Australia Dark Fiber Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

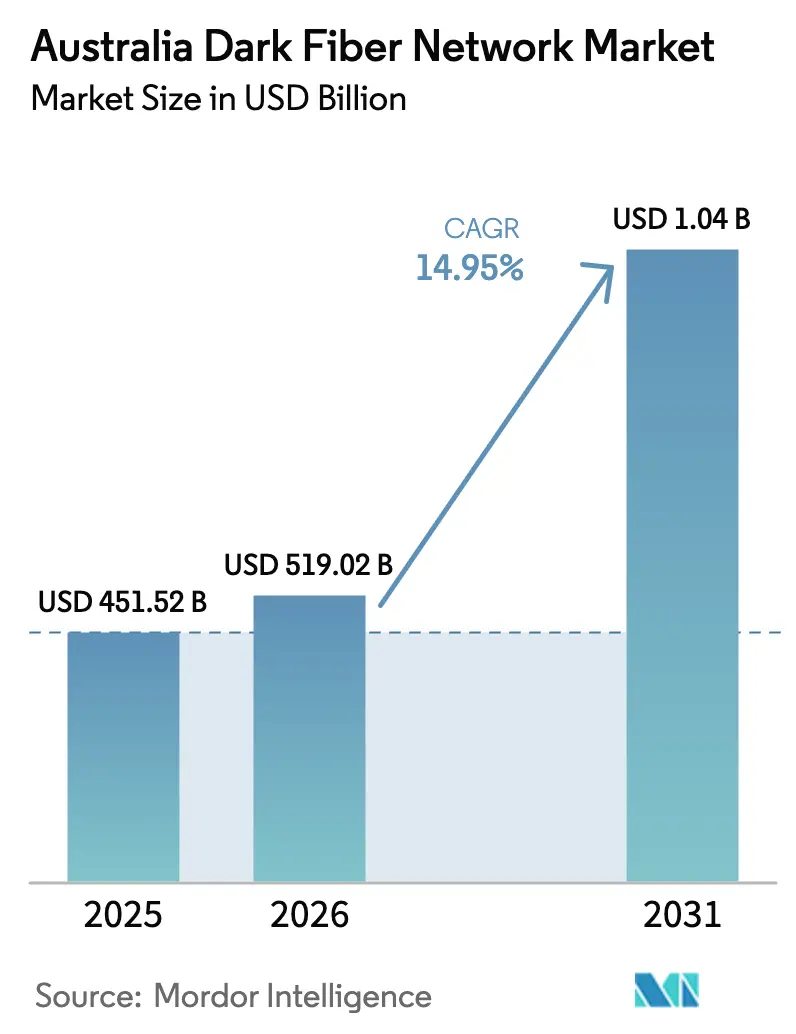

| Base Year Market Size (2025) | USD 451.52 Million |

| Market Size (2026) | USD 519.02 Million |

| Market Size (2031) | USD 1041.67 Million |

| Growth Rate (2026 - 2031) | 14.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Dark Fiber Network Market Analysis by Mordor Intelligence

The Australia Dark Fiber Network market size is expected to grow from USD 451.52 million in 2025 to USD 519.02 million in 2026 and is forecast to reach USD 1,041.67 million by 2031 at 14.95% CAGR over 2026-2031. Rising hyperscale cloud deployments, a multi-billion-dollar federal fiber upgrade program, and surging 5G backhaul requirements position the Australian dark fiber network market for sustained double-digit expansion. Strategic consolidation, highlighted by Vocus’s acquisition of TPG Telecom’s fixed and fiber assets, is creating large-scale operators that can fund long-haul builds and metro densification.[1]ChannelNews, “Vocus Acquires TPG Telecom’s Fixed and Fibre Assets for $5.25 Billion,” channelnews.com.au Simultaneously, government equity injections into NBN Co and regional connectivity grants reduce last-mile risk, enabling providers to enter difficult, low-density corridors. Capacity-hungry industries, such as manufacturing and healthcare, are migrating toward private fiber pairs for sovereignty and latency reasons, while renewable-energy zone build-outs are opening up entirely new rights-of-way that favor single-mode deployment. Competitive pressure from wholesale DWDM services continues to curb price escalation, but resilient route diversity and service-level guarantees enable operators to maintain margins in premium corridors.

Key Report Takeaways

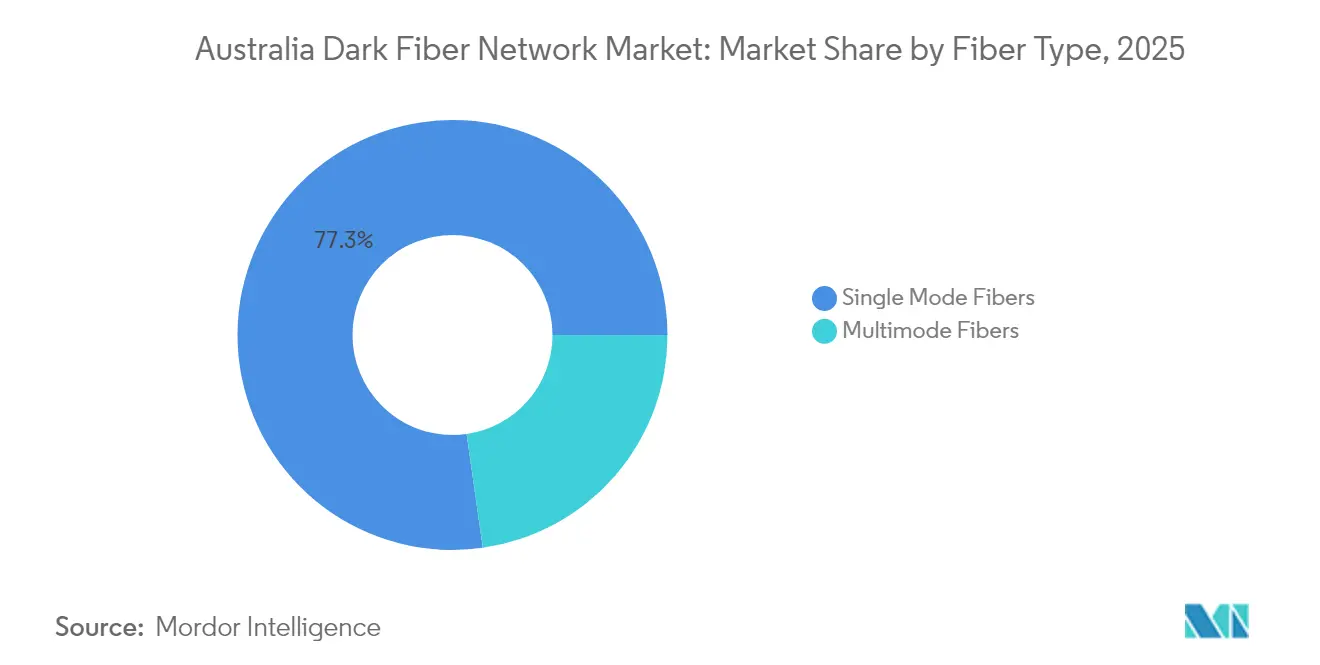

- By fiber type, single-mode captured 77.25% of Australia's dark fiber network market share in 2025; the segment is forecast to post a 15.95% CAGR through 2031.

- By network type, metro routes led with 61.15% revenue share of the Australian dark fiber network market in 2025, while long-haul networks are expected to expand at a 16.15% CAGR to 2031.

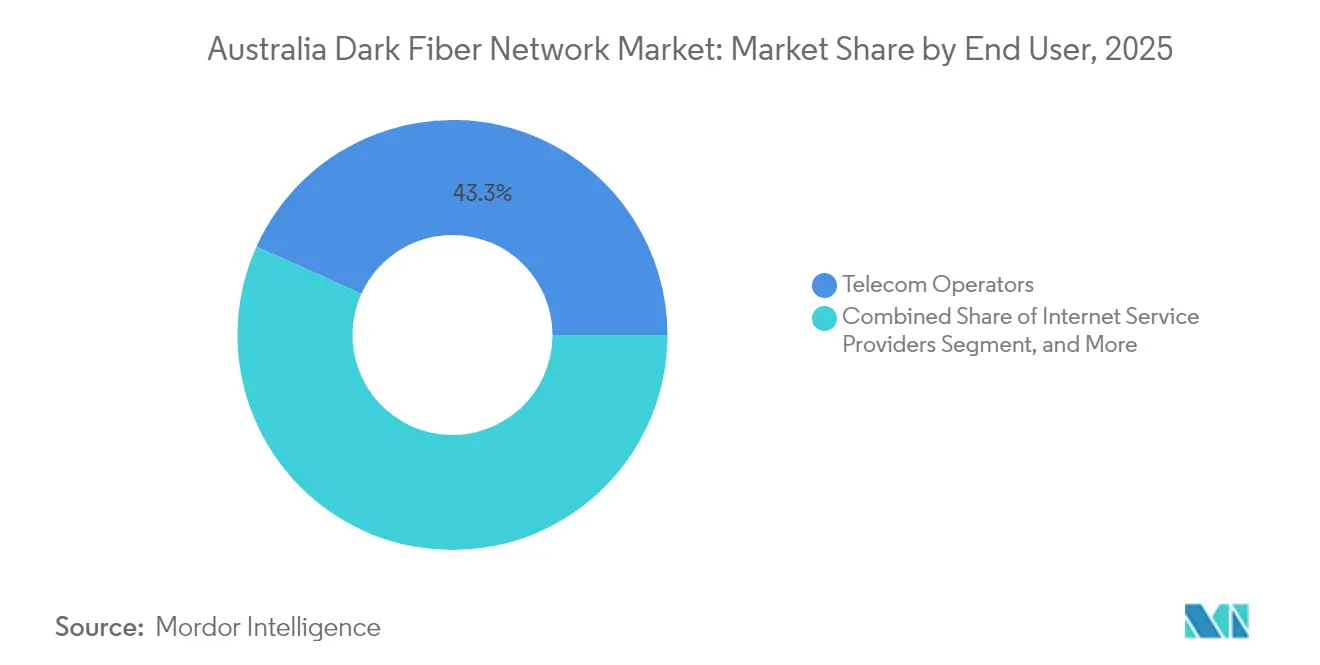

- By end user, telecom operators accounted for 43.25% of the Australian dark fiber network market size in 2025; enterprises and data centers represent the fastest-growing segment, with a 17.05% CAGR through 2031.

- By industry vertical, IT and telecom held 38.55% of the Australian dark fiber network market size in 2025, whereas the manufacturing sector is projected to advance at a 17.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Dark Fiber Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Data Center Expansion in Sydney and Melbourne | +2.8% | New South Wales and Victoria, spillover to Queensland | Medium term (2-4 years) |

| Surging 5G Backhaul Capacity Requirements | +2.5% | National, concentrated in metropolitan areas | Short term (≤ 2 years) |

| Government's National Fibre Initiative and Regional Connectivity Funding | +2.2% | National, prioritizing regional and remote areas | Long term (≥ 4 years) |

| Rising Demand from Hyperscale Cloud Providers for Dark Fiber IRUs | +2.1% | Sydney, Melbourne, Perth data center hubs | Medium term (2-4 years) |

| Submarine Cable Landing Diversity Driving Terrestrial Dark Fiber Buildouts | +1.9% | Coastal regions, particularly NSW, WA, QLD | Long term (≥ 4 years) |

| Emergence of Renewable Energy Zones Requiring High Bandwidth Connectivity | +1.8% | NSW, Victoria, Queensland renewable corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Data Center Expansion in Sydney and Melbourne

Hyperscale operators continue to expand their campus footprints in both cities, with NextDC’s S7 expansion and Equinix’s multi-site investment solidifying Sydney and Melbourne as Australia’s highest-density interconnection corridors.[2]NextDC, “S7 Sydney Data Centre Expansion,” nextdc.com New availability zones require dark fiber rings that guarantee sub-millisecond latency and triple-path resilience, driving sustained demand for route diversity. Competition for premium ducts linking metro facilities to submarine landings inflates lease rates as much as 60% above comparable Asian markets. Cloud on-ramp clustering further concentrates traffic, prompting operators to deploy high-count single-mode cables able to support wavelength upgrades beyond 400G. Financial services firms colocate trading engines near these hyperscale nodes, thereby compounding low-latency requirements and reinforcing the value proposition of dark fiber.

Surging 5G Backhaul Capacity Requirements

Optus and TPG’s shared-RAN roadmap will activate 2,444 regional 5G sites by 2030, with each site demanding 10-20× the backhaul throughput of legacy 4G equipment.[3]Optus Media Centre, “TPG Telecom and Optus Sign Network Sharing Agreement,” optus.com.au Nokia’s 83 Gbps field test on NBN Co’s live network demonstrates that existing strands can carry multi-terabit traffic; however, densification still requires new pairs in metro cores. Wholesale dark fiber enables mobile operators to avoid oversubscription risks as interactive gaming, AR, and private 5G enterprise traffic proliferate. Urban zoning delays push providers to adopt micro-trenching where allowed, reducing build times but intensifying the race for scarce conduit. Regional installations depend on government co-funding, making NBN backhaul extensions a critical enabler for rural 5G coverage.

Government’s National Fibre Initiative and Regional Connectivity Funding

The federal Better Connectivity Plan allocates USD 1.1 billion for rural backbones, including the 226-kilometer Burketown–Normanton route, which serves approximately 780,000 Queenslanders. Equity injections totaling AUD 3 billion into NBN Co accelerate fiber-to-the-premises upgrades for 622,000 locations now on copper. Public grants lower demand risk by guaranteeing anchor traffic, unlocking private capital for adjacent commercial routes. Local carriers can bid for wholesale agreements that bundle dark pairs with duct access, smoothing entry into previously unviable zones. These projects also standardize access conditions, gradually shortening approval cycles at state and council levels.

Rising Demand from Hyperscale Cloud Providers for Dark Fiber IRUs

Google, AWS, and Microsoft increasingly secure 15- to 25-year indefeasible rights of use to maintain optical-layer control and satisfy sovereignty clauses. Customizable line-systems let them push 400G+ wavelengths and implement domain-specific encryption without relying on lit-service SLAs. Long-term commitments provide operators with predictable cash flows, supporting high-capex builds through Australia’s sparsely populated interiors. Sovereign-cloud mandates in defense and regulated industries intensify preference for domestically governed infrastructure. This structural shift diverts traffic from public wholesale networks, but also spurs carriers to deploy new metro loops where cloud tenants pre-book entire cable counts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for New Fiber Deployment | -1.8% | National, particularly challenging in regional areas | Long term (≥ 4 years) |

| Delays in Local Council Approvals and Rights-of-Way | -1.5% | Metropolitan areas with complex approval processes | Medium term (2-4 years) |

| Competition from Wholesale NBN and DWDM Lit Services | -1.2% | National, concentrated where NBN has fiber coverage | Short term (≤ 2 years) |

| Bushfire Risk Increasing Maintenance Costs | -0.9% | Eastern states bushfire corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for New Fiber Deployment

Unit costs range from USD 16,250 to USD 65,000 per kilometer, with underground metro routes at the upper end due to traffic management and utility coordination fees. Telstra’s 14,000-kilometer intercity project consumed roughly USD 1.6 billion, underscoring the investment barrier that deters new entrants. Sparse populations diminish revenue per route-kilometer, extending breakeven timelines beyond a decade. Financing costs remain elevated despite low sovereign risk, as lenders demand long-term anchor contracts before releasing funds. These economics favor incumbents with sunk costs assets and limit the pace of greenfield competition outside government-backed corridors.

Delays in Local Council Approvals and Rights-of-Way

Multi-agency permits can span up to 18 months, particularly when routes cross multiple local authorities with distinct environmental and heritage requirements. Utility pole access is further complicated by power company safety reviews, often forcing carriers to redesign aerial plans into more costly underground alternatives. Regulatory inconsistency introduces schedule risk, which has discouraged several smaller ISPs from proceeding with planned metro rings during 2024. The Australian Communications and Media Authority is developing a single-window portal; however, implementation is uneven across states, resulting in project planners still including 12-month buffers in their Gantt charts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Single-Mode Dominance Drives Long-Haul Expansion

Single-mode strands accounted for 77.25% of the Australian dark fiber network market in 2025, and the segment is projected to grow at a 15.95% CAGR through 2031. This dominance reflects the technical necessity for ultra-low attenuation across Australia’s extended intercity spans. The Australian dark fiber network market size for single-mode links is poised to outpace multimode demand as coherent optics push per-strand capacity past 800G. Operators further prefer single-mode when trenching new REZ corridors because future-proof performance offsets initial capex. Multimode retains relevance inside data-center campuses where reaches stay below 300 meters, but falling transceiver prices are eroding its cost advantage.

In 2025, researchers funded by Microsoft demonstrated a hollow-core fiber with a loss of 0.091 dB/km, promising 45% faster propagation. While commercial deployment remains several years away, major carriers have begun factoring upgrade options into duct design specifications. Early pilot trials on Sydney–Melbourne financial routes could see adoption within the forecast period if latency benefits translate into trading-desk premiums. Multimode vendors respond by promoting OM5 variants, yet customer roadmaps increasingly align with single-mode’s scalability, cementing its share over the projection window.

By Network Type: Metro Leads but Long-Haul Expansion Gains Momentum

Metro deployments generated 61.15% of 2025 revenue as Sydney and Melbourne data-center clusters demand dense lateral paths for east-west resilience. The largest operators added more than 3,500 route-kilometers of urban duct in 2025 alone, underscoring the Australian dark fiber network market’s metro skew. Nevertheless, long-haul capacity needs are rising fastest, with a projected 16.15% CAGR to 2031, driven by renewable-energy and submarine-landing diversification. NBN equity funding indirectly encourages private long-haul builds by extending wholesale lateral links into regional townships, shrinking the gap between urban rings and rural access points.

Long-haul strands also support defense and sovereign cloud mandates, requiring separate inland and coastal paths. Telstra’s bushfire-hardening plan now includes deeper burial on 1,200 kilometers of the Sydney–Brisbane corridor, highlighting resiliency premiums that customers are willing to pay. Meanwhile, metro competition is tightening as lit-service entrants leverage NBN ducts, prompting established carriers to bundle dark pairs with managed wavelength add-ons to defend their share.

By End User: Enterprise Momentum Accelerates

Telecom operators held a 43.25% market share of the Australian dark fiber network in 2025, reflecting their historical control of backhaul and interconnect infrastructure. However, enterprise and data-center tenants are booking pairs at a 17.05% forecast CAGR as digital transformation drives private connectivity preferences. Transaction-intensive industries now negotiate IRUs that bundle metro loops with inter-capital extensions to guarantee deterministic latency.

The Australian dark fiber network market size, driven by enterprise uptake, increased sharply after cybersecurity mandates enhanced control over physical paths. Manufacturing plants utilize dark fiber to connect time-sensitive industrial IoT endpoints directly to cloud analytics, bypassing public IP networks. Government agencies and universities expand campus rings to support high-resolution imaging and genomics workloads, reinforcing cross-sector momentum.

By Industry Vertical: Manufacturing Surge Outpaces Traditional Leaders

IT and telecom generated 38.55% of 2025 revenue, maintaining leadership through data-center interconnect and wholesale wave off-take. Manufacturing, however, is forecast to expand at an annual rate of 17.65% as Industry 4.0 adoption sweeps through food processing, metals, and advanced-materials facilities. Predictive-maintenance analytics and computer-vision inspection require deterministic 10G+ links between shop floors and edge compute clusters, fostering high-margin pair leasing.

Financial services institutions are pursuing shorter settlement windows, tightening their tolerance for jitter, and driving the uptake of dark routes parallel to the Sydney–Melbourne rail corridor. Healthcare systems scale radiology and tele-surgery bandwidth needs, while state education departments migrate virtual learning platforms to regional hubs, each incrementally expanding the Australian dark fiber network market.

Geography Analysis

New South Wales led revenue in 2025 owing to Sydney’s hyperscale campus concentration and the majority of Australia’s submarine cable landings. The Hunter–Central Coast REZ alone underpins more than USD 4.2 billion in renewable investment, each project wiring gigawatt-class installations back to metropolitan control rooms. Coupled with federal funding for rural spur lines, the state accounts for more than 40% of the current metro and long-haul route kilometers.

Victoria maintains a strong second place, supported by Melbourne’s sizable colocation ecosystem and recent additions to Perth-linked subsea systems. Vocus’s newly acquired fiber assets extend multiple diverse paths into the city, providing enterprises with flexible options for hybrid-cloud connectivity. The state government’s fiber-as-a-service initiative also lowers municipal-access costs, thereby accelerating SME uptake.

Queensland’s growth trajectory is steep as Far North communities gain backhaul through the 226-kilometer Burketown–Normanton build. Agricultural technology subsidies worth USD 30,000 per farm drive last-mile demand, while Sunshine Coast’s cable landing strengthens the coastal city’s appeal as a low-latency gateway to Asia. Western Australia leverages mining automation projects and the INDIGO landing at Perth to justify expanded inland paths toward Pilbara sites.

South Australia, Tasmania, the Northern Territory, and the Australian Capital Territory collectively form an emerging cluster. Tasmania stands out after NBN prioritized 19,000 rural premises for fiber upgrades, effectively seeding future enterprise routes into Hobart. Northern Territory’s Top End corridor adds more than 10,000 upgraded premises, creating sufficient anchor traffic to stimulate private expansion. These territories face high deployment costs and bushfire exposure, yet government grants and anchor tenancy models mitigate financial risk for operators willing to pursue targeted builds.

Competitive Landscape

Australia’s dark fiber arena exhibits moderate concentration, with Telstra, Vocus, and the pre-existing TPG backbone jointly owning more than 70% of route kilometers as of the end of 2024. However, consolidation is reshaping the distribution of shares. Vocus’s USD 3.54 billion acquisition of TPG’s fixed assets vaulted it into second place by fiber length, creating an independent challenger to Telstra’s legacy dominance. Superloop, meanwhile, strengthened its enterprise offer by purchasing Uecomm from Optus, adding 2,000 route kilometers that intersect core CBD buildings.[4]Superloop, “Completion of Uecomm Acquisition,” superloop.com

Technology leadership increasingly determines share capture. NBN Co and Nokia’s 83 Gbps trial showed incumbents can postpone fresh trenching through spectral efficiency gains, while AARNet’s successful 400G subsea test validated coherent optics for academic and research networks. Operators now bundle managed wavelengths and managed encryption on top of pair leases to compete against cheaper lit services.

Regulatory requirements surrounding critical-infrastructure security raise entry barriers, favoring carriers with ISO 27001 data center footprints and sovereign cloud certifications. Renewable-energy zones represent white-space territory where smaller specialists can carve share by aligning with transmission-network builders at project inception. Pricing competition persists in mature metro loops, but differentiated SLAs, latency guarantees, and proactive route hardening enable premium positioning in high-value corridors.

Australia Dark Fiber Network Industry Leaders

Vocus Group Limited

Telstra Corporation Limited

TPG Telecom Limited

Superloop Limited

Optus Networks Pty Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: University of Southampton researchers, backed by Microsoft, recorded a loss of 0.091 dB/km on hollow-core fiber, approximately 45% faster than traditional solid-core strands, suggesting potential commercial latency breakthroughs within five years.

- January 2025: NBN Co secured an AUD 3 billion (USD 2.03 billion) equity injection from the federal government to finish nationwide fiber-to-the-premises upgrades by 2030. The funds cover 622,000 copper-served premises and create fresh wholesale capacity that dark-fiber providers can tap for last-mile links.

- December 2024: The Regional Telecommunications Independent Review Committee published 14 recommendations aimed at improving rural connectivity; the federal response, due in early 2025, will shape the next wave of dark fiber regulation.

- October 2024: Vocus closed its AUD 5.25 billion (USD 3.54 billion) purchase of TPG Telecom’s fixed and fiber portfolio, adding more than 50,000 kilometers of terrestrial routes and about 15,000 kilometers of subsea cable. The deal positions Vocus as Telstra’s strongest infrastructure rival.

Australia Dark Fiber Network Market Report Scope

| Single Mode Fibers |

| Multimode Fibers |

| Metro Dark Fiber |

| Long-Haul Dark Fiber |

| Internet Service Providers |

| Telecom Operators |

| Enterprises and Data Centers |

| Government and Public Sector |

| IT and Telecom |

| BFSI |

| Healthcare |

| Manufacturing |

| Government and Defense |

| Other Industry Verticals |

| By Fiber Type | Single Mode Fibers |

| Multimode Fibers | |

| By Network Type | Metro Dark Fiber |

| Long-Haul Dark Fiber | |

| By End-User | Internet Service Providers |

| Telecom Operators | |

| Enterprises and Data Centers | |

| Government and Public Sector | |

| By Industry Vertical | IT and Telecom |

| BFSI | |

| Healthcare | |

| Manufacturing | |

| Government and Defense | |

| Other Industry Verticals |

Key Questions Answered in the Report

How large will Australia’s dark-fiber footprint be by 2031?

The network is forecast to reach USD 1,041.67 million in revenue by 2031, growing at a 14.95% CAGR from 2026.

Which customer group is adding pairs fastest?

Enterprises and data centers are expanding capacity at a 17.05% CAGR thanks to cloud migration and sovereignty requirements.

Why are single-mode strands favored over multimode?

Single-mode provides lower attenuation across long intercity spans and supports coherent-optic upgrades beyond 400G, making it ideal for Australia’s vast geography.

What role does government funding play?

Equity injections into NBN Co and regional connectivity grants de-risk long-haul builds, shorten payback periods, and open previously uneconomical corridors.

How is market consolidation affecting competition?

Vocus’s purchase of TPG assets and Superloop’s Uecomm deal create larger infrastructure challengers to Telstra, raising competitive intensity while expanding route diversity.

Which vertical will post the strongest growth?

Manufacturing is projected to advance at a 17.65% CAGR as Industry 4.0 deployments require deterministic, high-bandwidth private links.

Page last updated on: