Australia Automotive Engine Oils Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

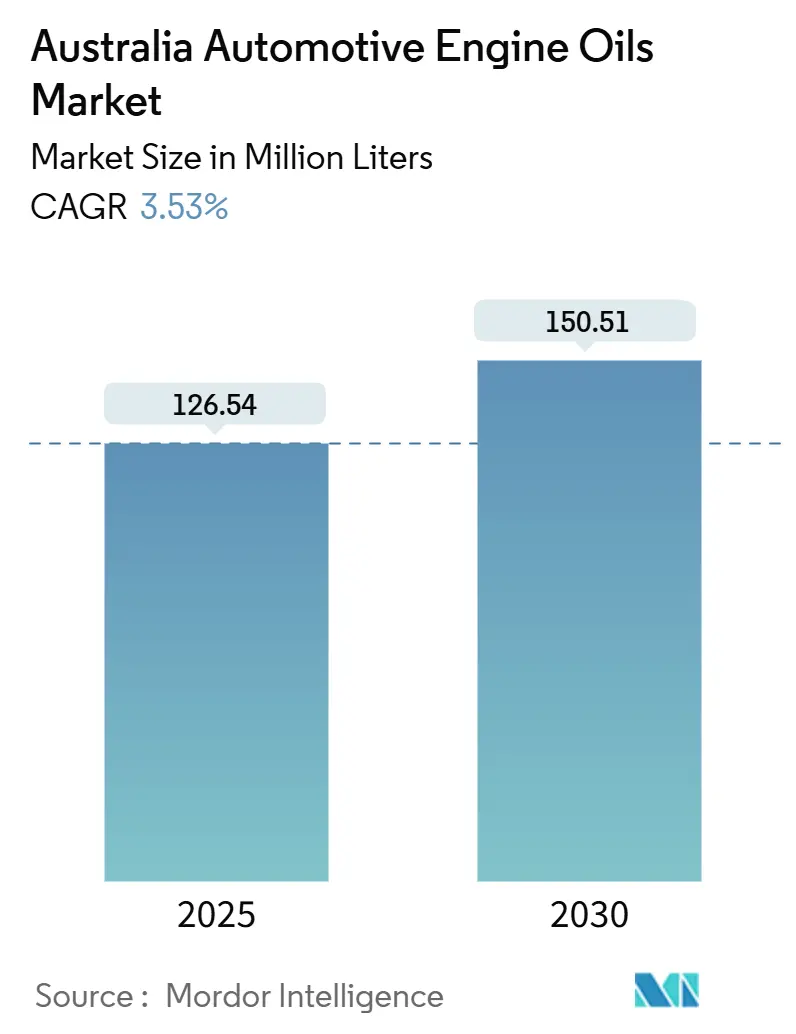

| Market Volume (2025) | 126.54 Million liters |

| Market Volume (2030) | 150.51 Million liters |

| Growth Rate (2025 - 2030) | 3.53% CAGR |

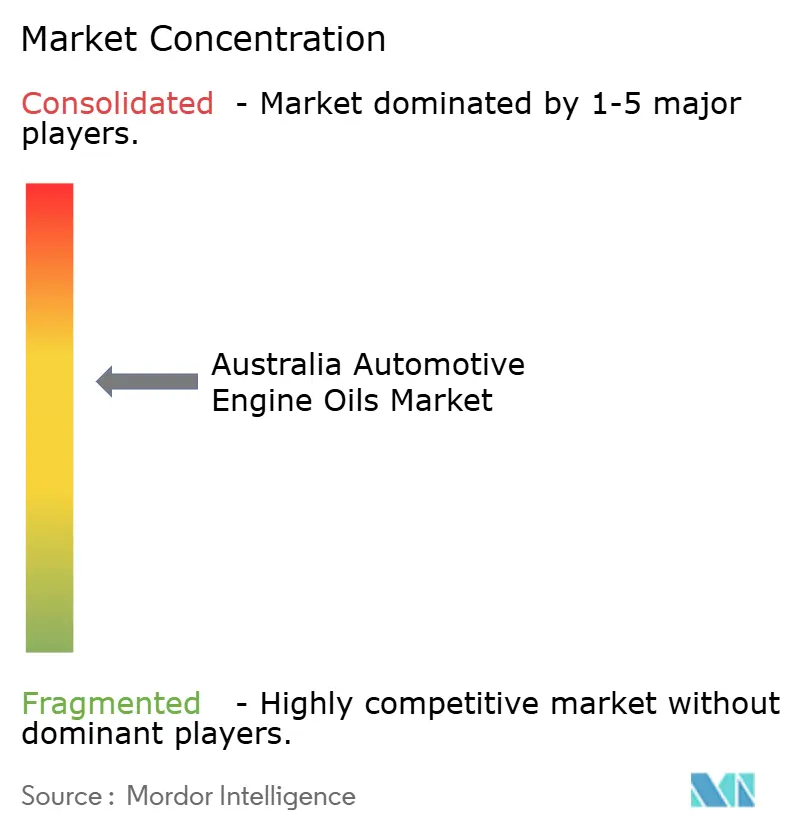

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Automotive Engine Oils Market Analysis by Mordor Intelligence

The Market size is estimated at 126.54 million liters in 2025, and is expected to reach 150.51 million liters by 2030, at a CAGR of 3.53% during the forecast period (2025-2030). Robust growth stems from an expanding vehicle parc, an aging fleet that needs more maintenance, and the steady roll-out of Euro 6d-ready, low-SAPS lubricants that fulfill stricter emissions regulations. Passenger, light-commercial, and mining fleets continue to rely on internal-combustion powertrains, ensuring that the Australian automotive engine oil market retains volume resilience even as battery-electric adoption accelerates in urban corridors. Premiumization is evident in all key channels, as synthetic and ultra-low-viscosity oils gain market share, particularly in New South Wales and Victoria, where higher household incomes and robust dealer networks favor higher-value formulations. Heavy-duty mining equipment in Western Australia and Queensland further underpins demand for extreme-duty formulations that support 1,000-hour drain intervals under harsh ambient conditions. Intense competition among BP, Shell, ExxonMobil, and a cadre of agile regional producers sustains price discipline while encouraging technology investments that keep pace with OEM approval cycles.

Key Report Takeaways

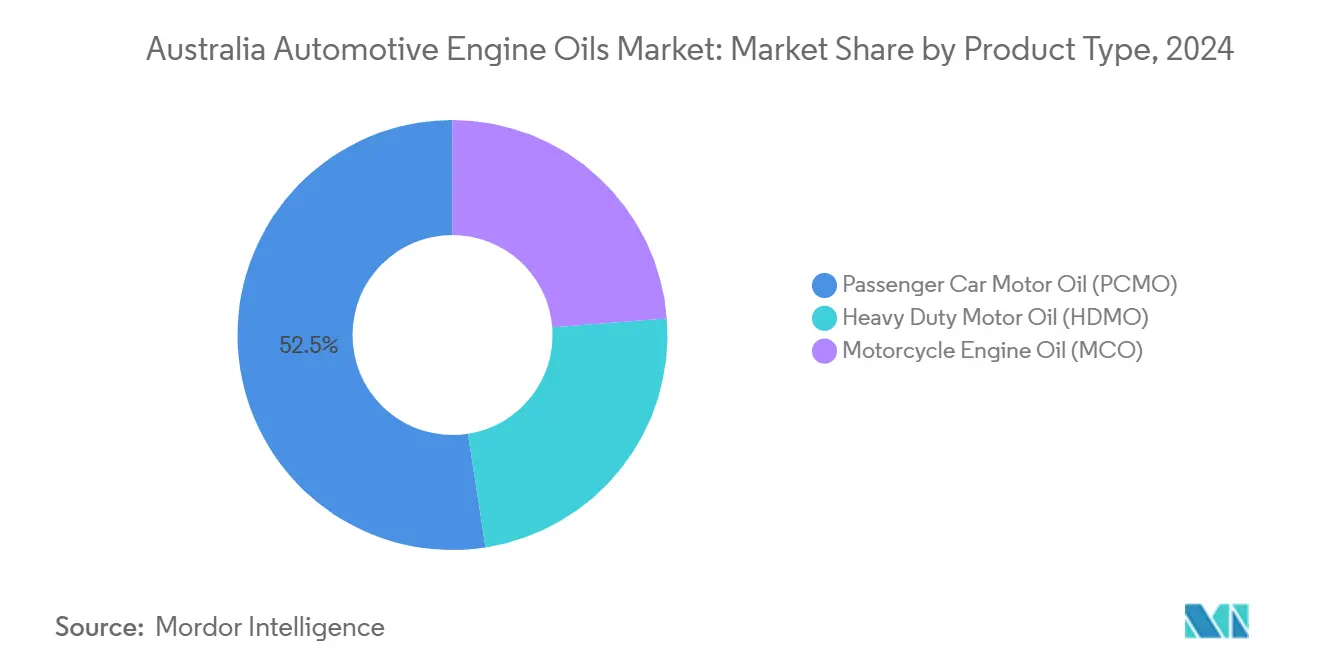

- By product type, passenger car motor oil accounted for 52.46% of the Australian automotive engine oil market share in 2024, while motorcycle engine oil is projected to post the fastest growth rate of 3.68% through 2030.

- By base stock, mineral oils captured 64.38% revenue share in 2024, while synthetic oils are forecast to grow at the swiftest 3.88% CAGR between 2025 and 2030.

Australia Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Passenger-car parc expansion and higher vehicle retention | +1.2% | NSW, VIC, QLD | Medium term (2-4 years) |

| Growing light-commercial and last-mile delivery fleets | +0.8% | Urban hubs | Short term (≤2 years) |

| Expansion of mining and agricultural equipment (HDMO) | +0.9% | WA, QLD, NT | Long term (≥4 years) |

| Shift to synthetic and ultra-low-viscosity oils | +0.4% | National | Medium term (2-4 years) |

| Euro 6d fuel-quality mandate accelerating low-SAPS demand | +0.3% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Passenger-car parc expansion and higher vehicle retention

Australia’s on-road fleet reached 21.74 million units in 2024, and the average vehicle age stretched to 11.3 years as households delayed new-car purchases[1]Australian Bureau of Statistics, “Motor Vehicle Census, Australia,” abs.gov.au. Older engines consume more lubricant per kilometer than newer powertrains, lifting annual service demand even as new-car sales plateau. The dynamic is pronounced in regional communities where disposable incomes lag behind those of major cities, leading owners to keep vehicles well past the first decade of service. Independent workshops benefit, capturing routine oil-change business from cars whose warranties have lapsed. Premium synthetics continue to penetrate this cohort because drivers seek longer drain intervals, which reduce the time and travel costs associated with servicing in remote areas. As a result, the Australian automotive engine oil market continues to benefit from both volume and value growth, tied to the aging of the fleet.

Growing light-commercial and last-mile delivery fleets

Surging e-commerce drove an increase in light-commercial registrations in 2024, with courier fleets in Sydney, Melbourne, and Brisbane adding thousands of vans to support same-day delivery routes. Stop-start duty cycles and short trip lengths accelerate oil degradation, prompting operators to adopt synthetic 5W-30 and 0W-20 formulations that meet OEM fuel economy targets. Fleet managers favor national suppliers that guarantee 48-hour delivery of bulk drums, and signed supply contracts often stipulate oil analysis services that minimize unplanned downtime. The scaling of urban logistics, therefore, injects steady incremental demand into the Australian automotive engine oil market, especially for premium PCMO grades that align with Euro 6d emission profiles.

Expansion of mining and agricultural equipment (HDMO)

Mining capital expenditure climbed in 2024. Massive trucks and excavators operating in Pilbara and Bowen Basin run 24/7 across abrasive terrain. OEMs such as Caterpillar and Komatsu specify low-ash CK-4/SN or better oils that endure extreme thermal loads and extended intervals up to 1,000 operating hours. Bulk deliveries to remote depots necessitate robust supply partnerships; major oil brands co-locate storage facilities alongside diesel fuel hubs to streamline logistics. Concurrently, farm mechanization in grain-dominant states increases demand for multi-grade HDMO compatible with Tier 4-Final diesel engines. These trends keep the Australian automotive engine oil market closely tied to resource- and agriculture-driven GDP activity.

Shift to synthetic and ultra-low-viscosity oils

OEM approvals for 0W-16 and 0W-20 grades multiplied in 2024 as brands like Toyota, Mazda, and Honda optimized powertrains for lower emissions. Synthetic penetration increased among premium passenger cars, a trend that continues to advance as dealers offer longer warranty packages contingent on approved oil usage. The shift trims overall liters per service due to longer drains, yet boosts supplier revenues because high-performance synthetics command price premiums of 60–80% over mineral alternatives. Marketing campaigns emphasize cold-start protection during alpine winters and oxidative stability in the northern tropics, ensuring national resonance for synthetics. Over time, this gradual migration adds sustainable value to the Australian automotive engine oil market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV and strong-hybrid penetration trimming ICE km-travelled | -0.6% | Urban centers | Medium term (2-4 years) |

| Extended-drain OEM approvals lowering replacement frequency | -0.4% | National | Short term (≤2 years) |

| Tightened waste-oil-to-energy emission caps raising cost base | -0.2% | National | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

BEV and strong-hybrid penetration trimming ICE km-travelled

Battery-electric vehicle sales increased in 2024. While hybrids add another 4.2%, most kilometers driven still accrue to internal-combustion cars. Nevertheless, early adopters in densely populated metropolitan areas are shifting their annual mileage away from traditional engines. Ride-share operators that switch to BEVs reduce oil-change visits entirely, signaling a slow but irreversible drag on volume. The Australian automotive engine oil market, therefore, observes a gradual decoupling of lubricant demand from new-car sales in core cities, prompting suppliers to broaden outreach toward commercial and off-road segments that face no near-term electrification.

Extended-drain OEM approvals lowering replacement frequency

From 2024 onward, leading brands authorized service intervals of 15,000 to 20,000 kilometers for mainstream passenger cars using API SP synthetic oils[2]Australian Automotive Aftermarket Association, “Market Trends and Industry Analysis 2024,” aaaa.com.au. Premium European marques go further, allowing for 25,000-kilometer cycles under normal driving conditions. Workshops experience lower foot traffic per vehicle, resulting in reduced throughput of bulk oil. Suppliers adapt by promoting ancillary services such as oil analysis and coolant packages, monetizing value over volume. Meanwhile, independent garages promote mid-grade semi-synthetic blends to older cars, whose owners are price-sensitive. The overall impact is a net decline in liters sold per passenger vehicle but an uptick in revenue per liter in the Australian automotive engine oil market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominance Amid MCO Acceleration

Passenger car motor oil generated the largest share, representing 52.46% of the Australian automotive engine oil market in 2024, and remains the backbone of routine service channels. Aging sedans and SUVs across suburban and regional households require consistent oil-change schedules every 10,000–12,000 kilometers, anchoring baseline demand. Dealers align factory warranties with approved 5W-30 and 0W-20 synthetics that meet Euro 6d and approvals from Toyota, Mazda, and Hyundai. Independent workshops cater to cost-conscious drivers by stocking 10W-30 mineral blends, ensuring that mineral PCMO still enjoys meaningful throughput. Fleet operators facing high utilization ratios increasingly opt for advanced synthetics to reduce downtime.

Motorcycle engine oil, though a smaller absolute volume contributor, will pace the Australian automotive engine oil market at a 3.68% CAGR through 2030. Recreational riding regained popularity after the pandemic lockdowns were lifted, and premium bikes from Harley-Davidson, Ducati, and BMW Motorrad require JASO MA2 5W-40 synthetics that protect their integrated wet clutches. Urban commuters in Sydney and Melbourne favor scooters but still rely on 10W-40 semi-synthetics that balance cost with durability. Suppliers bundle clutch additives to enhance gear-shift feel, a feature enthusiast riders value. As a result, both the average price per liter and total volumes in the motorcycle segment trend upward, mitigating the deceleration in passenger-car volumes. The Australian automotive engine oil market size for motorcycle oils is projected to increase steadily, although it remains a fraction of the PCMO base.

Heavy-duty motor oil rounds out the product mix, led by mining and agriculture fleets in Western Australia and Queensland that consume high-TBN 15W-40 and 10W-30 formulations tailored for high-sulfur diesel. OEM endorsements from Caterpillar, Cummins, and Volvo drive purchasing decisions, and drain intervals extend to 1,000 hours, reducing service events but increasing specialty additive demand. Consequently, the Australian automotive engine oil market exhibits a polarized product-type structure, where PCMO remains the largest contributor by volume, HDMO commands higher margins per liter, and MCO delivers the fastest growth trajectory.that

By Base Stock: Mineral Resilience Versus Synthetic Momentum

Mineral grades captured 64.38% of the Australian automotive engine oil market in 2024, underscoring entrenched purchasing habits among older-vehicle owners and small workshops. Price sensitivity remains high in rural zones where average vehicle age exceeds the national mean. Mineral PCMO 10W-30 and HDMO 15W-40 offer adequate protection under moderate duty, and distributors maintain wide inventories to ensure rapid fulfillment. Bulk-buy promotions further cement loyalty. However, minimal technological differentiation leaves suppliers vulnerable to commoditization, which compresses their margins.

Synthetic oils will expand at a 3.88% CAGR between 2025 and 2030, propelled by OEM 0W-20 approvals and the mining sector’s need for high-stability CK-4 formulations. These lubricants withstand severe temperature swings from alpine regions to desert interiors without experiencing a drop in viscosity, a crucial attribute demonstrated in field trials. Despite extended drain intervals that lower liters per service, revenue rises because the price per liter can be double that of mineral counterparts. The Australian automotive engine oil market size for synthetics will therefore outpace overall industry averages as premiumization continues to deepen.

Semi-synthetics bridge the gap, appealing to courier fleets that seek better oxidation stability without incurring the full costs of synthetics. Bio-based stocks remain nascent, currently limited to environmentally sensitive mining leases near heritage sites where chemical runoff restrictions are in effect. Suppliers view bio-based offerings as reputational differentiators rather than short-term revenue drivers. Over the forecast horizon, the Australian automotive engine oil industry anticipates a gradual yet persistent shift in mix from mineral to synthetic, reinforcing the premium value narrative.

Geography Analysis

Western Australia and Queensland dominate heavy-duty consumption as iron-ore, coal, and gold extraction push lubricant usage well above population-based expectations. Mining trucks with 400-ton payloads rely on bulk deliveries to remote depots, and mobile service units perform field oil changes to protect uptime. Synthetic HDMO adoption is highest in Pilbara, where daytime temperatures exceed 45 °C, compelling operators to prioritize oxidation stability. These states also maintain substantial fleets of agricultural machinery, which add seasonal peaks to demand during harvest cycles.

New South Wales and Victoria underpin passenger-car motor oil volumes due to their dense urban populations and established dealership networks. High disposable incomes favor premium synthetics, and many owners contract dealership service plans that specify OEM-approved 0W-20 grades. Motorcycle ownership is also concentrated along coastal corridors, driving niche demand for JASO-spec oils. As a result, the Australian automotive engine oil market records above-average per-vehicle spend in these states.

South Australia and Tasmania maintain stable but smaller volumes, driven by agricultural and tourism vehicles. Seasonal tourism patterns result in demand surges during the summer months, when interstate travelers drive long distances to visit their destinations. Lubricant distributors position regional warehouses near Adelaide and Hobart to ensure rapid resupply. The Northern Territory, although sparsely populated, hosts defense and gas projects that consume specialized lubricants, including compressor oils for LNG facilities. Collectively, geography-driven nuances necessitate that suppliers strike a balance between national brand propositions and localized product assortments, thereby reinforcing logistical partnerships that are crucial to the Australian automotive engine oil market.

Competitive Landscape

The Australian automotive engine oil market is moderately consolidated. Regional specialists compete on formulation tailoring and brand heritage. Penrite’s HPR range emphasizes extra-ten additive packages designed for older, high-kilometer engines common in regional Australia. Nulon pioneers the local blending of low-SAPS oils that meet Euro 6d, ahead of the 2025 deadline, and wins shelf space in independent parts stores. Multinational entrants expand their share through motorsport sponsorships that boost consumer recognition. The competitive environment thus fosters continuous product innovation, which benefits the Australian automotive engine oil market. Strategic moves increasingly center on sustainability. Collectively, these shifts illustrate an industry in transition, yet one that remains anchored by long-standing brand loyalties.

Australia Automotive Engine Oils Industry Leaders

BP p.l.c.

Shell plc

Chevron Corporation

Exxon Mobil Corporation

Penrite Oil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c. announced plans to sell its Castrol lubricants division, valued at up to USD 10 billion, as part of a broader USD 20 billion divestment program.

- December 2024: Liqui-Moly introduced a new range of generalist motor oils tailored for Australian conditions, formulated in Germany and produced in Thailand.

Australia Automotive Engine Oils Market Report Scope

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

How large is the Australian automotive engine oil market in 2025?

The market stands at 126.54 million liters in 2025 and is projected to reach 150.51 million liters by 2030.

Which product type generates the most demand?

Passenger car motor oil leads with 52.46% of total volume, thanks to the nation’s large passenger parc.

What is the fastest-growing segment?

Motorcycle engine oil is forecast to expand at a 3.68% CAGR as premium bike ownership rises.

Why are synthetic oils gaining share?

OEM approvals for 0W-20 grades, extended drain intervals, and extreme temperature stability drive a 3.88% CAGR for synthetics.

How will electric vehicles impact lubricant demand?

BEV adoption trims internal-combustion mileage in major cities, lowering volume growth, yet the aging ICE fleet sustains baseline demand through 2030.

Page last updated on: