Asset Tokenization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

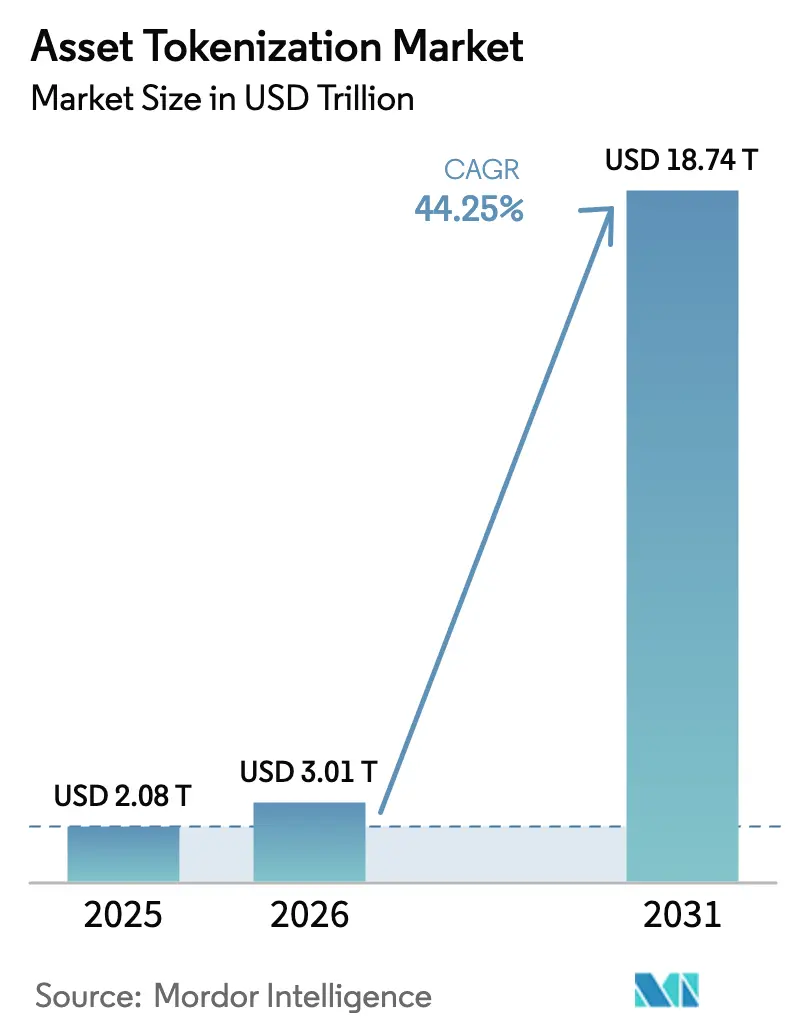

| Market Size (2026) | USD 3.01 Trillion |

| Market Size (2031) | USD 18.74 Trillion |

| Growth Rate (2026 - 2031) | 44.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asset Tokenization Market Analysis by Mordor Intelligence

The asset tokenization market size was valued at USD 2.08 trillion in 2025 and estimated to grow from USD 3.01 trillion in 2026 to reach USD 18.74 trillion by 2031, at a CAGR of 44.25% during the forecast period (2026-2031). Regulatory clarity in North America and the European Union, rapid institutional capital re-allocation, and the maturing of cross-chain interoperability now underpin the commercial viability of large-scale token issuance and secondary trading. Permissioned architectures still dominate issuance volumes, yet surging demand for open networks signals rising comfort with decentralized liquidity as compliance tooling improves. Commodities tokenization is emerging as the clear growth frontier as corporates use carbon-credit and precious-metal tokens to hedge ESG liabilities and inflation exposure. Platform vendors that can fuse robust legal wrappers with seamless ISO-20022 messaging are gaining a tangible advantage in winning tier-1 banking mandates.

Key Report Takeaways

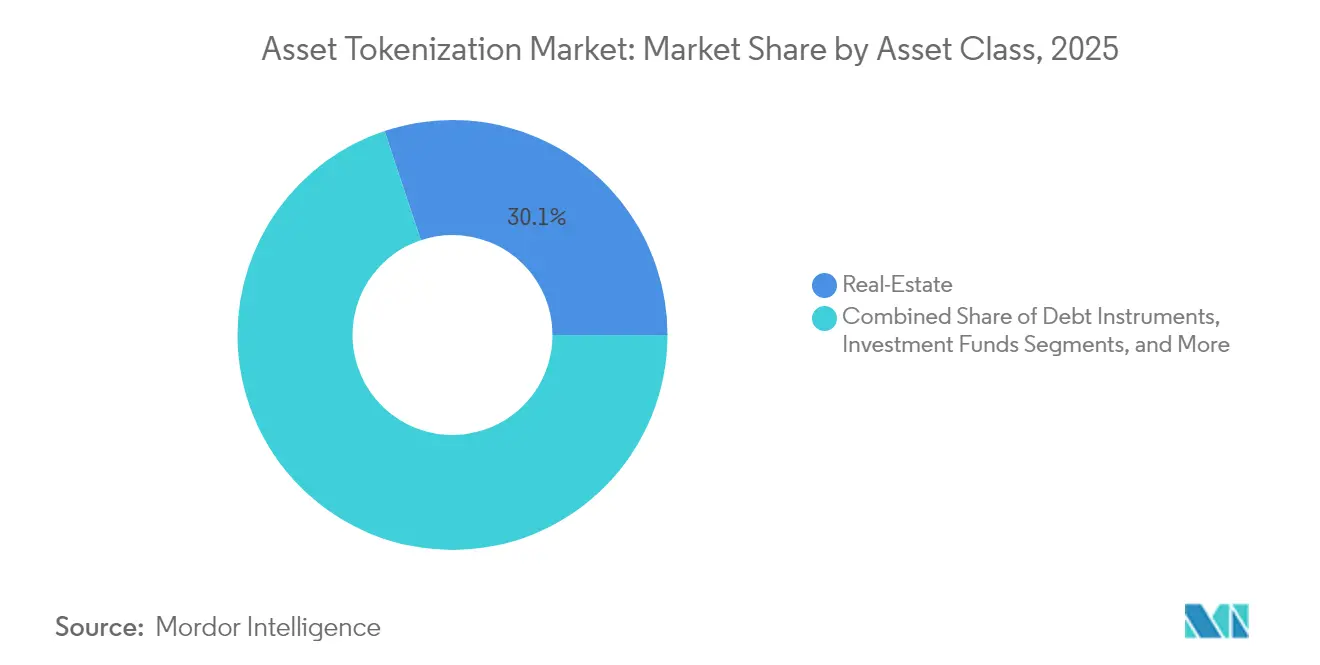

- By asset class, real estate led with 30.12% of asset tokenization market share in 2025; commodities are projected to expand at a 48.35% CAGR through 2031.

- By investor type, institutional investors held 69.10% of the asset tokenization market share in 2025, while the retail segment is advancing at 50.20% CAGR to 2031.

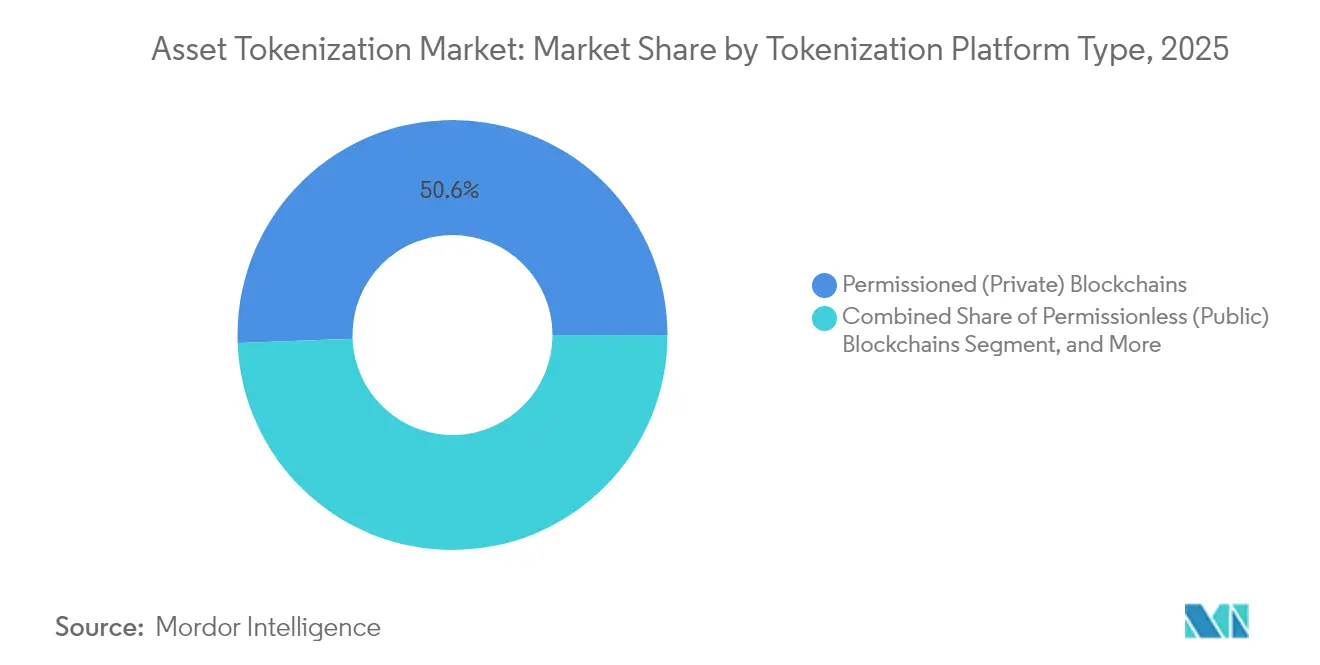

- By tokenization platform type, permissioned blockchains captured 50.60% of the asset tokenization market size in 2025, yet permissionless networks are forecast to grow at 51.60% CAGR.

- By offering, tokenization platforms/middleware accounted for 59.05% of revenue in 2025, while Compliance and legal-technology services are expanding fastest at 47.95% CAGR to 2031

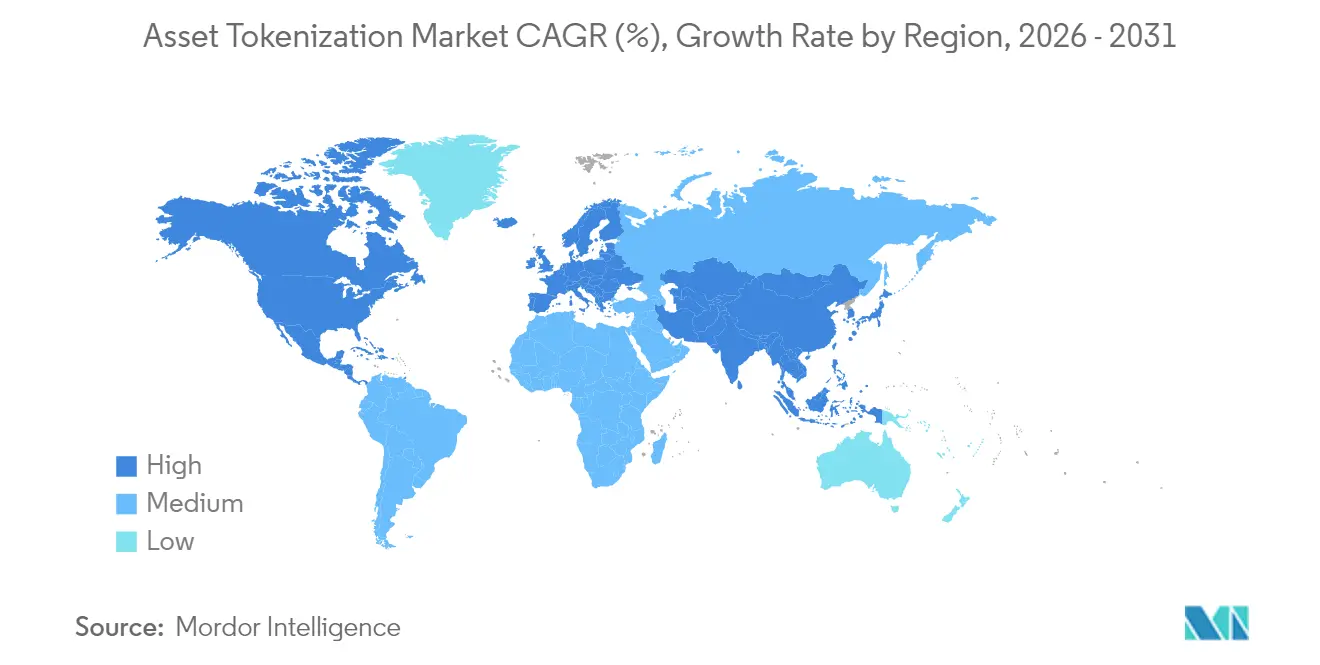

- By geography, North America generated 39.10% revenue share in 2025; Asia-Pacific is set to record a 53.75% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Asset Tokenization Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory clarity in key financial hubs | +8.2% | North America and EU | Medium term (2-4 years) |

| Rising institutional adoption and tokenized funds | +12.5% | Global, focus in North America and Asia-Pacific | Short term (≤ 2 years) |

| Demand for fractional real-estate ownership | +6.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Advancements in blockchain interoperability | +7.1% | Global | Long term (≥ 4 years) |

| ISO-20022 integration enabling seamless settlement | +4.3% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Emergence of tokenized carbon-credit instruments | +3.9% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Institutional Adoption and Tokenized Funds

Institutional allocations into tokenized money-market and fixed-income products are accelerating. BlackRock’s USD Institutional Digital Liquidity Fund attracted over USD 550 million within months of launch, showing clear appetite for on-chain treasury alternatives that offer daily dividend distribution and intraday redemption windows. Goldman Sachs is preparing three tokenized products for roll-out by year-end 2025, while JPMorgan’s Kinexys network has processed USD 1.5 trillion in tokenized transactions by end-2024 and is piloting on-chain foreign-exchange settlement for early-2025 release. These moves create network effects that encourage custodians, fund administrators, and asset managers to build compatible rails.

Demand for Fractional Real-Estate Ownership

Token-enabled fractional structures lower minimum ticket sizes, allowing a broader investor base to enter prime property markets. T-RIZE Group’s USD 300 million residential development tokenization illustrates how sponsors are securing diverse investor pools while reducing financing costs through wider market reach [1]T-RIZE Group, “USD 300 Million Residential Tokenization Deal,” t-rize.com. Enhanced transparency from immutable performance data also mitigates information asymmetry, a long-standing barrier in commercial real-estate investing, which in turn boosts secondary liquidity. Crowdfunding regulations aligned with tokenization frameworks in the United States and the European Union further reinforce growth potential for retail-accessible real-estate products.

Advancements in Blockchain Interoperability

Cross-chain protocols are eliminating siloed liquidity. Deutsche Bank’s collaborative pilot with financial peers tests network-of-networks models that interlink multiple ledgers with existing core banking systems. Chainlink’s Cross-Chain Interoperability Protocol enables atomic swaps that honor delivery-versus-payment logic, a prerequisite for regulated institutions looking to avoid settlement risk. Surveys among institutional treasurers show that 93% view unified liquidity pools as necessary for scaling digital asset adoption, underscoring why vendors that master interoperability reach faster commercialization.

ISO-20022 Integration Enabling Seamless Settlement

The shift to ISO-20022 messaging is aligning on-chain assets with mainstream payment systems. Coreum’s native ISO-20022 support demonstrates how standardized data fields allow real-time reconciliation between custodians and central securities depositories. Swift research highlights that Single Pools of Liquidity can lower intraday credit lines when tokenized cash co-exists with traditional balances on integrated ledgers. For banks, these efficiencies translate into capital-use optimization and lower operational overhead, making compliance-ready ISO-20022 layers a competitive differentiator for tokenization platforms.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory fragmentation and compliance costs | -5.7% | Developing markets | Short term (≤ 2 years) |

| Cyber-security and smart-contract vulnerabilities | -4.2% | Global | Short term (≤ 2 years) |

| Oracle manipulation and off-chain data risks | -2.8% | DeFi-centric regions | Medium term (2-4 years) |

| Custodial liability during insolvency events | -3.1% | Jurisdictions with unclear bankruptcy rules | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Smart-Contract Vulnerabilities

High-profile exploits continue to dent market confidence. In January 2024 the KiloEx decentralized exchange lost USD 7 million after attackers manipulated an on-chain price oracle, exposing gaps in real-time data validation. Insurance premiums for smart-contract cover have since risen as underwriters reprice risk. Platforms are now mandating multi-layer audits, automated circuit breakers, and real-time monitoring to regain trust. Yet the evolving threat landscape means even rigorously vetted code can harbor latent flaws, keeping security a top-tier boardroom concern for tokenization providers.

Custodial Liability During Insolvency Events

The 2024 bankruptcy filings of several smaller crypto broker-dealers resurfaced questions around asset segregation and investor recourse. Legal analyses showed that in jurisdictions without explicit digital-asset custody statutes, client tokens risk being pooled with estate assets during liquidation, leaving holders exposed to pro-rata recovery. Regulators in Singapore, the European Union, and the United States are now drafting enhanced segregation guidance, yet cross-border disparities persist. Institutions consequently demand bankruptcy-remote custody structures and tri-party trust arrangements before onboarding large balance sheets onto tokenized rails.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Real-Estate Leadership Faces Commodities Disruption

Real-estate contributes the largest revenue slice, accounting for 30.12% of the asset tokenization market in 2025. Institutional demand centers on flagship office towers and logistics assets that deliver predictable cash flows, while token structures reduce entry thresholds and amplify portfolio diversification across regions. The segment uses permissioned networks where audited smart contracts automatically distribute rental income, thus easing reconciliation for fund administrators. Commodities, though smaller today, are posting the fastest trajectory with a 48.35% CAGR through 2031, powered by carbon-credit and precious-metal token launches underpinned by ESG mandates. Renewable energy producers see tokens as a liquid instrument for monetizing verified emission reductions, which boosts bilateral trading volumes on digital commodity exchanges. Debt instruments also show steady interest, with municipal-bond token pilots in the United States offering same-day settlement and lower issuance fees.

Regulatory harmonization is pivotal for real-estate sponsors seeking cross-border investor pools. Jurisdictions such as the United Arab Emirates and Luxembourg now recognize on-chain share registries, easing secondary transfers and collateral pledges. For commodities, standardization initiatives like the London Bullion Market Association’s blockchain provenance project are spurring confidence in digital gold products. Carbon-credit tokens benefit from transparent lifecycle data that supports compliance reporting for corporate buyers. As interoperability frameworks mature, exchanges can list multi-asset pools that bundle real-estate and commodities tokens, improving risk-adjusted returns for institutional portfolios and enlarging the addressable asset tokenization market.

By Investor Type: Institutional Dominance Meets Retail Democratization

Institutional investors controlled 69.10% of deployed capital in 2025, reflecting their readiness to navigate complex legal structures and their sizeable balance sheets. Asset managers leverage tokenized funds to gain operational efficiencies, including near-instant share issuance and automated corporate-action processing. Securitize has crossed USD 1 billion in issued tokens and now administers USD 38 billion across 715 funds after acquiring MG Stover, positioning itself as an end-to-end service provider linking primary issuance and secondary marketplaces. Pension funds also view tokenized real-estate and infrastructure as a match for long-duration liabilities given the potential for improved liquidity.

Retail participation is scaling swiftly at 50.20% CAGR, helped by compliant crowdfunding exemptions and intuitive mobile wallets that mask blockchain complexity. Accredited retail segments occupy a bridging role, bringing higher average ticket sizes yet still benefiting from fractional exposure to venture-fund tokens and commercial real-estate. Education portals embedded into issuance platforms guide new entrants through wallet creation, risk disclosures, and tax documentation, broadening funnel conversion rates. Looking ahead, embedded-finance integrations with neobanks will further lower onboarding friction, expanding the overall asset tokenization market by tapping under-served demographics in emerging economies.

By Tokenization Platform Type: Permissioned Stability Versus Permissionless Innovation

Permissioned chains, with 50.60% market share in 2025, remain the preferred avenue for pilot programs that must satisfy stringent know-your-customer and anti-money-laundering obligations. Bank consortiums deploy consortium-governed ledgers where gatekeepers grant node access, ensuring audit trail integrity and regulator visibility. However, permissionless networks are racing ahead at a 51.60% CAGR. They attract liquidity from global traders who value 24×7 market access and composability with decentralized finance protocols that amplify yield opportunities.

Hybrid models blend both paradigms. JPMorgan’s Kinexys executes large-value transactions on a private layer and then anchors state proofs to a public chain, combining settlement finality with public verifiability. Token issuers appreciate the optionality of migrating between layers to optimize fees or compliance requirements. As zero-knowledge proofs mature, public chains can enforce selective disclosure of transaction data, eroding a historic advantage of permissioned systems. This progress will likely rebalance platform shares, yet permissioned frameworks will continue serving regulated asset classes where counterparty due-diligence is non-negotiable.

By Offering: Platform Middleware Leads as Compliance Services Surge

Tokenization platforms and middleware accounted for 59.05% of revenue in 2025, forming the backbone that converts traditional securities, real-estate titles, or commodities certificates into standardized digital tokens. These vendors supply workflow orchestration, identity management, and API gateways that integrate seamlessly with transfer agents and custodians. Larger financial-market infrastructures opt for white-label solutions to shorten time-to-market while maintaining brand control. Compliance and legal-technology services are expanding fastest at 47.95% CAGR to 2031 as multilayer regulatory mandates heighten demand for automated rule engines that embed jurisdiction-specific constraints directly into smart contracts.

Smart-contract audit and cybersecurity consultancies are capitalizing on rising code-risk awareness. Custody providers differentiate through secure multi-party computation and hardware-security modules that align with institutional insurance thresholds. Secondary marketplaces focus on matching-engine upgrades and settlement-cycle compression to meet equities-like service levels that institutional traders expect. Collectively, these offerings enlarge the asset tokenization market size by removing pain points that once deterred mainstream adoption, especially among highly regulated asset managers.

Geography Analysis

North America remains the largest regional contributor, holding 39.10% of global revenue in 2025. The United States benefits from April 2025 SEC guidance clarifying that certain USD-backed stablecoins are not securities, which in turn catalyzes bank participation in tokenized deposit pilots. Canada’s regulatory sandbox supports experimentation with tokenized mortgage pools, and its pension funds are beginning to acquire minority stakes in infrastructure-backed security tokens. Venture investment also concentrates in the region, with specialized blockchain funds closing USD 2.4 billion in fresh capital in 2024 according to PitchBook, further reinforcing the innovation loop.

Asia-Pacific is the fastest-growing region, expanding at a 53.75% CAGR through 2031. Singapore’s Project Guardian now involves over 40 financial institutions testing tokenized bonds, deposits, and funds on interoperable ledgers governed by the Monetary Authority of Singapore. Hong Kong’s June 2025 digital-asset roadmap introduces a stablecoin licensing regime and government tokenized-bond issuance, signaling official endorsement that will likely mobilize regional banks and insurers. Japan is advancing a framework that reclassifies certain digital assets, paving the way for tokenized exchange-traded funds and broadening retail access to alternative assets .

Europe posts steady progress under the Markets in Crypto-Assets (MiCA) regulation that sets passport-able licensing for crypto-asset service providers. Germany’s electronic securities law recognizes bearer bonds and fund units on DLT registers, prompting public-sector issuers to test fully digital workflows. France’s public blockchain sandbox accepted three tokenization projects focused on green-bond distribution, reflecting the continent’s climate-finance focus. Meanwhile, the Middle East and Africa are piloting energy-backed security tokens inside regulatory sandboxes in Abu Dhabi and Johannesburg, and South America is evolving from proof-of-concepts toward limited public offerings as infrastructure matures.

Competitive Landscape

The asset tokenization market shows moderate fragmentation with signs of consolidation. Global banks such as JPMorgan, Goldman Sachs, and Citi are launching proprietary issuance rails while forming external partnerships to accelerate go-to-market timetables. Citi collaborated with BondbloX to tokenize a USD 500 million corporate bond in October 2024, shortening settlement from T+5 to sub-minute finality. Goldman Sachs plans to route broker-dealer flows onto its Digital Asset Platform by Q4 2025, citing lower custody and reconciliation expenses.

Specialist providers continue to scale. Securitize raised USD 47 million in April 2025, led by BlackRock, and now supports primary issuance, secondary trading, and fund administration under a single roof which positions it as a full-stack alternative to legacy transfer agents. Digital Asset secured USD 135 million in June 2025 from Goldman Sachs and Citadel to expand the Canton Network, a privacy-enabled ledger expected to host live institutional deployments within 18 months. Swarm introduced a permissionless yet EU-compliant venue for trading tokenized Treasury Bills in March 2025, underlining competitive pressure from agile startups [3]Swarm, “EU-Compliant Permissionless Treasury Platform Launch,” swarm.com.

Strategic differentiation hinges on three factors. First is interoperability, where players integrate ISO-20022 codecs and cross-chain bridges to provide seamless connectivity with custodians and central depositories. Second is regulatory expertise, as vendors that embed jurisdiction-specific constraints into smart contracts lower compliance overhead for clients. Third is institutional-grade security, with providers investing in formal-verification tooling and zero-knowledge proof frameworks to reassure risk committees. As consolidation advances, top performers will likely couple deep regulatory relationships with technical agility, enabling them to capture greater share of the growing asset tokenization market.

Asset Tokenization Industry Leaders

Securitize Markets, LLC

tZERO Technologies

Tokensoft Inc.

Polymath Research Inc.

Tokeny Solutions SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hong Kong unveiled a digital-asset strategy featuring a stablecoin licensing regime and tokenized government-bond program to position the city as an institutional tokenization hub.

- June 2025: Digital Asset raised USD 135 million from Goldman Sachs and Citadel to scale the privacy-enabled Canton Network for institutional tokenization.

- April 2025: Republic completed the acquisition of INX Digital for up to USD 60 million to build a regulated global platform for tokenized assets.

- April 2025: Securitize acquired MG Stover’s fund administration business, becoming the largest digital-asset fund administrator with USD 38 billion under administration.

Global Asset Tokenization Market Report Scope

Asset tokenization is the process of converting the value of a tangible or intangible asset into a digital token using blockchain technology. This transformation allows for fractional ownership, increased liquidity, clear traceability and auditability.

The asset tokenization market is segmented by asset type (real estate, debt, investment funds, private equity, public equity, other asset types), end-user verticals (institutional investors, retail investors), geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Real-Estate |

| Debt Instruments |

| Investment Funds |

| Private Equity |

| Public Equity |

| Commodities |

| Institutional Investors |

| Accredited Retail Investors |

| Retail Investors |

| Permissioned (Private) Blockchains |

| Permissionless (Public) Blockchains |

| Hybrid Models |

| Tokenization Platforms / Middleware |

| Smart-Contract Development and Audit |

| Custody and Wallet Services |

| Compliance and Legal-Tech Services |

| Secondary Trading and Exchanges |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Asset Class | Real-Estate | ||

| Debt Instruments | |||

| Investment Funds | |||

| Private Equity | |||

| Public Equity | |||

| Commodities | |||

| By Investor Type | Institutional Investors | ||

| Accredited Retail Investors | |||

| Retail Investors | |||

| By Tokenization Platform Type | Permissioned (Private) Blockchains | ||

| Permissionless (Public) Blockchains | |||

| Hybrid Models | |||

| By Offering | Tokenization Platforms / Middleware | ||

| Smart-Contract Development and Audit | |||

| Custody and Wallet Services | |||

| Compliance and Legal-Tech Services | |||

| Secondary Trading and Exchanges | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the asset tokenization market?

Regulatory clarity across major financial hubs, rising institutional allocation to tokenized funds, and breakthroughs in blockchain interoperability are propelling the asset tokenization market toward a 44.25% CAGR through 2031.

Which asset class leads in tokenized issuance today?

Real estate remains the largest asset class with 30.12% share in 2025, though commodities tokens are expanding fastest at 48.35% CAGR.

How significant is institutional participation?

Institutional investors held 69.10% of deployed capital in 2025, and marquee launches such as BlackRock’s on-chain liquidity fund signal deeper engagement.

Which region will grow fastest between 2025 and 2031?

Permissionless chains offer larger global liquidity pools and lower intermediation costs, supporting a 51.60% CAGR that outpaces growth on permissioned networks.

Page last updated on: