Oscillator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.87 Billion |

| Market Size (2031) | USD 9.52 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

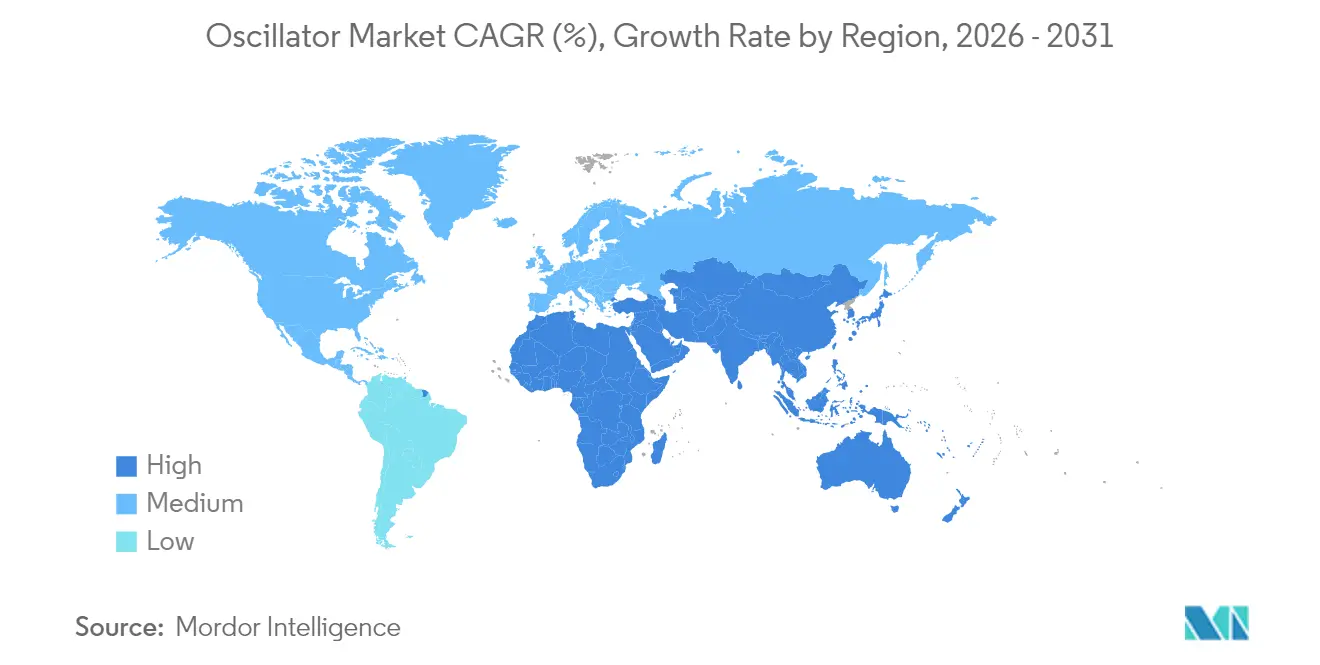

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

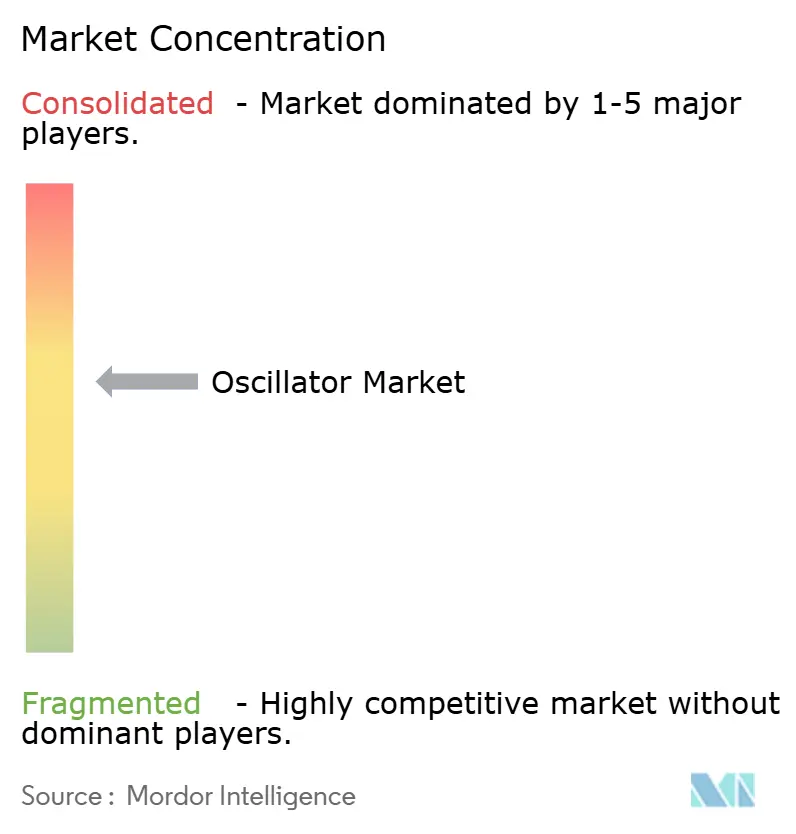

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oscillator Market Analysis by Mordor Intelligence

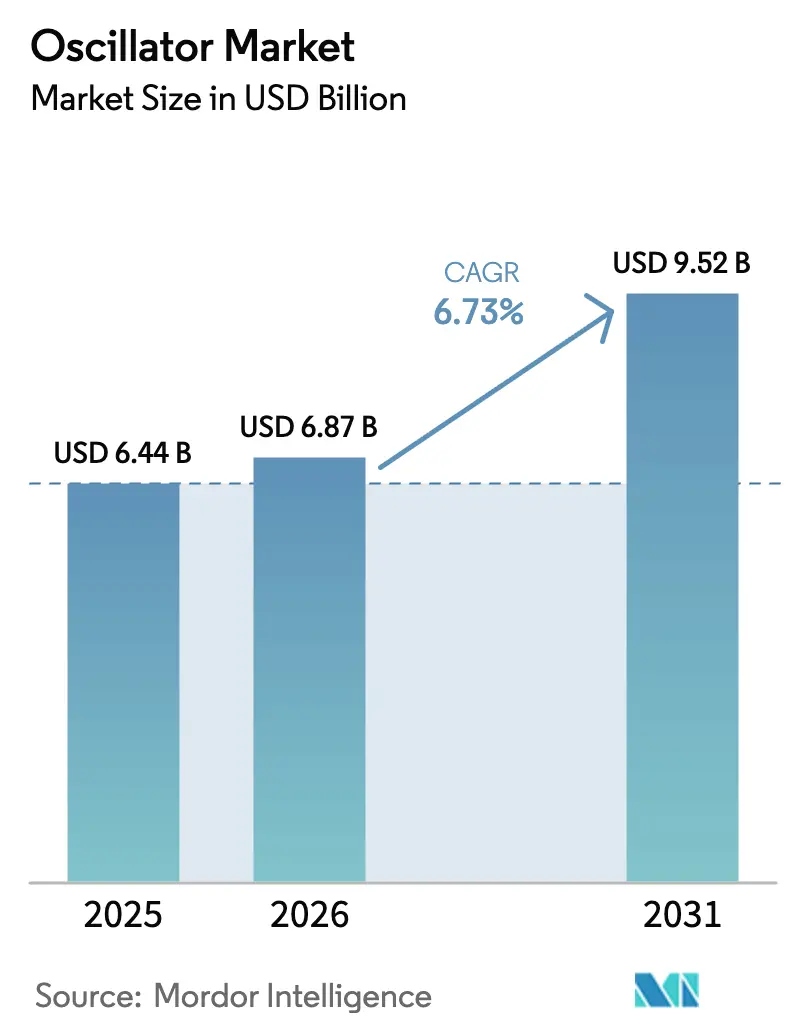

oscillator market size in 2026 is estimated at USD 6.87 billion, growing from 2025 value of USD 6.44 billion with 2031 projections showing USD 9.52 billion, growing at 6.73% CAGR over 2026-2031. Growth has hinged on widening 5G roll-outs, the rapid electrification of vehicle electronics, and rising low-Earth-orbit satellite deployments that all require tighter timing accuracy. Device makers also benefited from demand for ultra-low-jitter clocks in AI data-center GPUs and from automotive migration toward zonal architectures that favor robust MEMS timing. Meanwhile, concerns over quartz blank concentration in Japan encouraged many original-equipment manufacturers (OEMs) to validate multi-sourced silicon-based alternatives.[1]SiTime, “Why MEMS Outperforms Quartz in Precision Timing,” sitime.com

Key Report Takeaways

- By product type, Temperature-Compensated Crystal Oscillators led with 33.60% of oscillator market share in 2025, while MEMS oscillators are expected to expand at 17.4% CAGR through 2031.

- By mounting scheme, surface-mount devices commanded 76.40% share of the oscillator market size in 2025 and are projected to grow at 6.05% CAGR to 2031.

- By material, quartz retained 89.30% share in 2025, yet silicon-MEMS clocks are projected to post the same 17.4% CAGR that makes them the fastest material class.

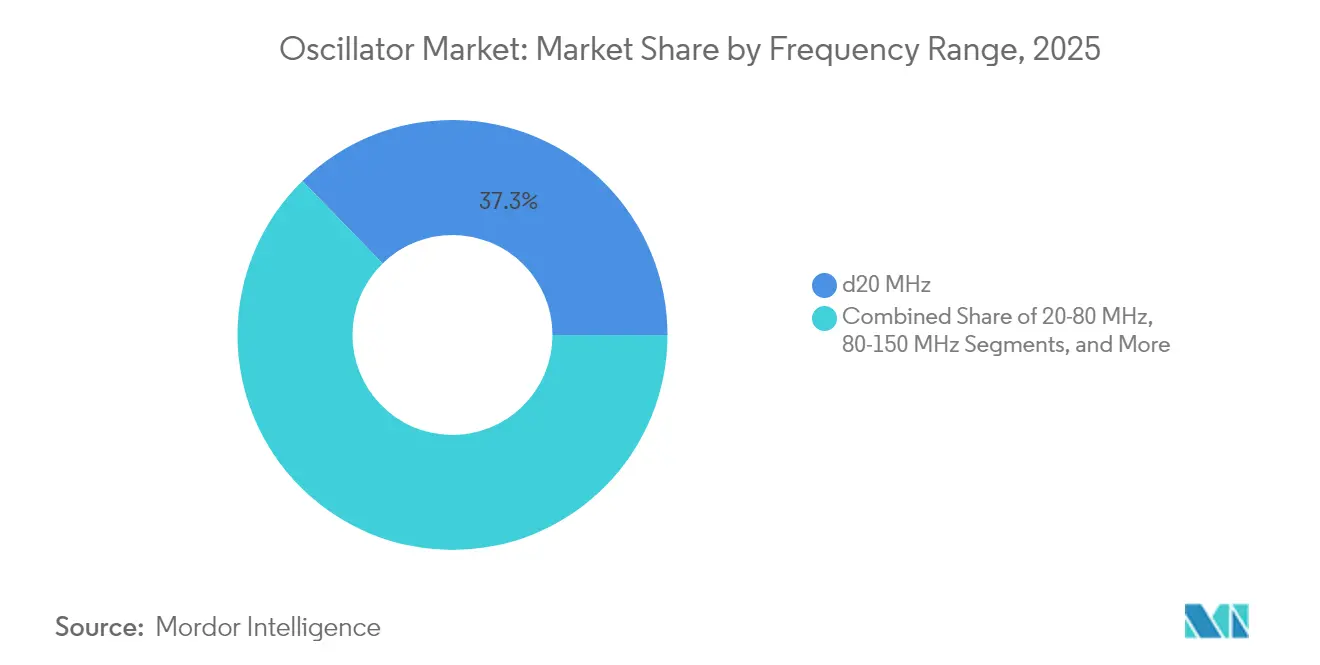

- By frequency range, the ≤20 MHz category captured 37.30% of oscillator market share in 2025; the >150 MHz tier shows the quickest 10.1% CAGR through 2031.

- By end-user industry, consumer electronics accounted for 37.60% of the oscillator market size in 2025 whereas automotive is advancing at an 8.6% CAGR to 2031.

- By geography, Asia-Pacific dominated with 58.50% revenue share in 2025, and the Middle East and Africa region is forecast to post a 9.05% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oscillator Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G small-cell roll-outs requiring ultra-low-jitter TCXOs | +1.8% | Asia-Pacific, North America, Europe | Short term (≤ 2 years) |

| Electrification of ADAS domain controllers elevating MEMS oscillator ASPs | +1.5% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Migration from legacy MCU clocks to programmable XOs in over-the-air updatable IoT modules | +1.2% | Global, with emphasis on North America, Europe, China | Medium term (2-4 years) |

| Aerospace LEO-satellite fleet expansion fueling OCXO demand | +0.9% | North America, China, Europe | Long term (≥ 4 years) |

| SC-Cut crystal adoption for mmWave backhaul links | +0.7% | Europe, North America, Japan | Medium term (2-4 years) |

| Emergence of automotive Ethernet-TSN synchronisation driving VCXO volumes | +0.6% | Japan, South Korea, Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Small-Cell Roll-outs Requiring Ultra-Low-Jitter TCXOs

Extensive 5G densification forced operators to deploy millions of small cells, each needing timing accuracy of ±130 ns. Manufacturers, therefore, designed TCXOs with ≤0.1 ppm jitter, such as CTS Corporation’s 535/536 series, which sustained stability from −40 °C to +105 °C. Asia led these installations, with China and South Korea consuming the bulk of premium clocks. Migration from GPS-disciplined timing in 4G toward IEEE 1588 PTP widened addressable demand, while network operators in North America and Europe mirrored Asian specifications to maintain interoperability. Resulting pull-through volumes steadily enlarged the oscillator market across both quartz and MEMS variants.

Electrification of ADAS Domain Controllers Elevating MEMS Oscillator ASPs

Vehicle OEMs replaced multiple distributed electronic control units with centralized ADAS domain controllers that consolidate sensor fusion workloads. The Renesas R-Car V4H SoC integrates a programmable clock generator to support 34 TOPS of AI inferencing, illustrating rising oscillator precision requirements.[2]Renesas Electronics, “R-Car V4H,” renesas.com MEMS devices gained preference because their single-crystal silicon structure survives 30,000 g shock and offers low g-sensitivity—attributes essential in harsh automotive environments. As vehicles move to zonal architectures, timing components per car increase, tilting the oscillator market mix toward higher-margin MEMS products.

Migration from Legacy MCU Clocks to Programmable XOs in Over-the-Air Updatable IoT Modules

IoT suppliers moved beyond fixed-frequency crystals to field-programmable XOs that permit cloud-based firmware to retune clock speed. Silicon Labs’ EFR32xG21 platform incorporates multiple on-chip oscillators that can be trimmed remotely, allowing power optimisation without physical recalls. This flexibility extends device life cycles in smart-metering, asset-tracking, and industrial monitoring deployments, broadening global oscillator market penetration. Cloud-managed timing also provided a cybersecurity benefit by mitigating timing-side-channel vulnerabilities post-deployment.

Aerospace LEO-Satellite Fleet Expansion Fueling OCXO Demand

Constellations such as Starlink and OneWeb collectively orbited hundreds of LEO satellites, each demanding oven-controlled crystal oscillators that sustain sub-ppb stability for inter-satellite links. FrontierSI identified position-navigation-timing services as a new use case that compounds precision requirements. MEMS OCXOs like SiTime’s Endura family offered 50 × lower acceleration sensitivity than quartz, conforming to MIL-PRF-55310 standards critical for launch survivability. Steady launch cadence pushed long-term demand, anchoring a strategic growth pillar within the oscillator market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain single-source dependency on quartz blanks from Japan | −0.7% | Global, highest impact on North America, Europe | Medium term (2-4 years) |

| MEMS-XO phase-noise limitation below 100 kHz offset in 5G infrastructure | −0.5% | Asia-Pacific, North America, Europe | Short term (≤ 2 years) |

| Design-in cycles >5 years in tier-1 automotive ECUs | −0.4% | Global, emphasis on Europe, Japan, North America | Long term (≥ 4 years) |

| Export-control regimes on OCXO/EMXO for military end-use | −0.3% | North America, Europe, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Single-Source Dependency on Quartz Blanks from Japan

Roughly 80% of high-grade quartz blanks came from Japan, exposing global manufacturers to geopolitical or natural-disaster disruptions Seiko. Lengthy crystal-growing and polishing cycles further constrained recovery speeds when incidents occurred. Device vendors countered by dual-sourcing with MEMS oscillators fabricated in standard semiconductor fabs located across North America, Europe, and Asia. Nevertheless, mission-critical clients that still require legacy quartz grades retained conservative qualification policies, limiting short-term substitution in parts of the oscillator market.

MEMS-XO Phase-Noise Limitation Below 100 kHz Offset

While MEMS clocks excelled in vibration and temperature stability, silicon resonators historically lagged quartz in ultra-low phase noise at <100 kHz offsets, an attribute vital for 5G basestations. Network planners worried that elevated noise floors would degrade error-vector-magnitude performance in high-order modulation schemes. Suppliers responded with digitally compensated “super-TCXO” architectures that combine temperature control and DSP filtering to approach quartz noise floors. Continued research and development are expected to narrow the gap, yet this constraint presently tempers adoption in premium telecom infrastructures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: MEMS Reshapes Timing Hierarchy

TCXOs retained the largest 33.60% slice of oscillator market share in 2025 because telecom OEMs valued their cost-to-performance balance. MEMS devices, however, recorded an 17.4% CAGR outlook that is steering future oscillator market expansion toward silicon-based designs. Reliability at 50 × quartz levels, coupled with micro-packaged form factors below 2 mm², makes MEMS attractive for wearables, drones, and EVs. OCXOs still dominate satellite payloads where ±5 ppb stability is non-negotiable. SPXOs serve price-sensitive gadgets, whereas VCXOs supply video broadcast equipment requiring frequency pullability.

The oscillator industry witnessed a migration from construction-based labels toward application-centred definitions; aerospace now requests radiation-tolerant EMXOs, and IoT integrators demand field-programmable FCXOs. This re-categorisation helped smaller innovators target niches rather than compete head-on with large quartz companies. Consequently, competitive dynamics shifted as MEMS-centric firms secured design wins in spaces once monopolised by quartz. The oscillator market benefits from this specialization because each performance envelope—be it vibration, radiation or temperature extremes—receives a tailored solution set rather than a one-size-fits-all device.

By Mounting Scheme: Surface-Mount Sustains Miniaturisation Momentum

Surface-mount packages controlled 76.40% of the oscillator market in 2025, owing to pick-and-place efficiency and reduced board real estate. The 6.05% projected CAGR illustrates how OEM roadmaps favour ever-smaller footprints, such as 1.6 × 1.2 mm outlines introduced for wearable sensors. Through-hole parts remained in rail, avionics and heavy-industrial platforms where board rigidity outranks size.

Advanced packaging merged multiple resonators, voltage regulators and dividers into single system-in-package blocks, slashing component counts for designers. Automotive and medical customers championed such integration to shrink bill-of-material line items while raising reliability via reduced solder joints. Over the forecast horizon, automated optical inspection thresholds and reflow temperature constraints will further push the oscillator market toward surface-mount exclusivity except where severe vibration or serviceability dictates sockets.

By Material: Silicon Challenges Quartz’s Historical Stronghold

Quartz represented 89.30% of 2025 market share yet MEMS silicon resonators are pegged for the quickest 17.4% CAGR. Automotive contracts accelerated the shift because MEMS withstand high-G crash events and −40 °C to +125 °C ranges without aging drift. Ceramic and SAW substrates filled specialist roles such as microwave front-ends that need high-Q performance.

Materials science innovation continued on both fronts; quartz laboratories reported 10 × sensitivity gains in biosensing via elliptical electrodes. MEMS manufacturers refined epi-seal vacuum encapsulation to trap resonators in hermetic silicon cavities, halving motional resistance and extending lifetime. The oscillator market therefore no longer views material categories as binary rivals but as complementary toolkits to match application trade-offs around cost, power and stability.

By Frequency Range: Demand Climbs Into High-GHz Territory

The ≤20 MHz bracket accounted for 37.30% of the oscillator market size in 2025, anchored by wristbands, remote controls, and basic MCU timing. Yet the >150 MHz slice is set for 10.1% CAGR through 2031 as 5G backhaul, millimetre-wave radars and multi-core processors crave higher carrier frequencies. Middle tiers between 20 MHz and 150 MHz serviced fiber-optic modules and networking cards that need moderate speeds with low phase noise.

Emerging 27.5–29.5 GHz antenna arrays for 6G research magnify the importance of cutting-edge SC-cut crystals and hybrid MEMS-SAW combinations that keep noise floors at bay. Consequently, oscillator suppliers offer family lines optimised for discreet frequency windows instead of stretching a single architecture across decades of bandwidth. This segmentation lets the oscillator market capture value by aligning price points, size and operating temperature to each band’s technical ceiling.

By End-User Industry: Automotive Surges While Consumer Holds Volume Crown

Consumer electronics maintained 37.60% revenue share in 2025 as every smartphone uses dozens of timing nodes. Connected vehicles, however, are racing ahead with an 8.6% CAGR thanks to ADAS, battery-management systems and in-vehicle infotainment. Telecom carriers remained vital patrons, particularly for ultra-stable clocks inside 5G gNodeBs. Aerospace and defense clients demanded the highest-grade OCXOs and newly qualified MEMS parts for CubeSats.

Industrial automation and factory Ethernet synchronisation also gathered pace, reinforcing growth beyond cyclical consumer gadgets. Automotive ethernet PHYs such as Texas Instruments’ DP83TC818S-Q1, highlighted how hardware designers now embed time-sensitive networking features that depend on sub-µs clock precision. As each vertical deepens electronic content, the oscillator market benefits from a broader mix of margin profiles, buffering suppliers against single-sector downturns.

Geography Analysis

Asia-Pacific dominated 58.50% of 2025 revenue, propelled by China’s smartphone production hubs, Japan’s quartz supply dominance and South Korea’s early adoption of 5G small cells. Taiwan’s foundries and timing-component vendors such as TXC Corporation anchored regional self-sufficiency, while India attracted greenfield fabs from companies like Rakon to diversify supply. Strong local demand plus export momentum kept the oscillator market growth curve steep despite pockets of trade tension.

North America ranked second; its defense primes and New-Space launch providers bought premium OCXOs and radiation-tolerant MEMS. Data-center operators pursued super-TCXOs that cut GPU idle cycles in AI clusters, reinforcing domestic development funding. Automotive tier-1s based in the United States and Canada validated MEMS clocks for centralised ADAS compute, further enlarging the regional oscillator market.

Europe remained influential, particularly within Germany’s vehicle ecosystem and the continent’s strong industrial automation base. SC-cut crystals gained popularity in mmWave backhaul links to meet European Commission spectrum mandates. Export-control frameworks occasionally slowed shipment cycles for high-precision military oscillators, yet domestic champions in France and the United Kingdom kept specialty production alive. The Middle East and Africa recorded the fastest 9.05% CAGR outlook as Gulf smart-city projects and African telecom expansions modernised infrastructure. South America, led by Brazil, showed steady but modest uptake tied to 4G/5G network upgrades. Collectively, these regional patterns ensured the oscillator market retained a geographically diverse demand structure.

Competitive Landscape

Incumbent quartz manufacturers sought to preserve their share by refining frequency stability and offering extended temperature grades, whereas MEMS-centric challengers emphasized reliability, integration, and shorter lead times. SiTime’s Epi-Seal technology sealed its resonators in vacuum cavities to eliminate particulate contamination, yielding 50 × reliability gains over quartz SiTime. Microchip Technology extended its footprint by acquiring BAW and SAW specialists, allowing the bundling of mixed resonator portfolios for 5G timing decks.

Merger and Acquisition momentum continued: Infineon bought Marvell’s automotive Ethernet business for USD 2.5 billion, aligning timing with in-vehicle networking silicon. VIAVI announced plans to acquire Spirent Communications to strengthen 5G testing capabilities that depend on precision clocks. Such moves illustrate how timing products increasingly intertwine with complete subsystems rather than remaining stand-alone components.

Regulatory shifts shaped strategy as well. The U.S. Bureau of Industry and Security expanded the Foreign-Produced Direct Product Rule to cover advanced timing devices, compelling exporters to tighten compliance pipelines. Suppliers responded by delineating civil versus defense part numbers and re-shoring assembly lines. Overall, the oscillator market continues to see technology-driven competition where speed of innovation and flexible manufacturing outrank mere volume scale.

Oscillator Industry Leaders

Murata Manufacturing Co. Ltd

Seiko Epson Corp.

Nihon Dempa Kogyo (NDK) Co., Ltd.

Kyocera Corporation

SiTime Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Abracon launched several MEMS oscillator lines targeting space-constrained electronics.

- April 2025: SiTime posted USD 202.7 million revenue for FY 2024, up 41% year-over-year on strong MEMS uptake.

- April 2025: Infineon acquired Marvell’s automotive Ethernet unit for USD 2.5 billion to bolster TSN synchronization capabilities.

- January 2025: Research from SiTime confirmed 50 × reliability advantage of silicon MEMS over quartz.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the oscillator market covers every discrete quartz, MEMS, thin-film, and surface-acoustic-wave device that converts direct current into a stable, periodic electrical signal used for timing, clocking, or carrier generation across consumer, telecom, automotive, industrial, medical, and aerospace electronics. Revenue is booked at factory gate for new surface-mount and through-hole units; multi-chip timing modules sit in a separate study.

Scope Exclusions: miniature atomic clocks and standalone RC or LC oscillators are outside this scope.

Segmentation Overview

- By Product Type

- Temperature-Compensated XO (TCXO)

- Voltage-Controlled XO (VCXO)

- Oven-Controlled XO (OCXO)

- Simple-Packaged XO (SPXO)

- Frequency-Controlled XO (FCXO)

- MEMS Oscillator (Si-MEMS)

- Evacuated Miniature XO (EMXO)

- By Mounting Scheme

- Surface-Mount Device (SMD)

- Through-Hole

- By Material

- Quartz

- Silicon-Based MEMS

- Ceramic / SAW

- By Frequency Range

- ≤20 MHz

- 20–80 MHz

- 80–150 MHz

- >150 MHz

- By End-User Industry

- Consumer Electronics

- Telecom and Networking

- Automotive

- Aerospace and Defense

- Industrial and Manufacturing

- Medical and Research

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- Taiwan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- GCC Countries

- Turkey

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview oscillator design engineers, component distributors, automotive Tier-1 timing leads, and telecom RAN planners across Asia-Pacific, North America, and Europe. Their insights on attach rates, ASP shifts, and qualification cycles validate desk findings and tighten model assumptions.

Desk Research

We start with public datasets, UN Comtrade code 854160 shipments, ITU 5G build-outs, OICA vehicle tallies, WSTS semiconductor indices, and IEEE papers to frame demand baselines. Trade bodies such as JEITA, SEMI, IPC, and SAE, plus regulatory filings, add technology cadence and pricing cues. Company 10-Ks alongside paid snapshots from D&B Hoovers and Dow Jones Factiva enrich revenue splits. This list is illustrative; many additional sources inform the model.

Market-Sizing & Forecasting

We deploy a top-down build that multiplies device-level oscillator content into global outputs for smartphones, 5G radios, EV control units, and LEO satellites, then cross-check with sampled supplier roll-ups (units × blended ASP). Five variables, 5G site growth, MEMS share, quartz price erosion, low-jitter premium uptake, and automotive ADAS penetration, anchor a multivariate regression producing 2025-2030 values. Outliers prompt iterative reviews before freeze.

Data Validation & Update Cycle

Each draft passes automated variance screens, a peer review within the devices desk, and senior sign-off. We refresh annually and issue interim updates whenever material events such as M&A, export rules, or macro shocks shift assumptions.

Why Mordor's Oscillator Baseline Commands High Reliability

Published numbers differ because firms mix device scopes, price points, and refresh cadences. We flag these drivers so users understand divergences before budgeting.

Key gap drivers: many external studies exclude MEMS, lift list prices without discount factors, or roll forward 2023 volumes without adjusting for 5G small-cell surges and MEMS wins that Mordor analysts capture through quarterly channel calls; some also convert currencies at spot rather than period averages.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.44 B (2025) | Mordor Intelligence | - |

| USD 2.89 B (2025) | Global Consultancy A | MEMS omitted; list prices; five-year refresh |

| USD 3.26 B (2025) | Trade Journal B | Telecom-centric scope; spot FX; limited regions |

These contrasts show that Mordor's blended-price, device-inclusive, annually updated approach delivers a balanced baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size and projected growth of the global oscillator market?

The oscillator market stood at USD 6.87 billion in 2026 and is forecast to reach USD 9.52 billion by 2031, advancing at a 6.73% CAGR.

Which oscillator type shows the strongest growth outlook?

MEMS oscillators hold the fastest trajectory with an 17.4% CAGR expected for 2026-2031, driven by superior shock resistance, compact size and high reliability.

How do 5G roll-outs influence oscillator demand?

Dense 5G small-cell networks require ultra-low-jitter TCXOs with ±130 ns accuracy, steadily lifting volumes for precision timing components across Asia, North America and Europe.

Why are automotive applications accelerating oscillator adoption?

Centralised ADAS domain controllers, zonal vehicle architectures and Automotive Ethernet-TSN protocols together push oscillator use in vehicles, resulting in an 8.6% CAGR for the automotive segment.

What supply-chain risks should executives watch?

Around 80% of high-grade quartz blanks originate in Japan, creating a single-source bottleneck that encourages dual-sourcing with silicon-based MEMS alternatives.

Which geographic market is set to grow the fastest?

The Middle East and Africa region shows the highest expansion rate, with a projected 9.05% CAGR from 2026-2031 as telecom and industrial automation investments rise.

Page last updated on: