South Asia Automotive Engine Oils Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

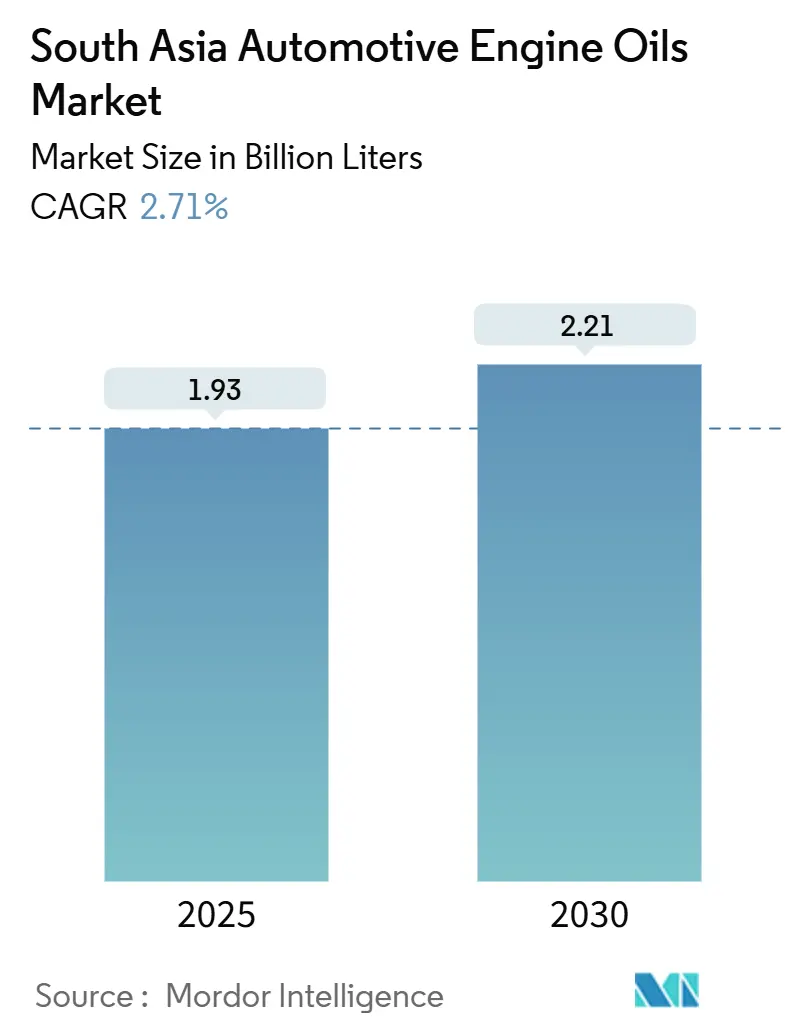

| Market Volume (2025) | 1.93 Billion liters |

| Market Volume (2030) | 2.21 Billion liters |

| Growth Rate (2025 - 2030) | 2.71% CAGR |

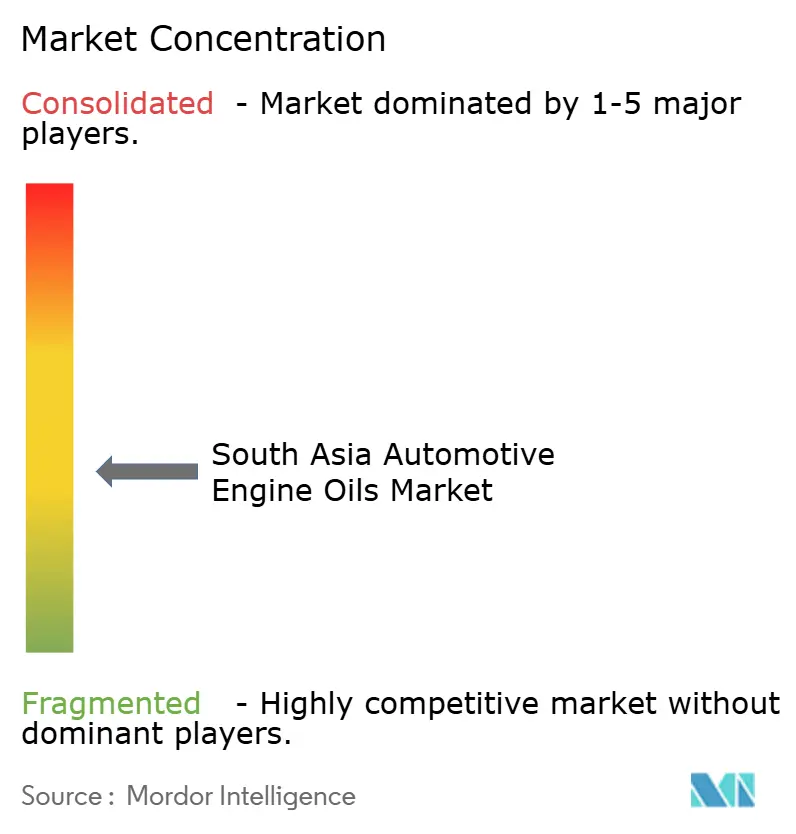

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Asia Automotive Engine Oils Market Analysis by Mordor Intelligence

The South Asia Automotive Engine Oils Market size is estimated at 1.93 billion liters in 2025, and is expected to reach 2.21 billion liters by 2030, at a CAGR of 2.71% during the forecast period (2025-2030). The vehicle parc is expanding across rural India and emerging urban centers, while commercial fleets operate longer hours, increasing lubricant throughput even as extended-drain synthetics gain market share. India’s 80.87% contribution anchors regional consumption, but Bangladesh’s double-digit demand growth and Pakistan’s post-stabilization recovery are widening the addressable base. Regulatory moves, such as BS-VI limits, raise viscosity index and low-SAP requirements, accelerating the adoption of premium synthetics, whereas cost-sensitive motorists still favor affordable mineral blends. Competitive tactics focus on refining integration, developing low-ash gas-engine oils for the growing CNG market, and offering value-added telematics services that offset drain interval extensions.

Key Report Takeaways

- By product type, passenger car motor oil led with a 51.34% share of the South Asia automotive engine oil market in 2024, whereas motorcycle engine oil is projected to register the fastest growth at a 2.88% CAGR from 2024 to 2030.

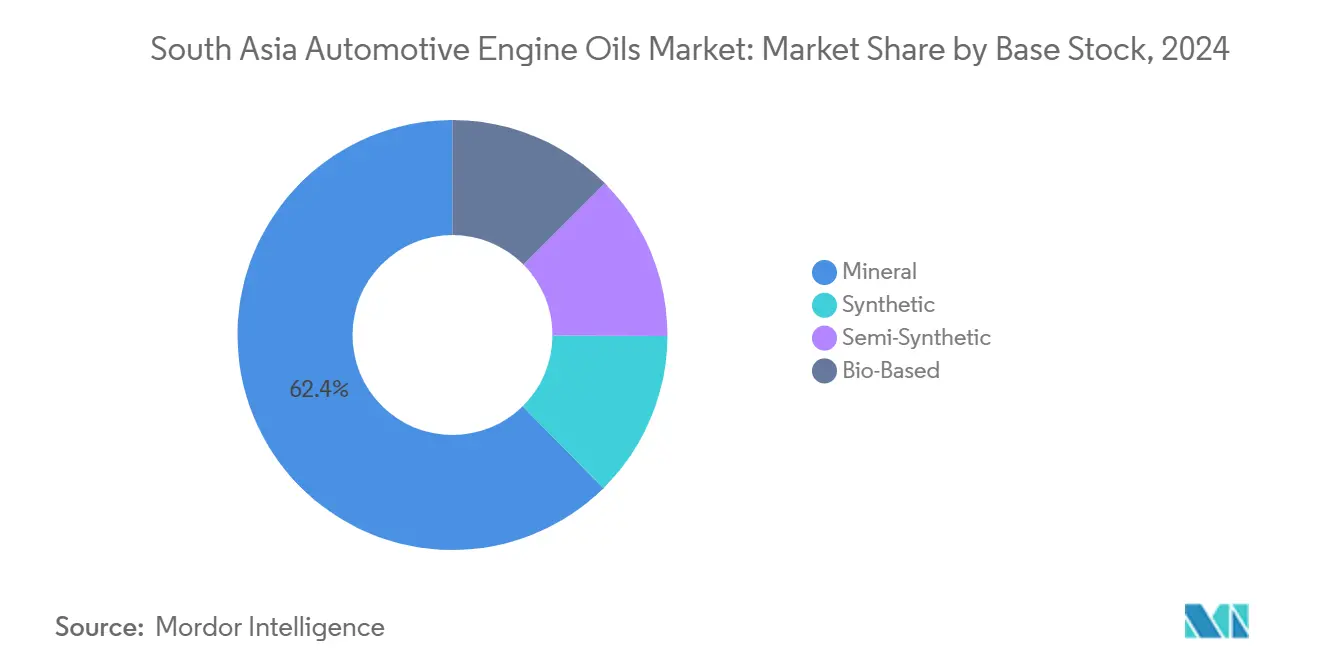

- By base stock, mineral oils accounted for 62.38% of the South Asia automotive engine oil market size in 2024, while synthetic grades are poised to grow at a 2.92% CAGR to 2030.

- By geography, India dominated the market with an 80.87% share in 2024 and is expected to expand at a 2.83% CAGR through 2030.

South Asia Automotive Engine Oils Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Passenger and two-wheeler parc expansion | +0.8% | India, Bangladesh, Pakistan core, spillover to Sri Lanka | Medium term (2-4 years) |

| Two and three-wheeler dominance fuels MCO demand | +0.6% | India, Bangladesh, Sri Lanka with high motorcycle density | Long term (≥ 4 years) |

| Intensifying commercial-freight and bus utilisation | +0.5% | India, Pakistan commercial corridors, Bangladesh ports | Short term (≤ 2 years) |

| E-commerce last-mile fleets shorten drain intervals | +0.4% | Urban India, Bangladesh, Sri Lanka metropolitan areas | Medium term (2-4 years) |

| CNG and RNG vehicle surge needs low-ash gas-engine oils | +0.3% | India, Pakistan with CNG infrastructure expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Passenger and Two-Wheeler Parc Expansion

India’s vehicle parc is on track to surpass 400 million units by 2030 as rural motorization expands, ensuring a robust volume base for the South Asian automotive engine oil market. Bangladesh consumed 165,000 tons of lubricants in 2024, driven by 12-15% annual growth in automotive demand, as motorcycle registrations accelerated. Sri Lanka’s fleet comprises 3.07 million motorcycles and 0.71 million passenger cars, highlighting a two-wheeler-centric mix that intensifies the drain frequency per liter of displacement. Pakistan’s production rebound after 2023 contractions is re-inflating local lubricant needs, while older vehicles across the region necessitate shorter service cycles, amplifying per-unit consumption. Rural roads, electrification projects, and micro-finance availability unlock fresh ownership pockets, widening geographic demand for both mineral and synthetic blends.

Two and Three-Wheeler Dominance Fuels MCO Demand

Motorcycle sales in India exceed 20 million units a year, each requiring tailored 4-stroke oils with friction-modifier additives distinct from PCMO blends. Sri Lanka’s two-wheeler preponderance tilts the South Asia automotive engine oil market toward higher-volume monograde and low-viscosity MCO products. Three-wheelers, vital for last-mile mobility in Bangladesh and Sri Lanka, impose harsh duty cycles that multiply oil-change counts. Price-sensitive riders still choose Group I mineral oils, yet demand for fuel-saving synthetics is rising in Tier 1 cities where heat stress and stop-go traffic degrade oils faster. Electric two-wheelers remain a minority because of charging gaps and upfront cost barriers, preserving combustion-engine lubricant relevance through the decade.

Intensifying Commercial-Freight and Bus Utilization

Logistics corridors in India operate around the clock, pushing heavy-duty diesel engines toward accelerated lubricant turnover. Bangladesh’s port complexes and Pakistan’s China-linked freight lanes raise annual mileage per truck, locking in resilient HDMO demand even as some fleets trial extended-drain synthetics. Bus electrification is nascent, so urban and intercity diesel fleets continue to rely on CI-4-PLUS and CK-4 oils. Fleet managers adopt telematics to balance uptime and oil health, but high engine loads offset lengthened change intervals. The net effect sustains volume gains for the South Asia automotive engine oil market despite gradual efficiency improvements.

CNG and RNG Vehicle Surge Needs Low-Ash Gas-Engine Oils

India aims to have 10,000 CNG stations by 2030 under GAIL's expansion plans, while Pakistan is expanding its gas-dispensing network to reduce liquid-fuel imports. Spark-ignited CNG engines require low-ash, phosphorus-limited oils that meet API CK-4 and OEM-specific natural-gas standards to safeguard three-way catalysts. Suppliers able to formulate dual-fuel-ready products capture premium margins as public-transport buses and light trucks switch to gaseous fuels. The specialized additive packs involved push per-liter prices higher, thereby elevating the revenue share for advanced formulations within the South Asian automotive engine oil market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV and e-2W penetration | -0.3% | India urban centers, Sri Lanka metropolitan areas | Long term (≥ 4 years) |

| Extended-drain synthetic oils cut per-vehicle litres | -0.2% | India premium segments, urban Bangladesh, Sri Lanka | Medium term (2-4 years) |

| Telematics-based predictive maintenance reduces oil changes | -0.2% | India commercial fleets, Pakistan freight corridors, Bangladesh ports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV and E-2W Penetration

Government incentives, GST rebates, and declining battery costs are stimulating the uptake of electric vehicles in Delhi, Bengaluru, and Colombo. Yet grid instability, range anxiety in freight duty cycles, and limited rural charging infrastructure temper the immediate threat to the South Asia automotive engine oil market. Heavy-duty electrification lags because the mass of batteries erodes payload economics, so diesel HDMO volumes remain stable over the medium term. Policy timelines suggest a gradual rather than abrupt displacement of combustion-engine oils, allowing suppliers to redeploy resources into thermal-management fluids and dedicated driveline lubricants.

Telematics-Based Predictive Maintenance Reduces Oil Changes

Connected-vehicle platforms track engine load, soot, and viscosity index in real-time, allowing fleet managers to defer oil service until laboratory data indicate a threshold has been breached. Early adopters include Indian e-commerce couriers and Pakistani cross-border bulk carriers. Reduced unproductive workshop visits cut HDMO volumes, yet lubricant suppliers are bundling analytics packages with branded oils, preserving customer engagement and offsetting volume attrition through higher per-service value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Holds the Volume Crown as MCO Surges Ahead

Passenger car motor oil accounted for 51.34% of the South Asian automotive engine oil market in 2024, driven by new model introductions and longer average trip lengths. The adoption of BS-VI-compliant low-viscosity grades, such as 0W-16, is increasing as OEMs pursue fuel-economy credits. Meanwhile, motorcycle engine oil volumes grew at a 2.88% CAGR and are slated to overtake PCMO beyond 2030 if two-wheeler sales trajectories persist. Shared-mobility bike fleets in Dhaka and Bengaluru, which clock high mileage under harsh conditions, refresh oil every 3,000-4,000 km, amplifying per-unit consumption despite smaller sump capacities.

The market is witnessing rapid formulation upgrades, from JASO MA2 friction standards to zinc-dialkyldithiophosphate reinforcement for oxidation resistance under high rev conditions. Synthetic-blend MCOs are gaining shelf space in organized retail as urban riders perceive tangible cold-start smoothness and marginal fuel-saving benefits. Public transport authorities still mandate semi-annual oil changes regardless of predictive health data, keeping baseline demand buoyant.

By Base Stock: Mineral Dominance Persists, but Synthetics Capture the Upside

Mineral oils retained a 62.38% share in 2024, reflecting entrenched consumer price sensitivity across South Asia. The South Asia automotive engine oil market volumes are projected to increase at a 2.92% CAGR by 2030, as BS-VI and OEM warranty conditions encourage the adoption of low-viscosity oils. Refinery modernization programs are critical. Indian Oil’s investment in a 25% capacity expansion and a re-refined base-oil pilot aligns with national circular economy policies[1]Indian Oil Corporation, “R&D and Sustainability Report 2025,” iocl.com. BPCL’s expansion to 45 million tons/annum by 2029 will increase domestic Group II output, reducing reliance on imports. Suppliers integrate ester and poly-alkylene glycol chemistries for extreme-temperature resilience, positioning premium synthetics at double the per-liter value of mineral grades and providing revenue insulation against volume dilution within the South Asia automotive engine oil market.

Geography Analysis

India accounted for an 80.87% share in 2024, reflecting unmatched vehicle parc depth, multi-brand service networks, and integrated refining infrastructure. India’s automotive engine oil volumes are projected to post a 2.83% CAGR during 2025-2030. Government BS-VI norms drive a shift from 20W-40 to 10W-30 and 0W-20 viscosities, raising additive treat-rates and boosting per-liter value. The South Asia automotive engine oil market size attributable to India will therefore outpace wider regional GDP growth as rural disposable income lifts passenger-car ownership. In Bangladesh, international brands partner with local blenders to navigate a 32% import duty on finished lubricants, stimulating in-country investments in additives and packaging that deepen market penetration.

Pakistan’s recovery from 2023 currency shocks restores import letters of credit, allowing OEM assembly plants to ramp up output and revive lubricant pull-through. CNG accounts for one-third of Pakistani passenger-vehicle fuel, spurring demand for low-ash gas-engine oils compatible with three-way catalysts. Sri Lanka targets USD 2 billion in vehicle exports by 2030, positioning local assemblers as captive lubricant customers. Lanka IOC operates a 60,000 tpa blending plant that supplies both domestic and export channels, thereby cementing a resilient supply chain[2]Lanka IOC PLC, “Lubricant Operations Fact Sheet 2025,” lankaioc.com .

Competitive Landscape

State-owned majors such as Indian Oil Corporation control crude-to-can value chains, providing cost leverage through captive base-oil production and nationwide retail footprints. Indian Oil’s SERVO brand caters to multi-tier segments, ranging from mineral PCMO packs retailing at INR 300 per liter to PAO-based synthetics at INR 1,200. International players capitalize on performance niches. Suppliers are increasingly bundling field-testing, oil-analysis kits, and telematics dashboards, competing on service rather than just liters in the South Asian automotive engine oil market. Local independents expand through motorcycle-centric SKUs and rural penetration via agricultural-input dealers. Private-label and counterfeit risks persist in price-sensitive micro-markets, prompting major brands to roll out QR-coded tamper-proof packaging. Competitive intensity is thus moderate, with brand equity and distribution reach trumping pure price play.

South Asia Automotive Engine Oils Industry Leaders

Indian Oil Corporation Ltd

Shell plc

BP p.l.c.

Exxon Mobil Corporation

Bharat Petroleum Corporation Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Castrol India launched API SQ-ready Castrol MAGNATEC, the first domestically blended oil to meet the latest passenger-car specification, supporting the ‘Made in India’ agenda.

- April 2024: Shell India unveiled upgraded Shell Advance motorcycle oils with flexi-molecule chemistry and confirmed plans for 10,000 EV chargers by 2030 alongside development of next-gen battery-coolant fluids.

South Asia Automotive Engine Oils Market Report Scope

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| India |

| Bangladesh |

| Sri Lanka |

| Pakistan |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | India | |

| Bangladesh | ||

| Sri Lanka | ||

| Pakistan | ||

Key Questions Answered in the Report

What volumes does the South Asia automotive engine oil market currently represent?

The market stood at 1.93 billion liters in 2025 and is projected to reach 2.21 billion liters by 2030.

Which product category is expanding fastest in South Asia?

Motorcycle engine oil leads growth at a 2.88% CAGR, assisted by the region’s dominant two-wheeler parc.

How large is India’s contribution to regional demand?

India accounts for roughly 80.87% of total 2024 volumes, reflecting its 400-million-plus vehicle parc.

What impact do CNG vehicles have on lubricant formulation?

Spark-ignited CNG engines require low-ash oils to protect catalysts, opening higher-margin niches for specialized suppliers.

How will electric vehicles influence future engine-oil volumes?

BEV adoption will trim long-term growth, but limited charging infrastructure and cost barriers mean combustion-engine oils remain critical through the decade.

Page last updated on: