Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 23.42 Billion |

| Market Size (2026) | USD 24.35 Billion |

| Market Size (2031) | USD 29.56 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Telecom MNO Market Analysis by Mordor Intelligence

The Australia Telecom MNO Market size is expected to grow from USD 23.42 billion in 2025 to USD 24.35 billion in 2026 and is forecast to reach USD 29.56 billion by 2031 at 3.96% CAGR over 2026-2031. In terms of subscriber volume, the market is expected to grow from 34.65million subscribers in 2025 to 41.42million subscribers by 2030, at a CAGR of 3.63% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 34.65million subscribers in 2025 to 41.42million subscribers by 2030, at a CAGR of 3.63% during the forecast period (2025-2030). This outlook reflects a resilient growth trajectory powered by nationwide 5G coverage gains, fiber-to-the-premises (FTTP) upgrades, and rising enterprise demand for managed ICT and cloud connectivity. At present, data services secure the largest revenue share of 47% while voice services retain 25%, underscoring the structural shift toward bandwidth-intensive applications. Competitive intensity continues to rise as TPG finalizes network-sharing with Optus, Vocus absorbs TPG’s fixed assets, and Telstra invests USD 800 million in AI-enabled network automation. Meanwhile, daily mobile traffic has climbed to 9 million GB and average monthly usage is projected to double to 28.7 GB by 2028, sustaining capacity monetization opportunities even as higher NBN wholesale charges and retail price increases squeeze household budgets.

Key Report Takeaways

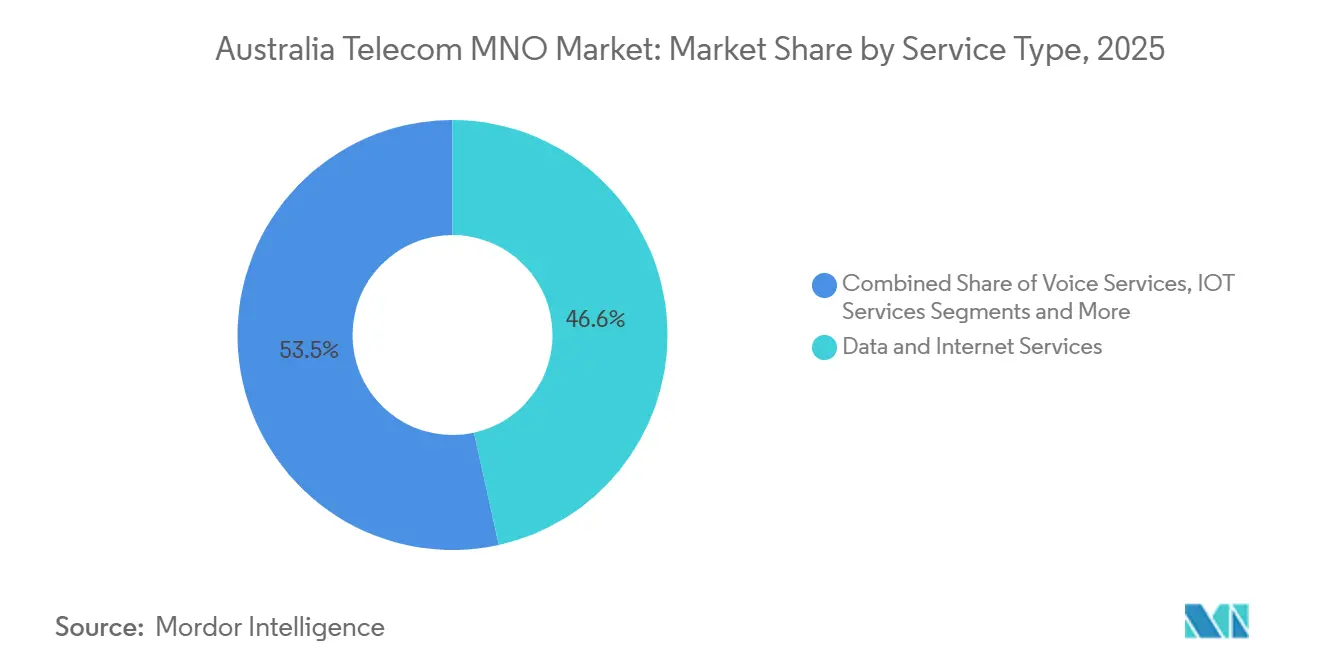

- By service type, data services captured 46.55% of Australian telecom MNO market share in 2025 and are pacing at a 3.99% CAGR through 2031.

- By end-user, the enterprise segment held 31.15% share of the Australian telecom MNO market size in 2025 and is expanding at a 4.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G coverage expansion and premium monetization | +1.2% | National, high impact in Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Fibre-to-the-premises upgrades boosting ARPU | +0.8% | National NBN footprint, priority metro areas | Long term (≥ 4 years) |

| Surging enterprise demand for managed ICT and cloud connectivity | +1.0% | National, major business centers | Short term (≤ 2 years) |

| Mobile-data growth from streaming and gaming services | +0.9% | National, higher in urban areas | Short term (≤ 2 years) |

| Direct-to-device LEO satellite partnerships for rural reach | +0.4% | Regional and remote Australia | Long term (≥ 4 years) |

| Private 5G networks adoption in mining and heavy industry | +0.3% | Western Australia, Queensland mines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Coverage Expansion Driving Premium Service Monetization

Australia’s 5G rollout has passed the early-adopter phase and is now the primary engine of revenue uplift. Telstra reaches 91% population coverage and Optus exceeds 80%, underpinned by a USD 800 million multiyear capex plan that embeds Ericsson’s AI-based network management to unlock differentiated speed tiers. Customers migrating to premium 5G plans lifted mobile service revenue 3.7% year-over-year in 2024, counterbalancing price fatigue in lower tiers. Enterprise interest is likewise robust: Newmont’s Cadia mine reported 80% improvement in underground communications after pilot 5G deployment, validating advanced use cases in autonomous haulage. Spectrum availability in the 26 GHz and 28 GHz bands, allocated under ACMA’s apparatus licensing framework, further accelerates metropolitan small-cell densification.[1]Australian Communications and Media Authority, “26 GHz and 28 GHz Bands,” acma.gov.au

FTTP Network Upgrades Accelerating ARPU Recovery

The federal government’s USD 3 billion infusion and NBN Co’s USD 800 million co-investment will upgrade 622,000 premises to gigabit capability by 2030, lifting the share of ultrafast connections to 94% of households. Average household data consumption has risen ten-fold in the past decade, and gigabit tiers position service providers to reclaim ARPU lost to discount plans. NBN Co projects a USD 10.4 billion GDP contribution from productivity gains linked to FTTP, yet annual wholesale increases aligned to CPI—4.1% for FY25—continue to squeeze retailer margins.[2]Australian Financial Review, “Labor Invests USD 3 Billion in NBN,” afr.com Operators are mitigating cost pressure by nudging customers to NBN 100 and NBN 250 plans, where usage-based overage fees and bundling create incremental margin headroom.

Enterprise ICT Demand Fueling Managed Services Growth

Enterprise outlays on secure connectivity, private cloud on-ramps, and managed services are rising faster than consumer spend. Optus signed a seven-year USD 1.6 billion deal with Suncorp that spans voice, contact center, and data networks, signalling confidence in long-term contract economics. The enterprise segment’s 4.35% CAGR eclipses consumer expansion due to higher ARPU, network-level service-level agreements, and cybersecurity certifications such as ISO-27001 that tilt demand toward Tier-1 carriers. Consolidation is reshaping supply: Vocus’ USD 5.25 billion acquisition of TPG’s wholesale and government arm brings 50,000 km of fiber under a single challenger brand, strengthening buyer choice in data-center interconnect and dark-fiber leasing. Telstra’s Cloud Connector platform reports double-digit client growth as enterprises bypass public internet to reach Microsoft Azure and AWS with deterministic latency.

Mobile Data Surge from Streaming and Gaming Applications

Mobile traffic keeps setting records as video streaming adoption broadens. Telstra now carries 9 million GB daily, and national average monthly usage is forecast to jump from 14.4 GB in 2023 to 28.7 GB in 2028. Subscription video-on-demand (SVOD) services reached 49.9 million active subscriptions in 2024, generating USD 2.7 billion revenue while driving a 47% increase in downstream data over the fixed and mobile networks. Unlimited mobile plans are rapidly replacing metered tiers, accounting for 57% of active services versus 6% a decade earlier. Gaming intensifies bandwidth demand: low-latency titles such as Call of Duty Mobile spur further traffic while pushing carriers to unlock edge-compute resources near population centers to manage jitter.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying price competition eroding mobile ARPU | -0.7% | National, acute in metro markets | Short term (≤ 2 years) |

| Regulatory price-setting and NBN wholesale cost pressures | -0.5% | National NBN areas | Medium term (2-4 years) |

| Rising fixed-wireless and LEO satellite substitution risk | -0.3% | Regional and remote Australia | Long term (≥ 4 years) |

| Talent shortage in advanced network engineering and AI | -0.4% | National, major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

NBN Wholesale Cost Pressures Constraining Operator Margins

Retail providers face widening cost-revenue gaps because NBN Co’s wholesale pricing has increased 4.1% annually, with higher-speed tiers absorbing the largest absolute jumps. The ACCC flagged NBN’s proposed special access undertaking as a “potential price shock,” adding oversight risk should indexation outpace CPI. Telstra warns that 25% of copper disconnections have not migrated to NBN due to affordability issues and argues that sustained wholesale rises threaten broadband penetration targets. Retailers increasingly upsell higher speed tiers and bundle entertainment to buffer gross margins, but headroom is limited as households tighten discretionary spend amid cost-of-living pressures.

Price Competition Intensifying Across Mobile Services

Telstra raised postpaid prices 4% in August 2024 to offset inflationary costs while Optus lifted prepaid tariffs by USD 4 in April 2025; TPG strategically responded with 50% promotional discounts, igniting churn in value-oriented customer segments. The ACCC’s 2024 market report notes retail mobile prices climbed an average 3.5% year-over-year but ARPU fell 2% as users shifted to lower cost plans or deferred handset upgrades.[3]Australian Competition and Consumer Commission, “Downloads Soar as Australians Binge on Streaming,” accc.gov.au TPG’s network-sharing with Optus extends coverage to 98.4% of the population, intensifying urban competition and restraining premium pricing power. Bundled offers—pairing mobile with NBN or streaming—are now core to loyalty strategies as carriers defend subscriber bases in saturated metro corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Command Market Leadership

Data services generated USD 10.9 billion in 2025, equating to 46.55% of Australian telecom MNO market share and growing at 3.99% CAGR through 2031. The rise of OTT video, cloud gaming, and enterprise VPN traffic positions data revenues to exceed USD 13.8 billion by the end of the period, sustaining their dominance within the Australian telecom MNO market. Voice services delivered USD 5.81 billion and hold 24.80% share but trail other categories with 3.74% CAGR as users pivot to over-the-top calling. IoT and M2M services contributed USD 1.87 billion, supported by projections that cellular IoT connections will climb to 6.4 billion globally by 2029. OTT and PayTV fetched USD 2.59 billion, while value-added and roaming services collectively accounted for USD 2.25 billion.

Data traffic grew threefold in five years, and average monthly consumption is poised to double through 2028, confirming the structural shift in user behavior. SVOD revenue expanded 14% year-over-year to USD 2.7 billion as subscription counts neared 50 million, explaining why data ARPU growth outstrips voice. ACMA performance codes now require carriers to publish peak-time packet-loss metrics, raising service-quality benchmarks that favor providers with dense backhaul and caching resources.

By End-user: Enterprise Segment Outpacing Consumer Growth

Enterprises contributed USD 7.3 billion in 2025, or 31.15% of Australian telecom MNO market size, and are set to widen their weight as 4.18% CAGR eclipses consumer growth. Large contracts such as Optus-Suncorp validate the premium enterprises pay for managed SD-WAN, secure cloud on-ramps, and unified communications. Government initiatives mandating Essential Eight cyber controls drive agencies toward certified telcos with Tier-IV data centers and ISO-27001 compliance.

Consumers still represent USD 16.12 billion of revenue, yet growth slows to 3.70% CAGR amid price fatigue and saturation. YouGov polling found 28% of Australians struggled to pay mobile bills in 2024, pushing carriers to extend hardship programs and low-income concessions. Small-business clients occupy a middle ground, demanding elastic bandwidth and zero-touch provisioning. Telstra’s Adaptive Networks suite bundles 4G/5G backup links and management portals, capturing SME wallet share while feeding cross-sell to cyber and UCaaS.

Geography Analysis

Metropolitan hubs exert disproportionate influence on traffic and revenues. Sydney posts the fastest median fixed download speed at 67.29 Mbps while Adelaide tops mobile at 125.79 Mbps, reflecting operator densification strategies. The National Broadband Network reaches more than 8.6 million premises, and 78% of its fixed-line footprint supports ultrafast tiers.

Rural Australia encounters persistent coverage gaps that direct-to-device LEO satellites now begin to bridge. Telstra’s June 2025 launch of Starlink-powered messaging covers thousands of blackspots and will add voice in 2027, aligning with government plans to embed LEO within the universal mobile service obligation framework. Optus targets 2028 for its counterpart service, with spectrum coordination rules under ACMA review to forestall interference.

Industrial regions in Western Australia and Queensland accelerate private 5G adoption, catalyzed by mining automation. Newmont’s Cadia mine demonstrated an 80% boost in communication reliability, and BHP trials edge-linked drones for real-time ore assessment. Tasmania and South Australia benefit from network-sharing accords that inject fresh capacity without duplicative towers, and dark-fiber backhaul routes through Adelaide’s data-center cluster ease interstate congestion. Ongoing ACMA spectrum auctions plus state-level co-investment grants under the Regional Connectivity Program ensure continued capex allocation outside big cities.

Competitive Landscape

Australia remains an oligopoly dominated by Telstra (44% share), Optus (31%), and TPG (17%). Their combined 92% revenue share underscores high, though gradually loosening, concentration. Telstra continues to invest USD 800 million over four years in AI-enabled self-optimizing networks, leveraging Microsoft Azure to cut outage incidence and shorten mean-time-to-repair. Optus differentiates on speed, achieving 230.5 Mbps median 5G downloads, and stakes growth on customer-experience refinements. TPG doubled coverage to 98.4% via network-sharing with Optus, positioning itself as price leader.

Infrastructure sharing is now strategic orthodoxy. The ACCC endorsed the Optus-TPG pact in 2024 but previously blocked a Telstra-TPG deal, citing undue market power. Vocus emerged as a formidable challenger after its USD 5.25 billion purchase of TPG’s enterprise fixed network, forming Australia’s largest independent fiber operator. Disruptors include LEO satellite entrants and IoT specialists such as M2M One that lease Telstra wholesale SIMs yet deliver full-stack device management.

Regulatory oversight anchors market openness. ACMA enforces spectrum-sharing conditions in the millimeter-wave bands, while the ACCC’s merger guidelines deter asset swaps that would entrench dominance. Privacy reforms and cybersecurity directives are adding compliance costs, but also level the field for mid-tier ISPs able to certify zero-trust architectures.

Australia Telecom MNO Industry Leaders

Telstra Corporation Limited

TPG Telecom Limited

Singtel Optus Pty Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Vocus completed acquisition of TPG Telecom’s Enterprise, Government and Wholesale fixed business for USD 5.25 billion, forming a 50,000 km fiber footprint.

- June 2025: Telstra launched Australia’s first direct-to-satellite text service over Starlink, with voice slated for 2027 rollout.

- March 2025: Government approved Vocus’ takeover of TPG fixed assets following ACCC and FIRB clearance.

- February 2025: Telstra posted 6% EBITDA growth to USD 4.2 billion and earmarked USD 800 million for mobile network upgrades.

Australia Telecom MNO Market Report Scope

The study provides an in-depth analysis of the telecommunication industry in Australia. The Australian telecom MNO market is segmented by services, which is further classified into voice services (wired, wireless), data and messaging services, and OTT and pay TV.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How fast is the shift from 4G to 5G connections in Australia?

5G already accounts for 41% of mobile subscriptions and is expected to hit 86% by 2031 on the back of a 15.90% CAGR in connections.

What is driving revenue growth in enterprise telecom services across Australia?

Rising demand for managed ICT, secure cloud connectivity, and private 5G networks is pushing enterprise revenue up at a 4.18% CAGR.

How much government funding is directed to fiber-to-the-premises upgrades?

The federal government has pledged USD 3 billion, matched by NBN Co’s USD 800 million, to extend gigabit access to 622,000 more premises by 2031.

Which player offers the fastest median 5G download speed?

Optus leads with a 230.5 Mbps median download rate, although Telstra retains the widest geographic 5G reach.

Page last updated on: