Semiconductor Bonding Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

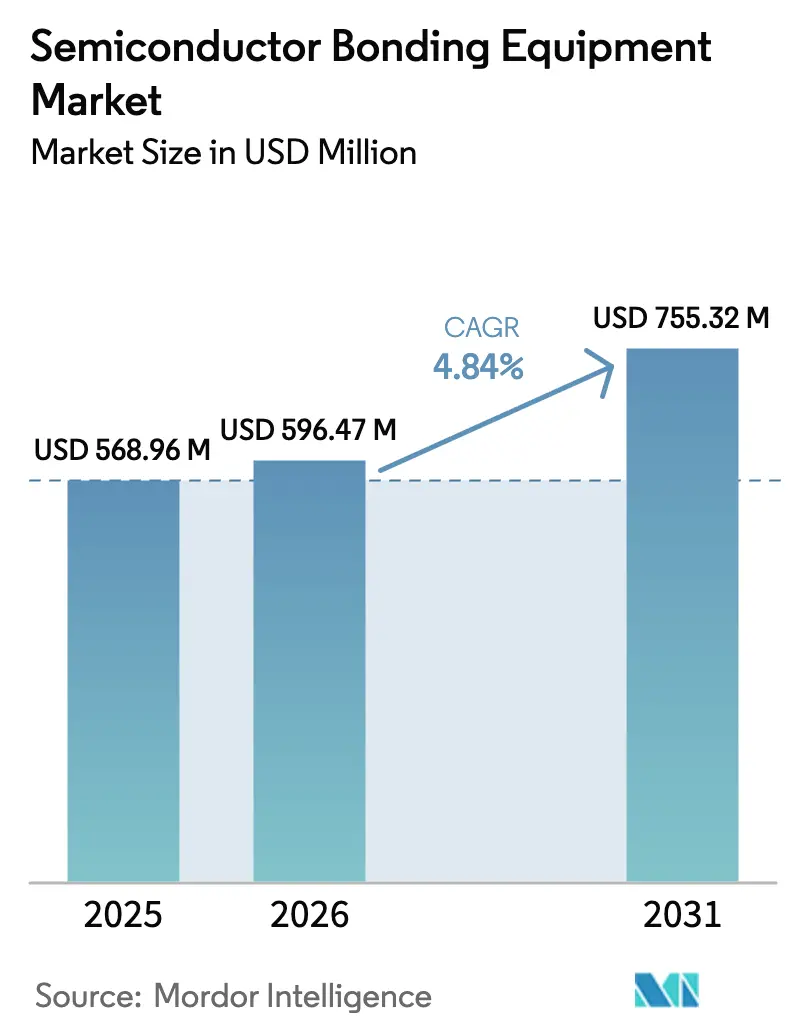

| Market Size (2026) | USD 596.47 Million |

| Market Size (2031) | USD 755.32 Million |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

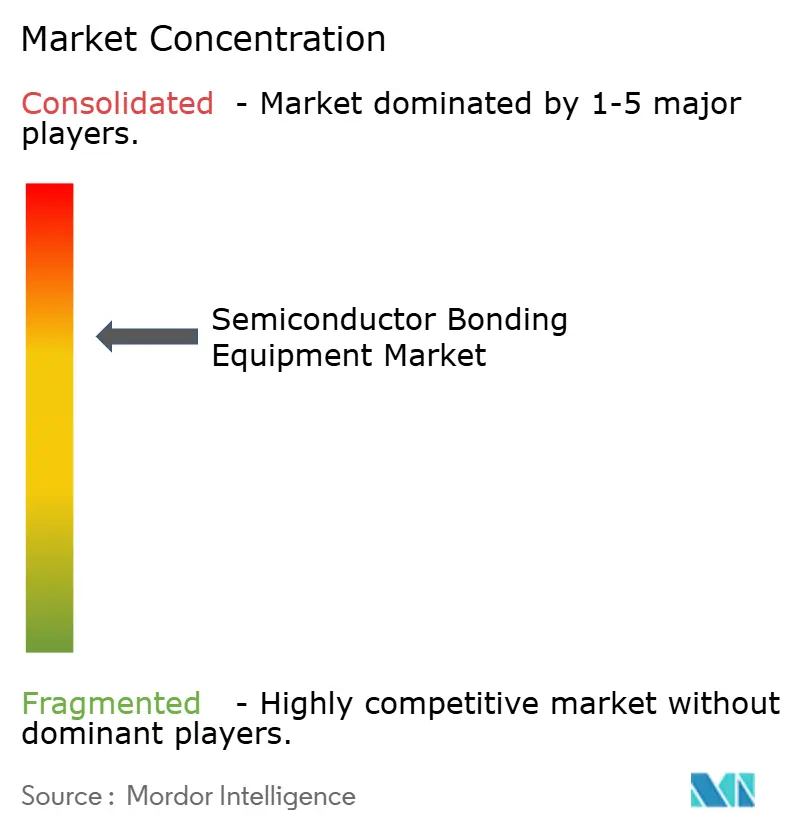

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Semiconductor Bonding Equipment Market Analysis by Mordor Intelligence

The semiconductor bonding equipment market size in 2026 is estimated at USD 596.47 million, growing from 2025 value of USD 568.96 million with 2031 projections showing USD 755.32 million, growing at 4.84% CAGR over 2026-2031. Demand growth mirrors the industry shift from planar scaling to vertical stacking, where heterogeneous integration strategies require precise wafer-to-wafer and die-to-wafer connections. Leading chipmakers have accelerated capital spending on advanced packaging lines to improve bandwidth, latency, and energy efficiency for AI accelerators and high-performance computing devices. Hybrid copper-to-copper processes are eclipsing conventional wire bonding as sub-3 nm nodes move into risk production, raising alignment-accuracy demands below 10 µm. At the same time, automotive electrification and IoT miniaturization widen the application footprint, expanding order books for permanent, temporary, and hybrid platforms. However, the high total cost of ownership and tighter environmental rules on volatile organic compounds add pressure to sustain utilization levels above 70%, prompting buyers to negotiate full-service contracts and predictive-maintenance packages.

Key Report Takeaways

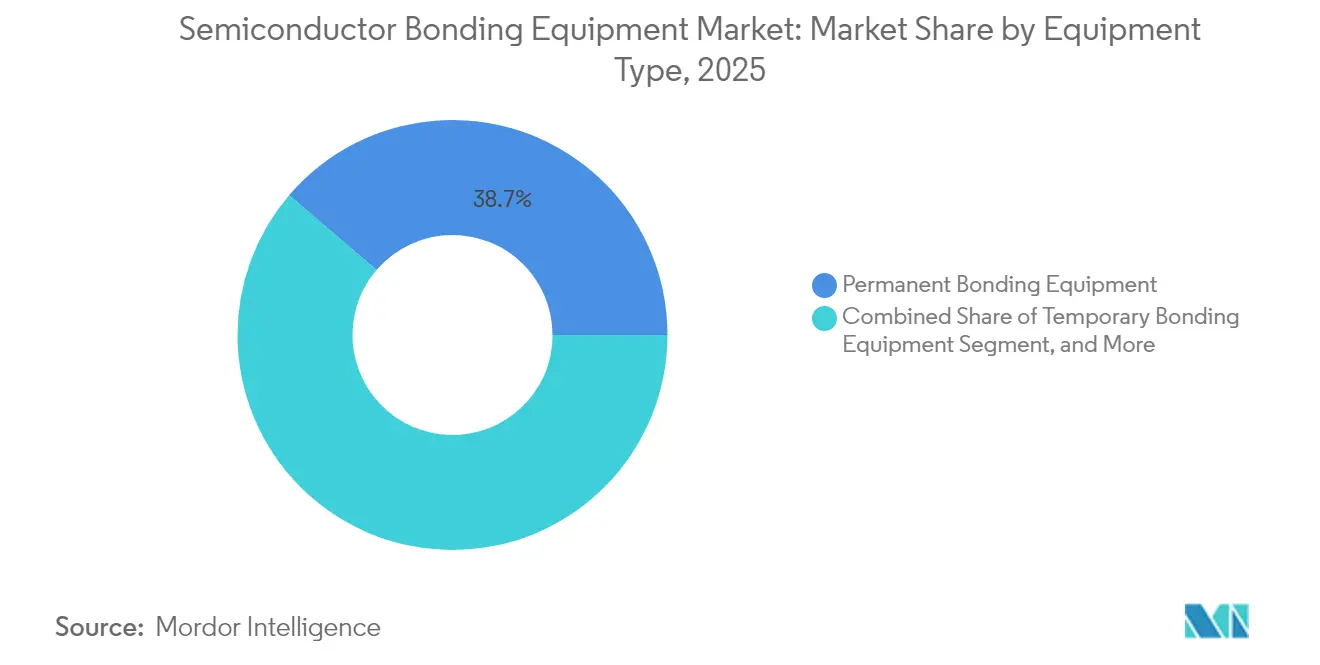

- By equipment type, permanent bonding equipment held the largest 38.74% of the semiconductor bonding equipment market share in 2025, while hybrid bonding systems are projected to grow at a 5.88% CAGR to 2031.

- By application, advanced packaging captured a 35.42% share of the semiconductor bonding equipment market in 2025; silicon photonics is forecast to expand at a 5.73% CAGR by 2031.

- By bonding technology, thermocompression led with 40.92% share of the semiconductor bonding equipment market size in 2025, and hybrid technology is advancing at a 6.07% CAGR through 2031.

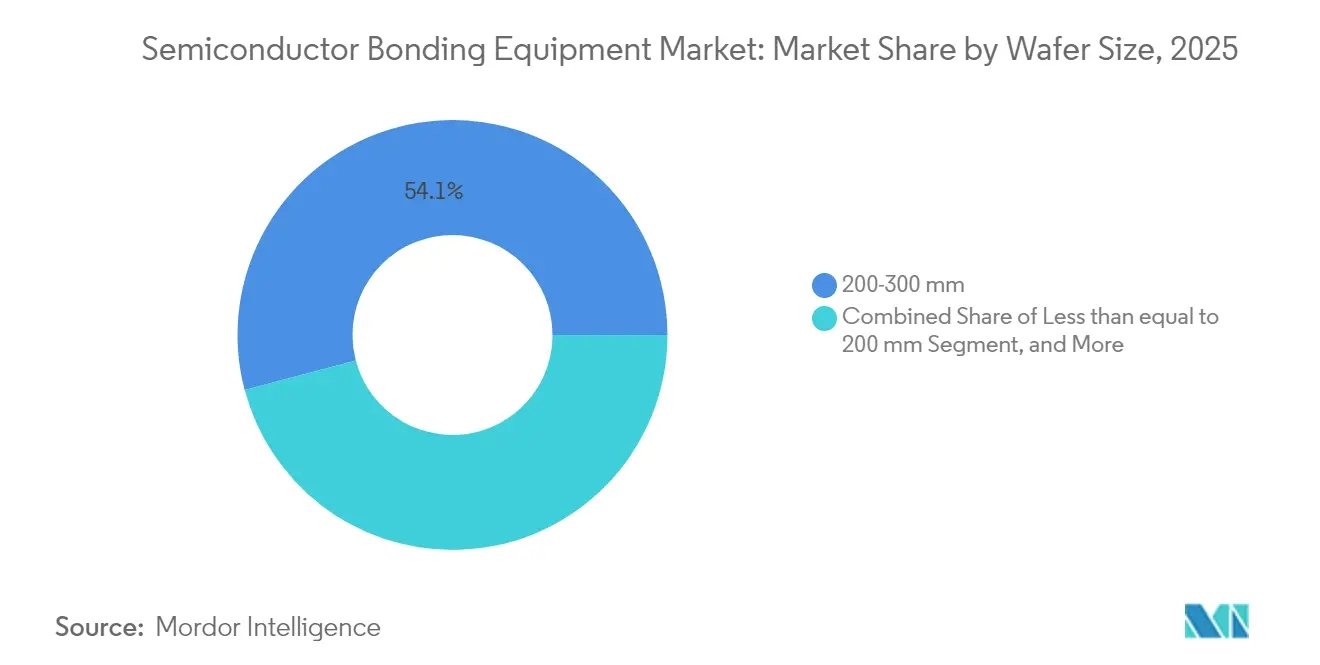

- By wafer size, 200-300 mm represented 54.12% of the semiconductor bonding equipment market size in 2025; the >300 mm category is set to climb at 6.44% CAGR to 2031.

- By end-user, integrated device manufacturers represented 45.66% of the semiconductor bonding equipment market size in 2025; the foundries end-user is set to climb at 6.32% CAGR to 2031.

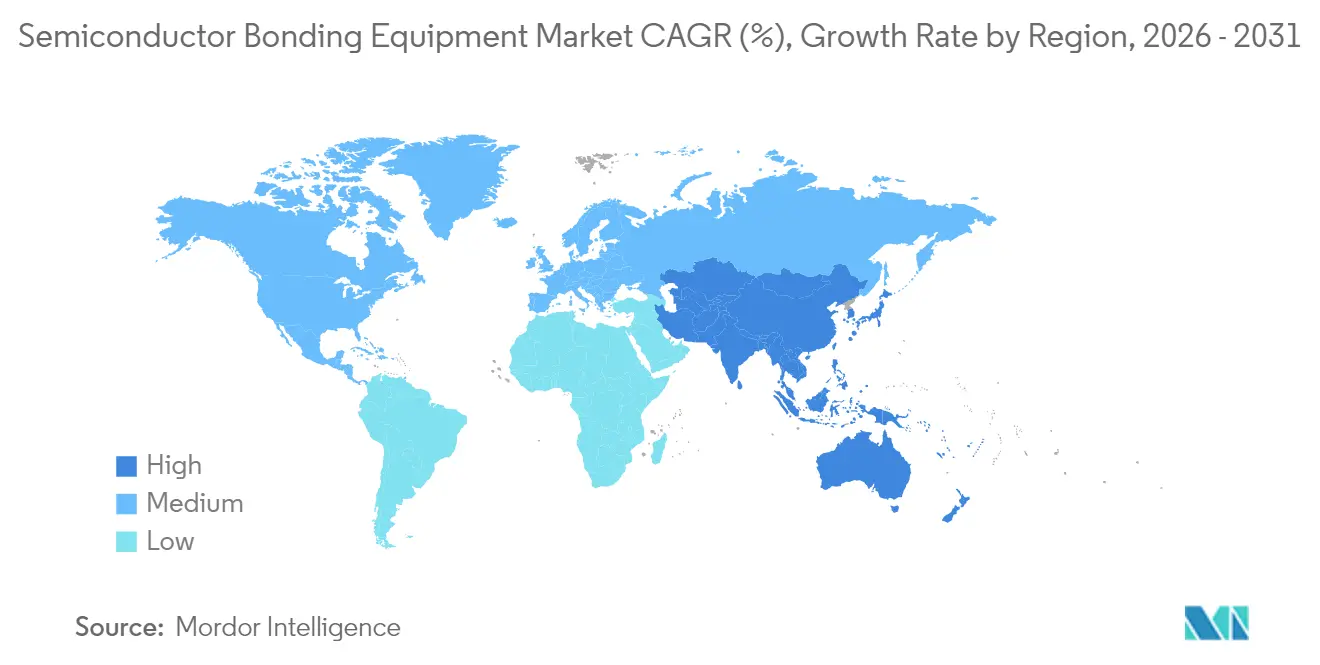

- By geography, Asia-Pacific represented 52.64% of the semiconductor bonding equipment market size in 2025; the segment is set to climb at 5.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Semiconductor Bonding Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing CAPEX by IDMs and foundries | +1.2% | Global, concentrated in APAC | Medium term (2-4 years) |

| Surging semiconductor content in automotive and IoT devices | +0.9% | Global, with early gains in Europe, North America | Long term (≥ 4 years) |

| Rapid adoption of advanced 2.5D/3D packaging platforms | +1.1% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Government-backed "CHIPS" subsidies and tax incentives | +0.8% | North America and EU, with selective APAC programs | Short term (≤ 2 years) |

| Commercial roll-out of hybrid wafer-to-wafer bonding in CIS and 3D-NAND | +0.7% | APAC dominance, expanding to North America | Medium term (2-4 years) |

| Silicon-photonic interposers for AI datacenters driving wafer bonding tools | +0.6% | North America and EU, with APAC manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing CAPEX by IDMs and Foundries

Global semiconductor equipment spending hit USD 110 billion in 2024 and is on track for USD 130 billion by 2026.[1]SEMI, “2024 Equipment Spending by Region,” semi.org TSMC alone earmarked USD 38-42 billion for 2025 facility upgrades, a substantial portion of which funds advanced packaging and bonding lines.[2]Taiwan Semiconductor Manufacturing Co., “2025 CAPEX Guidance,” tsmc.com Comparable expansions by Samsung and Intel emphasize the competitive need for wafer-level integration that supports high-bandwidth memory and chiplet designs. Capital allocation now targets line items such as sub-micrometer optical alignment modules, vacuum bond chambers, and AI-enabled process control. Vendors that provide modular upgrade paths are gaining preferred-supplier status as device makers hedge against future design pivots. The investment uptick stimulates the semiconductor bonding equipment market by shortening replacement cycles and broadening the installed base across both front-end and back-end fabs.

Surging Semiconductor Content in Automotive and IoT Devices

Average semiconductor value per vehicle climbed to USD 950 in 2024, driven by electrified powertrains, advanced driver-assistance systems, and zonal architectures.[3]Bosch, “Semiconductor Content in Electric Vehicles,” bosch.com Electric models specify silicon-carbide and gallium-nitride power devices that need high-force, high-temperature bonding heads and robust flux-management systems. In parallel, IoT wearables and smart home nodes demand wafer-level chip-scale packages that shrink footprint and extend battery life. These divergent requirements converge at the equipment level, where configurable bonders must toggle between high-power pressure profiles and delicate MEMS handling. Suppliers are addressing the gap with adaptive clamp designs, real-time chuck-planarity feedback, and recipe-driven force curves. The trend raises unit shipments in the semiconductor bonding equipment market while diversifying revenue streams across automotive Tier-1s and consumer OEMs.

Rapid Adoption of Advanced 2.5D/3D Packaging Platforms

Shipments of 2.5D interposers rose 35% year over year in 2024 as HPC processors adopted chiplet architectures for die-to-die interconnect flexibility.[4]Applied Materials, “Hybrid Bonding in Advanced Packaging,” appliedmaterials.com Three-dimensional stacking pushes throughput-first bonders to achieve placement repeatability below 500 nm while containing warp on thinned wafers. Equipment makers now bundle thermal-modeling software and in-situ metrology to pre-correct distortion during compression cycles. Reliability validation, once a downstream test-house function, moves upstream into the bonding tool with embedded acoustic imaging. As front-end and back-end workflows merge, purchasing departments renegotiate service agreements to cover the hybrid process window, reinforcing demand momentum for comprehensive platforms in the semiconductor bonding equipment market.

Government-Backed “CHIPS” Subsidies and Tax Incentives

The U.S. CHIPS and Science Act allocates USD 52.7 billion, including sizeable grants reserved for advanced packaging lines. Texas Instruments, for instance, secured USD 1.6 billion to expand domestic assembly facilities focused on wafer-to-wafer bonding of analog and power devices. Europe mirrors the effort with an EUR 43 billion package that guides member states toward packaging self-sufficiency. Early awardees are leveraging funds to offset the capital premium of vacuum bonders and temperature-controlled cleanrooms. While subsidies accelerate orders in the semiconductor bonding equipment market, vendors remain cautious about cliff-edge risks once funding sunsets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of ownership and TCO uncertainty | -0.7% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Process complexity at sub-10 µm alignment tolerances | -0.5% | Global, concentrated in advanced node facilities | Medium term (2-4 years) |

| Supply-chain bottlenecks for ultra-flat carrier wafers | -0.4% | Global, with APAC supply concentration | Short term (≤ 2 years) |

| Stricter VOC / adhesive-chemistry environmental regulations | -0.3% | EU and North America leading, APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Ownership and TCO Uncertainty

State-of-the-art hybrid bonders list above USD 3 million, while annual running costs including spares, consumables, and calibration can lift lifetime spend to USD 8 million. Smaller OSATs struggle when utilization drifts below 70%, especially in consumer-electronics off-seasons. Rapid roadmap updates further complicate financial modeling because a tool qualified for 10 µm overlay may need retrofit kits after only two product cycles. Leasing programs, outcome-based service contracts, and shared-risk pricing models are emerging, yet CFOs still cite uncertain residual value as a brake on new orders within the semiconductor bonding equipment market.

Process Complexity at Sub-10 µm Alignment Tolerances

Bringing overlay error down to single-digit micrometers forces fabs to enforce temperature stability within ±0.1 °C and implement active vibration isolation on the sub-nanometer scale. Process engineers spend extra quarters refining bond recipes, extending time-to-money for greenfield lines. Even mature fabs must recalibrate inspection metrology, edge-bead removal, and plasma-clean steps to curb void defects. Training requirements intensify as operators shift from mechanical adjustments to software-defined offsets guided by real-time machine-vision feedback. The heightened complexity contributes to lengthier qualification and validation cycles, tempering roll-out speed in the semiconductor bonding equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Hybrid Platforms Gain Ground

Permanent bonders accounted for 38.74% of 2025 revenue, underpinned by their proven reliability in legacy device packaging. Temporary bonding tools cater to wafer thinning and TSV creation, providing the reversible adhesion needed for mechanical support. Hybrid systems register the quickest climb at 5.88% CAGR, targeting sub-3 nm integration where copper-to-copper direct attach minimizes resistance and electromigration. That growth lifts the semiconductor bonding equipment market size for hybrid platforms from a modest base toward parity with permanent tools before the decade closes. Manufacturers differentiate through dual-stage alignment optics, active levelling chucks, and closed-loop pressure control that collectively push placement error below 500 nm. Buyers favor multi-modal units that accept future recipe add-ons, lowering capital risk. The pivot intensifies R&D around heat-spreader materials and compliant under-fill chemistries that withstand repeated thermal cycles without delamination. Competition also hinges on throughput, with flagship machines now promising 20% cycle-time reductions achieved via parallel clamp arms and predictive servo tuning.

A broader equipment refresh cycle accompanies the shift. Line managers audited older eutectic stations and discovered maintenance outlays rising 12% per year. Swapping to hybrid bonders eliminates dual-pass processes, improving floor utilization. Yet stakeholders insist that new gear integrate seamlessly with MES and factory automation layers that handle traceability down to die serial number. Vendors respond by embedding OPC-UA gateways and edge analytics that channel process data into AI-based yield dashboards. Such ecosystem compatibility accelerates factory-wide adoption, reinforcing the hybrid segment’s contribution to the semiconductor bonding equipment market.

By Application: Silicon Photonics Takes Off

Advanced packaging maintained 35.42% of 2025 revenue and remains the anchor segment, buttressed by chiplet processors, high-bandwidth memory, and premium smartphone SoC programs. Power IC bonding, while less glamorous, delivers stable volumes that depend on rigorous void-control protocols and high-pressure thermocompression heads. Silicon photonics is the standout high-velocity niche at a 5.73% CAGR. Optical engines co-packaged with switch ASICs need micron-accurate placement of germanium photodetectors and III-V lasers onto silicon carrier wafers, driving specialized bond recipes with controlled temperature ramps under 250 °C. The strong demand trajectory has already lifted the silicon-photonics slice from single digits toward a double-digit share of the overall semiconductor bonding equipment market size.

MEMS sensors, notably for automotive lidar and industrial automation, require hermetic seals that endure 1,000-cycle temperature swings. These stress profiles favor glass-frit or anodic bonding, sustaining a market foothold for niche tool vendors. CMOS image sensors push alignment fidelity to safeguard optical axis integrity, stoking orders for advanced auto-focus optics built into bond heads. RF devices, meanwhile, introduce unique impedances that compel low-loss interconnect metallurgy, influencing material-delivery subsystems on next-gen machines. The blend of widespread and emerging uses buffers suppliers from cyclical swings and keeps the semiconductor bonding equipment market on a stable growth path.

By Bonding Technology: Thermocompression Dominance Under Review

Thermocompression retained 40.92% market revenue in 2025 by fusing gold stud bumps and solder caps across diverse IC tiers. Its repeatable process window and known failure mechanisms encourage conservative buyers to stay invested. Eutectic and solder methods populate industrial and automotive lines where elevated temperature cycling dictates high-lead, high-tin alloys. Adhesive polymer bonding remains critical for flexible electronics and sensor foils, but rarely crosses into high-density silicon photonics.

Hybrid bonding is the clear disruptor, sprinting at 6.07% CAGR and expected to erode thermocompression’s turf by the late decade. Vendors deploy oxide-CMP steps coupled with nanosecond laser activation to lower bonding temperature without sacrificing copper diffusion paths. Such innovations catapult the hybrid slice of the semiconductor bonding equipment market share to strategic relevance for both memory stackers and logic foundries. Ultrasonic and thermosonic wire methods decline gradually yet retain irreplaceable status for large-power devices where cost per lead rules purchasing criteria. Anodic and fusion processes sit in specialized corners, favored by defense-grade sensors requiring void-free, glass-to-silicon interfaces.

At the engineering level, each technology group now threads AI engines that map time-series vibration and temperature to predictive yield scores. The cross-pollination of software and hardware ensures bonding platforms stay field-upgradeable, curbing obsolescence fears that once limited adoption speed across the semiconductor bonding equipment market.

By Wafer Size: Large Formats Capture Investment

Wafers in the 200-300 mm range delivered 54.12% of 2025 sales, benefiting from well-depreciated fab infrastructure and a robust second-hand tool chain. The category still attracts incremental upgrades such as in-situ metrology modules that retrofit onto existing bonders. In contrast, ≤200 mm formats serve compound semiconductor and mixed-signal nodes where cost per wafer is acceptable at lower volumes. The leap to >300 mm drives the highest momentum, projected at 6.44% CAGR, propelled by mega-fabs that chase die-per-wafer economics for AI and memory macros. Early pilot lines for 330 mm gallium-nitride substrates are already in place at select Asian foundries, hinting at a future realignment of capex priorities.

Tool builders must strike a balance: retain design libraries for legacy clamp sizes and stepper alignment marks while fielding new platforms with extended vacuum chucks and wafer-edge exclusion algorithms. The dual demand profile increases R&D spend yet opens parallel revenue streams. As a result, volume growth in the >300 mm category enlarges the semiconductor bonding equipment market size without cannibalizing mature-node demand.,

By End User: Foundry Momentum Builds

Integrated Device Manufacturers still represented 45.66% of 2025 revenue through captive lines optimized for latency-sensitive parts such as smartphone application processors. However, accelerated outsourcing by fabless houses pushes foundry order books ahead at a 6.32% CAGR. Giants like TSMC, Samsung Foundry, and GlobalFoundries now pitch turnkey heterogenous integration services, consolidating wafer production and packaging in contiguous campuses. Such verticality compels high-mix bonders capable of quick recipe changes. Foundry procurement teams thus prioritize modular platforms that share spares across multiple technology nodes, trimming total service cost.

OSAT players focus on cost-sensitive consumer and IoT segments where standard wire-bond packages remain viable. They continue to buy refurbished units while trialing one or two hybrid systems for premium tiers. The tri-modal customer landscape fosters healthy competition among equipment makers, sustaining order visibility in the semiconductor bonding equipment market across up- and down-cycles.

Geography Analysis

Asia-Pacific held 52.64% of 2025 revenue, underlined by USD 49.6 billion in equipment spending from China alone, up 35% year over year. South Korea followed with USD 20.5 billion, and Taiwan contributed USD 16.6 billion despite temporary inventory corrections. Regional policy packages include tax deductions, duty exemptions, and infrastructure subsidies that lower effective purchase prices of hybrid bonders, sustaining leadership in the semiconductor bonding equipment market. Local champions such as TSMC and Samsung spearhead 3D and hybrid adoption, elevating regional technical standards and reshaping supply-chain expectations for precision chucks and ultra-flat carrier wafers.

North America posted USD 13.7 billion in 2024 sales, advancing 14% alongside CHIPS Act allocations targeting domestic capacity expansion. Intel, Micron, and Texas Instruments have announced multiyear packaging projects anchored in Arizona, Ohio, and Texas. The subsidy stimulus accelerates inbound orders but raises concerns over long-term cost competitiveness once grants taper. Yet the region benefits from proximity to hyperscale-data-center customers demanding low-latency interposers for AI workloads, a segment that outlets more value-added hybrid bonders into the semiconductor bonding equipment market. Europe concentrates spending in Germany and the Netherlands where analog, power, and EUV tool vendors cluster. Collaborative programs like IPCEI-ME/CT channel EUR funding into 3D integration, especially for automotive power modules that require stringent reliability. Middle East and Africa remain nascent, though Saudi Arabia’s Vision 2030 and the UAE’s strategic tech funds have earmarked pilot lines for compound semiconductors. These early moves hint at wider regional diversification that could incrementally enlarge the semiconductor bonding equipment market beyond its traditional APAC stronghold.,

Competitive Landscape

The semiconductor bonding equipment market shows moderate concentration, with five vendors accounting for a significant 2024 revenue. Applied Materials, Tokyo Electron, and ASMPT leverage deep process libraries and service footprints to preserve incumbent status; emerging specialists like EV Group carve niches through sub-micrometer alignment innovations. Strategic alliances proliferate. Applied Materials’ 9% stake in BE Semiconductor Industries strengthens its hybrid-bonding roadmap, allowing co-development of oxide planarization and copper surface-activation modules. Similar tie-ups between tool suppliers and fabs accelerate joint learning cycles, converting bespoke prototypes into volume tools within 18 months instead of the historical 30-month window.

Competition is pivoting from pure throughput metrics to holistic ecosystem integration. Vendors embed machine-learning controllers that predict bond voids, thereby boosting first-pass yield and lowering rework costs. Supply resilience becomes another battleground, with manufacturers dual-sourcing critical components like high-resolution encoders or ceramic heaters to hedge geopolitical disruptions. Price elasticity is limited because performance gains in sub-3 nm nodes outweigh upfront capex. Nonetheless, smaller OSAT customers negotiate performance-based payment schedules to spread risk, compelling vendors to refine lifetime-value calculations in the semiconductor bonding equipment industry.

Looking forward, white-space opportunities lie in silicon photonics and automotive power devices that require field-upgradeable chambers to accommodate new III-V and SiC materials. Patent filings cluster around laser-assisted hybrid bonding and self-learning alignment optics, signaling where the next performance leaps will occur. Meanwhile, stricter sustainability metrics push contenders to develop solvent-free wafer-clean chemistries and low-energy vacuum pumps, differentiators that could tilt RFQs as ESG mandates tighten across the semiconductor bonding equipment market.

Semiconductor Bonding Equipment Industry Leaders

EV Group

ASMPT Semiconductor Solutions

MRSI Systems. (Myronic AB)

WestBond Inc.

Panasonic Holding Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Applied Materials acquired a 9% stake in BE Semiconductor Industries for USD 100 million to co-develop hybrid bonding solutions.

- December 2024: Tokyo Electron unveiled a JPY 1.5 trillion five-year R&D initiative targeting advanced packaging tools.

- November 2024: ASMPT reported record thermo-compression bonding revenue driven by AI packaging demand.

- October 2024: EV Group launched the GEMINI platform with sub-micrometer alignment for 2.5D and 3D packages.

Global Semiconductor Bonding Equipment Market Report Scope

Wafer bonding is the process of adhering a thin substrate wafer to a support carrier disc using wafer substrate bonding units. Several bonding techniques are used to achieve this, requiring various equipment or machinery. Equipment types include permanent bonding, temporary bonding, and hybrid bonding. The scope of the bonding equipment market is limited to applications such as advanced packaging, power IC and power discrete, photonic devices, MEMS sensors and actuators, engineered substrates, RF devices, and CMOS image sensors (CIS).

The semiconductor bonding equipment market is segmented by type (permanent bonding equipment, temporary bonding equipment, hybrid bonding equipment), application (advanced packaging, power IC and power discrete, photonic devices, MEMS sensors and actuators, engineered substrates, RF devices, CMOS image sensors (CIS)), and geography (North America, Asia, Europe, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Permanent Bonding Equipment |

| Temporary Bonding Equipment |

| Hybrid Bonding Equipment |

| Advanced Packaging |

| Power IC and Discrete |

| Photonic Devices |

| MEMS Sensors and Actuators |

| Engineered Substrates |

| RF Devices |

| CMOS Image Sensors |

| Thermocompression Bonding |

| Eutectic/Solder Bonding |

| Adhesive/Polymer Bonding |

| Ultrasonic / Thermosonic Bonding |

| Anodic / Fusion Bonding |

| Less than equal to 200 mm |

| 200-300 mm |

| Greater than 300 mm |

| Integrated Device Manufacturers (IDMs) |

| Foundries |

| Outsourced Semiconductor Assembly and Test (OSAT) |

| North America | United States |

| Rest of North America | |

| South America | |

| Europe | Germany |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | |

| Africa |

| By Equipment Type | Permanent Bonding Equipment | |

| Temporary Bonding Equipment | ||

| Hybrid Bonding Equipment | ||

| By Application | Advanced Packaging | |

| Power IC and Discrete | ||

| Photonic Devices | ||

| MEMS Sensors and Actuators | ||

| Engineered Substrates | ||

| RF Devices | ||

| CMOS Image Sensors | ||

| By Bonding Technology | Thermocompression Bonding | |

| Eutectic/Solder Bonding | ||

| Adhesive/Polymer Bonding | ||

| Ultrasonic / Thermosonic Bonding | ||

| Anodic / Fusion Bonding | ||

| By Wafer Size | Less than equal to 200 mm | |

| 200-300 mm | ||

| Greater than 300 mm | ||

| By End User | Integrated Device Manufacturers (IDMs) | |

| Foundries | ||

| Outsourced Semiconductor Assembly and Test (OSAT) | ||

| Geography | North America | United States |

| Rest of North America | ||

| South America | ||

| Europe | Germany | |

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | ||

| Africa | ||

Key Questions Answered in the Report

What is the current value of the semiconductor bonding equipment market?

The market is valued at USD 596.47 million in 2026.

How fast is the market expected to grow?

It is forecast to log a 4.84% CAGR through 2031.

Which equipment type is expanding the quickest?

Hybrid bonding platforms are rising at a 5.88% CAGR.

Which region leads demand?

Asia-Pacific commands 52.64% of 2025 revenue due to strong foundry spending.

Why are subsidies important?

CHIPS Act and EU programs lower capital risk, accelerating domestic bonding-tool purchases.

What technology trend poses the biggest challenge?

Achieving sub-10 µm alignment tolerances increases process complexity and equipment costs.

Page last updated on: