Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

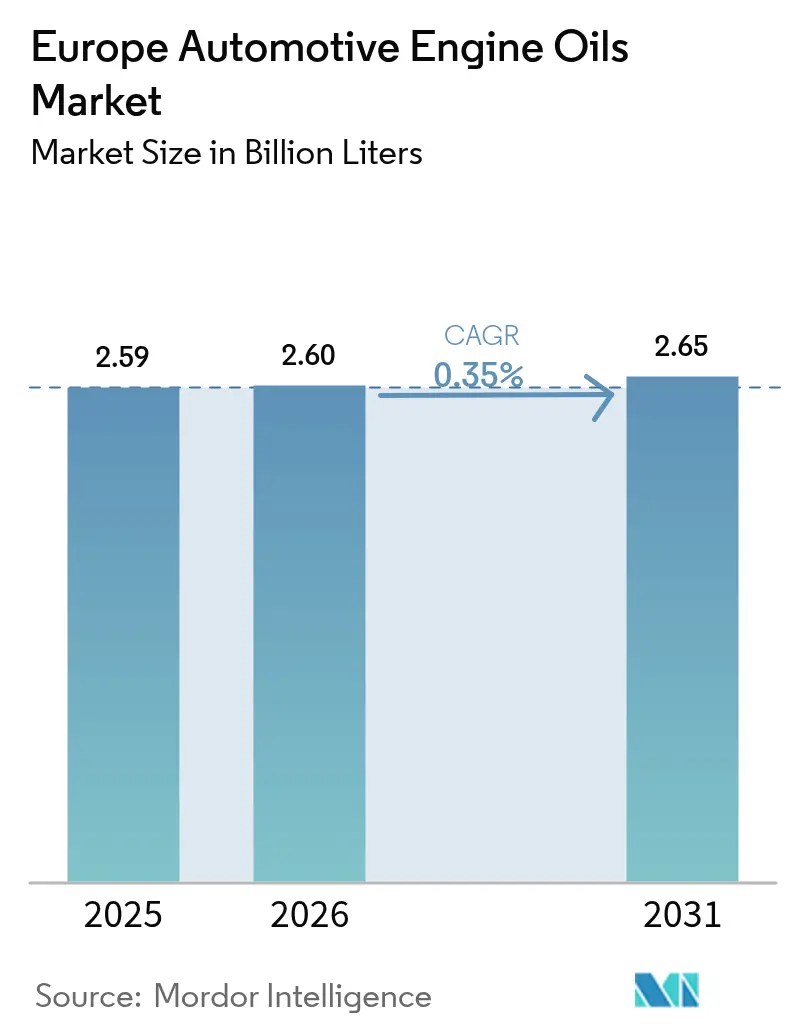

| Base Year Market Size (2025) | 2.59 Billion liters |

| Market Volume (2026) | 2.6 Billion liters |

| Market Volume (2031) | 2.65 Billion liters |

| Growth Rate (2026 - 2031) | 0.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Engine Oils Market Analysis by Mordor Intelligence

The European Automotive Engine Oils Market size in 2026 is estimated at 2.6 billion liters, growing from 2025 value of 2.59 billion liters with 2031 projections showing 2.65 billion liters, growing at 0.35% CAGR over 2026-2031. The muted trajectory reflects structural changes as battery-electric vehicles erode internal-combustion volumes, yet a large aging vehicle parc, low-viscosity regulatory mandates, and growing hybrid sales continue to underpin lubricant demand. Suppliers respond by intensifying research and development on premium synthetics, expanding regenerated base-oil capacity, and aligning specifications with stringent OEM approvals that favor low-sap, low-viscosity formulations. Competitive intensity now centers on technological differentiation and sustainability credentials rather than sheer output, while margin volatility stems from crude price swings and additive supply disruptions. Policy drivers such as the European Union “Fit for 55” package, national circular-economy regulations, and waste-oil regeneration quotas are accelerating the shift toward advanced synthetics and bio-based lubricants.

Key Report Takeaways

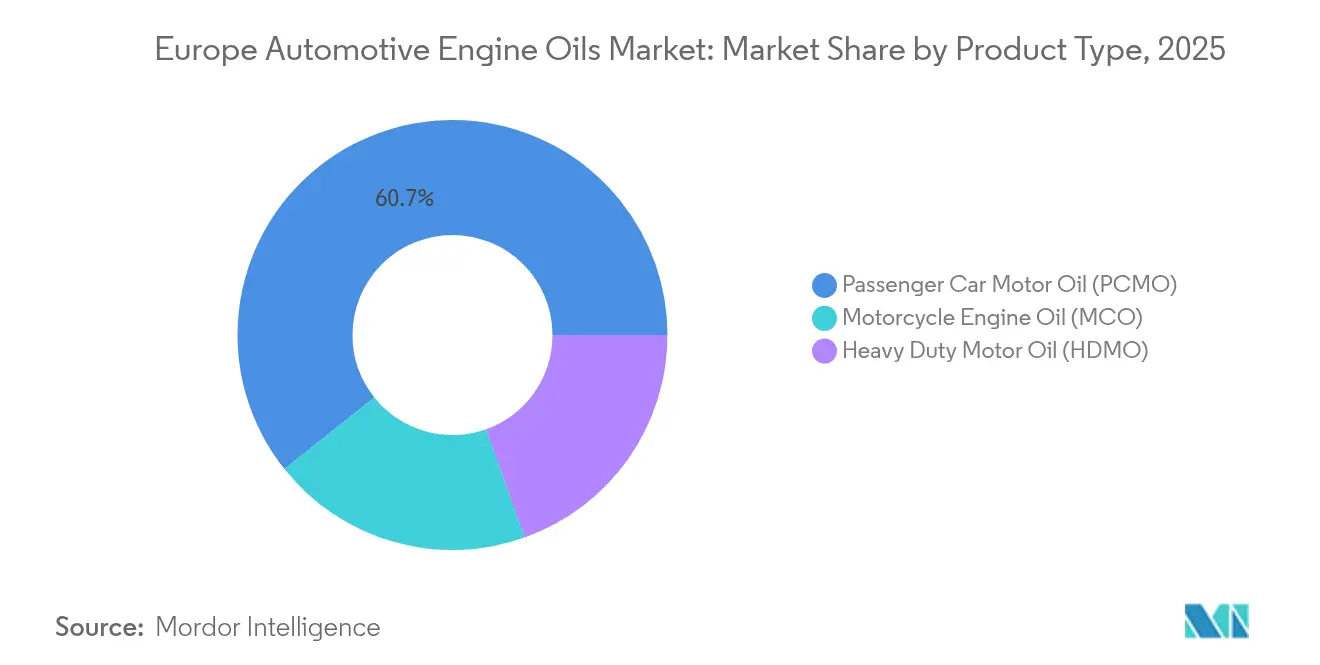

- By product type, Passenger Car Motor Oil held 60.72% of the Europe automotive engine oils market share in 2025, whereas Motorcycle Engine Oil is forecast to expand at a 0.92% CAGR through 2031.

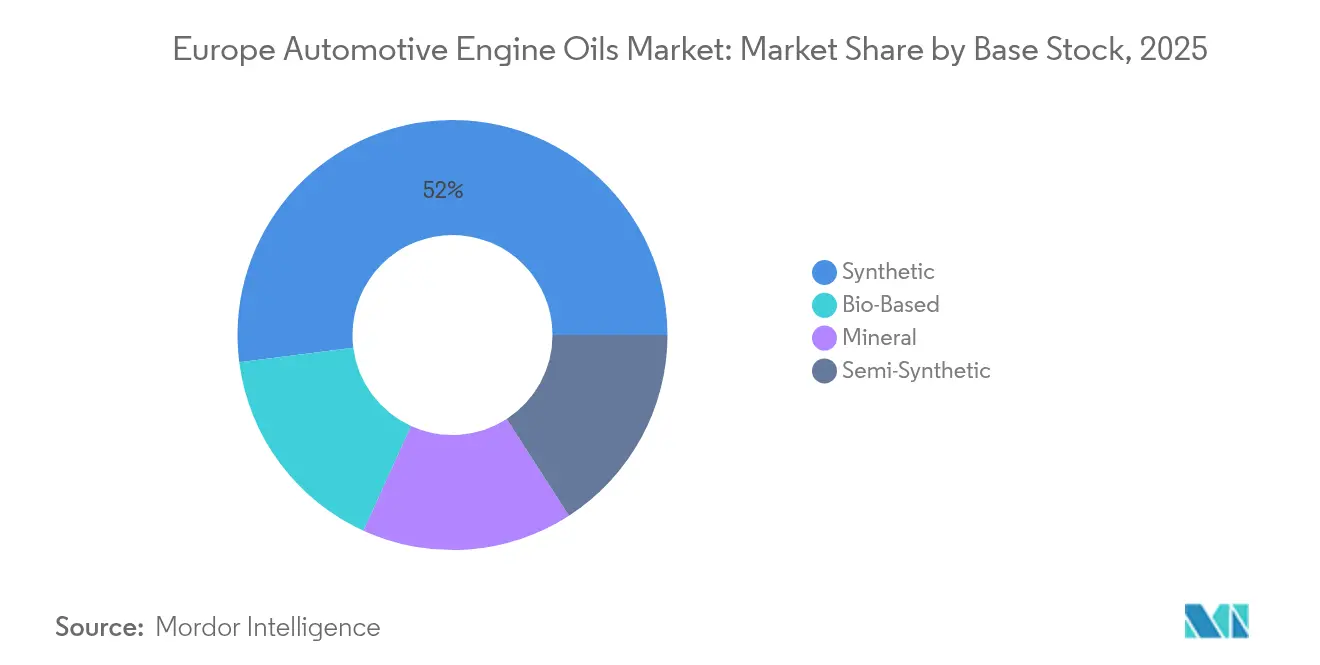

- By base stock, synthetic oils accounted for 52.02% share of the Europe automotive engine oils market size in 2025, while bio-based formulations record the highest projected CAGR at 0.9% to 2031.

- By geography, Russia represented 19.05% revenue share of the Europe automotive engine oils market in 2025; Poland is set to record the fastest growth at 0.83% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European Union CO₂ and fuel-economy targets push low-viscosity formulations | +0.15% | EU core markets, spillover to UK and Nordic countries | Medium term (2-4 years) |

| Aging ICE vehicle parc sustains oil-change volumes | +0.12% | Germany, France, Italy, Spain with established vehicle fleets | Long term (≥ 4 years) |

| OEM specification proliferation drives premium synthetics | +0.08% | Germany, Nordic countries, premium vehicle markets | Medium term (2-4 years) |

| Hybrid-vehicle growth needs low-ash, low-viscosity oils | +0.06% | Western Europe, Nordic countries leading electrification | Short term (≤ 2 years) |

| Waste-oil regeneration quotas spur re-refined base-oil demand | +0.05% | France, Germany, Italy with established collection systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

European Union CO₂ and Fuel-Economy Targets Push Low-Viscosity Formulations

Upcoming fleetwide CO₂ caps compel automakers to specify ultra-thin 0W-20 and even 0W-16 grades that deliver measurable fuel-efficiency gains. Volkswagen shifted its entire TSI engine family to 0W-20 service fills in 2025, prompting aftermarket workshops to stock advanced synthetics with high Group III and poly-alpha-olefin content[1]European Environment Agency, “Waste oil,” eea.europa.eu. Low-viscosity grades command 20-30% price premiums because heavier 5W-30 and 10W-40 oils cannot meet viscosity-temperature targets. The mandate boosts Europe automotive engine oils market demand for high-performance base stocks and premium additive packages while commoditizing legacy grades.

Aging ICE Vehicle Parc Sustains Oil-Change Volumes

The average German passenger car age climbed to 10.1 years in 2024, and similar trends appear across France, Italy, and Spain[2]Kraftfahrt-Bundesamt, “Vehicle Registration Statistics,” kba.de . Older engines require more frequent oil changes and tolerate conventional or semi-synthetic formulations, offsetting volume lost to electrification. Independent workshops capture a larger share of this replacement business as vehicles exit warranty coverage, thereby maintaining baseline lubricant demand in the Europe automotive engine oils market even as new-car electrification rises.

OEM Specification Proliferation Drives Premium Synthetics

Mercedes-Benz introduced MB-Approval 229.72 for hybrid models, while BMW launched Longlife-17 FE+ in 2024, adding to more than 40 new approvals last year. Workshops now juggle a growing matrix of proprietary specs, and non-compliance can void warranties. This complexity locks in premium synthetics from suppliers with extensive approval portfolios, reinforcing price resiliency in the Europe automotive engine oils market.

Waste-Oil Regeneration Quotas Spur Re-Refined Base-Oil Demand

EU circular-economy legislation now requires member states to regenerate a minimum of 85% of collected waste oil by 2030, initiating a wave of re-refinery investments in France, Germany, and Italy. Suppliers incorporate recycled base stocks into premium blends to meet sustainability targets without compromising performance, adding a new competitive dimension to the Europe automotive engine oils market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV penetration shrinks long-term ICE pool | -0.18% | Nordic countries, Netherlands, Germany leading adoption | Long term (≥ 4 years) |

| Volatile crude and additive supply costs pressure margins | -0.08% | Global impact with particular pressure on smaller European blenders | Short term (≤ 2 years) |

| OEM lifetime-fill and sensors extend drain intervals | -0.12% | Germany, premium markets with advanced vehicle technology adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV Penetration Shrinks Long-Term ICE Pool

Battery-electric vehicles captured 14.6% of European new-car registrations in 2024, and the share could exceed 30% of the rolling fleet by 2035. Nordic markets already display lubricant volume contraction, signaling future pressure for suppliers heavily exposed to internal-combustion demand. The contraction risk looms largest for the Europe automotive engine oils market participants lacking diversification into electrification-adjacent fluids.

Volatile Crude and Additive Supply Costs Pressure Margins

Crude price spikes and additive shortages inflate raw-material costs, challenging small and mid-sized blenders that lack procurement leverage. Many have responded by raising prices or trimming product lines, but escalating input volatility still compresses margins, especially in price-sensitive mineral segments of the Europe automotive engine oils market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Passenger Car Motor Oil Dominance Faces MCO Growth Challenge

Passenger Car Motor Oil held 60.72% of the European automotive engine oils market in 2025. PCMO volumes benefit from a 250 million-unit passenger car fleet, yet growth remains flat as fleet electrification offsets miles-driven recovery. Premium fully synthetic 0W-20 and 0W-16 formulations extend drain intervals to 30,000 kilometers, allowing OEMs to advertise lower ownership costs while still protecting engines. Independent garages lead distribution, but authorized dealer channels retain high-margin factory-fill business where OEM approvals remain non-negotiable.

Motorcycle Engine Oil is expected to post the fastest 0.92% CAGR through 2031. Urban congestion, last-mile delivery, and recreational riding boost two-wheeler demand, especially in Italy, Spain, and France. High-performance motorcycles require JASO MA2 oils with shear stability, wet-clutch compatibility, and thermal resilience, driving premium pricing. Europe automotive engine oils market participants that cultivate dealer networks and sponsor racing events capture brand loyalty among enthusiasts who accept higher per-liter prices.

By Base Stock: Synthetic Leadership Meets Bio-Based Innovation

Synthetics comprised 52.02% of the European automotive engine oils market share in 2025. Group III and PAO heavy blends deliver superior cold-start viscosity and oxidation resistance, aligning with OEM goals for fuel economy and long service intervals. Semi-synthetic products bridge price and performance gaps for cost-conscious drivers.

Bio-based lubricants registers a leading 0.9% CAGR. EU eco-label programs and corporate sustainability pledges spur adoption, and regenerated base stocks satisfy circular-economy criteria. TotalEnergies cooperated with Stellantis to launch a recycled-content engine oil that meets OEM durability standards. As supply scales, cost parity approaches, positioning bio-based blends to carve a share from conventional mineral formulations across the European automotive engine oils market.

Geography Analysis

Russia generated 19.05% of the European automotive engine oils market volume in 2025. A 45 million-unit passenger car parc plus heavy-duty fleets serving resource extraction maintain robust lubricant demand. Sanctions impeded Western additive imports, prompting domestic players such as LUKOIL and Gazprom Neft to intensify local formulation work while sourcing alternative chemistries from Asia. Distribution remains primarily through fuel-station channels and independent retailers; however, premium synthetic penetration lags Western Europe, leaving room for future value-added growth.

Poland represents the fastest-growing national market at 0.83% CAGR. OEM investments from Stellantis, Volkswagen, and Toyota expand factory-fill requirements, while rising disposable income supports vehicle ownership growth. Aftermarket volume benefits from a relatively young but expanding passenger car fleet that leans toward semi-synthetic upgrades. Government incentives for industrial upgrading have also encouraged refinery construction, enhancing domestic circular-economy capacity in the European automotive engine oils market.

Germany, France, Italy, and Spain make up a mature core with flat volumes but strong premiumization. German consumers show the highest synthetic adoption, with 0W-20 now the dominant grade for new cars. France advances recycled content deployment, while Italy and Spain offer growth pockets in motorcycle lubricants owing to favorable climate and riding culture. Nordic countries provide a test bed for low-temperature and high-BEV specialty fluids, shaping future product roadmaps for the wider Europe automotive engine oils market.

Competitive Landscape

The Europe automotive engine oils market displays moderate fragmentation. Medium-sized regional players compete through agility and local branding. LIQUI MOLY wins share in Germany via motorsport sponsorships and enthusiast marketing, while Wolf Oil grows in Benelux by offering OEM-approved private-label products. Strategic emphasis has shifted from volume to sustainability positioning. Suppliers promote carbon-neutral production, low-carbon packaging, and digital service platforms that guide workshops on correct oil selection, adding service value while defending premiums in the European automotive engine oils market.

Europe Automotive Engine Oils Industry Leaders

BP plc

Exxon Mobil Corporation

FUCHS

Shell plc

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: LIQUI MOLY unveiled an engine-oil formulation meeting Stellantis FPW9.55535/03 for PSA engines with wet timing belts, mitigating abrasive wear in belt-in-oil architectures.

- November 2023: Telko expanded its Castrol distribution agreement to cover the full automotive range in Denmark, strengthening Nordic and Baltic lubricant coverage.

Europe Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Nordic Countries |

| Russia |

| Rest of Europe |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected volume of lubricant demand in Europe by 2031?

The Europe automotive engine oils market is forecast to reach 2.65 billion liters by 2031, rising only marginally from 2026.

How fast will bio-based engine oils grow in Europe?

Bio-based formulations are projected to expand at a 0.9% CAGR through 2031 as circular-economy mandates boost recycled content adoption.

Which resin type is growing the quickest?

Motorcycle Engine Oil leads with a 0.92% CAGR thanks to urban mobility trends and high-performance bike popularity in Southern Europe.

Why do low-viscosity oils command premium prices?

They help automakers meet CO? targets and require advanced synthetic base stocks, allowing suppliers to price them 2030% higher than heavier grades.

Which country offers the strongest growth prospects?

Poland tops the outlook with a 0.83% CAGR, driven by expanding vehicle production and rising consumer ownership.

Page last updated on: