home use and compatibility with non-invasive procedures. BD submitted its at-home Onclarity HPV assay to the FDA in July 2025, featuring a fiber self-collection swab designed for room-temperature mailing. The market is expanding through new channels rather than relying solely on traditional care pathways.

Ambient-Stable Transport Media Adoption Expands Market Access In Resource-Limited Settings

The bacterial and viral specimen collection market is expanding its reach in regions previously constrained by cold-chain requirements. Traditional transport media pose challenges in low-resource areas where refrigeration is limited. Ambient-stable media address these issues, enabling testing in community clinics and remote locations. This is critical for public health surveillance systems requiring consistency across large geographic areas. Simplified transport logistics allow collection programs to scale efficiently, overcoming previous bottlenecks. The market is benefiting from this shift, increasing participation in routine infectious disease and surveillance testing across diverse settings.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price sensitivity in commodity swabs and transport media | -1.5% | Global, most acute in North America and Europe where group purchasing leverage is strongest | Short term (≤ 2 years) |

| Regulatory burden for validation, shelf-life, and compatibility testing | -1.0% | Europe and North America, with spillover through quality and compliance frameworks | Medium term (2-4 years) |

| Supply risk for synthetic fibers, polymers, and reagent inputs | -0.8% | Global, with higher exposure in import-dependent Asia-Pacific markets | Medium term (2-4 years) |

| Limited reimbursement for non-hospital specimen collection points | -0.6% | North America and Western Europe, especially for community and at-home collection | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity In Commodity Swabs And Transport Media Compresses Margins

The bacterial and viral specimen collection market faces significant pricing pressure in its commodity segment. Standard swabs and traditional transport media are often procured through large tenders, favoring suppliers with scale or low-cost manufacturing. Group purchasing organizations in North America and Europe play a key role in driving down prices for routine products. This environment challenges mid-sized manufacturers to maintain margins unless they offer differentiated materials or workflows. In 2025, Puritan Medical Products emphasized domestic manufacturing as a stable supply option amidst tariff-related dynamics, though premium pricing continues to compete with procurement systems focused on minimizing unit costs. The market remains divided between premium validated products and a commodity tier constrained by price competition.

Regulatory Burden For Validation, Shelf-Life, And Compatibility Testing Creates Entry Barriers

Stringent validation standards in the bacterial and viral specimen collection market have slowed product rollouts. Manufacturers must ensure compatibility across collection devices, media, and analytical platforms, increasing costs and time to market. Introducing new materials or reformulated media triggers additional testing and documentation requirements. European compliance frameworks further extend certification and recertification burdens across product portfolios. Suppliers with robust regulatory infrastructures manage these challenges more effectively than smaller competitors. While higher quality standards benefit the market, they also delay the availability of improved pre-analytical products in clinical use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Viral Leadership Holds While Bacterial Demand Builds Faster

In 2025, viral specimen collection accounted for 57.45% of revenue, maintaining its central role in the market due to high routine testing volumes for respiratory viruses. Influenza, RSV, and SARS-CoV-2 testing continue to dominate across hospitals, clinics, and public health systems. Viral transport media and flocked swabs drive revenue in this segment, offering broad assay compatibility and stable specimen integrity. COPAN's UTM Universal Transport Medium remains a key product supporting respiratory testing workflows.

Bacterial specimen collection is projected to grow at a 15.99% CAGR through 2031, driven by expanding antimicrobial resistance surveillance. Demand for bacterial products is fueled by bloodstream infection testing, wound culture collection, and stewardship-linked sampling programs. COPAN's launch of LBM CABroth in May 2026 for Candida auris surveillance highlights the diversification of bacterial collection portfolios. Urine containers, culture media, and tissue collection kits also play a critical role, as bacterial testing is integral to clinical decision-making.

By Specimen Type: Respiratory Volumes Remain Largest While Saliva Gains Speed

Respiratory specimens held 42.35% of the market share in 2025, reflecting their dominance in seasonal infection testing and outbreak responses. National surveillance systems and clinical workflows rely heavily on nasopharyngeal and throat collections for diagnostics like influenza, COVID-19, and Group A Streptococcus. Continuous consumption of respiratory collection kits ensures stable demand.

Saliva specimens are expected to grow at a 17.95% CAGR through 2031, driven by non-invasive testing preferences, ease of self-collection, and the rise of direct-to-consumer and remote research programs. Salimetrics' launch of Participant Sampling Packs in October 2025 supports remote collection and sample integrity. Blood specimens remain vital for research, while stool, wound, and tissue samples cater to specialized testing niches.

By Application: Diagnostics Supports Scale While Research Adds Premium Growth

Diagnostics accounted for 61.27% of revenue in 2025, making it the largest application in the market. Clinical testing generates recurring demand, with hospitals, clinics, and laboratories relying on collection products for infectious disease workups. Multiplex panels requiring multiple specimen types further intensify demand, ensuring diagnostics remain the primary revenue driver.

Research is forecast to grow at a 16.55% CAGR through 2031, driven by biobanking, multi-omic studies, and translational infectious disease research. Tasso's next-generation dried blood spot collection system, launched in February 2025, reflects innovation in remote clinical trial blood collection. Smaller applications like occupational health and food safety testing contribute incremental volume as PCR-based microbial detection expands.

By End User: Hospitals Hold Scale While Diagnostic Laboratories Post Faster Expansion

Hospitals and clinics held 39.76% of revenue in 2025, maintaining their lead as primary sites for inpatient infectious disease workups, surgical site monitoring, and emergency testing. Many specimens are collected at the point of care before being routed to laboratories, anchoring the market in hospital-based collection activity.

Diagnostic laboratories are projected to grow at a 15.45% CAGR through 2031, driven by reference lab consolidation, higher testing throughput, and automation. COPAN's UriVerse, launched in August 2025, aligns with high-volume laboratory workflows. Academic and research institutions, CROs, and public health agencies are also growing due to decentralized trials and surveillance programs.

By Technology: Manual Systems Lead Today While Automation Gains Ground

Manual collection systems accounted for 72.65% of revenue in 2025, reflecting their widespread use in clinics, community health centers, and field settings. These systems remain relevant due to their accessibility, simplicity, and low upfront costs, alongside performance factors like swab materials and transport compatibility.

Automated collection systems are expected to grow at a 17.66% CAGR through 2031, as laboratories adopt them to reduce errors, improve throughput, and address staffing challenges. COPAN's PhenoMATRIX, cleared by the FDA in February 2026, exemplifies the integration of automation and image analysis into specimen workflows. Digital tracking tools are also gaining importance for reliable specimen management in distributed networks.

Geography Analysis

In 2025, North America accounted for 42.55% of the revenue in the bacterial and viral specimen collection market, driven by its extensive reference laboratory network and consistent investments in preparedness. The region's strong molecular diagnostics base boosts demand for validated collection methods and integrated workflows. The United States leads as a major testing market and an early adopter of home and decentralized collection models. BD's FDA submission for its at-home Onclarity HPV self-collection method and Puritan's PurSafe Plus launch in 2025 highlight North America's influence on room-temperature and non-clinical specimen logistics. Canada supports this growth through province-led public laboratory systems moving toward standardized and automated pre-analytical handling.

Europe remains a key region in the bacterial and viral specimen collection market, with certification requirements shaping portfolio diversity and supplier strategies. Full IVDR enforcement has increased recertification challenges for swabs, transport media, and specimen kits, favoring manufacturers with strong compliance capabilities. Germany and the UK are significant markets due to their public health surveillance and hospital microbiology networks requiring standardized collection protocols. BD's expansion of its BD MAX system with IVDR-certified VIASURE assays in 2025 reflects Europe's push for alignment between assay systems and collection tools.

Asia-Pacific is projected to grow at a 16.26% CAGR through 2031, making it the fastest-growing region in the bacterial and viral specimen collection market. Growth is driven by China's hospital laboratory expansion, India's infectious disease surveillance, and South Korea's molecular diagnostics manufacturing base. Japan and Australia contribute with high testing intensity and early adoption of automation-compatible formats. South America is advancing through Brazil and Argentina, where public laboratory networks and private diagnostic chains are adopting standardized kit procurement.

Competitive Landscape

The bacterial and viral specimen collection market is moderately consolidated, with a small group of global platform suppliers holding strong positions alongside a long list of regional and niche manufacturers. Competitive strength is increasingly tied to the ability to connect collection products with transport media, automation, software, and diagnostic platforms rather than selling swabs or containers as standalone items. This gives larger suppliers an advantage because laboratories prefer validated workflows that reduce operational risk and simplify procurement. The bacterial and viral specimen collection market therefore shows meaningful concentration at the platform level, even though local and specialized suppliers still remain active across many product categories.

In July 2025, BD announced a USD 17.5 billion Reverse Morris Trust transaction combining its Biosciences and Diagnostic Solutions business with Waters Corporation. This move highlighted the growing alignment between specimen management and diagnostics as interconnected domains rather than separate procurement areas. COPAN has strengthened its automation capabilities with UriVerse in 2025 and FDA-cleared PhenoMATRIX in 2026, enhancing its role in high-throughput microbiology workflows. Puritan Medical Products has focused on expanding liquid media transport and domestic manufacturing to address procurement volatility and pricing pressures. The competitive landscape indicates that scale alone is no longer sufficient, as workflow relevance is becoming equally critical alongside manufacturing capacity.

White space remains in the bacterial and viral specimen collection market, particularly in ambient-stable bacterial transport media, multi-analyte saliva collection formats, and cost-effective automation for mid-volume laboratories. Regional specialists such as Greiner Bio-One International GmbH, Hardy Diagnostics, and Medical Wire and Equipment Co. Ltd. remain competitive by leveraging customization, material diversity, and local distribution access. The industry is safeguarded by quality and certification barriers, with ISO-aligned systems and regulatory documentation creating entry challenges for new participants. These factors maintain active competition while enabling incumbents to defend their positions once their products are integrated into laboratory workflows.

Bacterial and Viral Specimen Collection Industry Leaders

Becton, Dickinson and Company

Thermo Fisher Scientific Inc.

QuidelOrtho Corporation

COPAN Diagnostics Inc.

Hardy Diagnostics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: COPAN Diagnostics launched LBM CABroth, a selective enrichment broth for Candida auris surveillance, expanding its bacterial collection portfolio to fungal-bacterial co-infection workflows in response to WHO's critical priority pathogen designation.

- April 2026: Bruker Corporation introduced MyGenius PRO, a fully automated molecular diagnostics system that enhances throughput for infectious disease labs by automating workflows across various sample types.

- March 2026: BABIO released an upgraded Non-Inactivated Virus Transport Kit (VTM) with CE certification, targeting global clinical diagnostics markets with optimized formulations for PCR, nucleic acid extraction, and virus isolation workflows.

- February 2026: COPAN Diagnostics received FDA 510(k) clearance for PhenoMATRIX, an AI-assisted microbial colony image assessment system integrated into the WASPLab platform, advancing digital microbiology capabilities in clinical labs.

- December 2025: BD and Certest Biotec expanded the BD MAX System menu with IVDR-certified VIASURE assays for automated molecular detection of respiratory pathogens and STIs in European markets, reinforcing ecosystem integration strategies.

Global Bacterial and Viral Specimen Collection Market Report Scope

As per the scope of the report, bacterial and viral specimen collection is the process of safely gathering biological samples such as nasal swabs, blood, or saliva to detect infectious germs. Proper methods and sterile equipment are vital. They prevent contamination and ensure test accuracy.

The bacterial and viral specimen collection market is segmented by product type, specimen type, application, end-user, technology, and geography. By product type, the market includes bacterial specimen collection (swabs, transport media, blood collection kits, culture plates and media, biopsy and tissue collection kits, urine collection containers, and other specialized bacterial collection devices) and viral specimen collection (viral transport media, swabs, blood collection tubes, saliva collection kits, sputum collection containers, stool collection kits, and other specialized viral collection devices). By specimen type, the market is categorized into respiratory specimens, blood specimens, urine specimens, wound and tissue specimens, saliva specimens, stool specimens, and other specimen types. By application, the market is segmented into diagnostics, research, and others. By end-user, the market includes hospitals and clinics, diagnostic laboratories, academic and research institutions, clinical research organizations, and others. By technology, the market is segmented into manual collection systems, automated collection systems, and digital sample tracking and traceability. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Bacterial Specimen Collection | Swabs |

| Transport Media | |

| Blood Collection Kits | |

| Culture Plates and Media | |

| Biopsy and Tissue Collection Kits | |

| Urine Collection Containers | |

| Other Specialized Bacterial Collection Devices | |

| Viral Specimen Collection | Viral Transport Media |

| Swabs | |

| Blood Collection Tubes | |

| Saliva Collection Kits | |

| Sputum Collection Containers | |

| Stool Collection Kits | |

| Other Specialized Viral Collection Devices |

| Respiratory Specimens |

| Blood Specimens |

| Urine Specimens |

| Wound and Tissue Specimens |

| Saliva Specimens |

| Stool Specimens |

| Other Specimen Types |

| Diagnostics |

| Research |

| Others |

| Hospitals and Clinics |

| Diagnostic Laboratories |

| Academic and Research Institutions |

| Clinical Research Organizations |

| Others |

| Manual Collection Systems |

| Automated Collection Systems |

| Digital Sample Tracking And Traceability |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Bacterial Specimen Collection | Swabs |

| Transport Media | ||

| Blood Collection Kits | ||

| Culture Plates and Media | ||

| Biopsy and Tissue Collection Kits | ||

| Urine Collection Containers | ||

| Other Specialized Bacterial Collection Devices | ||

| Viral Specimen Collection | Viral Transport Media | |

| Swabs | ||

| Blood Collection Tubes | ||

| Saliva Collection Kits | ||

| Sputum Collection Containers | ||

| Stool Collection Kits | ||

| Other Specialized Viral Collection Devices | ||

| By Specimen Type | Respiratory Specimens | |

| Blood Specimens | ||

| Urine Specimens | ||

| Wound and Tissue Specimens | ||

| Saliva Specimens | ||

| Stool Specimens | ||

| Other Specimen Types | ||

| By Application | Diagnostics | |

| Research | ||

| Others | ||

| By End User | Hospitals and Clinics | |

| Diagnostic Laboratories | ||

| Academic and Research Institutions | ||

| Clinical Research Organizations | ||

| Others | ||

| By Technology | Manual Collection Systems | |

| Automated Collection Systems | ||

| Digital Sample Tracking And Traceability | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the bacterial and viral specimen collection market by 2031?

The bacterial and viral specimen collection market is forecast to reach USD 51.70 billion by 2031 from USD 26.81 billion in 2026, growing at a 14.03% CAGR.

Which product category leads revenue in bacterial and viral specimen collection?

Viral specimen collection led revenue with a 57.45% share in 2025 because respiratory virus testing still drives the largest routine specimen volume.

Which specimen type is growing the fastest through 2031?

Saliva specimens are projected to record the fastest growth at a 17.95% CAGR through 2031, supported by non-invasive and self-collection use cases.

Why are diagnostic laboratories becoming more important in this field?

Diagnostic laboratories are forecast to grow at a 15.45% CAGR because testing volumes are consolidating into high-throughput reference lab models with stronger automation economics.

Which region is expanding the fastest in bacterial and viral specimen collection?

Asia-Pacific is the fastest-growing region with a 16.26% CAGR through 2031, supported by laboratory expansion and infectious disease surveillance investment.

What is driving demand for automated collection systems?

Automated collection systems are projected to grow at a 17.66% CAGR because laboratories want fewer pre-analytical errors, better throughput, and less dependence on manual handling.

Page last updated on: