Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

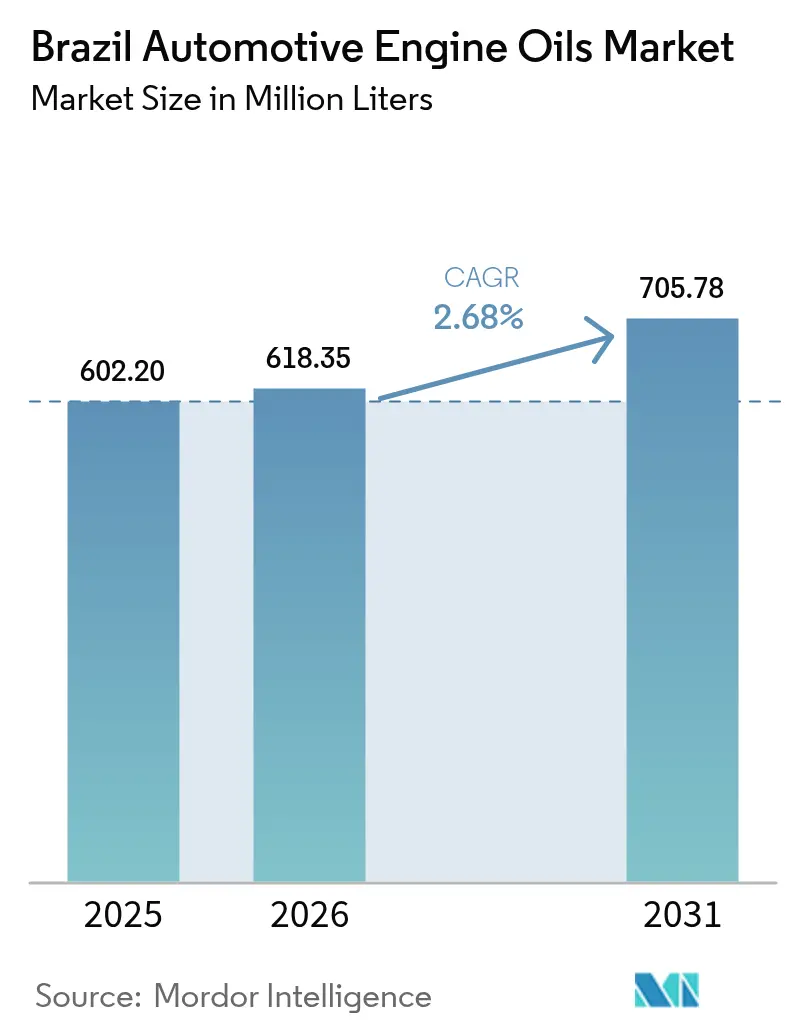

| Base Year Market Size (2025) | 602.20 Million Liters |

| Market Volume (2026) | 618.35 Million Liters |

| Market Volume (2031) | 705.78 Million Liters |

| Growth Rate (2026 - 2031) | 2.68% CAGR |

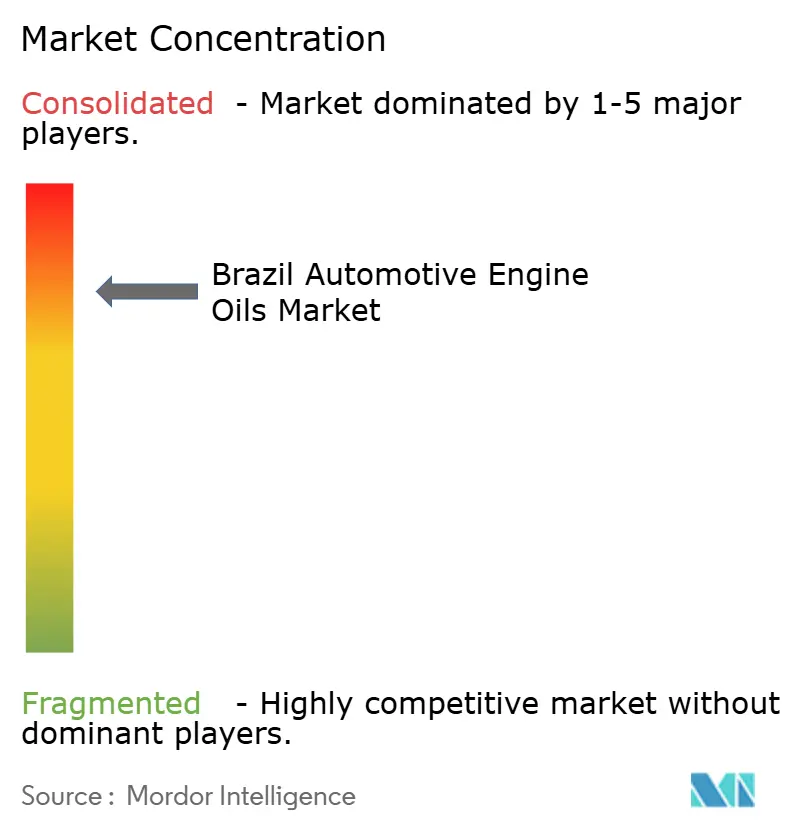

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Automotive Engine Oils Market Analysis by Mordor Intelligence

Brazil Automotive Engine Oils Market size in 2026 is estimated at 618.35 million liters, growing from 2025 value of 602.20 million liters with 2031 projections showing 705.78 million liters, growing at 2.68% CAGR over 2026-2031. Over the outlook period, demand resilience stems from the country’s large flex-fuel light-vehicle fleet, an ageing parc that needs more frequent oil changes, and stricter PROCONVE L7/L8 emission rules that accelerate the shift toward synthetic formulations. Mineral oils still dominate volumes yet value migrates toward synthetics as OEMs extend drain intervals and install after-treatment hardware that low-SAP formulations protect. E-commerce platforms reduce intermediary mark-ups and allow lubricant marketers to reach urban riders directly, while freight activity along agricultural corridors supports heavy-duty demand despite biodiesel blending challenges. Competitive intensity remains high because incumbents expand vertically integrated base-oil capacity and digital distribution capabilities to defend share in the Brazil automotive engine oils market.

Key Report Takeaways

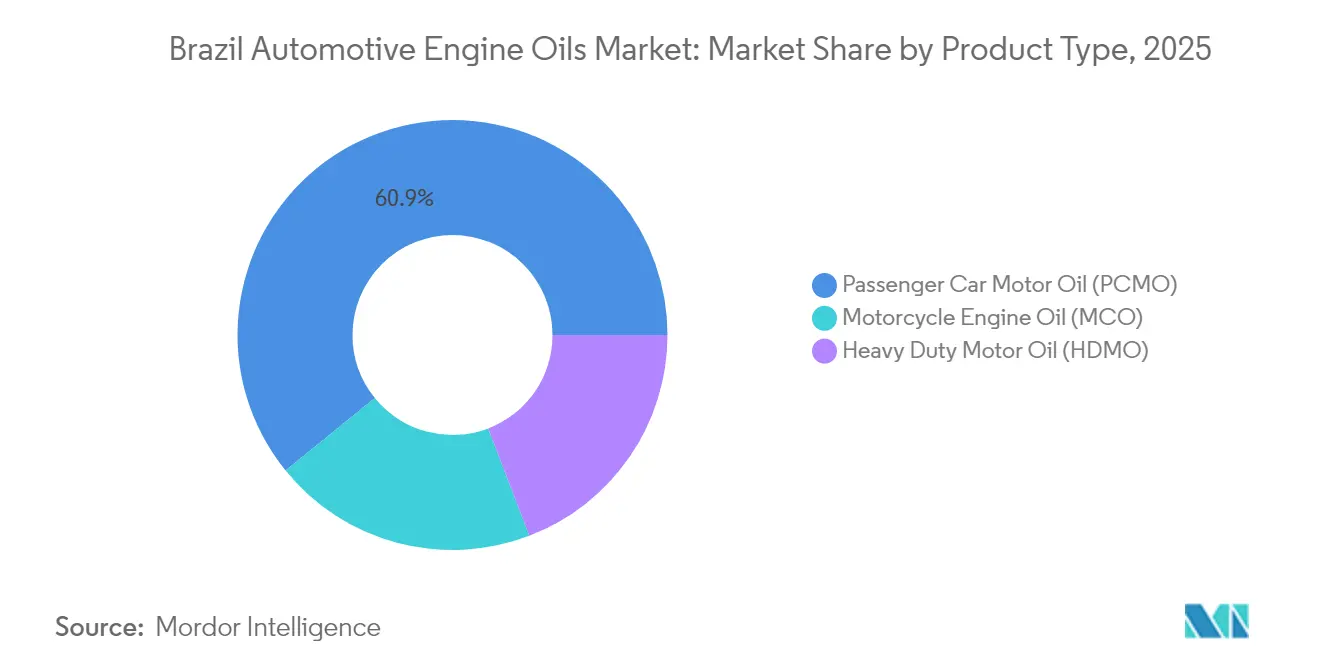

- By product type, passenger car motor oil held 60.85% of the Brazil automotive engine oils market share in 2025. Motorcycle engine oil is projected to expand at a 2.83% CAGR through 2031, the fastest among all product categories.

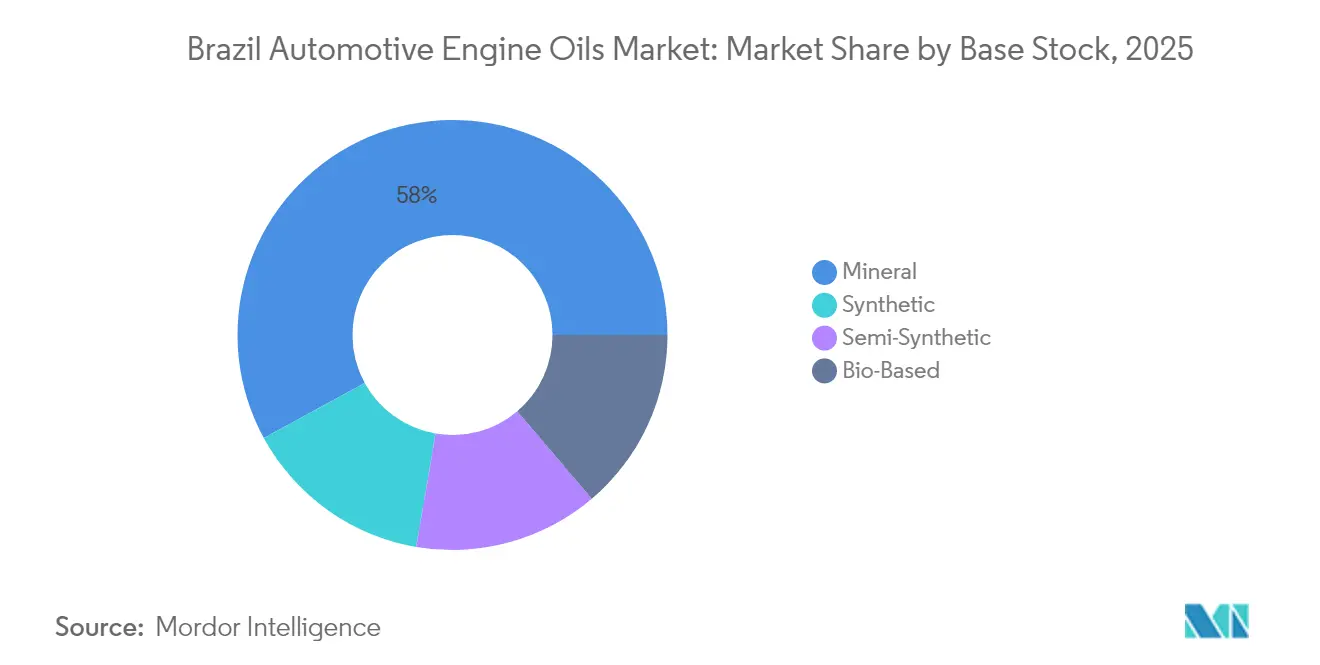

- Mineral formulations commanded 57.95% share of the Brazil automotive engine oils market size in 2025. Synthetic base oils are forecast to record a 2.96% CAGR between 2026 and 2031, outpacing every other base-stock type.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid ageing vehicle parc and higher average mileage | +0.80% | National, concentrated in Southeast and South regions | Medium term (2-4 years) |

| Stricter PROCONVE-L7/L8 emission norms raising need for low-SAP and synthetic oils | +0.60% | National, with early adoption in São Paulo and major urban centers | Short term (≤ 2 years) |

| Growth of e-commerce and quick-commerce lubricant retail channels | +0.40% | Urban centers, particularly São Paulo, Rio de Janeiro, and Belo Horizonte | Medium term (2-4 years) |

| Macroeconomic recovery boosting long-haul freight movement | +0.50% | National, with emphasis on freight corridors connecting Southeast to Northeast | Short term (≤ 2 years) |

| Ride-hailing fleet service contracts that mandate premium drain-interval lubricants | +0.30% | Metropolitan areas, São Paulo and Rio de Janeiro leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Ageing Vehicle Parc Drives Premium Lubricant Demand

Brazil’s light-vehicle fleet continues to age as new-car affordability weakens. Engines with higher mileage lose tighter clearances and operate under greater thermal stress, thereby consuming more oil per kilometer. Flex-fuel operation amplifies wear because ethanol attracts moisture and burns at higher temperatures. Workshops and fleet managers consequently specify synthetic or semi-synthetic blends that maintain viscosity, mitigate gasket hardening, and stretch drain intervals to offset rising labor costs. These practices underpin incremental volume as well as premiumization within the Brazil automotive engine oils market.

PROCONVE L7/L8 Standards Accelerate Synthetic Oil Adoption

The shift from L7 to L8 emission stages, effective January 2025, cuts NOx + NMOG limits from 80 mg/km to 50 mg/km nationwide, with another tightening to 30 mg/km in 2029. Diesel particulate filters, SCR units, and longer durability mandates create a lubricant performance envelope that conventional mineral stocks cannot satisfy. Oil marketers must deliver low-SAP packages that guard after-treatment catalysts over 160,000 km or 10 years. This regulatory inflection propels synthetic penetration and lifts the value per liter in the Brazil automotive engine oils market.

E-commerce Channels Transform Distribution Economics

Digital platforms lower barriers between blenders and end users. Vibra Energia launched a standalone online lubricants division in October 2025 to capture shoppers who bypass traditional fuel-station retail. Subscription models, smaller pack sizes, and gig-economy partnerships such as Petronas-iFood give marketers granular access to an estimated 70,000 São Paulo couriers. These couriers represent a dense cluster of repeat purchasers whose daily mileage accelerates oil-change frequency and cements predictable throughput for the Brazil automotive engine oils market.

Macroeconomic Recovery Amplifies Freight Transport Demand

Moderating inflation and infrastructure spending revive agricultural exports, boosting diesel consumption along the Midwest-to-coast freight axis. Extended highway runs favor high-TBN, shear-stable synthetics that can safely double historical drain intervals to 20,000 km on Euro-VI trucks. Petrobras and Amazon Brazil have also announced joint work on low-carbon fuels, yet ICE trucks will dominate freight for the foreseeable future, sustaining HDMO volumes in the Brazil automotive engine oils market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended OEM drain intervals for Euro-VI compliant engines | -0.40% | National, with concentration in commercial vehicle fleets | Medium term (2-4 years) |

| Weak new-vehicle sales amid high interest-rate cycle | -0.30% | National, with particular impact in Northeast and North regions | Short term (≤ 2 years) |

| Accelerating BEV and hybrid penetration in urban centres | -0.20% | São Paulo, Rio de Janeiro, and other major metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extended Drain Intervals Reduce Volume Consumption

Euro-VI hardware enables 20,000 km oil-change schedules on commercial trucks compared with legacy 15,000 km intervals. This interval stretch directly trims litres per vehicle. Although synthetics carry higher margins, unit volume loss partially offsets revenue gains for suppliers in the Brazil automotive engine oils market. Fleet owners prioritize total cost of ownership, pressuring blenders to justify price premiums on oxidation stability and soot dispersion performance[1]ResearchGate, “Extended Drain Interval Feasibility on Euro VI Trucks,” researchgate.net .

Interest-Rate Headwinds Constrain New-Vehicle Sales

The policy Selic rate climbed to 12.25% in 2025 and is projected to hit 13.50% before year-end. Tight credit suppresses showroom traffic, especially in price-sensitive regions such as the Northeast. Fewer registrations translate into smaller factory-fill requirements and slower replenishment demand during warranty periods, tempering near-term growth of the Brazil automotive engine oils market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Motorcycle Oils Drive Growth Despite PCMO Dominance

The motorcycle segment accounts for 1,748,317 units produced in 2024, an 11.1% year-over-year increase that underpins 2.83% CAGR volume expansion for MCO in the Brazil automotive engine oils market. This surge is anchored in last-mile delivery demand that pushes riders beyond factory drain intervals within months, motivating upgrades to semi-synthetic 10W-40 formulations that withstand ethanol dilution and high-RPM shear. Passenger Car Motor Oil still dominates at 60.85% of 2025 volume, reflecting a 33-million-unit light-vehicle parc spread across urban and rural Brazil. PCMO consumption plateaus, but flex-fuel engine chemistry keeps value elevated due to the need for superior oxidation control and corrosion inhibition.

Heavy-Duty Motor Oil volumes grow in tandem with freight activity along the Midwest-Southeast export route, yet interval extension offsets part of that uplift. Fleet trials confirm 20,000 km drains on CK-4 15W-40 synthetics, which trims top-up frequency. The Brazil automotive engine oils market consequently rebalances toward higher-margin SKUs even as litre growth moderates. Blenders that tailor additive chemistries for biodiesel blends up to B20 safeguard injector cleanliness and cylinder wear, preserving share in this critical product class.

By Base Stock: Synthetic Growth Outpaces Mineral Dominance

Mineral oils contributed 57.95% of national consumption in 2025 and were the largest absolute pool within the Brazil automotive engine oils market. However, synthetic volumes climb at a 2.96% CAGR as PROCONVE L8 drives demand for uniform molecular structures that resist oxidation under high-temperature duty cycles. Petrobras is installing 12,000 barrels per day of Group II capacity at Projeto Refino Boaventura, signaling domestic alignment with this performance migration. Semi-synthetic blends remain the value bridge for price-sensitive motorists who seek partial synthetic benefits without full premium costs.

Bio-based stocks derived from castor oil exhibit a 20% lower friction coefficient than SAE 20W-50 mineral benchmarks, offering an indigenous sustainability pathway. Lab-scale results encourage incremental adoption by fleet owners aligned with corporate ESG commitments. As B15 diesel blends roll out in August 2025, formulations need stronger solvency control to mitigate ester-based fuel degradation. Synthetic and semi-synthetic bases meet this challenge better than mineral equivalents, reinforcing their trajectory within the Brazil automotive engine oils market.

Geography Analysis

Regional consumption skews toward the Southeast, which holds more than half of national lubricant volumes thanks to vehicle density, industrial GDP, and concentrated logistics hubs. São Paulo alone operates the world’s largest flex-fuel fleet, a factor that shapes additive demand profiles notably different from gasoline-only territories. Elevated ethanol penetration increases engine temperatures, requiring oils with robust antioxidant packages, which positions synthetics for faster adoption in this part of the Brazil automotive engine oils market.

The Northeast records the highest forecast growth through 2031 as infrastructure initiatives open new freight corridors. Diesel fleets in this region historically run longer between services due to sparse workshop networks, so they benefit disproportionately from CK-4 and FA-4 synthetics that sustain viscosity. Retail channel fragmentation in smaller cities creates opportunity for e-commerce fulfillment models that bypass brick-and-mortar shortages and expand reach for the Brazil automotive engine oils market.

Northern territories rely on river transport, yet motorcycle usage is rising within Manaus and Belém. The Polo Industrial de Manaus hosts major motorcycle assembly operations that secure factory-fill contracts locally, boosting MCO volumes. High humidity accelerates oil degradation, reinforcing the switch to sealed synthetic bottles that resist moisture ingress. Although absolute demand remains lower than the Southeast, tailored distribution and climate-specific product mixes safeguard future share for the Brazil automotive engine oils market.

Regulatory Landscape

Brazil regulates automotive engine oils primarily through the Agencia Nacional do Petroleo, Gas Natural e Biocombustiveis (ANP), which requires prior product registration and specification control for finished lubricants under Resolucao ANP No. 804/2019. Registration covers product identity (including viscosity grade and brand) and Portuguese labeling, and ANP enforces compliance through periodic quality monitoring that compares market samples against the registered specifications at its CPT laboratory. This raises the bar for low-SAP and performance-aligned formulations as PROCONVE L7/L8 vehicle requirements tighten from January 2025.

Environmental obligations also shape market conduct via CONAMA Resolucao 362/2005, which mandates collection and proper destination of used or contaminated lubricating oil (OLUC) and prohibits improper disposal. OLUC collection targets are defined through interministerial instruments, including Portaria Interministerial MMA/MME No. 475/2019, and are monitored by bodies such as IBAMA and ANP. As a result, lubricant producers, importers, distributors, and collectors need to formalize reverse logistics and supporting documentation as part of go-to-market execution in Brazil.

Value Chain Analysis

The Brazil automotive engine oils value chain starts with base oil supply (domestic refining and imports) and additive procurement, then moves to blending or formulation, packaging, and route-to-market through distributors, fuel-station networks, workshops, retail, and fast-growing online channels. ANP influences decisions across this chain because finished lubricants must be registered before commercialization (Resolucao ANP No. 804/2019) and base oils are governed by technical specifications under ANP rules, including Resolucao ANP No. 911/2022. For producers and importers, technical documentation and batch discipline are therefore core operating requirements.

Downstream, large distributors and fuel retailers, supported by associations such as SINDICOM, provide reach into both passenger and commercial service points. ANP's Lubricant Monitoring Program (PML) adds ongoing surveillance, increasing the cost of non-compliance for informal supply. In parallel, CONAMA 362/2005 requires OLUC collection and appropriate final destination, so distributors and marketers rely on partnerships with collectors and re-refiners to meet collection targets and maintain license-to-operate, especially where workshop density and collection logistics vary across regions.

Competitive Landscape

Market concentration is highly consolidated. Petrobras, through its Lubrax brand, leverages a fuel-station footprint approaching 8,200 retail sites to cross-sell motor oils. The company’s BRL 9.6 billion Group II expansion enhances in-house feedstock security and allows tighter quality control, solidifying leadership in the Brazil automotive engine oils market. Iconic Lubrificantes distributes Chevron Oronite’s OLOA additive packages, giving it advanced formulation capabilities that comply with PROCONVE L8 and Euro VI specifications.

International firms adapt strategies to local biofuel chemistry. Shell markets low-SAP HX8 synthetics tested on B15 diesel and high-ethanol blends, while TotalEnergies divested downstream fuel assets to focus on higher-margin lubricants. Vibra Energia created a dedicated lubricants division led by Marcelo Bragança to accelerate e-commerce penetration. Petronas secures brand presence through its partnership with iFood, providing discounted packs to couriers who ride beyond 200 km daily, evidence of niche digital engagement in the Brazil automotive engine oils market.

Disruption looms from bio-based entrants that exploit castor and soybean feedstocks. Research institutes collaborate with private blenders to scale pilot production, and early customer trials signal acceptable oxidative stability under Brazilian climatic stress. These initiatives could shift differentiation away from purely synthetic versus mineral framing toward carbon-intensity metrics. Established players therefore invest in circular-economy programs, such as closed-loop used-oil collection, to reinforce ESG credentials and maintain loyalty in the Brazil automotive engine oils market.

Brazil Automotive Engine Oils Industry Leaders

Cosan S.A. (Moove/Ipiranga)

Exxon Mobil Corporation

Petrobras

Shell plc

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An actionable opportunity is upgrading the national product mix toward registered, compliant low-SAP and higher-performance formulations that align with newer emissions and durability requirements. ANP registration under Resolucao ANP No. 804/2019 links commercialization to declared specifications and ongoing monitoring. OEM-linked service networks also concentrate demand for approved engine oils: Stellantis and Shell expanded their partnership to cover Citroen and Peugeot in Brazil, extending the Mopar Oil by Shell program across additional brands for factory fill and authorized service usage. This broadening supports premium PCMO grades and service-fill programs through OEM-controlled channels.

On the supply side, capacity and efficiency programs announced by major players support localized production and distribution for higher-value formulations. Petrobras included a 12,000 bpd increase in Group II base oil production at the Boaventura Energy Complex in its 2025-2029 plan. Fuchs also advanced a new blending facility in Sorocaba (Sao Paulo), with a stated 50,000 tonnes/year capacity and investment above R$ 220 million. Vibra Energia completed a R$ 100 million expansion at its Duque de Caxias plant, raising capacity from 300 million to 460 million liters/year, and Iconic initiated a R$ 250 million investment program through end-2026 focused on capacity, operational efficiency, and sales-channel growth. Together, these moves create whitespace for suppliers that can secure consistent base-oil sourcing, maintain ANP-compliant registrations, and meet faster delivery needs for workshops and e-commerce buyers.

Recent Industry Developments

- April 2026: Brazil lubricant demand remained elevated, with reported monthly volumes exceeding 130,000 cubic meters amid high procurement following a multi-year peak in March. Sustained off-take supports tighter supply planning for blenders and distributors and increases the importance of dependable base-oil and additive sourcing for engine-oil product lines.

- March 2026: Stellantis expanded its partnership with Shell in Brazil to include Peugeot and Citroen, extending the Mopar Oil by Shell program across additional brands for factory fill and authorized service networks. The broader OEM-linked channel strengthens branded engine-oil pull-through in the aftermarket and raises the bar for spec compliance and service-fill availability.

- June 2024: FUCHS introduced TITAN CARGO PRO 15C140 SAE 0W-20, developed for Daimler Trucks engines such as Mercedes-Benz AROCS and ACTROS II that meet Euro VI-d and Euro VI-e requirements. The launch highlights the shift toward low-viscosity, high-performance heavy-duty formulations that protect after-treatment systems and support extended drain strategies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Brazil automotive engine oils market includes finished engine oils used in on-road vehicles, and it is sized on the volume of product sold and consumed within Brazil.

Scope exclusions: We exclude industrial lubricants, hydraulic and transmission fluids, greases, and other non-engine oil lubricant categories, even if they are sold through similar channels.

Segmentation Overview

- By Product Type

- Passenger Car Motor Oil (PCMO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- Monogrades

- Other Grades

- Heavy Duty Motor Oil (HDMO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- Monogrades

- Other Grades

- Motorcycle Engine Oil (MCO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- Monogrades

- Other Grades

- Passenger Car Motor Oil (PCMO)

- By Base Stock

- Mineral

- Synthetic

- Semi-Synthetic

- Bio-Based

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the vehicle and maintenance context in Brazil, and then narrowing it to engine oil consumption patterns. We rely on public datasets and standards sources such as Brazil's ANP publications, IBGE statistics, foreign trade summaries from MDIC, and technical standards from API and SAE that help align viscosity and performance grade definitions.

To make the model practical, we also review association and regulatory publications, along with OEM maintenance guidance, to understand drain intervals and how they shift with newer engines. Company filings, investor presentations, and reputable press are used to cross-check capacity changes and product mix, and then paid subscriptions for company financials and lubricants-specific market information are used as consistency checks where public detail is thin. The sources named above are illustrative, and many other public and paid references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating how engine oil demand is formed in Brazil, and where desk sources can mislead due to mix changes across passenger cars and heavy duty fleets. We spoke with a spread of blenders, distributors, workshop networks, and fleet and retail channel participants to confirm drain intervals, packaging mix, and how price changes were passed through across regions inside the country.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 18% | |

| Mid tier: 53% | Functional/Unit leaders: 30% | |

| Smaller Players: 18% | Managers: 52% |

Market-Sizing & Forecasting

Sizing is built mainly using a top-down demand pool, where the vehicle parc by type is linked to typical oil fill volumes and service intervals, which are then adjusted for usage intensity and maintenance behavior in Brazil. To keep totals realistic, we corroborate the demand pool with selective bottom-up checks, such as channel roll ups and sampled liters per oil change across workshop and retail routes, and then we correct for gaps where one channel is under-represented.

Key inputs that steer the model include vehicle parc and annual utilization, average oil change frequency, the split between passenger cars and commercial vehicles, the share of synthetic and semi-synthetic grades, and the balance of packaged versus bulk sales because it changes apparent consumption in channel data. For forecasting, scenario analysis is used around macro and auto indicators, and then the near-term path is anchored with exponential smoothing on historical consumption patterns, before assumptions are finalized through expert feedback on fleet growth and drain interval trends.

Data Validation & Update Cycle

Outputs are checked against independent signals, including lubricants consumption cues, vehicle parc shifts, and channel movement indicators, and then variances are investigated before sign-off. When a mismatch appears, we revisit assumptions, re-check unit conversions, and re-contact relevant respondents to confirm whether the change came from mix shifts, pricing pass-through, or a temporary demand spike.

The model is reviewed in multiple steps by analysts, followed by a final consistency pass before publication. Reports are refreshed annually, and interim updates are done when material events occur, such as regulation changes, major capacity additions, or visible shifts in vehicle activity.

Mordor Intelligence's Brazil Automotive Engine Oils Market Estimate Compared With Other Published Estimates

It is common to see different market sizes for Brazil automotive engine oils, even when the topic sounds identical, because the unit of measure, included product set, and the timing of the year used in the calculation are not always aligned. Gaps also show up when some sources translate liters into USD with pricing that is not matched to the same period, which can swing the outcome during volatile base oil and finished lubricant cycles.

A repeat driver of differences is that some estimates appear to bundle broader lubricants or use supplier-limited totals and then treat them as engine oils. The refresh cadence on currency timing and average selling price checks, supported by channel validation close to publication, keeps the liters-based view anchored to observed service behavior in Brazil, which is where Mordor Intelligence tends to separate engine oils from adjacent lubricant categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 602.20 M (2025) | |

| Industry Publisher A | USD 4.80 B (2026) | This figure is reported as revenue and relies on its own price and mix assumptions, and the included scope may extend beyond engine oils or use a different automotive definition, which limits reconciliation back to liters. |

| Trade News Source B | USD 1.21 B (2024) | This number reflects overall lubricants consumption for a limited supplier group and is stated in cubic meters and tonnes, which likely includes non-engine oil categories and does not map cleanly to total engine oil demand. |

Taken together, the spread is mainly explained by unit selection and scope boundaries, followed by how value is derived from volume through pricing and currency timing. When the sizing steps keep vehicle activity, drain intervals, and channel coverage explicit, we can adjust assumptions transparently without losing track of what is actually being counted.

Key Questions Answered in the Report

How large is the Brazil automotive engine oils market in 2026?

The Brazil automotive engine oils market size is 618.35 million liters in 2026 with a 2.68% CAGR outlook to 2031 (2026-2031).

Which product segment is expanding the fastest?

Motorcycle Engine Oil is forecast to grow at 2.83% CAGR through 2031, outpacing PCMO and HDMO.

Why are synthetic oils gaining share?

PROCONVE L8 emission limits demand low-SAP, oxidation-resistant oils that mineral stocks cannot match, pushing synthetics to a 2.96% CAGR.

What role do e-commerce channels play?

Online platforms reduce retail mark-ups and give marketers direct access to urban delivery riders, accelerating premium product uptake.

How does biodiesel blending affect engine oil formulations?

Higher B15 blends increase solvency and oxidation stress, so blenders adjust additive packages and rely more on synthetic base oils to maintain performance.

Are electric vehicles a significant threat to lubricant volumes?

BEV penetration remains small nationally, but rising adoption in São Paulo and Rio de Janeiro introduces a long-term volume headwind beyond 2030.

Page last updated on: