Audiobook Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

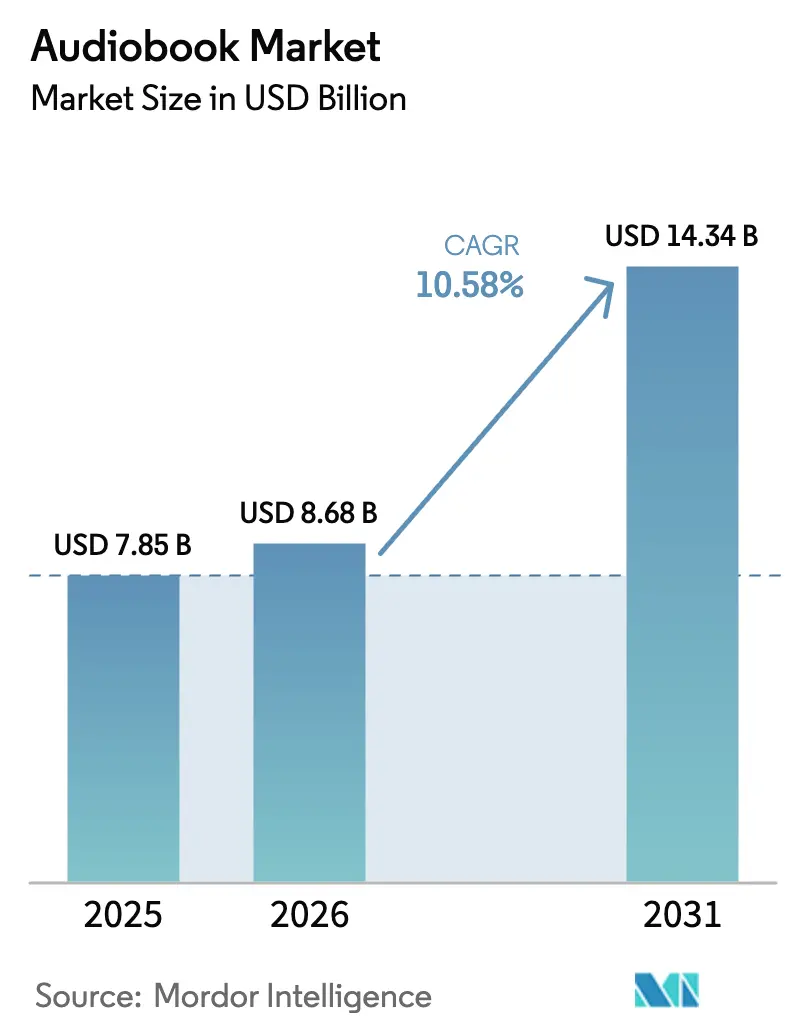

| Market Size (2026) | USD 8.68 Billion |

| Market Size (2031) | USD 14.34 Billion |

| Growth Rate (2026 - 2031) | 10.58% CAGR |

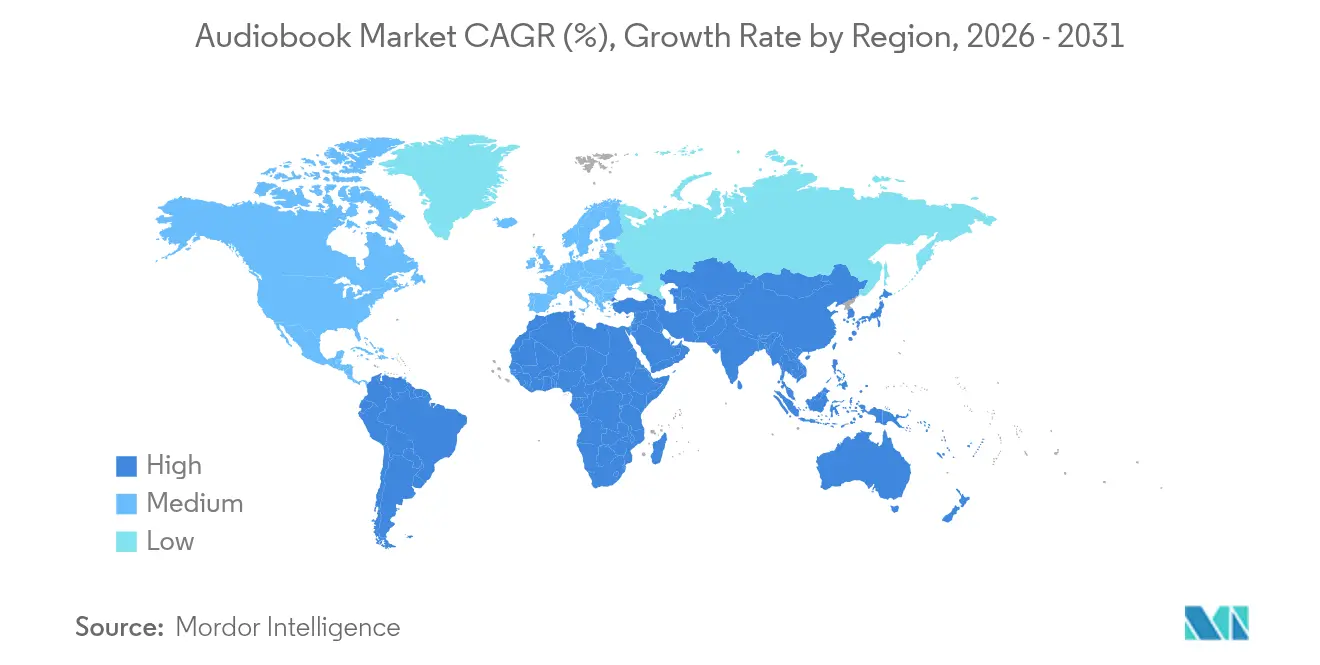

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Audiobook Market Analysis by Mordor Intelligence

The audiobook market size was valued at USD 7.85 billion in 2025 and estimated to grow from USD 8.68 billion in 2026 to reach USD 14.34 billion by 2031, at a CAGR of 10.58% during the forecast period (2026-2031). Faster and cheaper AI-driven production, subscription bundling inside music streaming plans, and rapid uptake of smart-speaker listening are moving the audiobook market from niche to mainstream. Unit economics have improved as publishers slash studio time and talent costs, allowing deep backlists and niche language titles to receive audio versions. Concurrently, platforms such as Spotify and Amazon Music are embedding audiobooks into existing subscriptions, enlarging reach among younger demographics. Rising educational use, especially in North America and the UK, is lifting the audiobook market in K-12 and higher-education settings, while smart-speaker adoption in Asia-Pacific is reshaping listening habits and creating fresh demand for localized catalogs.

Key Report Takeaways

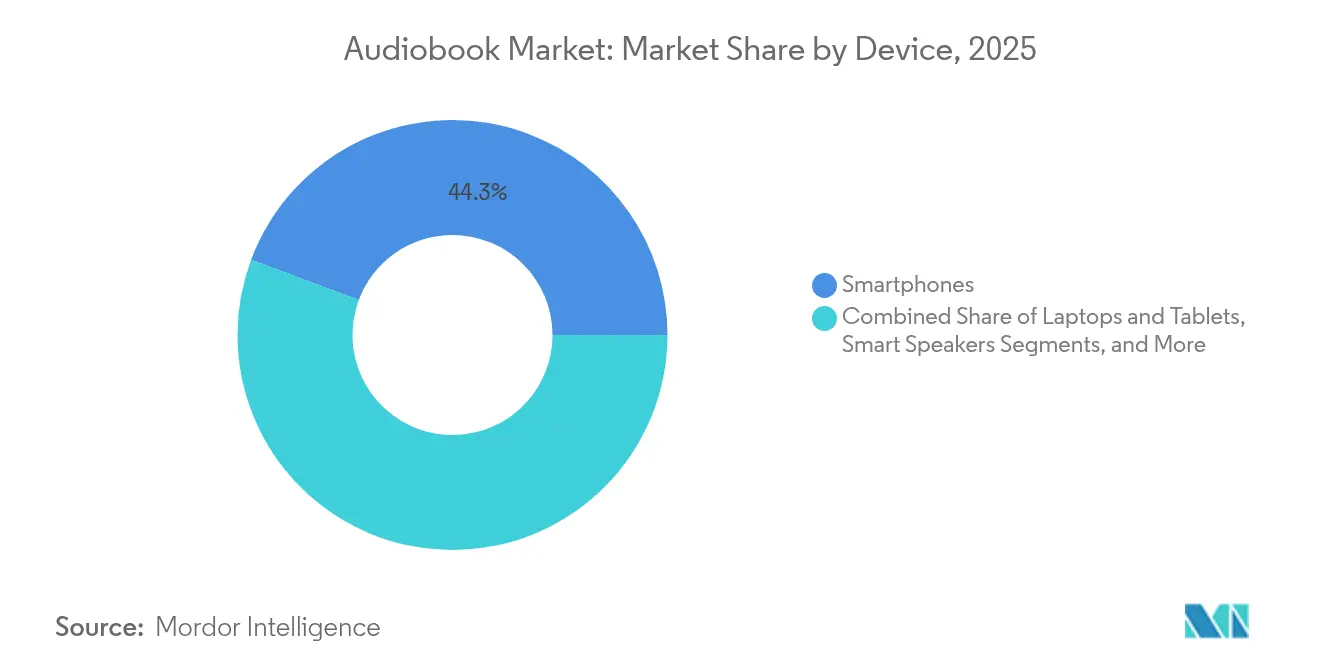

- By device type, smartphones led with 44.30% of audiobook market share in 2025, whereas smart speakers are projected to record the fastest 28.3% CAGR to 2031.

- By distribution channel, one-time downloads accounted for 53.90% of the audiobook market size in 2025; subscription services are forecast to expand at 26.5% CAGR through 2031.

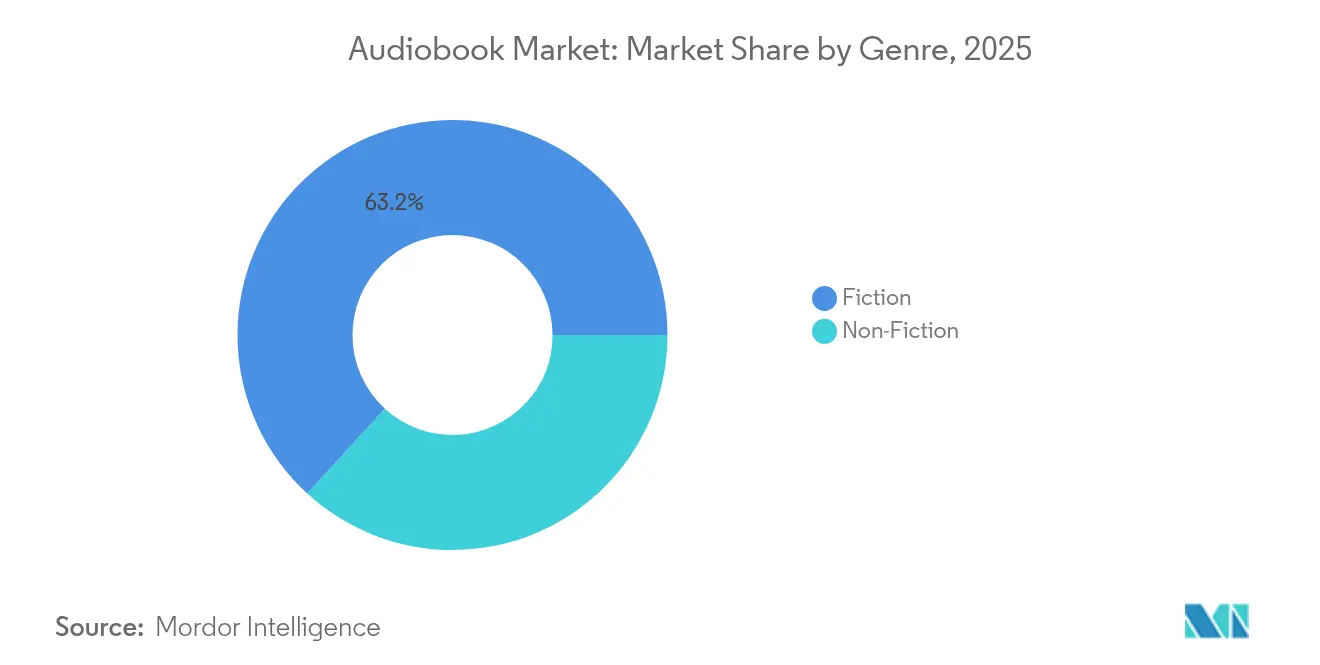

- By genre, fiction captured 63.20% of audiobook market share in 2025; non-fiction titles are set to grow at a 25.2% CAGR between 2026-2031.

- By geography, North America dominated with 44.90% revenue share in 2025, while Asia-Pacific is expected to post the highest 27.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Audiobook Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-narrated Content Slashing Production Costs | +2.5% | Global, with early adoption in North America and Europe | Short term (≤2 yrs) |

| Bundling of Audiobooks into Music-Streaming Subscriptions | +2.1% | North America and Europe | Short term (≤2 yrs) |

| Accessibility-Driven Adoption in Education | +1.3% | United States and UK, with spillover to EU | Medium term (3-4 yrs) |

| Surge of Spanish-language Subscription Platforms | +1.8% | Latin America, with spillover to US Hispanic market | Medium term (3-4 yrs) |

| Publisher "Audio-First" Release Strategy | +0.9% | Global | Short term (≤2 yrs) |

| Smart-Speaker and In-Car Infotainment Listening | +1.8% | Asia-Pacific, with spillover to North America | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

AI-narrated production cost cuts

Publishers now deploy synthetic voices that lower recording expenses by as much as 80%, freeing budgets to convert dormant backlists into audio format. Audible has released more than 40,000 AI-narrated titles and offers over 100 multilingual synthetic voices, demonstrating that professional quality is attainable without full-length human sessions. Independent authors benefit from faster turnarounds, creating deeper, more diverse catalogs that address underserved genres. Lower break-even points also encourage academic presses and regional language publishers to experiment with direct-to-audio releases. Because artificial narration archives voice profiles, future updates or translations can be generated quickly, providing durable cost advantages that will keep widening through 2030.

Subscription bundling on music platforms

Spotify integrates 15 hours of audiobooks into its Premium plan each month and reports that 1 in 4 subscribers now listen to long-form audio on the service's newsroom.[1]Spotify, “Audiobooks Now Included in Premium,” newsroom.spotify.com Amazon Music mirrors this trend, offering one Audible title per month with its music subscription. Bundling drives discovery because consumers encounter audiobooks in the same interface used for playlists. Average listening time on bundled platforms has risen, building cross-format engagement that benefits both music and spoken-word content. As telcos and device makers also explore packaged offerings, bundled access will push the audiobook market deeper into the mainstream.

Accessibility-driven educational adoption

Libraries recorded 739 million digital checkouts in 2024, and a growing portion came from audiobooks that assist learners with visual impairments or dyslexia.[2]OverDrive, “Libraries Achieve Record 739 Million Digital Checkouts in 2024,” company.overdrive.com U.S. and UK school districts are incorporating narrated textbooks into their reading curricula to reduce screen fatigue and enhance comprehension. Studies presented at academic conferences show that pairing narration with visual aids improves immediate recall by more than 30%, giving administrators measurable justification for new procurements. University presses such as Princeton and MIT are licensing scholarly titles for simultaneous print-plus-audio release, signaling the long-term institutionalization of narrated learning resources.

Smart-speaker and in-car infotainment listening

Asia-Pacific households are adding voice-activated devices at record pace; smart-speaker shipments in Japan, South Korea, China, and India underpin a 29.5% usage CAGR forecast for audiobook streaming through speakers. Automakers embed voice assistants and sizeable touch displays, letting drivers move from podcasts to full audiobooks without handheld devices. In the United States, 29% of audio consumers already listen via mobile in the car, nearly double 2014 levels. As autonomous features expand sit-back time, cabin acoustics and personalized recommendations will further enlarge listening windows, lifting the audiobook market across commuter-heavy metro areas.

Restraints Impact Analysis of Audiobook Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Royalty and Margin Pressures | -1.2% | Global | Short term (≤2 yrs) |

| Fragmented Multilingual Rights | -0.8% | Global, with highest impact in Europe and Asia | Medium term (3-4 yrs) |

| Piracy via Telegram and Stream-Ripping | -0.7% | Emerging Markets, particularly Latin America and Asia | Long term (≥5 yrs) |

| Low Willingness-to-Pay in Middle East and Africa | -0.3% | Middle East and Africa | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Royalty and margin pressures

Music collectives and author groups argue that bundling reduces per-unit royalties, forcing platforms to defend new accounting models in court. While Spotify won a United States case in February 2025, lingering disputes may raise operating costs or delay new market entries. For smaller publishers, unpredictable royalty rates complicate P&L planning, sometimes slowing investment in experimental audio formats.

Fragmented multilingual rights

Ownership of translation, narration, and region-specific merchandising rights often sits with different entities, complicating global rollout schedules. European and Asian markets suffer most because a single work may need separate rights clearance for each language variant. Negotiations inflate lead times and legal fees, partially offsetting the efficiency gains delivered by AI narration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Audiobook Market Segment Analysis

By Device:

Smart speaker surge challenges smartphone dominanceSmartphones held 44.30% of audiobook market share in 2025, reflecting their role as the default listening gateway for commuters and multitaskers. Yet the audiobook market is poised for device diversification as smart speakers advance with a 28.3% CAGR. Living-room and kitchen usage rises because hands-free voice commands ease chapter navigation, and household profiles let family members share accounts. Wearables add further reach by supporting lightweight playback during workouts. In parallel, in-car infotainment integrations now appear in mid-tier vehicle trims, aligning with the audiobook market size target for mobility-focused cohorts through 2031.

Second-screen devices such as tablets and laptops remain supplementary, facilitating note-taking or simultaneous reading for education use cases. As the audiobook market further embeds into connected-home ecosystems, platform developers are optimizing sync across phones, speakers, and dashboards to deliver frictionless resume points. Such interoperability increases session length, improving subscriber retention and boosting lifetime value for service providers.

By Distribution Channel:

Subscriptions unsettle single-purchase modelsOne-time downloads accounted for USD 4.23 billion of the audiobook market size in 2025 but face share erosion as subscription plans outpace them, growing at a 26.5% CAGR. Bundled models encourage sampling, with average listeners completing 6.8 titles annually, compared to 4.9 in 2023. Ad-supported streaming remains experimental, attracting cost-sensitive users in emerging territories. Although advertising CPMs are lower for spoken-word content than music, dynamic ad insertion enables topical promotions that help keep revenue per user rising.

Publishers weigh channel trade-offs carefully. Downloads deliver higher gross margins per unit, yet subscription algorithms place older catalog items in curated carousels, reviving long-tail earnings. As the audiobook market broadens, rights holders employ windowing tactics, a premium window for downloads, followed by subscription inclusion, to maximize yield across formats.

By Genre:

Non-fiction momentum narrows fiction’s leadFiction led the audiobook market with 63.20% revenue share in 2025, fueled by serial fantasy, romance, and thriller franchises. AI narration lets publishers cast multiple voices at lower cost, heightening immersion. Meanwhile, non-fiction titles ranging from self-help to academic lectures clock a 25.2% CAGR, shrinking the fiction gap by 2031. Educational publishers mine course syllabi for evergreen listening, and business authors release audio companions timed with keynote tours.

The audiobook market size for scholarly works expands as university libraries adopt digital-first procurement policies. Biography and history segments also accelerate because narrative journalism benefits from contextual sound design. Collectively, these shifts diversify revenue sources, reducing dependence on blockbuster novel releases.

Geography Analysis

North America Audiobook Market

North America contributed 44.90% to 2025 revenue, with the United States alone reaching USD 2 billion in publisher receipts, a 9% year-over-year increase. Extensive commute times, high smartphone penetration, and the early arrival of subscription bundles keep the audiobook market on a solid track in the region. Libraries tallied a record number of digital loans, suggesting durable public-sector demand that supports inclusive access policies.

APAC Audiobook Market

Asia-Pacific is the fastest-rising region, set to post a 27.2% CAGR. China and India anchor volume growth as middle-class consumers adopt low-cost smartphones and data plans. Japan and South Korea showcase advanced device ecosystems, where connected cars and smart speakers are bolstering the audiobook market. Local production in Mandarin, Hindi, and Korean is expanding, often through partnerships between global platforms and regional media houses.

EMEA and LATAM Audiobook Market

Europe remains resilient, with the UK audiobook market generating GBP 206 million (USD 262.7 million) in 2023, a 24% jump from the prior year. Nordic countries already see audiobooks accounting for one-third of publishers' digital revenue. Latin America, driven by Spanish-language catalogs, is expected to surpass North America in total audio listenership by 2025. Rights clearance complexity and lower willingness-to-pay continue to limit immediate scale in the Middle East and Africa, but improving connectivity and local voice talent pipelines point to incremental upside.

Competitive Landscape

Established platforms maintain significant scale advantages, yet new entrants armed with streaming reach and AI technology are reshaping rivalry. Audible controlled roughly 63.4% of 2024 revenue, backed by a catalog exceeding 100 million downloads and exclusive original programming. Spotify, however, converted its vast music audience by adding audiobook hours to Premium accounts; 25% of the service’s paying users have tried the feature newsroom.spotify.com.

RBmedia continued roll-up activity by acquiring Dreamscape Media in July 2024, adding 7,000 titles plus stronger footholds in children’s and romance categories. Storytel leverages regional language content in Europe and India, partnering with telecoms for carrier billing that removes payment friction. Technology integration defines the next stage of the audiobook market: Audible’s voice-replica beta lets narrators monetize AI copies of their timbre, and Spotify worked with ElevenLabs to scale multilingual narration.

White-space opportunities remain in academic licensing, immersive full-cast productions, and localized originals for Spanish and Hindi audiences. Competitive intensity is therefore shifting from catalog size alone toward production agility, personalization algorithms, and the breadth of language support.

Audiobook Industry Leaders

Amazon.com Inc. (Audible)

Storytel AB

Apple Inc.

Google LLC

Rakuten Kobo Inc.

- *Disclaimer: Major Players sorted in no particular order

Audiobook Market Companies Covered in this Report

- Audible ( Amazon.com Inc.)

- Apple Inc.

- Google LLC

- Storytel AB

- Spotify AB

- Rakuten Kobo Inc.

- Scribd Inc.

- Penguin Random House

- Bookmate

- BookBeat AB

- Blackstone Publishing

- OverDrive Inc.

- HarperCollins Publishers

- Hachette Book Group

- Findaway Voices

- Dreamscape Media

- Podium Publishing

- RBmedia

- Tantor Media

- Downpour

Recent Industry Developments in Audiobook Market

- May 2025: Audible expanded its AI narration and translation suite, offering publishers multilingual conversion via 100+ synthetic voices audible.com

- March 2025: Spotify partnered with ElevenLabs to distribute AI-narrated titles in 29 languages, lowering translation costs newsroom.spotify.com

- February 2025: Spotify joined forces with Podium Entertainment and Crooked Lane Books to enhance Sci-Fi and Fantasy catalogs thebookseller.com

- November 2024: Bloomsbury signed a global distribution pact with Spotify, widening reach for its audiobook portfolio bloomsbury.com

Audiobook Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global audiobook market as all paid, full-length literary and educational titles that are professionally narrated, encoded into digital audio files, and distributed for on-demand listening through downloads, streaming, or subscription libraries. According to Mordor Intelligence, value is tracked at the point of publisher or platform revenue realization, expressed in constant 2025 US dollars.

Scope exclusion: We do not count podcasts, radio drama archives, or text-to-speech services converted on the fly.

Segments Covered in This Report

- By Device

- Smartphones

- Laptops and Tablets

- Smart Speakers

- Personal Digital Assistants

- In-Car Infotainment Systems

- Wearables

- By Distribution Channel

- One-time Download

- Subscription-Based

- Ad-Supported Streaming

- By Genre

- Fiction

- Fantasy

- Romance

- Mystery/Thriller

- Non-Fiction

- Biography/History

- Self-Help/Business

- Education/Academic

- Fiction

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interview publishers, distributors, narrators, and audiobook listeners across North America, Europe, and Asia-Pacific. Structured calls and short online surveys clarify price points, catalog refresh cycles, share of listening time, and regional royalty structures, which help us fill gaps left by secondary sources and refine contentious assumptions.

Desk Research

We begin by collating public data from tier-one sources such as the Audio Publishers Association, United States Copyright Office shipment filings, ITU and GSMA smartphone penetration dashboards, Eurostat household media access surveys, and national library lending statistics. Company 10-Ks, investor decks, and reputable trade press provide additional context on subscription uptake, catalog growth, and average selling price trends.

These materials are then supplemented with D&B Hoovers revenue snapshots and Dow Jones Factiva news archives, letting us benchmark corporate disclosures against independent indicators before any model inputs are locked. The sources named are illustrative, and several other databases and governmental releases are reviewed to complete validation.

Market-Sizing & Forecasting

A top-down approach reconstructs global spend from national production and trade data, listener penetration rates, and average revenue per user, which are then cross-checked with selective bottom-up snapshots such as leading platform revenues and sampled ASP × title volumes. Key variables feeding the model include smartphone user base, subscription share of total listens, title release counts, publisher royalty take-rate, and regional currency movements. Multivariate regression projects these drivers forward, while scenario analysis frames upside or downside paths when technology (for example, AI narration) accelerates or stalls. Where bottom-up estimates diverge, we reconcile them to the top-down baseline through weighted averaging that favors primary-verified data.

Data Validation & Update Cycle

Before sign-off, analysts run variance checks against external benchmarks, flag anomalies, and resolve outliers in a two-step internal review. Reports refresh each year, and we trigger interim revisions when mergers, regulatory shifts, or major pricing moves change the trajectory.

How Mordor Intelligence's Audiobook Market Size Compares to Other Published Estimates

Published figures often differ because each firm selects its own content mix, pricing ladders, and forecast cadence. We anchor our number to paid, professionally produced titles only, refreshed annually, and expressed in transparent constant-currency terms.

Key gap drivers include whether spoken-word podcasts are folded in, how aggressively future ARPU is escalated, and how frequently models are updated when exchange rates swing. Our disciplined scope, tighter ARPU ladder, and yearly refresh keep the baseline conservative yet actionable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.85 billion (2025) | Mordor Intelligence | |

| USD 8.70 billion (2024) | Global Consultancy A | Includes podcasts and applies 26 % CAGR without primary validation |

| USD 8.32 billion (2025) | Industry Journal B | Builds from shipment values and uniform ARPU, limited cross-checks with rights holders |

The comparison shows that once content scope and ARPU logic are aligned, numbers converge toward Mordor's figure, underscoring that our measured, transparent framework delivers a dependable baseline for strategic planning.

Key Questions Answered in the Report

What is the current Audiobook Market size?

In 2026, the Audiobook Market size is expected to reach USD 8.68 billion.

Who are the key players in Audiobook Market?

Amazon.com, Inc., Apple Inc., Blackstone Audio, Inc., Bookmate and Google Play Books are the major companies operating in the Audiobook Market.

Which is the fastest growing region in Audiobook Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Audiobook Market?

In 2025, the North America accounts for the largest market share in Audiobook Market.

What years does this Audiobook Market cover, and what was the market size in 2025?

In 2025, the Audiobook Market size was estimated at USD 8.68 billion. The report covers the Audiobook Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Audiobook Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: