Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

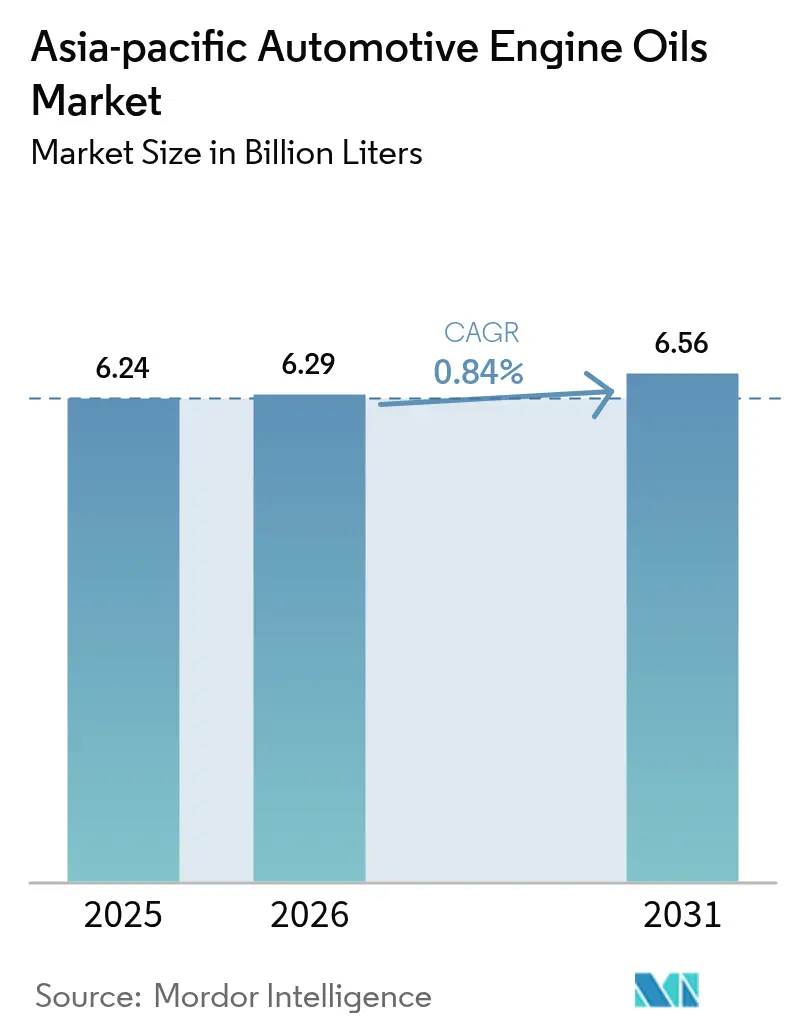

| Base Year Market Size (2025) | 6.24 Billion Liters |

| Market Volume (2026) | 6.29 Billion Liters |

| Market Volume (2031) | 6.56 Billion Liters |

| Growth Rate (2026 - 2031) | 0.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Automotive Engine Oils Market Analysis by Mordor Intelligence

The Asia-Pacific Automotive Engine Oils Market size is expected to grow from 6.24 Billion Liters in 2025 to 6.29 Billion Liters in 2026 and is forecast to reach 6.56 Billion Liters by 2031 at 0.84% CAGR over 2026-2031. The region’s measured growth stems from diverging mobility patterns in which a still-expanding internal combustion engine (ICE) fleet in emerging ASEAN economies compensates for the rising share of electrified vehicles in mature countries. Suppliers are therefore shifting strategic focus from volume scale to value optimization, emphasizing premium synthetic formulations, OEM-approved factory-fill relationships, and service-driven distribution. Tightening fuel-economy rules hasten the adoption of low-viscosity grades, while ride-hailing fleets boost lubricant consumption per vehicle despite moderating overall parc growth. Heightened competition, especially in China, is accelerating technology differentiation as companies pivot toward high-performance fluids for hybrid and electric powertrains.

Key Report Takeaways

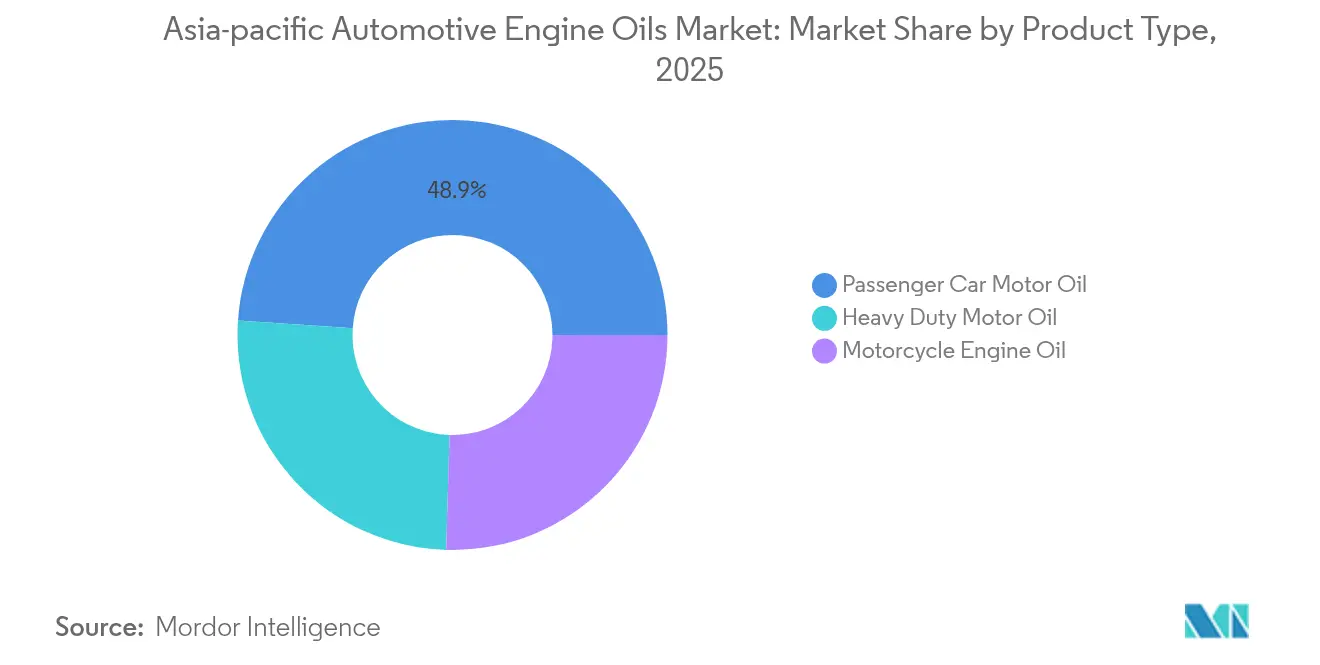

- By product type, Passenger Car Motor Oil held 48.92% of the Asia-Pacific Automotive Engine Oils Market share in 2025, while Motorcycle Engine Oil is projected to grow at a 0.93% CAGR through 2031.

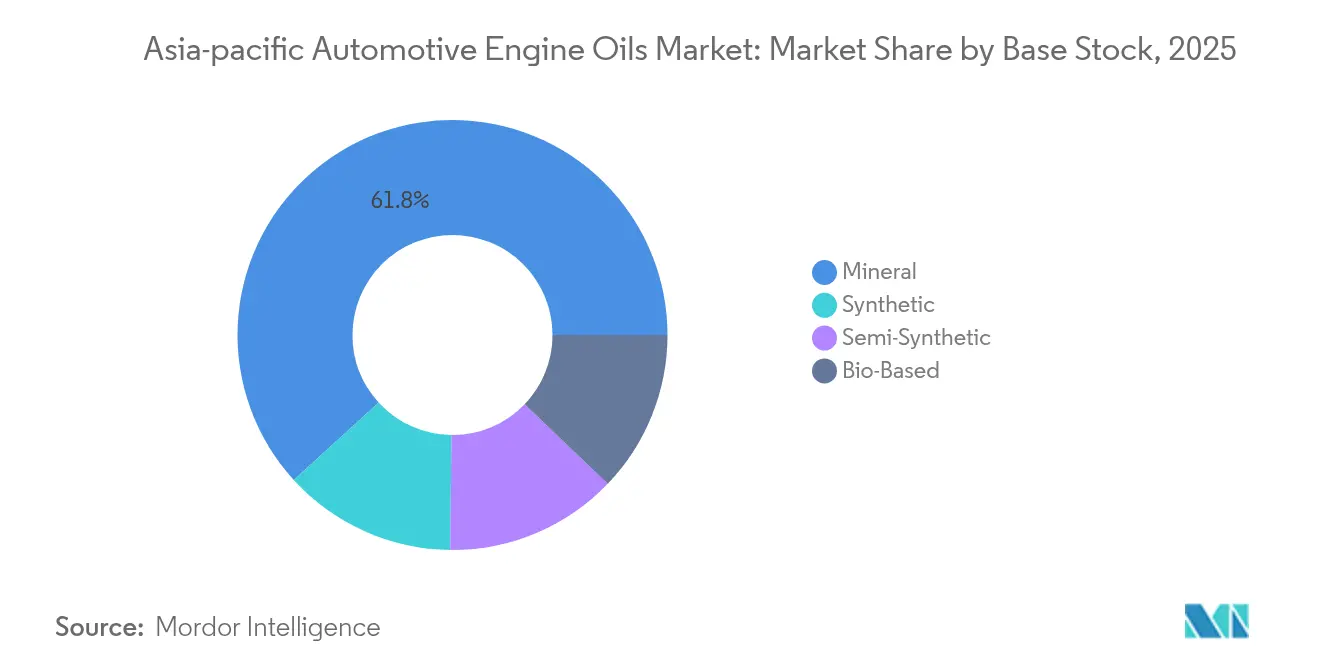

- By base stock, mineral oils accounted for 61.78% of the Asia-Pacific Automotive Engine Oils Market size in 2025; synthetics are expected to record the highest forecast growth at a 1.08% CAGR.

- By geography, China led with a 34.78% revenue share in 2025, whereas Vietnam is forecast to post the fastest growth at a 3.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE parc still expanding in emerging ASEAN | +0.3% | Indonesia, Thailand, Vietnam, Malaysia | Medium term (2-4 years) |

| OEM factory-fill tie-ups with lube majors | +0.25% | China, Japan, South Korea | Long term (≥ 4 years) |

| Tightening APAC fuel-economy standards | +0.2% | Japan, South Korea, China, India | Medium term (2-4 years) |

| Surge in ride-hailing motor-hours | +0.15% | ASEAN, China, India urban hubs | Short term (≤ 2 years) |

| Electrified two-wheeler range-extender hybrids | +0.1% | Taiwan, Japan, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ICE parc still expanding in emerging ASEAN

Rapid vehicle fleet growth in Vietnam, Indonesia, Thailand, and Malaysia continues to drive positive conventional lubricant demand, even as electrification advances. Vietnam’s automotive roadmap aims for 1 million annual vehicle sales by 2030, implying double-digit growth and stronger factory-fill volumes for local assemblers[1]Vietnam Investment Review, “Vietnam Aims for One Million Cars Annually by 2030,” vir.com.vn. Indonesia’s 125.31 million motorcycle fleet similarly sustains high consumption of Motorcycle Engine Oil as commuting remains two-wheeler-centric. Localization rules that mandate 55-60% domestic content by 2030 stimulate regional blending plants, which lower logistics costs and enable customized formulations for tropical duty cycles. Across these markets, the Asia-Pacific Automotive Engine Oils Market benefits from aftermarket demand tied to small-engine maintenance intervals common in congested urban traffic. Suppliers capitalizing on this upside deploy dealer-education programs and branded service chains to secure repeat purchases.

OEM factory-fill partnerships drive premium segment growth

Automakers increasingly embed lubricant brands into their warranty propositions, channeling purchases toward approved suppliers. Recent agreements between Shell and several Japanese manufacturers demonstrate how the co-development of 0W-20 and 5W-30 blends, tailored for hybrid engines, supports extended drain intervals of up to 10,000 km. TotalEnergies’ collaboration with Kia also ties lubrication recommendations to OEM telematics that prompt service visits, thereby increasing customer stickiness. These programs shift the competitive arena from retail shelves to design centers, rewarding formulators with additive chemistry that balances fuel economy, low-temperature start-up, and catalytic-converter durability. As hybrid sales rise, factory-fill volumes act as gateways to profitable dealership aftermarkets, reinforcing brand equity and accelerating the premiumization trajectory of the Asia-Pacific Automotive Engine Oils Market.

Tightening fuel-economy standards accelerate low-viscosity adoption

Japan’s top-tier fuel-efficiency mandates, India’s CAFE targets, and China’s dual-credit system are spurring a rapid transition from legacy 20W-50 grades to 0W-20 and 5W-20 formulations. To meet these norms, OEMs downsize engines and raise turbocharger pressures, demanding lubricants with stronger high-temperature shear stability. Synthetic Group III base stocks answer that need, leading refiners such as Shell to convert the Wesseling site for premium base oil output. This regulatory alignment sharpens the value proposition of the Asia-Pacific Automotive Engine Oils Market, incentivizing R&D investment in detergent dispersants that guard exhaust-gas-recirculation systems against high-soot loads. Vendors that master low-viscosity chemistries gain an early-mover advantage as smaller, direct-injection engines proliferate across compact car segments.

Ride-hailing expansion intensifies commercial lubricant demand

Urban ride-hailing fleets in Jakarta, Bangkok, Mumbai, and Manila often accumulate four to five times the mileage of private cars, resulting in disproportionate lubricant consumption. Fleet managers focus on reducing downtime, favoring high-performance synthetics that double drain intervals while maintaining piston cleanliness under stop-start cycles. This usage profile increases per-vehicle consumption, partly offsetting the slower growth in private car ownership. Lube suppliers increasingly bundle telematics-based oil-life monitoring to secure long-term service contracts. For the Asia-Pacific Automotive Engine Oils Market, these intensively utilized vehicles anchor demand pockets even in cities where electrification policies are most aggressive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronic vehicle penetration in China passenger cars | -0.4% | China, spillover to ASEAN | Medium term (2-4 years) |

| Longer OEM drain-interval specifications | -0.25% | Led by Japan and South Korea | Long term (≥ 4 years) |

| Government push for bio-lubricants | -0.15% | India, Indonesia, Malaysia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electronic vehicle penetration constrains traditional demand growth

China’s accelerating shift toward battery electric cars removes engine lubrication requirements entirely and influences ASEAN policy road maps. EV share in the region reached 13% in 2024 and is on track for 8.5 million units by 2035[2]Economic Research Institute for ASEAN and East Asia, “EV Outlook 2024,” eria.or.id. While hybrids moderate the decline by retaining small engines, overall per-vehicle lubricant volumes contract, forcing suppliers to hedge through EV thermal-management fluids and gear oils. Distribution models must also adapt as charging ecosystems reshape service-station economics, compressing conventional oil-change revenue streams across the Asia-Pacific Automotive Engine Oils Market.

Extended drain intervals reduce service frequency requirements

Advanced additive chemistries now enable 10,000-15,000 km passenger-car intervals and duty-cycle-based schedules for commercial engines. Cummins and Hyundai publish optimized drain guidelines that cut workshop visits by 30-40%, directly lowering liters consumed per vehicle. Although synthetics command higher unit prices, the net volume impact remains negative, posing a challenge to traditional high-turnover distributors. Producers respond by offering oil-condition analysis and predictive maintenance dashboards to embed themselves in fleet value chains, rather than relying solely on throughput.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO leads yet MCO outpaces on growth

Passenger Car Motor Oil generated the largest slice of the Asia-Pacific Automotive Engine Oils Market in 2025 at 48.92%, benefiting from the region’s still-dominant passenger-vehicle parc. Motorcycle Engine Oil, however, is the fastest riser, with a 0.93% CAGR to 2031, driven by the predominance of two-wheelers in ASEAN megacities and the emergence of range-extender hybrid scooters. Heavy-duty motor oil remains stable, reflecting steady infrastructure investment and regional freight expansion.

MCO growth also aligns with OEM experimentation in small-capacity hybrid engines that run at steady RPM for generator duties, demanding thermally robust lubricants. Suppliers attuned to this niche develop shear-stable 10W-30 grades that are compatible with the wet-clutch systems commonly found in Asia’s motorcycle designs. As urban congestion increases, ride-share scooter usage rises, and service chains that market fast oil swaps at roadside kiosks deepen consumer loyalty. Overall, diversified product portfolios enable vendors to cushion slowing PCMO volumes while capitalizing on the faster-growing MCO segment of the Asia-Pacific Automotive Engine Oils Market.

By Base Stock: mineral majority supports synthetic momentum

Mineral oils still hold 61.78% of Asia-Pacific Automotive Engine Oils Market share due to cost sensitivity in mass-market segments and entrenched supply chains. Yet synthetics record the strongest 1.08% CAGR thanks to premium vehicle penetration, fuel-efficiency regulation, and extended service mandates. Semi-synthetic blends bridge the gap, offering step-up performance at attainable price points.

Capital commitments by majors underscore the shift: Shell’s Wesseling refinery upgrade to Group III production and Ruifeng’s additive capacity build-out ensure regional availability of high-grade base stocks. China’s domestic 150N base-oil price averaging 8,651 CNY per tonne in first-half 2024 (USD 1,211 per tonne) influences finished-lube economics region-wide. Base-oil hedging and formulation flexibility thus become vital levers for profitability in the Asia-Pacific Automotive Engine Oils Market size competition.

Geography Analysis

China anchors demand with a 34.78% share, reflecting its large vehicle parc and integrated refining assets; however, growth moderates amid a sharp EV pivot and market saturation. Production reached 7.39 million tonnes in 2024, and state-owned giants CNPC and Sinopec leverage scale to defend roughly half of the country’s sales. Regulatory emphasis on low-viscosity and quality standards accelerates synthetic adoption and premium blend differentiation.

In contrast, Vietnam is projected to post the fastest 3.12% CAGR through 2031, as government programs target 1 million annual vehicle sales and 70% domestic content, thereby fostering new factory-fill volumes and aftermarket opportunities. Over 377 component manufacturers, 169 of them foreign-invested, underpin a widening parts ecosystem that favors local blending plants. Emerging hybrid and EV production mandates also position Vietnam as a dual-technology growth arena for the Asia-Pacific Automotive Engine Oils Market.

ASEAN neighbors, such as Indonesia, Thailand, and Malaysia, contribute sizable incremental volumes through a combined vehicle fleet of more than 200 million units, which is dominated by motorcycles. Policies that mix EV incentives with ICE export goals generate a blended demand structure that sustains mineral oil consumption while nudging synthetics higher. Meanwhile, Japan and South Korea set the technology tone, exporting stringent viscosity norms and extended drain expectations to the wider region via their OEM footprints. Collectively, these varied trajectories create a mosaic in which agile players match product lines, pricing, and service models to local mobility realities across the Asia-Pacific Automotive Engine Oils Market.

Competitive Landscape

The Asia-Pacific Automotive Engine Oils Market is moderately consolidated. Strategic pivots increasingly revolve around electrified-fluid portfolios and digital fleet services. Shell’s Group III expansion and EV-fluid R&D (research and development) exemplify how incumbents retool assets for hybrid and battery-electric lubrication needs. M&A (merger and acquisition) appetite centers on additive makers and regional blenders that supply OEM factory-fill channels in high-growth clusters such as Vietnam and Indonesia. Simultaneously, capital spending on bio-lubricant pilot lines reflects a hedge against policy moves favoring renewable content. In this environment, sustained differentiation relies on integrating chemical innovation with service ecosystems that secure repeat business volumes across the Asia-Pacific Automotive Engine Oils Market.

Asia-Pacific Automotive Engine Oils Industry Leaders

ExxonMobil Corporation

Shell plc

BP p.l.c.

CNPC

China Petrochemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Shell India rolled out its revamped premium automotive engine oil, Shell Helix Ultra, tailored to align with the cutting-edge 2025 API SQ Standard. The company also introduced a striking new packaging design for its Shell Helix lubricant lineup, emphasizing a contemporary aesthetic.

- September 2024: PETRONAS Lubricants International (PLI) unveiled PETRONAS Nexta, a fresh line of engine oils. Tailored for Thailand's lubricant market, these oils promise premium performance without the premium price tag. Developed with cost-conscious drivers in mind, PETRONAS Nexta is a product from the company's Global Research and Technology Centre located in Turin, Italy.

Asia-Pacific Automotive Engine Oils Market Report Scope

By Resin Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

By Geography

| China |

| India |

| Pakistan |

| Bangladesh |

| Japan |

| South Korea |

| Taiwan |

| Australia |

| Malaysia |

| Indonesia |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Resin Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | China | |

| India | ||

| Pakistan | ||

| Bangladesh | ||

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Australia | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Asia-Pacific Automotive Engine Oils Market?

The market stands at 6.29 billion liters in 2026 and is projected to reach 6.56 billion liters by 2031, registering a 0.84% CAGR.

Which product category leads demand across Asia Pacific?

Passenger Car Motor Oil remains dominant with 48.92% share, though Motorcycle Engine Oil is expanding the quickest.

How is electric-vehicle adoption affecting lubricant suppliers?

Rising EV penetration trims traditional engine-oil volumes but opens opportunities in EV-specific thermal-management fluids and driveline lubricants.

Why are OEM factory-fill agreements strategic for lubricant companies?

Factory-fill contracts secure guaranteed volumes, embed lubricant brands into vehicle service schedules, and accelerate premium synthetic adoption.

Which countries are driving the next phase of demand expansion?

Vietnam, Indonesia, Thailand, and Malaysia show the strongest incremental growth due to vehicle-parc expansion and supportive industrial policies.

Page last updated on: