Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

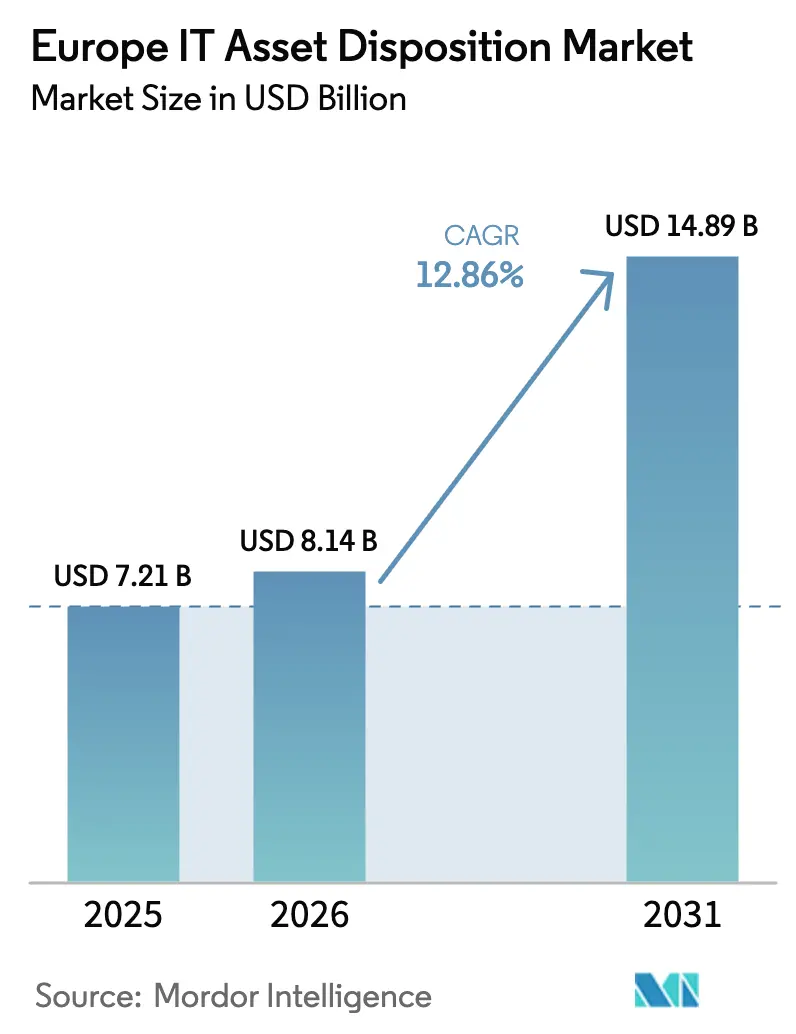

| Base Year Market Size (2025) | USD 7.21 Billion |

| Market Size (2026) | USD 8.14 Billion |

| Market Size (2031) | USD 14.89 Billion |

| Growth Rate (2026 - 2031) | 12.86% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe IT Asset Disposition Market Analysis by Mordor Intelligence

The Europe IT Asset Disposition market size was valued at USD 7.21 billion in 2025 and estimated to grow from USD 8.14 billion in 2026 to reach USD 14.89 billion by 2031, at a CAGR of 12.86% during the forecast period (2026-2031). Mandatory energy-efficiency labels for PCs coming into force in 2026, the Corporate Sustainability Reporting Directive (CSRD) now in effect, and multiyear cloud-migration programs are all combining to lift asset-retirement volumes and reshape provider revenue models. Corporate customers are moving rapidly to refresh entire hardware fleets ahead of the energy-label ban, while Device-as-a-Service agreements bundle disposition into predictable, subscription-style contracts. Take-back incentives from original equipment manufacturers (OEMs) are further supporting remarketing margins, and private-equity roll-ups are knitting together regional refurbishers into cross-border hubs that deliver scale advantages on testing, grading, and logistics.

Key Report Takeaways

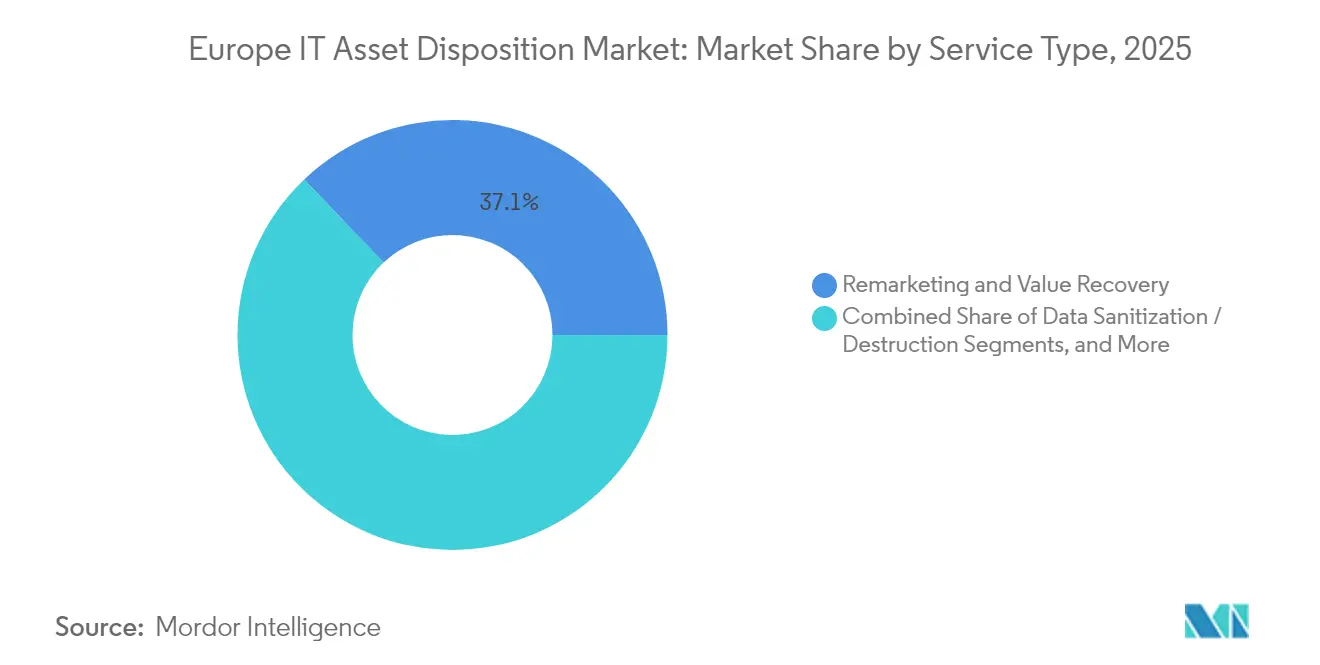

- By service type, Remarketing and Value Recovery led with 37.12% of the Europe IT Asset Disposition market share in 2025, whereas Reverse Logistics and De-installation is projected to surge at 13.48% CAGR through 2031.

- By asset type, Computers and Laptops accounted for 34.92% share of the Europe IT Asset Disposition market size in 2025, while Mobile Devices are forecast to expand at a 14.35% CAGR to 2031.

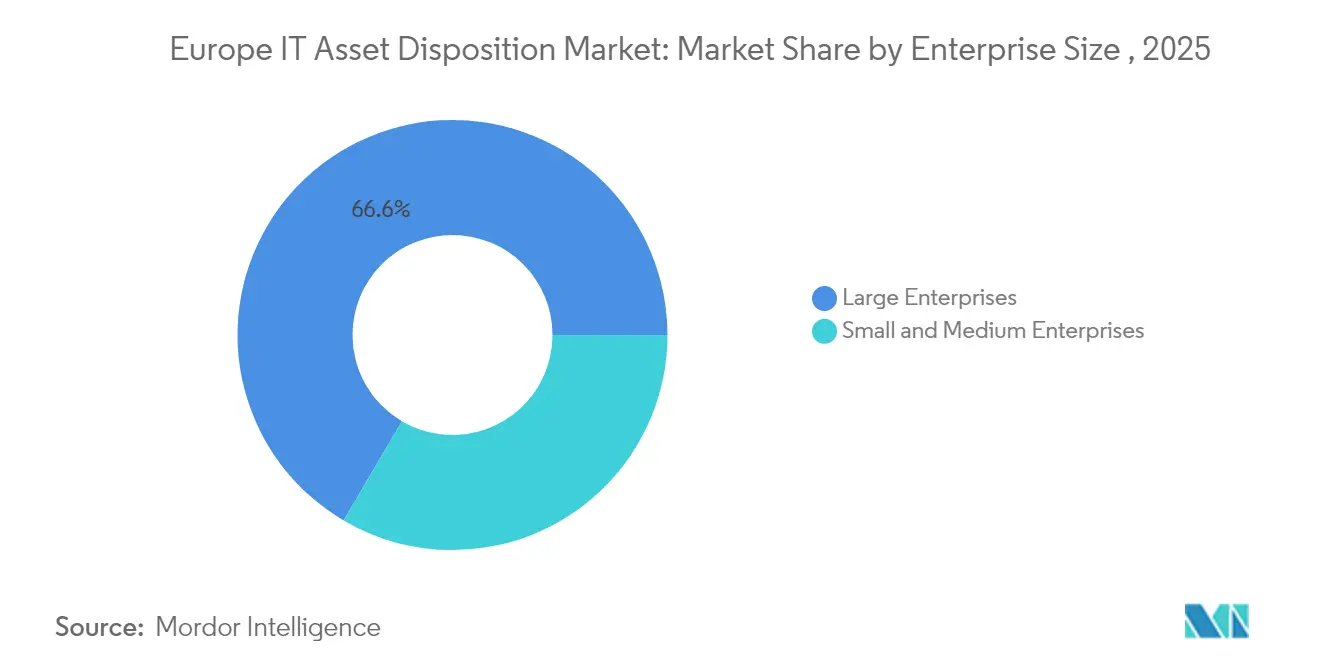

- By enterprise size, Large Enterprises captured 66.55% spending in 2025; Small and Medium Enterprises are advancing at a 14.92% CAGR through 2031.

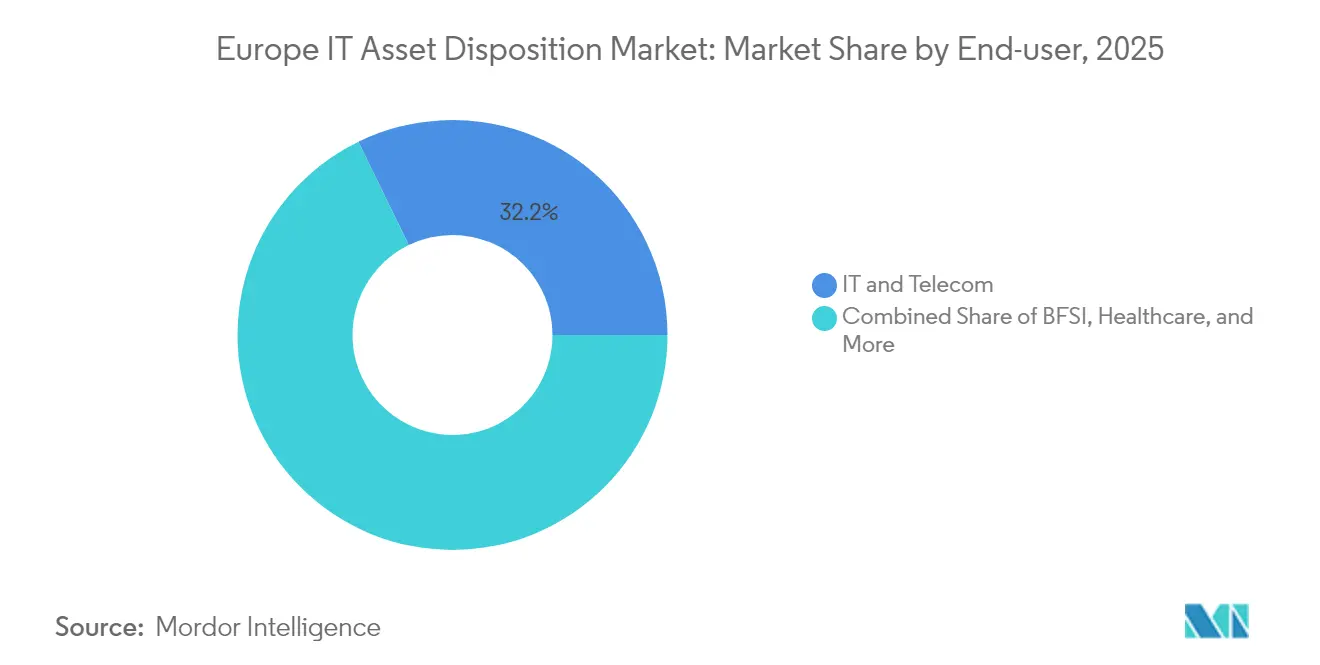

- By end-user vertical, IT and Telecom held 32.21% revenue share in 2025, whereas Healthcare is expected to grow fastest at 13.92% CAGR between 2026-2031.

- By country, the United Kingdom maintained 21.53% of the Europe IT Asset Disposition market share in 2025; Poland shows the highest projected growth at 12.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe IT Asset Disposition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated PC refresh from EU 2026 energy-label ban | +2.1% | EU-27, strongest in Germany, France, Netherlands | Short term (≤ 2 years) |

| Corporate-wide CSRD reporting pushes audited ITAD | +1.8% | EU-27 large enterprises, spillover to United Kingdom and Switzerland | Medium term (2-4 years) |

| OEM take-back schemes subsidise remarketing margins | +1.4% | Global, early adoption in Nordic countries and Germany | Medium term (2-4 years) |

| Shift to Device-as-a-Service contracts bundles ITAD | +1.6% | Western Europe core, expanding to Eastern Europe | Long term (≥ 4 years) |

| Cloud exit from ageing on-premise data-centre hardware | +1.9% | Global, concentrated in business centres | Short term (≤ 2 years) |

| Private-equity roll-ups create pan-EU hubs | +1.3% | Western Europe first, later Central and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated PC Refresh from EU 2026 Energy-Label Ban

The upcoming EU energy-efficiency label effectively removes low-performing computers from sale and pushes enterprises to replace legacy PCs before the 2026 deadline. Many procurement teams are front-loading refresh budgets to avoid non-compliant inventory, which is set to lift Europe's IT Asset Disposition market volumes significantly. Providers able to capture these units early profit from higher residual values before secondary-market saturation sets in, and the regulation dovetails with the broader Ecodesign for Sustainable Products framework that introduces Digital Product Passports starting in 2027.[1]Apple Inc., “Environmental Progress Report 2024,” apple.comAs a result, certified recyclers and refurbishers see a window to lock in supply contracts with large corporates and speed up capacity investments.

Corporate-wide CSRD Reporting Pushes Audited ITAD

From January 2024, the CSRD obliges around 50,000 European companies to disclose Scope 3 emissions, making verifiable end-of-life tracking for devices a board-level issue. Large multinationals are now awarding disposition contracts based on audit readiness, chain-of-custody transparency, and carbon-impact reporting rather than unit fees alone. ITAD providers with integrated data-destruction, recycling, and remarketing workflows, each accompanied by tamper-proof documentation, rise to preferred-supplier status in requests for proposals. Healthcare chains, for instance, increasingly select vendors that can prove Health Insurance Portability and Accountability Act (HITECH) compliance alongside greenhouse-gas savings, moving the Europe IT Asset Disposition market toward service-quality differentiation.

OEM Take-Back Schemes Subsidise Remarketing Margins

OEMs from consumer to industrial electronics now embed trade-in credits that guarantee minimum values for devices returned through authorized ITAD pipelines. Apple’s pledge to use 100% recycled cobalt in all batteries and 99% recycled rare-earth magnets by 2025 sets a benchmark for circularity that pushes enterprises to partner with brand-approved recyclers. Siemens offers pan-EEA return options for packaging and batteries, allowing customers to meet WEEE obligations without sourcing additional vendors.[2]Siemens AG, “Product Return and Recycling Information,” siemens.com These take-back incentives de-risk inventory for ITAD partners, let providers bid more aggressively, and keep high-quality assets in compliant channels.

Shift to Device-as-a-Service Contracts Bundles ITAD

Under Device-as-a-Service, hardware is delivered, supported, and eventually taken back under one multi-year subscription. SHI International, Foxway, and other providers now include certified disposition in the monthly fee, converting lump-sum disposal to recurring cash flow.[3]Foxway, “Annual and Sustainability Report 2024,” foxway.comCustomers gain predictable costs and skip multiple tenders, while providers lock in asset supply and can plan long-term investments in refurbishment lines or shredding equipment. The model aligns with finance teams’ push to classify devices as operating expenditure and meets CSRD data-tracking requirements out of the box.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented WEEE enforcement across EU-27 | -1.2% | Southern and Eastern Europe most affected | Medium term (2-4 years) |

| Inflation-linked logistics costs squeeze margins | -0.9% | High-cost Northern Europe | Short term (≤ 2 years) |

| Grey-market exports erode certified volume | -0.7% | Eastern EU borders | Long term (≥ 4 years) |

| Refurb device stigma among enterprise buyers | -0.5% | Mainly Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented WEEE Enforcement Across EU-27

Regulators interpret WEEE rules differently, so cross-border asset flows must comply with several record-keeping procedures, each adding cost. Germany’s 12.5 kg per-capita e-waste generation contrasts with less-stringent enforcement in Poland, forcing providers to maintain multiple licences and audits, complicating route planning and undermining potential economies of scale. Until harmonisation improves, operators incur duplicated compliance overheads and slower customs clearance on trans-EU lanes.

Inflation-Linked Logistics Costs Squeeze Margins

Fuel, driver wages, and specialised vehicle insurance have all risen, pushing transport to 25% of total disposal cost for low-value devices. Secure vans cannot simply join commodity haulage networks, and pick-ups from dispersed branch offices rarely fill a truck. These economics disadvantage smaller collection runs and erode margin, particularly for assets below USD 50 residual value. Providers respond by clustering pick-up days, investing in telematics for route optimisation, or rolling out on-site shredding to eliminate returns where feasible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Remarketing Remains the High-Value Core

Remarketing and Value Recovery held 37.12% of 2025 revenue, underlining the appetite for refurbished gear that meets budget and sustainability goals. Certified grading and robust warranty programs assure buyers, while OEM take-back schemes buttress minimum buy-back prices, letting providers capture extra margin on resale. Reverse Logistics and De-installation, the fastest-growing line at 13.48% CAGR, reflects multi-site enterprises scheduling simultaneous refreshes ahead of the energy-label deadline. Secure chain-of-custody removal services command price premiums, ensuring data and brand protection throughout transit. Lease Return and End-of-Life Management enjoys a tailwind from finance houses keen to present circular-economy credentials. Data Sanitisation gains steady demand as customers align with ISO 27001 and NIST SP 800-88 protocols.

Integrated contract structures dominate client procurement. Single-vendor frameworks covering collection, erasure, resale, and reporting remove coordination overhead. AI-enabled optical inspection and Internet-of-Things (IoT) trackers improve yield forecasting and increase labour productivity on the testing line. Battery-recovery and urban-mining offerings sit in the “Other” bucket and win share in markets where raw-material scarcity raises the value of critical minerals. Providers that master both component harvesting and full-device resale achieve higher return per kilogram and widen the moat around their platforms. The Europe IT Asset Disposition market thus continues to prize remarketing skills while rewarding logistical precision.

By Asset Type: Smartphones Surge Ahead

Computers and Laptops accounted for 34.92% of 2025 turnover, underpinned by a corporate fleet swap that accelerates through 2026. Yet Mobile Devices, from smartphones to rugged tablets, are the fastest-rising pool at 14.35% CAGR. Shorter two-to-three-year refresh intervals and the bring-your-own-device trend feed unit volumes, while strong secondary demand in Africa and South-East Asia lifts average selling prices. Servers and Storage arrays, although fewer in number, deliver high value density due to gold-plated connectors and aluminium casings. Their disposal schedules align with cloud migration milestones, and strict data-wiping needs make them premium margin for secure ITAD vendors.

Edge computing produces a new wave of micro-servers and gateways scattered across retail or industrial sites, adding collection complexity. Meanwhile, Advania’s Swedish refurbishment centre highlights the scale investments needed to process 1 million devices annually, reinforcing how capacity build-outs set the competitive pace. Emerging streams such as electric-vehicle chargers and renewables control boards sit within “Other Assets” and signal the broader electronic-waste spectrum the Europe IT Asset Disposition market will tackle over the next decade. For each category, providers must balance secure data handling against efficient material harvesting to maximise residual values.

By Enterprise Size: SMEs Become the Next Wave

Large Enterprises controlled 66.55% of spending in 2025, driven by multi-year global refresh plans and complex compliance files that only full-service providers can satisfy. These customers demand integration with asset-management platforms, real-time dashboards for carbon savings, and certificates of destruction within 24 hours of pick-up. Small and Medium Enterprises, however, offer the steepest trajectory at 14.92% CAGR. Greater cloud adoption reduces server counts but speeds up laptop renewal cycles. Rising cyber-risk awareness and CSRD spill-over provisions push SMEs to abandon informal disposal in favour of professional ITAD.

Triangle Ecycling’s focus on biotech firms in North Carolina, although US-based, illustrates how niche specialists package education, social-impact and security messages to resonate with mid-market buyers. European providers replicate this with subscription-style bundles, mobile collection days, and shared-drop programmes at coworking hubs. Digital quoting portals cut transaction cost per asset, unlocking scale even when pick-up volumes stay modest. As regulatory tightens, the Europe IT Asset Disposition market size for SMEs will amplify, encouraging regional providers to standardise offerings and thus narrow the service-quality gap with large enterprise contracts.

By End-User Vertical: Healthcare Outpaces All

IT and Telecom retained 32.21% of revenue in 2025, a logical result of chronic hardware churn, data-security standards, and high unit counts across fixed and mobile assets. Vertical-specific contracts include rigorous chain-of-custody and on-site shredding for failed drives. Healthcare, with a 13.92% CAGR outlook, rises on the back of connected diagnostic equipment, electronic health-record mandates, and bio-pharma digitalisation. Disposal must align with both HITECH and GDPR, lifting the barrier to entry and sustaining price premiums.

BFSI institutions require traceable serial-number reconciliation and multi-factor sign-off: Iron Mountain’s specialised financial-services program is emblematic ironmountain. Manufacturing injects industrial IoT nodes into the waste stream, demanding disassembly of sensors and controllers in line with hazardous-substances rules. Government plugs in as a steady, policy-driven buyer, while newer segments such as renewable-energy operators begin issuing tenders for inverter and battery disposal. Each sector adds its nuances, but all enlarge the addressable Europe IT Asset Disposition market size and raise expectations around carbon-impact accounting.

Geography Analysis

The United Kingdom contributed 21.53% of 2025 revenue, giving it the largest slice of the Europe IT Asset Disposition market. Long-established Waste Electrical and Electronic Equipment (WEEE) frameworks, mature sustainability reporting cultures, and dense clusters of multinational headquarters all converge to create high-value disposal contracts. London’s financial hub demands certified, same-day data destruction, and the nation’s early adoption of circular-economy targets underpins robust take-back volumes. Although Brexit triggered separate filing processes, functional alignment with EU environmental norms ensured cross-border equipment flows continued without material friction.

Germany follows as the second-largest contributor, driven by strict environmental legislation and one of the continent’s highest per-capita technology footprints. With strong manufacturing and automotive bases, the country produces both office-IT and industrial-control waste streams that require specialist treatment. Econocom’s investment in bb-net demonstrates how strategic consolidation seeks to secure refurbishment talent and local customer relationships inside Europe’s biggest economy econocom. France ranks closely behind, buoyed by vigorous enforcement of circular-economy regulations, targeted public funding for recycling infrastructure, and an enterprise culture already steeped in CSR audits. Poland stands out for pace, predicted to clock a 12.88% CAGR to 2031. Fast industrial expansion, rising household incomes, and EU-level co-financing widened the flow of used devices and encouraged foreign players to install processing lines locally. Nordic markets Sweden, Denmark, Finland show high per-capita electronics consumption and regulatory clarity, supporting premium pricing for carbon-scored disposal. The Netherlands, frequently a European logistics gateway, hosts specialised data-centre de-commissioning firms attracted by Amsterdam’s cloud density. Southern European markets such as Italy and Spain trail the North on enforcement consistency but display improving awareness as CSRD reporting obligations ripple down supply chains. Eastern European states, except Poland, continue building formal collection networks, creating white-space for operators willing to partner with municipal agencies.

Competitive Landscape

The Europe IT Asset Disposition market remains moderately fragmented. Global multinationals such as Iron Mountain capitalise on integrated shredding, warehousing, and global compliance frameworks to win multi-country contracts. Regional specialists like TES lean on niche strengths in data-centre de-installation, whereas Foxway differentiates through Device-as-a-Service and consumer-grade web storefronts for refurbished stock.

Consolidation accelerates as private equity hunts scalable circular-economy plays. The 2024-2025 window saw Econocom fold bb-net into its portfolio to gain refurbishment know-how and German coverage. Similar deals are expected in Spain and Italy, where family-owned recyclers seek capital for automation. Technology investments provide another competitive lever: AI vision systems score cosmetic grade in seconds, IoT tags give real-time chain-of-custody, and blockchain pilots test immutable destruction logs. Providers are able to finance equipment upgrades, therefore raising operational efficiency and preserving margin in the face of rising logistics costs.

Strategically, firms strive for vertical integration. OEM take-back partnerships guarantee inbound volume while resale channels capture consumer margins, locking in profitability. Some players explore component harvesting for critical minerals, expanding downstream into smelter partnerships. Competition intensifies in healthcare and BFSI niches where compliance-driven premium pricing attracts newcomers with sector-specific certifications. Despite this, barriers arise from the capital cost of shredders, licences and insurance, keeping entry thresholds significant and sustaining disciplined pricing across the Europe IT Asset Disposition market.

Europe IT Asset Disposition Industry Leaders

Flex IT

Liquid Technology

TecDis

Iron Mountain

Foxway

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Econocom Group reported 3.6% revenue growth to EUR 2.744 billion (USD 2.93 billion) for 2024 and finalised its 80% acquisition of bb-net, adding EUR 17 million (USD 18.1 million) in annual refurbishment revenue into its circular-economy portfolio.

- January 2025: SK tes expanded its Recklinghausen, Germany processing centre after repurposing 6 million assets and handling 101,766,393 kg of equipment across 40+ global sites in 2023.

- November 2024: DMD Systems Recovery purchased Basket Materials to deepen Bay-Area coverage and lower transportation emissions for West-Coast clients.

- May 2024: Foxway’s Annual Report showed 32% revenue growth to SEK 7.4 billion (USD 6.8 billion) in 2023, boosted by acquiring Teqcycle GmbH and Global Resale Ltd.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every revenue stream that European providers earn when they collect, wipe, refurbish, remarket, recycle, or certify the final destruction of end-of-life IT hardware, from laptops and servers to mobile devices and storage arrays. The valuation covers service fees and residual hardware sale proceeds expressed in 2025 US dollars.

Scope exclusions include devices handled purely in-house by corporates without third-party documentation, and scrap metal trade that is not traceable to an IT asset, which sit outside the model.

Segmentation Overview

- By Service Type

- Data Sanitization / Destruction

- Remarketing and Value Recovery

- Reverse Logistics and De-installation

- Lease-Return / End-of-Life Mgmt.

- Others

- By Asset Type

- Computers and Laptops

- Mobile Devices

- Servers and Storage

- Others

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Vertical

- BFSI

- IT and Telecom

- Healthcare

- Government and Public Institutions

- Manufacturing

- Others

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Nordics (Sweden, Denmark, Finland)

- Poland

- Russia

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews and online surveys with certified ITAD vendors, logistics partners, audit consultants, and sustainability officers across multiple EU economies helped us verify asset mixes, data-wipe failure rates, and typical remarketing discounts. Follow-ups with regulatory experts clarified gray areas in cross-border shipment rules and country-level WEEE fee structures.

Desk Research

We started with public datasets that anchor the disposal universe, such as Eurostat e-waste generation tables, the European Environmental Agency's WEEE collection reports, ENISA breach-notification statistics, and OECD trade dashboards that map outbound second-hand equipment flows. Company 10-Ks, investor decks, and procurement portals supplied average selling prices and lease durations, while government tender logs revealed contract volumes for large data-center decommissioning projects.

To enrich the financial picture, our analysts tapped D&B Hoovers for privately held dealer revenues and Dow Jones Factiva for press releases on plant expansions. These sources illustrate our approach only; many other web portals, academic papers, and association white papers informed smaller cross-checks.

Market-Sizing & Forecasting

We built a top-down model that scales the region's documented e-waste tonnage by device-class shares and business-only penetration, then multiplies the recoverable units by service uptake rates confirmed in interviews. Bottom-up checks, including sample dealer roll-ups and channel ASP volume snapshots, flag outliers before totals are finalized. Key variables include enterprise PC installed base, average refresh cycle length, certified data-erasure incidence, prevailing remarketing prices, and WEEE compliance costs. A multivariate regression, with GDP growth, corporate sustainability spending, and cyber-breach fines as predictors, projects values through 2030. Gap pockets in bottom-up data are bridged by weighted averages from nearest neighbor markets.

Data Validation & Update Cycle

Our two-step analyst review inspects variance against historical ratios and peer benchmarks, and any anomaly above three percentage points triggers a source recheck. Models refresh annually; material events such as a WEEE directive amendment or a major plant closure prompt an interim update, after which a fresh analyst pass precedes report release.

Why Our Europe IT Asset Disposition Baseline Commands Reliability

Published estimates often diverge because firms choose dissimilar asset lists, revenue inclusions, and forecast drivers. We acknowledge those variances upfront and show how disciplined scope setting and yearly refreshes steady Mordor's baseline.

Key gap drivers include some publishers omitting value-recovery proceeds, others working with global extrapolations that ignore national WEEE return rates, and a few carrying forward 2022 price decks without currency harmonization, which inflates variance when the euro shifts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.21 bn (2025) | Mordor Intelligence | - |

| USD 6.72 bn (2024) | Global Consultancy A | Excludes remarketing revenue and models only reported disposal fees |

| USD 2.76 bn (2024) | Research Boutique B | Covers five Western EU countries; relies on dated ASPs and no primary validation |

Taken together, the comparison shows that Mordor's clear scope boundaries, live price deck, and blended top-down/bottom-up corroboration yield a balanced, decision-ready baseline that clients can retrace and replicate with publicly available inputs.

Key Questions Answered in the Report

What is driving the rapid growth of the Europe IT Asset Disposition market through 2031?

Mandatory EU energy-efficiency labels for PCs, CSRD-driven audit requirements, cloud data-centre de-commissioning, and bundled Device-as-a-Service contracts are combining to lift asset-retirement volumes and accelerate market expansion at a 12.86% CAGR.

Which service line currently generates the most revenue?

Remarketing and Value Recovery leads with 37.12% of 2025 revenue, reflecting enterprise focus on residual-value capture and compliance-aligned resale channels.

Why are Mobile Devices forecast to outpace other asset types?

Smartphone refresh cycles are shortening, enterprise mobile fleets are expanding, and high secondary-market demand drives a 14.35% CAGR for Mobile Devices through 2031.

How important are Small and Medium Enterprises to future market growth?

SMEs show the fastest spending increase at 14.92% CAGR because rising cyber-security awareness and CSRD spill-over rules are pushing smaller firms toward professional ITAD services.

Which European country is expected to grow quickest?

Poland is projected to advance at 12.88% CAGR due to rapid economic development, technology-manufacturing clusters, and EU-funded recycling infrastructure build-out.

What competitive factors matter most when selecting an ITAD provider?

Enterprises typically weigh proof of secure data destruction, carbon-impact reporting, geographic coverage, and the provider’s ability to remarket devices to maximise residual value.

Page last updated on: