Healthcare Asset Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

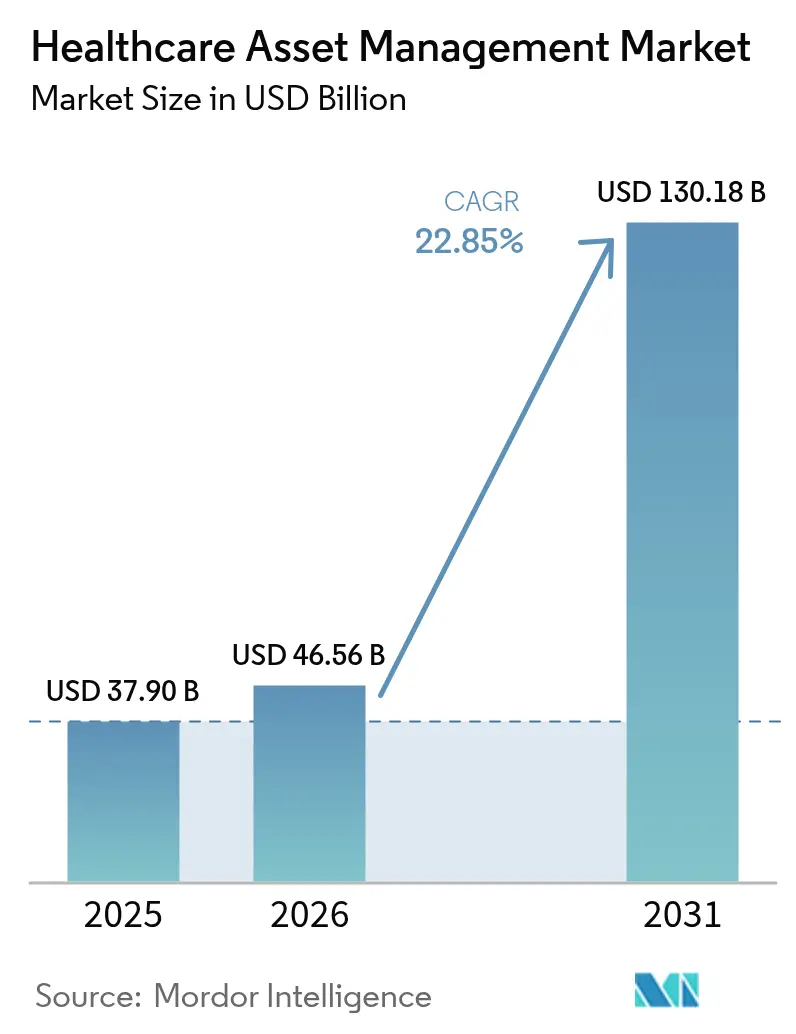

| Market Size (2026) | USD 46.56 Billion |

| Market Size (2031) | USD 130.18 Billion |

| Growth Rate (2026 - 2031) | 22.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Asset Management Market Analysis by Mordor Intelligence

The Healthcare Asset Management market size is expected to grow from USD 37.90 billion in 2025 to USD 46.56 billion in 2026 and is forecast to reach USD 130.18 billion by 2031 at 22.85% CAGR over 2026-2031.

The growth trajectory reflects how regulatory mandates, workforce shortages, and cybersecurity expectations converge to reposition asset tracking from a cost-containment tool to a strategic pillar of digital health operations. Hospitals are looking beyond bar-code inventory toward connected platforms that streamline compliance with the FDA’s 2024 device-security guidance, an obligation that can consume 5% or more of a manufacturer’s annual revenue. [1]Steute Meditec, “Medical Device Manufacturers Are Shocked at How Much Time and Money They’re Spending on Pre-Certification and Regulatory Compliance,” steute-meditec.com Demand also ties directly to nursing-staff constraints; shrinking clinical capacity magnifies the value of systems that free caregivers from locating equipment and instead let them focus on patient outcomes. In parallel, predictive analytics embedded in tags move maintenance from reactive to anticipatory, trimming downtime and extending asset life. Taken together, these forces enable a healthcare asset management market environment in which hospitals, pharma plants, and laboratories regard integrated visibility, cybersecurity, and analytics as non-negotiable features rather than optional add-ons.

Key Report Takeaways

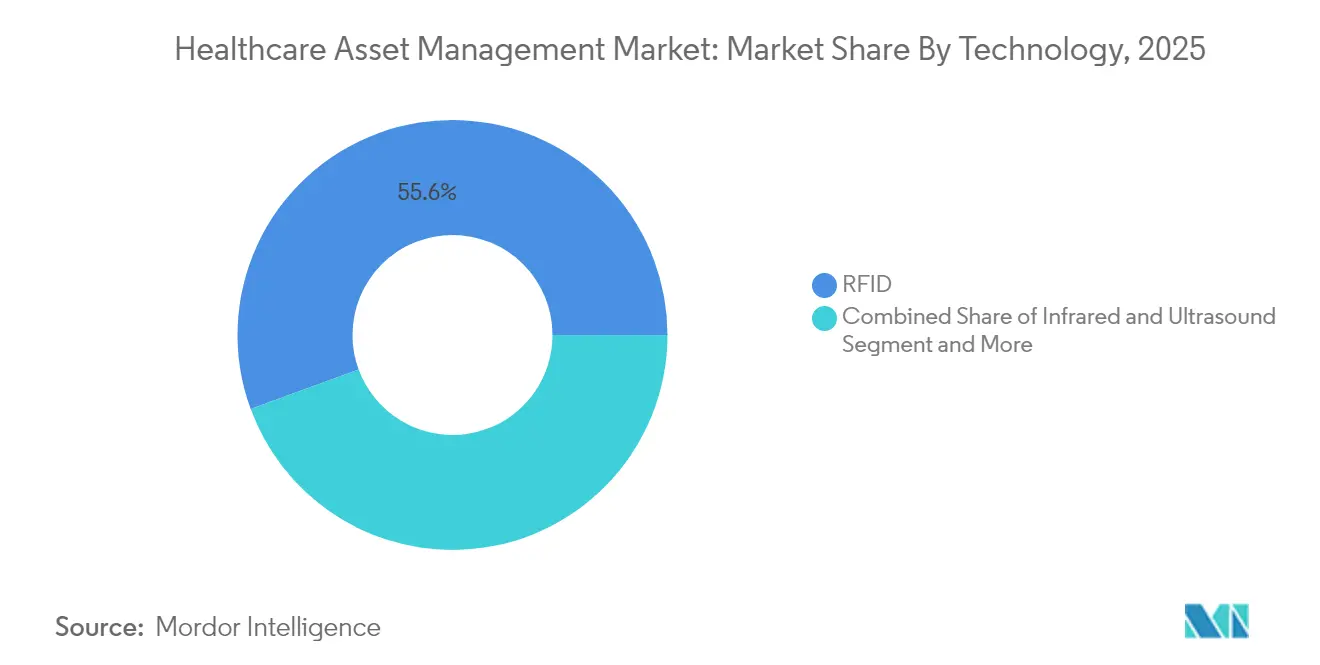

- By technology, RFID led with 55.60% revenue share in 2025, while Real-Time Location Systems are projected to expand at a 27.20% CAGR through 2031.

- By component, hardware accounted for 61.60% of the market in 2025; services hold the fastest outlook with a 24.90% CAGR to 2031.

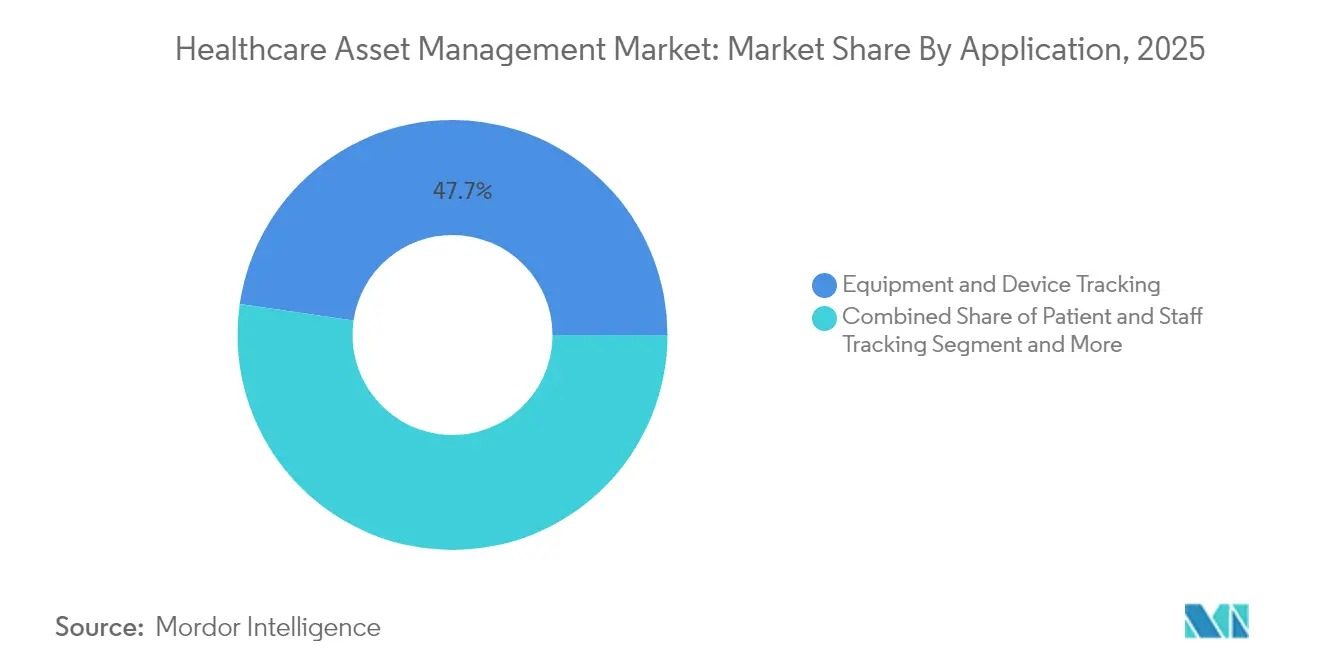

- By application, equipment and device tracking commanded 47.70% of the healthcare asset management market share in 2025, whereas patient and staff tracking is advancing at a 27.60% CAGR through 2031.

- By end user, hospitals and clinics held 64.40% of 2025 revenue, while pharmaceutical and biotech manufacturing is set to grow at 26.10% CAGR to 2031.

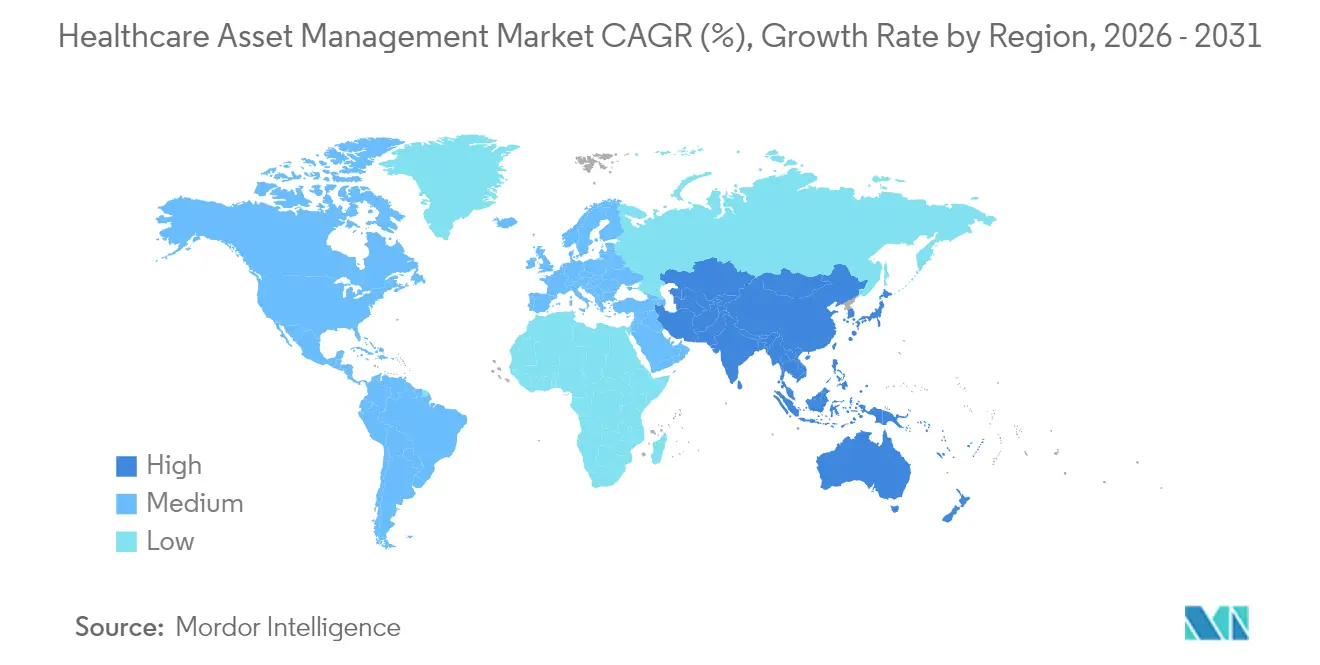

- By geography, North America retained 37.20% of 2025 revenue, yet Asia-Pacific registers the highest regional CAGR at 21.90% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for RFID to curb drug counterfeiting | +3.8% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Efficiency pressures from nursing-staff shortages | +5.2% | North America and EU core; spill-over to APAC | Short term (≤ 2 years) |

| Patient-safety regulations (e.g., UDI, EU-MDR) | +3.1% | North America and EU, expanding in APAC | Long term (≥ 4 years) |

| AI-based predictive maintenance embedded in tags | +2.4% | Global, led by North America | Medium term (2-4 years) |

| Pay-for-performance reimbursement tied to asset traceability | +2.1% | North America core, selective EU adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for RFID to curb drug counterfeiting

Pharmaceutical counterfeiting drains an estimated USD 200 billion from the global economy each year, prompting regulators to impose serialisation and pedigree requirements that make end-to-end visibility indispensable. Under the U.S. Drug Supply Chain Security Act, drug makers, wholesalers, and dispensers must prove product provenance at every hand-off. RFID with cryptographic authentication now underpins most of these deployments because it combines item-level identification with real-time environmental monitoring, a necessity for temperature-sensitive biologics. [2]Real Time Networks, “How Smart Technology Improves Pharmaceutical Asset Tracking and Compliance,” realtimenetworks.com Semiconductor shortages since 2024 lifted tag prices by up to 20%, yet organisations still invest because non-compliance fines and recall costs far exceed hardware spending. Vendors such as SATO have introduced sterilisation-resistant tags that deliver both authentication and workflow efficiency in one process step. [3]SATO Asia Pacific, “ニュース – アジア太平洋,” satoasiapacific.com These factors underpin the 26.8% CAGR projected for pharmaceutical and biotech manufacturing customers between 2025 and 2030.

Efficiency pressures from nursing-staff shortages

Nursing vacancy rates above 15% in major urban hospitals leave care teams stretched and force administrators to squeeze every efficiency gain possible from support technology. Studies reveal that nurses spend over one-fifth of each shift searching for missing equipment; RTLS implementations that cut search time by more than 90% therefore provide a direct labour dividend that keeps beds staffed without adding headcount. [4]INDTRAC, “Blogs and News – INDTRAC Real-Time Tracking,” indtrac.com British facilities have demonstrated time reductions from 60 minutes to 10 minutes per device, translating into heightened patient-safety scores and improved staff retention. Advanced deployments now combine BLE badges, panic buttons, and predictive analytics that stage equipment on units before clinicians request it, easing workflow strain and boosting satisfaction.

Patient-safety regulations (UDI, EU-MDR)

Unique Device Identification schemes in the United States and the broader EU-MDR framework require hospitals to capture device identity, maintenance logs, and cybersecurity status throughout a product’s life. Compliance costs can reach 5% of annual sales for manufacturers, spurring demand for platforms that automate data capture and report generation. The recent rise in device vulnerabilities—59% year over year—adds a cybersecurity layer to tracking, turning asset management software into a control point for patch status and threat monitoring. Hospitals that already run integrated tracking platforms are better positioned to meet the EU’s EUDAMED database submissions, reinforcing a virtuous cycle of adoption and compliance.

AI-based predictive maintenance embedded in tags

Embedding sensors and AI models inside capital equipment allows organisations to detect anomalies weeks before failure, cutting downtime by 30% and lowering service costs by close to 20%. Digital twins paired with RTLS events build a continuous data loop that schedules service only when wear indicators cross risk thresholds, rather than on rigid calendar intervals. MRI scanners, ventilators, and infusion pumps equipped with such intelligence can automatically trigger work orders, allocate loaner devices, and update regulatory audit trails, streamlining biomedical engineering workloads and safeguarding revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cybersecurity concerns | –2.8% | Global, heightened in EU and North America | Short term (≤ 2 years) |

| High upfront RTLS / RFID infrastructure cost | –3.2% | Emerging markets core; selective developed-market impact | Medium term (2-4 years) |

| Radio-interference with critical wireless medical devices | –1.4% | Global, acute in high-density medical facilities | Short term (≤ 2 years) |

| Fragmented legacy CMMS slowing integration | –1.8% | North America and EU, legacy-system concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and cybersecurity concerns

Average breach costs in healthcare reached USD 9.77 million per incident in 2024, making security risk a material deterrent to rapid roll-outs. The FDA’s 2024 draft guidance urges stronger pre-market security testing, compelling buyers to fund encryption, network segmentation, and continuous monitoring before go-live. Many hospitals, therefore, begin with on-premises deployments or air-gapped networks that limit data flow to the cloud, trading some analytics capability for risk reduction. Legacy devices without secure firmware further complicate integrations, extending project timelines and inflating budgets.

High upfront RTLS/RFID infrastructure cost

Comprehensive implementations often require USD 150,000-250,000 in software licensing plus hardware investments that can exceed USD 500,000 for a 350-bed facility. Semiconductor availability issues and shipping surcharges inflate tag and reader prices, while specialist install teams command premium rates due to scarce cross-disciplinary expertise. Hospitals in emerging economies commonly deploy phased roll-outs focused on high-value assets first, but staggered projects weaken network effects and defer break-even, lengthening payback to three years or more.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: RFID Dominance Faces RTLS Disruption

RFID accounted for 55.60% of 2025 revenue, underlining decades of protocol maturity and robust supply chains that made the technology the default for drug inventory and surgical kit tracking. The healthcare asset management market size for RFID was USD 21.07 billion in 2025, showing how deeply the modality is entrenched at point-of-care cabinets and central sterile processing. Yet software-defined workflows increasingly require location, not just identity. Real-Time Location Systems leveraging BLE, Wi-Fi, and ultra-wideband are therefore forecast to compound at 27.20% CAGR to 2031, eating into static RFID growth.

A second growth phase emerges as vendors collapse RFID and RTLS into multi-mode tags that pivot between passive ID and real-time telemetry, a design that preserves prior capital investment while enabling richer analytics. Deployments at paediatric-care centres demonstrate this twin-mode value: passive RFID limits shrinkage of high-value drugs, while RTLS ensures infusion pumps circulate where patient acuity is highest. Hardware still dominates spending because tags, gateways, and exciters blanket entire campuses; however, the profit pool is shifting toward platform licences that unite device identity, location, and utilisation into one dashboard. As this convergence proceeds, the healthcare asset management market will likely regard single-mode offerings as a niche.

By Component: Services Surge as Hardware Commoditizes

Hardware captured 61.60% of 2025 sales thanks to ongoing purchases of millions of tags, readers, and ceiling-mounted beacons. Even so, services are pacing ahead with a 24.90% CAGR as hospitals pivot from capital expense toward managed outcomes. Under subscription agreements, vendors guarantee uptime, firmware currency, and regulatory-ready audit logs, freeing IT teams to focus on patient-facing initiatives. The healthcare asset management market size tied to services is forecast to reach USD 55.32 billion by 2031, pointing to a maturation cycle where infrastructure becomes ubiquitous and differentiation shifts to consultative optimisation.

Professional and managed services also address the hardest obstacles—change management, systems integration, and cybersecurity accreditation—that no amount of shelf hardware alone can solve. Service contracts typically bundle remote device health checks, algorithm updates, and compliance documentation generation, costs that spread evenly across multi-year terms and match reimbursement cycles. Hospitals increasingly justify deals by showing that avoided nursing overtime, faster bed turnover, and reduced device rentals offset monthly subscription fees.

By Application: Patient Tracking Emerges as Growth Driver

Equipment and device tracking accounted for 47.70% of 2025 revenue because locating wheelchairs, IV pumps, and ventilators delivers a quick, measurable return. Yet the next frontier is human-centric tracking. Patient and staff tracking is slated for 27.60% CAGR to 2031, reflecting an operational philosophy where assets, providers, and patients form a single digital ecosystem. When wristbands and badges join tagged devices, care-team orchestration becomes algorithmic, enabling just-in-time delivery of equipment, medication, and specialist intervention.

Hospitals that merge these data layers report significant throughput gains. For example, by binding patient acuity scores, room environmental sensors, and asset availability, a predictive model can pre-stage dialysis machines in units expecting renal patients, slashing admission delays. The healthcare asset management market share for patient-centric applications is on track to eclipse equipment-only systems before 2029. Environmental monitoring remains a complementary use case, safeguarding cold cabinets and isolation suites with continuous temperature and humidity feeds. As software suites standardise API frameworks, cross-application synergies multiply, reinforcing the appeal of end-to-end platforms.

By End User: Pharmaceutical Manufacturing Accelerates

Hospitals and clinics represented 64.40% of turnover in 2025, a testament to early adoption and visible operating gains. Nonetheless, pharmaceutical and biotech plants now display the fastest momentum at 26.10% CAGR, lifted by strict serialisation timelines and cold-chain complexity. The healthcare asset management market size for pharma could top USD 12.85 billion by 2031 as factories retrofit production lines with in-line scanners, embedded sensors, and edge analytics that verify pedigree, temperature, and chain-of-custody in real time. Laboratories and diagnostic centres show steady uptake because grant-funded research protocols increasingly demand traceable reagents and calibrated instrumentation. Meanwhile, long-term-care facilities enter the radar as population ageing intersects with chronic-illness management, amplifying the need for round-the-clock visibility of mobility aids, oxygen concentrators, and smart beds.

Geography Analysis

North America held 37.20% of 2025 revenue, sustained by the United States’ comprehensive serialisation law, a mature EHR backbone, and rising incidents of medical device cyber threats that favour integrated, secure platforms. Canadian provinces are adopting similar policies, while Mexican private-sector hospitals invest in asset tracking to retain medical tourists and satisfy U.S. insurer audits. Government reimbursement models that penalise safety lapses make traceability a board-level metric, further supporting healthcare asset management market adoption across the region.

Asia-Pacific is the fastest-growing area with a 21.90% CAGR expected through 2031. Public-hospital construction programmes in China, India, and Southeast Asia enable greenfield deployments that skip legacy bar-code steps and implement RFID-RTLS convergence from day one. Many of these facilities integrate asset management with national digital-health clouds, allowing real-time drug authentication across regional supply chains. As capital investment aligns with universal health-coverage goals, vendors report multi-year master contracts covering hundreds of new hospitals.

Europe shows steady uptake led by the EU-MDR mandate, EUDAMED database roll-outs, and national sustainability targets that favour lifecycle optimisation. Germany and the United Kingdom drive early deployments, but funding mechanisms in Eastern Europe are catching up as structural funds emphasise digital transformation. Cybersecurity expectations anchored in GDPR elevate demand for on-premises or hybrid clouds with local data residency, nudging platform suppliers to broaden configuration options. With Brexit adding customs complexity for cross-channel medical trade, British providers rely on traceability to avoid port delays and product waste.

Competitive Landscape

The field remains moderately fragmented; no single supplier holds dominant control, yet a cluster of established companies creates a high barrier to newcomers. Stanley Healthcare, CenTrak, and Zebra Technologies benefit from broad portfolios, validated integrations, and nationwide support teams, giving them durable contracts with multi-hospital systems. Vertical specialists such as Securitas Healthcare focus on clinical workflow use cases, while component innovators like Impinj accelerate tag performance for dense metal environments. The market’s middle tier contains analytics startups that layer AI on top of installed RTLS networks, monetising data exhaust instead of hardware.

Consolidation pressures are rising because hospitals dislike stitching together point solutions. Siemens and IBM’s co-engineering agreement illustrates how asset management intersects with lifecycle simulation, bringing design-for-serviceability principles directly into operational dashboards. Vendors compete increasingly on outcome assurances, bundling uptime guarantees, compliance reporting, and cybersecurity insurance into subscription models. Companies capable of unifying device identity, location, and performance analytics inside a single SLA gain negotiation leverage, while hardware-only players risk commoditisation.

Strategic alliances also aim at addressing pharmaceutical cold-chain challenges. Tag manufacturers partner with temperature-controlled packaging firms to embed sensors that survive extreme shipping conditions, turning logistics data into predictive spoilage alerts. On the services side, integration firms hire biomedical engineers and clinical informaticists to provide 24 × 7 command-centre support. This talent mix, expensive to replicate, bolsters switching costs and underpins recurring revenue.

Healthcare Asset Management Industry Leaders

Stanley Healthcare (Stanley Black and Decker)

CenTrak Inc.

AiRISTA Flow Inc.

GE HealthCare Technologies Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GE HealthCare Technologies filed for a USD 650 million senior-notes offering to fund AI-enabled asset-management initiatives.

- March 2025: Beijing Yunji Technology reported 23.2% compound revenue growth to RMB 244.8 million for its robotic hospital-service platform.

- February 2025: Securitas Healthcare earned Best in KLAS recognition for RTLS solutions for the tenth consecutive year.

- February 2025: Motorola Solutions disclosed USD 917 million in 2024 R&D spending, supporting next-generation healthcare communication and tracking systems.

- December 2024: GE HealthCare Technologies secured a USD 1 billion revolving credit facility to expand digital-health product lines.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the healthcare asset management market as all hardware, software, and associated services that enable hospitals, laboratories, and life-science manufacturing sites to locate, monitor, maintain, and optimize physical assets, most commonly through RFID tags, real-time location systems (RTLS), Bluetooth Low Energy, and related analytics platforms.

Scope Exclusion: Facilities services such as catering, cleaning, or non-tracking facilities management contracts are outside this report's boundary.

Segmentation Overview

- By Technology

- RFID

- Real-Time Location Systems (RTLS)

- Bluetooth Low Energy (BLE) and Wi-Fi

- Infrared and Ultrasound

- By Component

- Hardware (Tags, Readers, Gateways)

- Software (Analytics, Middleware)

- Services (Deployment, Managed, Training)

- By Application

- Equipment and Device Tracking

- Inventory/Supply-Chain Management

- Patient and Staff Tracking

- Bed and Capacity Management

- Environmental and Condition Monitoring

- By End-user

- Hospitals and Clinics

- Laboratories and Diagnostic Centers

- Pharmaceutical and Biotech Manufacturing

- Long-Term Care and Assisted-Living Facilities

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Malaysia

- Singapore

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed biomedical engineers at large US and German hospital networks, procurement heads in three APAC teaching hospitals, and solution architects at asset-tracking vendors. Their insights tested adoption rates, average selling prices, and service attach ratios, and helped refine regional weightings suggested by desk research.

Desk Research

Mordor analysts began with publicly available sources such as the US FDA's Unique Device Identification registry, the American Hospital Association annual survey, Eurostat hospital infrastructure files, and customs import datasets from Volza for RFID readers. Industry white papers from groups like GS1 Healthcare, peer-reviewed studies in BMJ Health & Care Informatics, and company 10-Ks enriched quantitative ranges around device counts and tag penetration. Paid databases, D&B Hoovers for supplier revenues and Dow Jones Factiva for deal flow, supplied triangulating financial signals. The sources listed are illustrative; many other primary and secondary references informed our evidence base.

Market-Sizing & Forecasting

A top-down demand pool model converts installed acute-care beds, laboratory bench space, and biopharma clean-room footprints into trackable asset counts. These volumes are multiplied by validated tag densities and blended ASPs. Supplier roll-ups and channel checks act as a selective bottom-up cross-check before totals are finalized. Key variables include average tags per bed, RTLS gateway density per square meter, replacement cycles, capital spend elasticity, regulatory mandates (EU-MDR, US UDI), and staff-to-device ratios. A multivariate regression with ARIMA overlays projects 2026-2030 growth using indicators such as global hospital capital expenditure outlook, RFID price erosion, and regional nurse staffing gaps. Gaps in bottom-up data, common in smaller LatAm facilities, are bridged through regional analogs adjusted by GDP per capita and health spend shares.

Data Validation & Update Cycle

Every model run undergoes variance checks against historical purchase orders, shipment data, and vendor earnings. Senior reviewers challenge anomalies, and revisions trigger re-contact of key experts. Reports refresh annually, with interim updates when material events, such as large recalls or sudden policy shifts, occur. A final analyst pass ensures clients receive the most current view.

Why Mordor's Healthcare Asset Management Baseline Commands Reliability

Published figures often diverge because firms differ on what constitutes an 'asset,' how far service revenues extend, and how frequently they refresh estimates.

Key gap drivers center on scope breadth (hardware only versus hardware plus software plus services), treatment of emerging BLE/ultrasound tags, pricing assumptions for developing markets, and refresh cadence. Mordor's blend of medical facility metrics and cross-verified vendor revenues limits such drift and is revisited each year, whereas others may rely on wider extrapolations or older cost curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 37.9 B (2025) | Mordor Intelligence | - |

| USD 31.5 B (2024) | Global Consultancy A | Software only focus; two-year update lag; narrow primary checks |

| USD 26.9 B (2024) | Publishing Firm B | Excludes BLE and APAC RTLS rollouts; primarily top-down extrapolation |

| USD 18.3 B (2024) | Research House C | Omits services revenue; uses pre-pandemic price points; limited field validation |

The comparison shows that, by anchoring estimates to verifiable device counts, real-world ASPs, and annually refreshed field intelligence, Mordor delivers a balanced, transparent baseline that decision-makers can confidently trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is driving the rapid expansion of the healthcare asset management market?

A mix of regulatory compliance costs, nursing-staff shortages, and rising cybersecurity expectations is converting asset management from a cost-saving project into a strategic necessity, fuelling a 22.85% CAGR toward 2031.

Which technology segment is growing fastest within the healthcare asset management market?

Real-Time Location Systems lead growth with a projected 27.20% CAGR, as hospitals require dynamic location intelligence rather than static identification.

Why are services gaining momentum compared with hardware sales?

Hospitals prefer operational-expense models that bundle uptime guarantees, cybersecurity updates, and compliance reporting, propelling services to a 24.90% CAGR.

How do patient-tracking applications differ from traditional equipment tracking?

Patient and staff tracking unifies human and asset data streams, supporting workflow orchestration that reduces admission delays and boosts throughput; the segment is forecast to grow 27.60% annually.

Which region will contribute most to future market growth?

Asia-Pacific is expected to post a 21.90% CAGR through 2031 thanks to new-build hospitals and government digitisation initiatives that deploy integrated RFID-RTLS platforms from the outset.

What primary obstacle could slow adoption?

High upfront infrastructure cost remains the key restraint, particularly in emerging markets, where full-campus deployments can exceed USD 500,000 before ancillary network upgrades.

Page last updated on: