Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

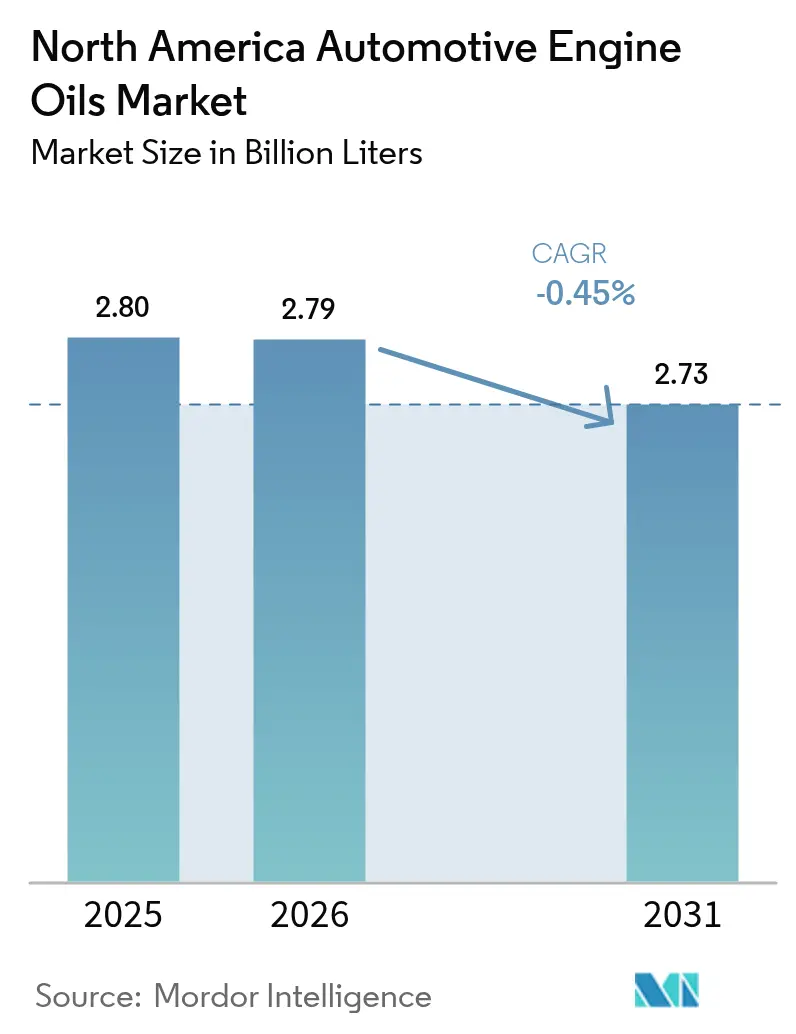

| Base Year Market Size (2025) | 2.80 Billion Liters |

| Market Volume (2026) | 2.79 Billion Liters |

| Market Volume (2031) | 2.73 Billion Liters |

| Growth Rate (2026 - 2031) | -0.45% CAGR |

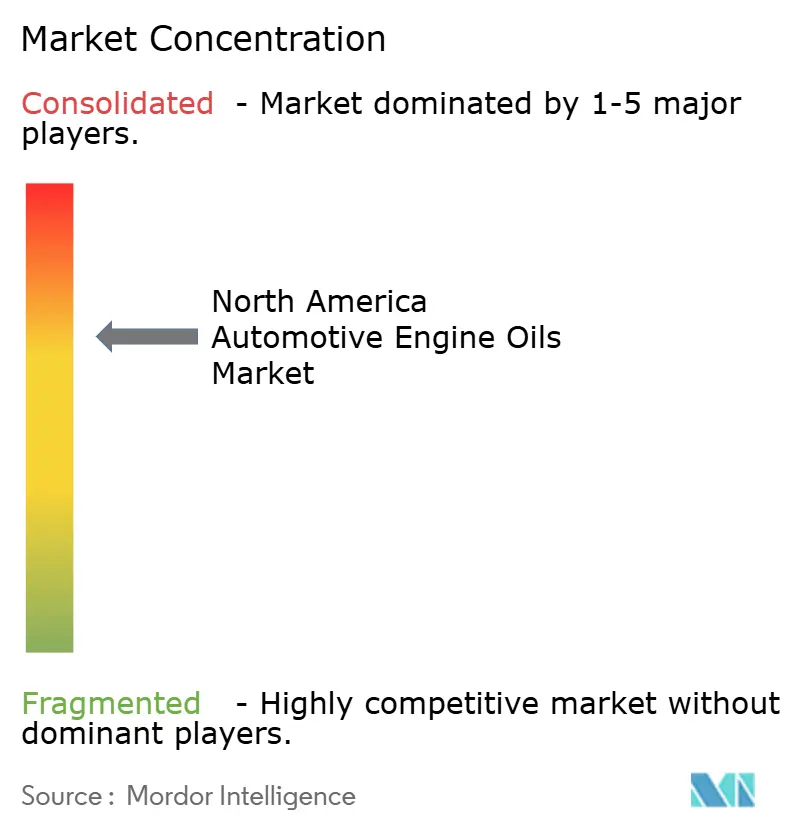

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Engine Oils Market Analysis by Mordor Intelligence

The North America Automotive Engine Oils Market size is expected to grow from 2.80 Billion Liters in 2025 to 2.79 Billion Liters in 2026 and is forecast to reach 2.73 Billion Liters by 2031 at -0.45% CAGR over 2026-2031. This negative growth trajectory is shaped by faster electrification, longer drain intervals, and rigorous CAFÉ and greenhouse-gas rules that collectively trim lubricant volumes while shifting demand toward premium synthetics. Regulatory actions, such as the Environmental Protection Agency’s 2027 heavy-duty standards, which require roughly 75% lower NOx and 50% lower particulate emissions, are prompting formulators to develop low-viscosity 0W-XX and 10W-30 products that improve fuel economy while reducing consumption per service. At the same time, the Department of Energy’s target of 55 million plug-in vehicles on US roads by 2032 materially erodes the internal-combustion parc, which has historically consumed the most engine oils. Against this backdrop, premium synthetic producers benefit from higher per-unit value, rapid OEM factory-fill transitions, and opportunities in re-refined base stocks that align with corporate ESG goals. Competitive intensity remains high as integrated oil majors, specialist blenders, and sustainability-focused newcomers all vie for a share in a shrinking market. Consolidation—epitomized by Aramco’s USD 2.65 billion purchase of Valvoline’s global products unit—illustrates the pivot toward scale efficiencies and portfolio focus amid structural headwinds.

Key Report Takeaways

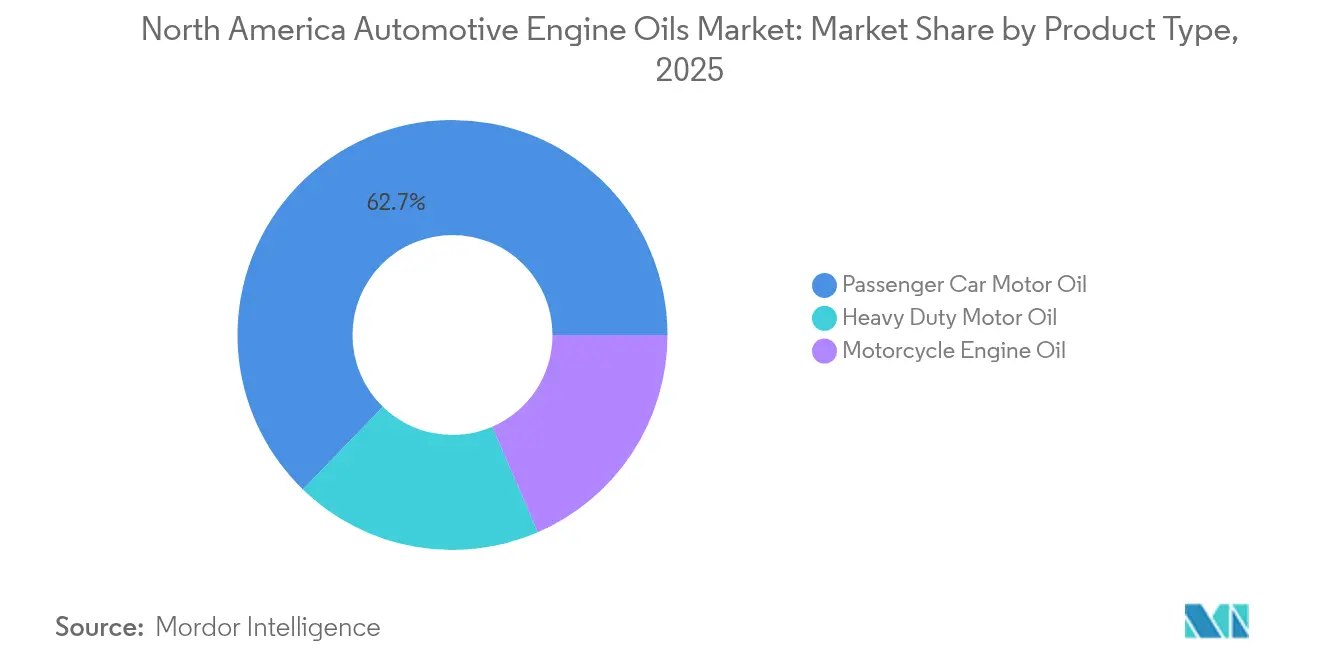

- By product type, passenger car motor oil led with 62.75% of the North America automotive engine oils market share in 2025. Motorcycle engine oil is forecast to record the mildest decline at a -0.35% CAGR through 2031.

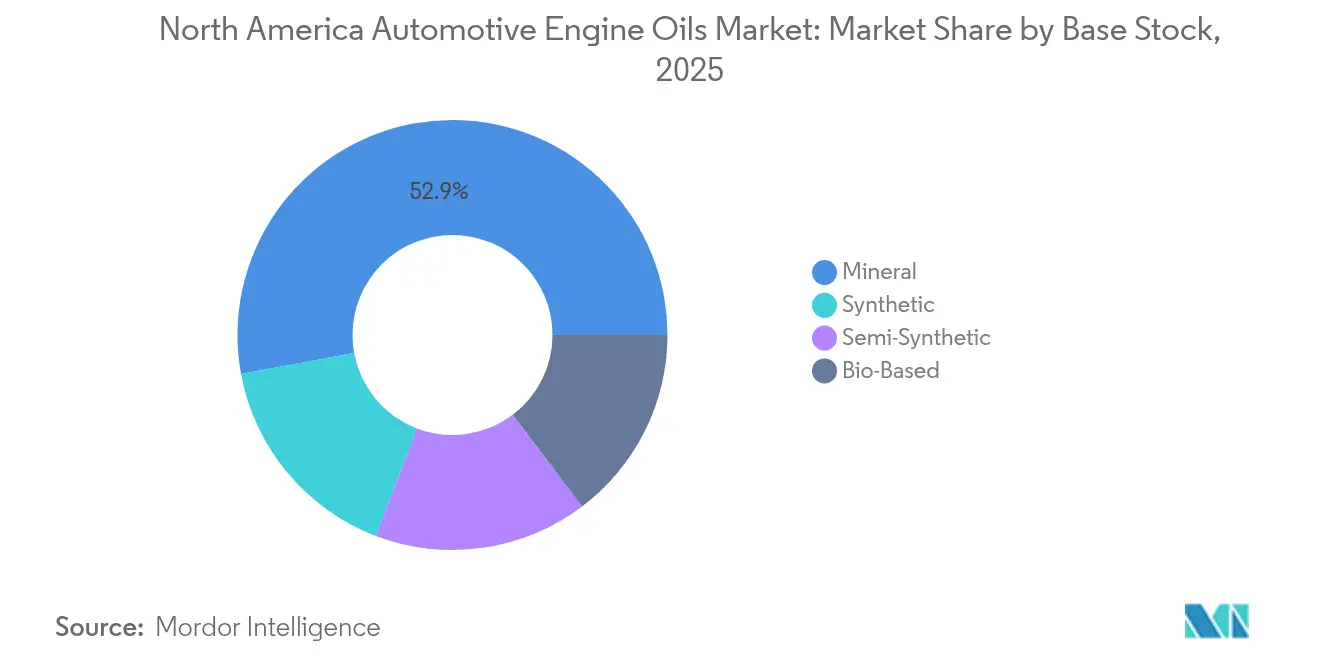

- By base stock, mineral oils accounted for 52.90% of the North America automotive engine oils market size in 2025, whereas full synthetics post the smallest drop at a -0.21% CAGR.

- By geography, the United States commanded 86.20% of the North America automotive engine oils market share in 2025, while Canada shows the slowest contraction at a -0.06% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening CAFÉ and GHG regulations driving demand for low-viscosity, high-performance oils | +0.8% | Global, with strongest impact in US and Canada | Medium term (2-4 years) |

| OEM factory-fill shift toward synthetics and 0W-XX grades | +0.6% | North America core, spill-over to Mexico | Long term (≥ 4 years) |

| Rising average vehicle age boosting aftermarket oil consumption | +0.4% | US and Canada primarily | Short term (≤ 2 years) |

| Growing ride-hailing and last-mile delivery fleet miles | +0.3% | Urban centers across North America | Medium term (2-4 years) |

| ESG-driven uptake of re-refined base-oil blends | +0.2% | US and Canada, early adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening CAFÉ and GHG Regulations Drive Premium Oil Demand

The Environmental Protection Agency’s Phase 3 greenhouse-gas program compels OEMs to cut heavy-duty CO₂ by roughly 50% by 2045, prompting lubricant makers to commercialize lower-viscosity PC-12 heavy-duty oils in 2026 that can unlock up to 3% fuel savings in fleet trials[1]Environmental Protection Agency, “Control of Air Pollution from New Motor Vehicles: Heavy-Duty Engine and Vehicle Standards,” epa.gov. Similar efficiency imperatives under ILSAC GF-7 for passenger cars are driving demand for 0W-16 and 0W-20 synthetics, which offer improved high-temperature shear stability. Field data from CITGARD tests confirm a 2.1% fuel-economy gain when fleets switch from 15W-40 to optimized 10W-30 formulations. As state and federal carbon-reduction policies converge, the regulatory cascade secures a durable premium segment, even as aggregate volumes decline. Blenders able to validate performance under the American Petroleum Institute’s new durability tests are positioned to capture share.

OEM Factory-Fill Synthetic Adoption Reshapes Product Mix

North American vehicle makers are embedding synthetic specifications in factory fill to meet warranty extensions and thermal load demands in turbocharged engines. General Motors’ dexos1 Gen3 specification imposes tighter sludge and LSPI limits, effectively standardizing the use of full synthetic 0W-20 or 5W-30 in new cars. In the heavy-duty sector, leading truck OEMs are now approving 10W-30 FA-4 oils, which is accelerating aftermarket acceptance. ExxonMobil forecasts 80% growth in high-value performance lubricants by 2030 and is expanding PAO output to support OEM partnerships. Synthetics command a higher price-mix even as drain intervals lengthen, cushioning revenue decline for suppliers with advanced base-stock capacity.

Rising Average Vehicle Age Boosts Aftermarket Consumption

The region’s average light-vehicle age rose to 12.6 years in 2025, the highest on record, a trend that keeps older engines in circulation longer and supports demand for higher-viscosity 5W-30 and 10W-40 grades formulated for wear control in legacy hardware. Independent repair shops report an increased use of high-mileage synthetics containing seal conditioners, while fleet operators retain trucks for longer depreciation cycles, which require incremental oil changes before retirement. Although electrification tempers long-term prospects, the near-term parc mix adds a modest uplift to lubricant-service occasions.

Growing Ride-Hailing and Last-Mile Delivery Miles

Urban mobility platforms and e-commerce logistics have expanded annual vehicle kilometers, particularly for light vans and hybrid sedans. Higher utilization translates to accelerated oil-change frequency even with extended-drain synthetics, offsetting part of the demand lost to efficiency gains. Major platform operators prescribe OEM-approved 0W-20 synthetics to minimize downtime, reinforcing premium-grade penetration. As last-mile fleets prioritize total cost of ownership, formulators that can document fuel economy and durability benefits capture contractual supply deals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV and hybrid penetration lowering oil demand | -1.2% | Global, with US leading adoption | Medium term (2-4 years) |

| Extended OEM drain-interval recommendations | -0.7% | North America and global markets | Short term (≤ 2 years) |

| Supply-chain pressure on API Group III/IV base stocks | -0.4% | Global supply chains affecting North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV and Hybrid Penetration Reduces Oil Demand

Plug-in sales reached new highs in 2024, and the Department of Energy projects 55 million EVs by 2032, displacing a substantial fraction of oil consumption. Hybrids still require lubricant, but at lower volumes because engines operate intermittently and at optimized loads. State-level zero-emission mandates—California’s Advanced Clean Cars II being a notable example—further compress the serviceable market. While new fluids for e-axles and thermal management emerge, fill-for-life designs and smaller sump volumes render these a fraction of traditional demand.

Extended OEM Drain-Interval Recommendations

As synthetic-technology resilience improves, automakers are pushing oil-change guidance from the traditional 5,000-mile regime to 10,000–15,000 miles for mainstream cars and up to 25,000 miles in select premium products from Castrol and Mobil 1[2]Castrol, “Edge Extended Performance Product Specifications,” castrol.com. On-board oil-life monitors refine intervals based on duty cycle, thereby reducing the need for aftermarket visits. Heavy-duty fleets deploying FA-4 synthetics achieve 70,000–100,000-mile drain intervals under oil-analysis programs, reducing annual lubricant needs per truck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Passenger Car Oils Lose Volume but Retain Value

Passenger car motor oil currently accounts for 62.75% of the total volume, yet the adoption of electric vehicles sets the segment on a downward slope. The North America automotive engine oils market recorded its peak PCMO consumption during 2019–2024, after which volumes started to shrink as battery-only cars expanded their share. Despite that contraction, synthetics aligned with ILSAC GF-7 continue to capture market share, allowing suppliers to defend their revenue. OEM factory-fill mandates for Dexos1 Gen3 and GF-7 spark stronger pull-through at dealerships, while quick-lube chains upsell 0W-20 full synthetic oils to maintain ticket size.

Heavy-duty motor oil ranks second by liters and benefits from freight growth, even as efficiency programs temper volume. Fleet pilots have shown that switching to new FA-4 10W-30 oils can unlock fuel-economy gains of 1–4%, supporting price premiums. Over the forecast period, motorcycle engine oil is expected to slip least, with a -0.35% CAGR, owing to the growing popularity of electric motorcycles, scooters, and e-bikes. Improvements in battery life, charging infrastructure, and overall performance have made electric two-wheelers a more affordable, practical, and attractive option for consumers.

By Base Stock: Synthetics Edge Ahead as Specifications Tighten

Mineral oils are expected to retain a 52.90% share in 2025, but every new vehicle entering service requires at least a synthetic blend, accelerating the shift. The North America automotive engine oils market size for mineral grades is projected to decline faster than the overall decline as environmental regulations cap VOC emissions from solvent-refined Group I production. Semi-synthetics remain a budget bridge product, mixing Group II with 10–30% Group III to hit mid-tier price points.

Full synthetics, powered by Group III and Group IV, achieve the shallowest drop at -0.21% CAGR to 2031. The demand for synthetic engine oil in North America is predicted to decline in the coming years, primarily due to the accelerated adoption of electric vehicles (EVs). Integrated producers Chevron and ExxonMobil leverage their GTL and PAO capacities to secure supply. CHEVRON.COM. Bio-based lubricants, although small, are gaining traction with municipal fleets seeking to reduce lifecycle carbon emissions by up to 50%. Castrol’s re-refined blends under the MoreCircular banner exemplify how ESG targets translate into purchasing criteria.

Geography Analysis

The United States dominates the North America automotive engine oils market, accounting for 86.20% of the 2025 volume. Federal CAFÉ standards and EPA Phase 3 rules require lower-viscosity formulations that enhance synthetic penetration while reducing liters. Domestic base-oil production from Baytown, Pascagoula, and Richmond refineries underpins supply security, though upcoming Group III investments lag Asian capacity builds. Connected-car data streams funnel service traffic to dealerships, pressuring independent quick-lube operators but opening channels for OEM-branded oils. State-level ZEV mandates accelerate electrification, reducing future demand while catalyzing the development of proprietary EV driveline fluids.

Canada, though smaller, contracts the least due to its severe winters, which necessitate premium 0W-20 and 5W-30 synthetics with pour points below -40°C. Rural resource-extraction vehicles and off-road machinery sustain diesel-engine oil volumes. Ottawa’s goal to sell only zero-emission light vehicles by 2035 coexists with heavy-duty exemptions in mining and forestry that still require high-TBN 15W-40 oils. Provincial VOC limits encourage low-sulfur base stocks, aligning with US formulations and enabling cross-border supply synergies.

Mexico contributes the smallest share but benefits from automotive manufacturing and a younger vehicle parc that continues to rely on internal-combustion powertrains. PEMEX’s Olmeca refinery brings 340,000 bpd of capacity that can back-integrate Group II base oils, reducing import reliance. Electrification adoption lags, affording mineral-oil volumes a longer runway. Nevertheless, planned alignment with US emissions regulations will progressively elevate synthetic demand over the next decade.

Competitive Landscape

The North America Automotive Engine Oils Market is consolidated. Competition centers on integrated majors—ExxonMobil, Chevron, Shell, and BP Castrol—leveraging crude-to-molecule scale, captive PAO/GTL assets, and direct OEM relationships. Their broad portfolios span PCMO, HDDO, and emerging EV fluids, enabling cross-segment resilience. API’s licensing framework and OEM approval matrices remain formidable entry barriers, but data-driven maintenance platforms and private-label programs furnish new avenues for challenger brands seeking share.

North America Automotive Engine Oils Industry Leaders

Chevron Corporation

ExxonMobil Corporation

Shell plc

BP p.l.c.

Saudi Arabian Oil Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TotalEnergies Marketing Canada Inc. announced a transition from mineral to a synthetic technology engine oil. TotalEnergies Marketing Canada showcased its comprehensive range of synthetic technology motor oils for both the light vehicle and heavy-duty markets.

- December 2024: The Carrera Panamericana, held in Mexico, concluded its 2024 edition, marking a collaboration with LIQUI MOLY as the official automotive engine oil partner of the event. The manufacturer conducted a range of promotional activities, including events at automotive workshops, retail stores, and car dealerships across the nation.

North America Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

By Geography

| United States |

| Canada |

| Mexico |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current volume of the North America automotive engine oils market?

The North America Automotive Engine Oils Market size is estimated at 2.79 Billion Liters in 2026, and is expected to decline to 2.73 Billion Liters by 2031.

How fast is the market expected to shrink?

Volume is forecast to decline at a -0.45% CAGR from 2026 to 2031.

Which product category retains the largest share?

Passenger car motor oil accounts for 62.75% of total volume in 2025.

Why are synthetics gaining mix even as overall liters fall?

OEM factory-fill mandates, extended drain intervals, and CAFÉ rules require the performance advantages of synthetic base stocks.

How will electrification affect lubricant demand by 2031?

Plug-in and hybrid adoption is projected to strip approximately 1.2 percentage points from the market CAGR, accelerating volume decline.

Page last updated on: