Semiconductor Applications In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.26 Billion |

| Market Size (2031) | USD 15.79 Billion |

| Growth Rate (2026 - 2031) | 11.26% CAGR |

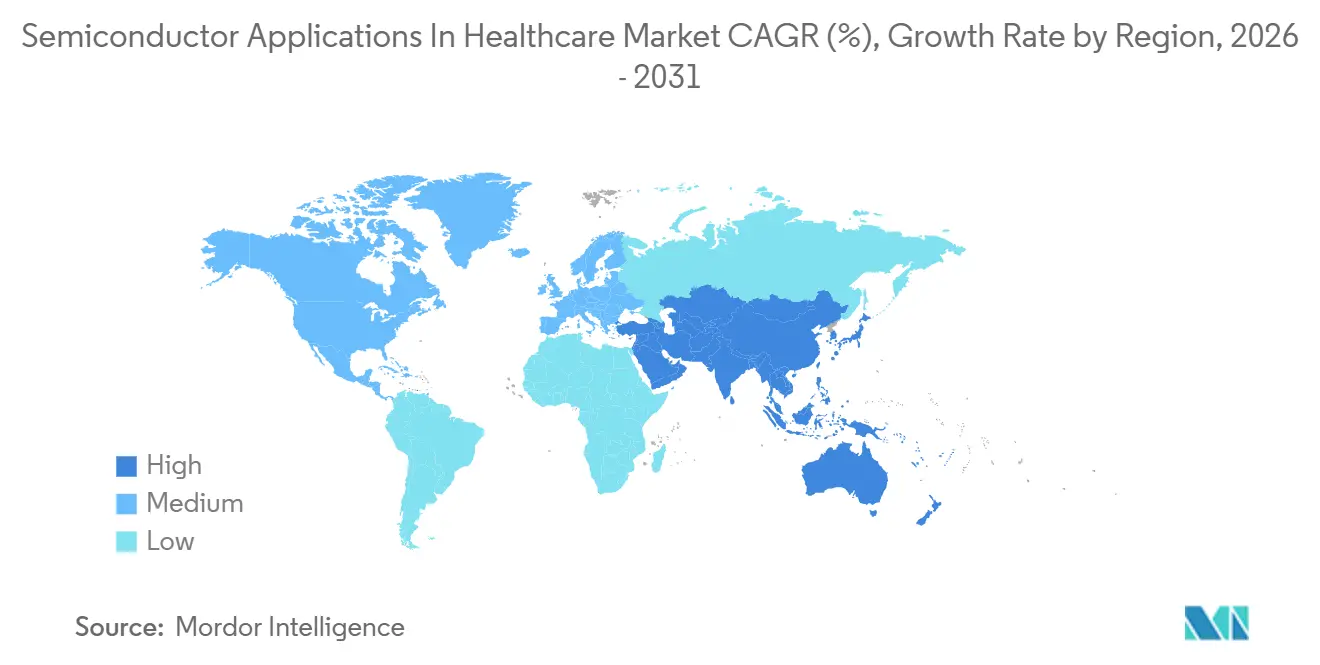

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

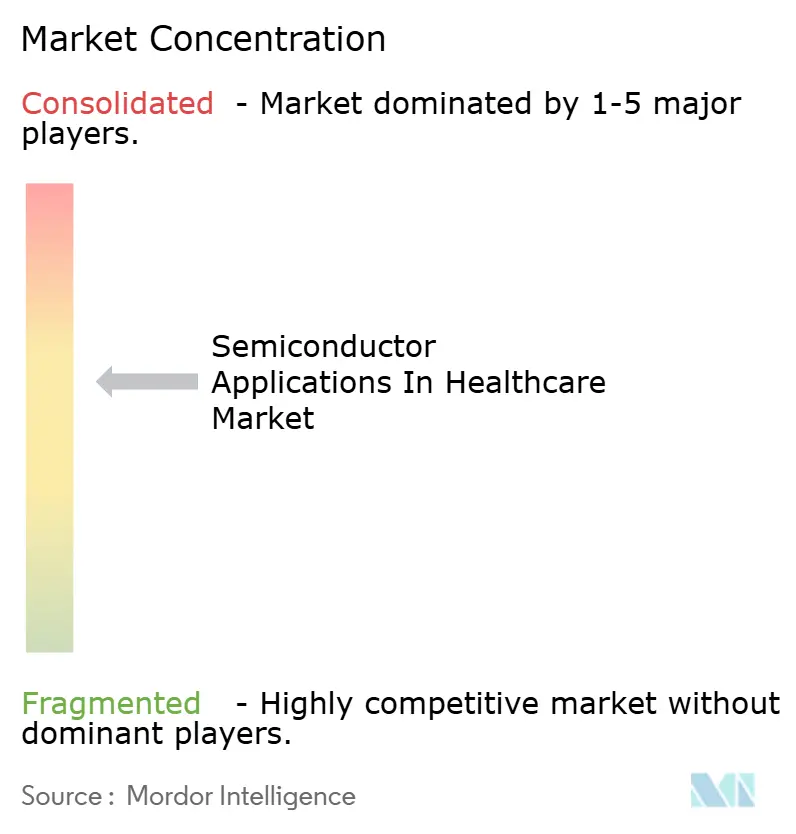

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Semiconductor Applications In Healthcare Market Analysis by Mordor Intelligence

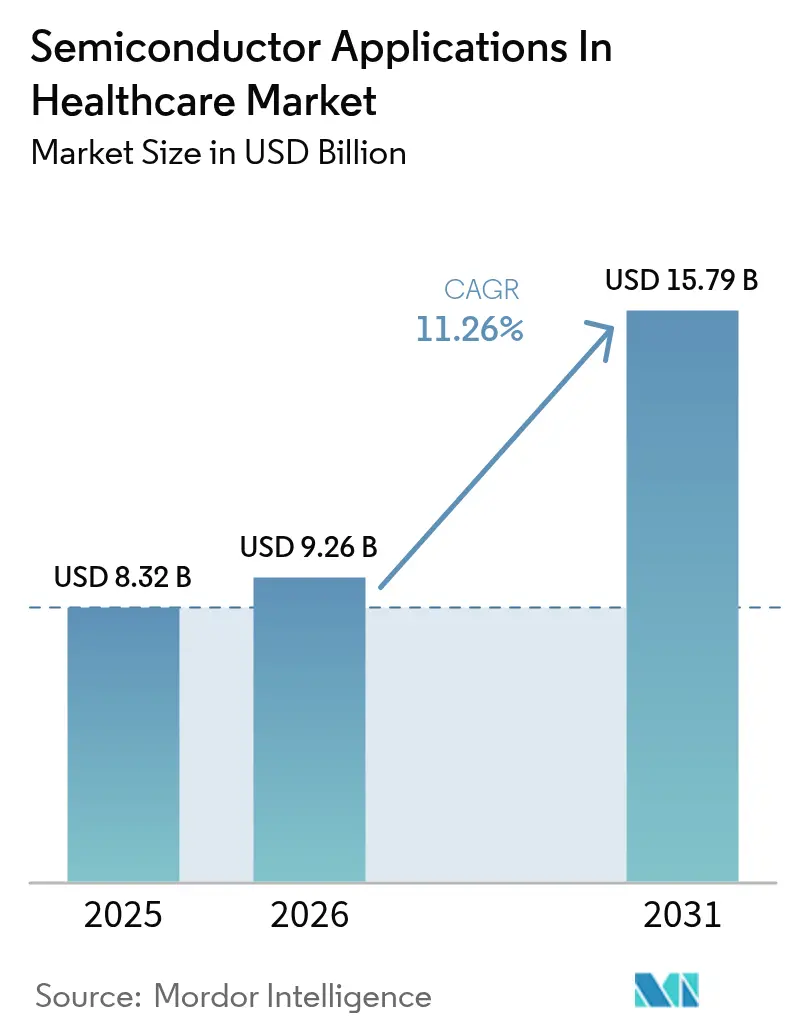

The Semiconductor Applications In Healthcare market size was valued at USD 8.32 billion in 2025 and estimated to grow from USD 9.26 billion in 2026 to reach USD 15.79 billion by 2031, at a CAGR of 11.26% during the forecast period (2026-2031). Demand is shifting from pure device miniaturization toward edge intelligence that executes diagnostic inference directly on sensors, cutting reliance on centralized data centers. Region-specific data-sovereignty mandates, reimbursement policies rewarding outcome-based care, and rapid progress in sub-28 nanometer processing collectively reinforce this transition. The Semiconductor Applications In Healthcare market is also benefiting from government fab incentives in Asia Pacific, surging patent activity in chiplet architectures, and falling advanced-packaging costs that open new design possibilities for startups. Against that backdrop, suppliers face two headline risks; thermal management in implantables operating near 1 W/cm² power densities and supply-chain concentration for specialty substrates produced at only three fabs worldwide.

Key Report Takeaways

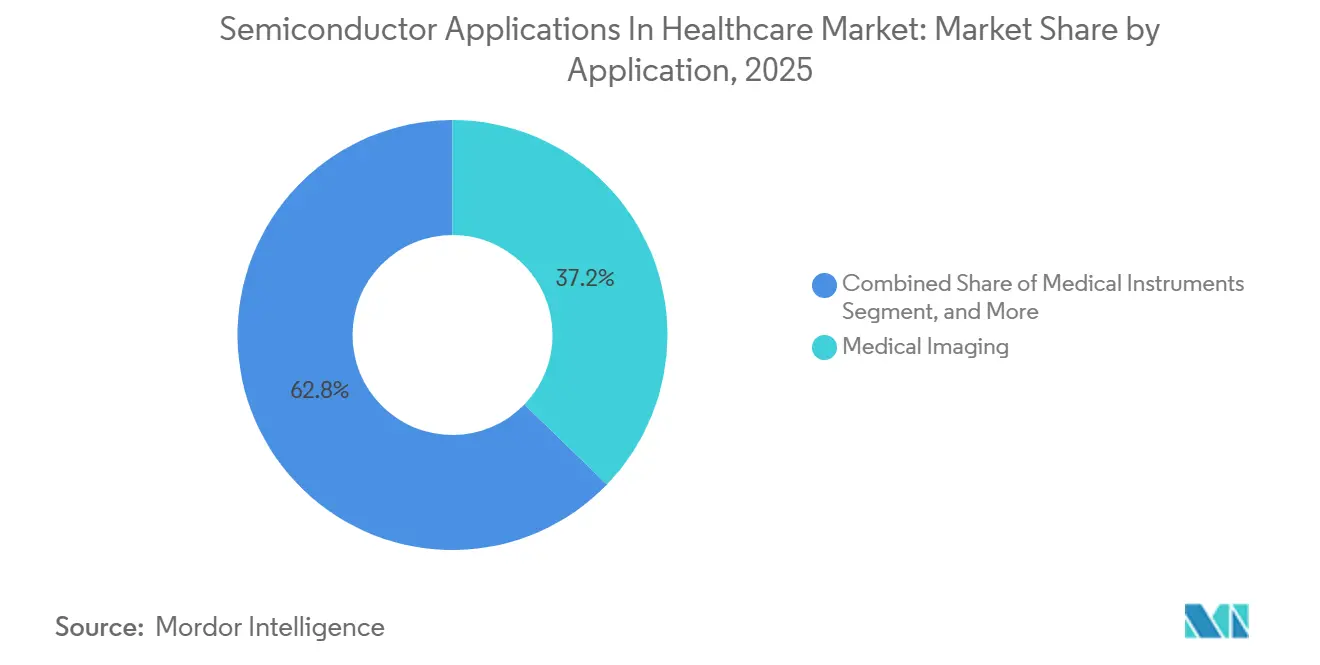

- By application, Medical Imaging led with 37.23% revenue in 2025, whereas Lab-on-Chip Diagnostics is projected to expand at a 12.12% CAGR through 2031.

- By component, Sensors captured 30.51% of 2025 demand, while Optoelectronics is forecast to grow at a 12.03% pace to 2031.

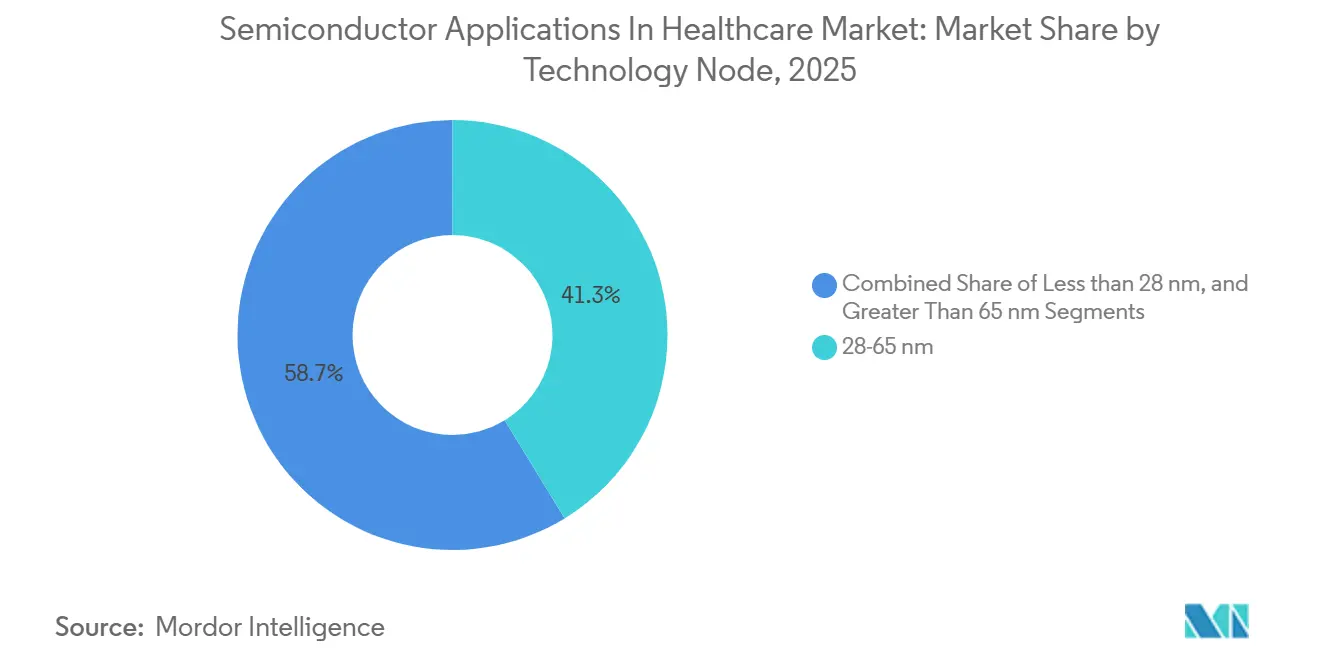

- By technology node, 28-65 nanometer processes accounted for 41.26% of the volume in 2025, yet sub-28 nanometer nodes are expected to grow at an 11.94% CAGR through 2031.

- By end-user, Hospitals and Diagnostic Centers accounted for 46.48% of revenue in 2025, whereas Home Healthcare Settings are set to achieve a 12.67% CAGR through 2031.

- By geography, Asia Pacific accounted for 32.73% of 2025 revenue and is poised for the fastest regional CAGR of 12.38% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Semiconductor Applications In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Connected Medical Devices and IoT | +2.1% | Global, early adoption in North America and Western Europe | Medium term (2–4 years) |

| Growing Adoption of AI-Enabled Imaging Systems | +2.4% | North America, Europe, Asia Pacific | Short term (≤2 years) |

| Rising Chronic-Disease Burden Driving Remote Monitoring | +1.8% | Global, notably Japan, Germany, United States | Long term (≥4 years) |

| Ultralow-Power Neuromorphic Edge ASICs for Implantables | +1.3% | North America and Europe, spill-over Asia Pacific | Long term (≥4 years) |

| Government Incentives for Healthcare-Specific Fabs | +1.6% | United States, European Union, India, China | Medium term (2–4 years) |

| Lab-on-Chip Diagnostics Reducing Central-Lab Dependence | +1.9% | Asia Pacific core, expanding Middle East and Africa | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Connected Medical Devices And IoT

More than 60% of new devices cleared by the U.S. Food and Drug Administration in 2025 embedded wireless connectivity, signaling a change from isolated instruments to data-rich ecosystems.[1]U.S. Food and Drug Administration, “Medical Devices,” FDA.GOV Bluetooth Low Energy 5.4 radios, Wi-Fi 6E modules, and NFC controllers now form mandatory blocks in design checklists rather than optional add-ons. Low-power dual-core chips such as Nordic Semiconductor’s nRF5340 achieve sub-3 µA standby current, enabling year-long use in glucose monitors and cardiac event recorders. Interoperability clauses in the 21st Century Cures Act force manufacturers to adopt standardized data formats, which pushes demand for hardware root-of-trust modules. NXP shipped 40% more EdgeLock secure elements for medical IoT in 2025, underscoring the linkage between cybersecurity mandates and silicon content.

Growing Adoption Of AI-Enabled Imaging Systems

Edge inference capabilities migrated swiftly into computed tomography and magnetic resonance imaging equipment, lifting AI-enabled installations to 28% in 2025, up from 11% two years prior. GE HealthCare’s Photonova CT integrates a 7 nm ASIC to halve radiation dose and cut scan time by 35%, proving that silicon design decisions now shape both clinical performance and reimbursement economics. Philips’ Verida platform leverages Qualcomm inference accelerators to triage intracranial hemorrhage within seconds, demonstrating the productivity gains that hospitals capture when latency-prone cloud calls are removed. As algorithms commoditize, competitive advantage shifts to energy efficiency at the chip level because portable carts and outpatient scanners cannot accommodate high-wattage data-center GPUs.

Lab-On-Chip Diagnostics Reducing Central-Lab Dependence

Disposable microfluidic cartridges containing CMOS-based fluorescence detectors allow nucleic-acid amplification, immunoassay, and biochemical analysis at points of care. The Semiconductor Applications In Healthcare market gains momentum here because chipmakers supply integrated photonic sensors that shrink laboratory workflows into palm-sized devices. Abbott’s ID NOW shipped 4.2 million COVID-19, influenza, and RSV cartridges in 2025, a scale that creates repeat silicon demand for optical excitation and detection circuits. High uptake in pharmacies and ambulances, particularly across Asia Pacific, boosts unit volumes even though average selling prices trend lower. Governments favor these systems during infectious-disease outbreaks, injecting stimulus funding that cascades directly to semiconductor orders.

Rising Chronic-Disease Burden Driving Remote Monitoring

Chronic illnesses consume 75% of healthcare budgets in OECD economies, spurring payers to back continuous monitoring over episodic hospital visits.[2]Organisation for Economic Co-operation and Development, “Health Statistics,” OECD.ORG Semiconductor content in remote-monitoring devices doubled to USD 12 per unit in 2025 because precision ADCs, power-management ICs, and multiradio SoCs now ship as integrated packages. Japan expanded reimbursement codes for wearable electrocardiogram services in 2025, triggering a 52% surge in patch shipments. Product roadmaps are therefore gated not by technology readiness but by payer policy, nudging suppliers to align launch cycles with changing coverage determinations. As proof, Analog Devices’ AD4130-8 replaces three discrete chips, lowering bill of materials while clearing a compliance path for manufacturers under tighter cost targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upgrade Costs for Legacy Medical Equipment | -1.4% | Global, acute in emerging-market hospitals | Medium term (2–4 years) |

| Stringent Regulatory Approval Cycles for Chip Changes | -1.1% | North America and Europe | Long term (≥4 years) |

| Thermal Issues in Miniaturized Wearable/Implantables | -0.8% | Global, advanced-node designs | Short term (≤2 years) |

| Supply-Chain Concentration in Specialist Substrates | -0.9% | Global, Asia Pacific supply hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Upgrade Costs For Legacy Medical Equipment

Computed tomography scanners now remain in service for 11.2 years on average, up from 8.7 years in 2019, because hospital budgets prioritize labor costs ahead of capital equipment. Adding AI-capable modules to vintage gantries can exceed 40% of new-system pricing and often voids IEC 60601 safety certifications. A 2024 HFMA survey showed that 63% of chief financial officers deferred upgrades for budgetary reasons, a trend that persisted through 2025. Vendors now offer compute blades that slide into existing chassis, decoupling analog detectors from digital processing, but uptake remains largely limited to academic centers that secure external grants.

Stringent Regulatory Approval Cycles For Chip Changes

Minor silicon revisions can trigger full pre-market reviews. Texas Instruments reported a 14-month clearance delay when a noise-immunity tweak in an ultrasound front-end required new FDA evaluation. Europe’s Medical Device Regulation insists on fresh clinical evidence for software or hardware changes that alter functionality, raising barriers for chipmakers lacking patient-data access. Industry coalitions argue for risk-based pathways that exempt performance-neutral node shrinks, yet regulators remain cautious after high-profile recalls tied to firmware vulnerabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Lab-On-Chip Gains As Imaging Matures

Medical Imaging contributed 37.23% of Semiconductor Applications In Healthcare market revenue in 2025, driven by sustained demand for computed tomography and magnetic resonance platforms that each embed thousands of high-accuracy ADCs. Imaging will continue to deliver stable, high-value silicon orders, yet growth decelerates as installed bases saturate in developed hospitals. Lab-on-Chip Diagnostics, in contrast, is projected to post a 12.12% CAGR through 2031, the quickest among all segments, thereby adding a fresh layer of demand for microfluidic-compatible optoelectronic ICs. The Semiconductor Applications In Healthcare market size tied to Lab-on-Chip platforms is amplified by payers who reimburse for near-patient respiratory and metabolic screening, shifting revenue away from centralized laboratories. Abbott’s ID NOW system shows how cartridge-based consumables re-order silicon per test, generating an annuity model that smooths cyclical capital-equipment swings.

Advances in CMOS fluorescence detection and micro-electromechanical pumps enable single-use cassettes that perform polymerase chain reaction within 15 minutes. As a result, components per device decline, yet total silicon shipment volume rises because each diagnostic uses its own sensor die. Imaging OEMs respond by integrating AI engines to maintain performance differentiation, steering the Semiconductor Applications In Healthcare market toward a dual-track path, high-value but slower-growth imaging versus lower-price, high-volume disposables.

By Component: Optoelectronics Ascends On Photonic Integration

Sensors held 30.51% share in 2025 as heart-rate, oxygen-saturation, and motion modules permeated hospital and home devices. The Semiconductor Applications In Healthcare market share for Sensors should erode gradually as analog front-ends consolidate multiple sensing modalities into single ICs, curbing discrete sales. Optoelectronics, however, is poised for a 12.03% CAGR through 2031 because integrated photonics now displace bulky scintillators and separate photodiodes in tomography and endoscopy. Photonic integrated circuits embed laser sources, modulators, and detectors on silicon, trimming system footprints and slashing power draw.

Hamamatsu’s silicon photomultiplier array with 16,384 channels improves time-of-flight positron emission tomography, raising lesion detectability by 30%. Likewise, ams OSRAM’s AS7058 integrates 18 spectral bands, broadening use cases from neonatal bilirubin checks to non-invasive hemoglobin monitoring. As photonics merges disparate wavelengths into single chips, demand extends beyond imaging into biochemical assays, driving diversity in wafer-level packaging technologies.

By Technology Node: Sub-28 Nanometer Unlocks Edge AI

The 28-65 nm category supplied 41.26% of 2025 wafer volume because it remains the sweet spot for mixed-signal integration balancing cost, analog fidelity, and digital density. Nonetheless, the Semiconductor Applications In Healthcare market size attributed to sub-28 nm designs is set to rise sharply, advancing at 11.94% CAGR. Edge artificial-intelligence accelerators for portable ultrasound and wearable cardiac monitors gain 1.8× power-efficiency benefits on TSMC’s N5 node, turning advanced lithography into a clinical performance lever. Samsung’s gate-all-around 3 nm process entered volume production for medical neural processing units in late 2025, promising further reductions in leakage current.

Economic trade-offs remain steep, with tape-out costs surpassing USD 50 million. To hedge, fabless firms deploy chiplets advanced-node compute dies stacked atop mature-node analog dies enabling feature expansion without resetting analog qualification baselines. Heterogeneous integration standards borrowed from automotive ISO 26262 now migrate into medical workflows, aligning safety cases across multi-die packages.

By End-User: Home Healthcare Reshapes Demand Profiles

Hospitals and Diagnostic Centers generated 46.48% of 2025 sales, reflecting large-ticket imaging and surgical purchases. Yet home-use devices are forecast for a 12.67% CAGR through 2031 as payers finance remote monitoring, shifting volume toward battery-powered, wireless equipment. The Semiconductor Applications In Healthcare market size for Home Healthcare devices expands alongside the Centers for Medicare and Medicaid Services policy that reimburses continuous glucose and rhythm monitoring starting 2025. Designers prioritize ultra-low standby currents, Bluetooth Low Energy radios, and intuitive user interfaces.

Dialog Semiconductor’s DA14531 system-on-chip exemplifies these constraints by delivering full Bluetooth stacks on coin-cell power, winning 12 production slots in 2025. Ambulatory Surgical Centers adopt ruggedized mobile scanners, demanding IEC 60601-1-2 electromagnetic compliance in harsh environments, while research laboratories pilot quantum-dot biosensors, seeding future high-margin silicon niches.

Geography Analysis

Asia Pacific controlled 32.73% of Semiconductor Applications In Healthcare market revenue in 2025 and is expected to remain the fastest-growing region at a 12.38% CAGR. China committed CNY 150 billion (USD 21 billion) to domestic medical-grade fabs under its updated Integrated Circuit Industry Development Guidelines, while India’s Production Linked Incentive scheme covers 50% of capex for healthcare-oriented production lines. Japan’s senior population climbed to 29% in 2025, intensifying demand for wearables and robotics that rely on Renesas and Rohm specialty MCUs. South Korea’s packaging innovations such as fan-out wafer-level techniques integrate sensors and processors for ear-level monitors.

North America remains the innovation nucleus, hosting 40% of global medical-device patent filings and benefitting from CHIPS and Science Act subsidies that bring a TSMC 4 nm line online in Arizona during late 2026. Hospitals there adopt AI imaging earlier because reimbursement models reward throughput. Europe’s EUR 43 billion Chips Act seeks sovereignty in strategic sectors including healthcare, yet heterogeneous country-level rules complicate synchronized launches.[3]European Commission, “European Chips Act,” EC.EUROPA.EU South America and Middle East and Africa trail, relying heavily on imports, though accelerated approval pathways in Brazil’s ANVISA and Saudi Arabia’s SFDA shorten time-to-market for connected devices.

Overall, regional policy plays a decisive role in capacity build-out, influencing wafer pricing and availability. Local incentive structures now cover not only logic and memory but also medical-grade analog, raising the prospect of vertically integrated supply chains that shield healthcare OEMs from geopolitical shocks.

Competitive Landscape

The Semiconductor Applications In Healthcare market is moderately fragmented. The top five vendors Texas Instruments, Analog Devices, STMicroelectronics, NXP Semiconductors, and Infineon Technologies captured major share of revenue in 2025. Incumbents bank on ISO 13485-certified design flows and multi-decade field-failure data to anchor supplier agreements with risk-averse device makers. Texas Instruments alone offers more than 1,200 medical-specific analog and embedded parts, enabling single-vendor sourcing that simplifies regulatory audits. Analog Devices broadened its Vital Signs platform by purchasing Movano Health’s wearable IP for USD 85 million in 2025, accelerating entry into home healthcare.

Fabless challengers including Qualcomm and Mediatek pursue smartphone-derived SoCs for wearables, trading lower margins for higher volume. Heterogeneous chiplet approaches create fresh competition as Broadcom and Renesas file patents for 3D-stacked medical sensor modules, a 34% rise year-over-year. BrainChip’s neuromorphic Akida processor targets decade-long battery life in neurostimulators, whereas Graphcore’s intelligence processing unit pilots real-time genomic sequencing. Compliance with IEC 62304 software lifecycle and IEC 62443 cybersecurity guidelines becomes a differentiator, as silicon-level safety features remove downstream validation work for OEMs.

Strategic collaborations tighten the ecosystem. STMicroelectronics partners with Philips to co-develop 28 nm FD-SOI ASICs for MRI, cutting power 40% versus existing chips. NXP’s i.MX RT1180 crossover MCU earned CE marking under MDR rules less than two months post-launch, highlighting the speed advantage of embedded security and safety blocks. Infineon’s XENSIV PAS CO₂ sensor captured early ventilator wins by clearing FDA 510(k) in 2024, showing how quick regulatory navigation converts to design wins.[4]Infineon Technologies, “XENSIV PAS CO₂ Sensor,” INFINEON.COM

Semiconductor Applications In Healthcare Industry Leaders

Analog Devices Inc.

ams Osram AG

Broadcom Inc.

Infineon Technologies AG

Mediatek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Renesas Electronics obtained ISO 13485:2016 certification for its RA microcontroller family, simplifying regulatory submissions for medical-device partners.

- February 2025: Texas Instruments committed USD 300 million to expand its Richardson, Texas analog fab, adding 200 mm lines dedicated to imaging and patient-monitor ICs.

- February 2025: ams OSRAM released the AS7058RB spectral sensor with 18 optical channels for neonatal hemoglobin and bilirubin monitoring, achieving CE marking in Mar 2025.

- January 2025: Analog Devices acquired Movano Health’s wearable-sensor IP for USD 85 million to enhance its Vital Signs Monitoring platform.

Global Semiconductor Applications In Healthcare Market Report Scope

The global semiconductor applications in the healthcare market are experiencing significant growth due to advancements in medical technology, increasing adoption of IoT-enabled healthcare devices, and the rising demand for efficient diagnostic and monitoring solutions. These factors are driving innovation and investment in semiconductor components tailored for healthcare applications.

The Semiconductor Applications In Healthcare Market Report is Segmented by Application (Medical Imaging, Consumer Medical Electronics, Diagnostic Patient Monitoring and Therapy, Medical Instruments), Component (Integrated Circuits, Optoelectronics, Sensors, Discrete Components), Technology Node (Less than 28 nm, 28-65 nm, Above 65 nm), End-User (Hospitals and Diagnostic Centers, Ambulatory Surgical Centers, Home Healthcare Settings, Research Laboratories), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Medical Imaging |

| Consumer Medical Electronics |

| Diagnostic Patient Monitoring and Therapy |

| Medical Instruments |

| Integrated Circuits | Analog |

| Logic | |

| Memory | |

| Micro-components | |

| Optoelectronics | |

| Sensors | |

| Discrete Components |

| Less than 28 nm |

| 28-65 nm |

| Greater Than 65 nm |

| Hospitals and Diagnostic Centers |

| Ambulatory Surgical Centers |

| Home Healthcare Settings |

| Research Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Application | Medical Imaging | |

| Consumer Medical Electronics | ||

| Diagnostic Patient Monitoring and Therapy | ||

| Medical Instruments | ||

| By Component | Integrated Circuits | Analog |

| Logic | ||

| Memory | ||

| Micro-components | ||

| Optoelectronics | ||

| Sensors | ||

| Discrete Components | ||

| By Technology Node | Less than 28 nm | |

| 28-65 nm | ||

| Greater Than 65 nm | ||

| By End-User | Hospitals and Diagnostic Centers | |

| Ambulatory Surgical Centers | ||

| Home Healthcare Settings | ||

| Research Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and projected value of the Semiconductor Applications In Healthcare market?

The Semiconductor Applications In Healthcare market is valued at USD 8.32 billion in 2025, expected to reach USD 15.79 billion by 2031, reflecting an 11.26% CAGR from 2026-2031.

Which region is expanding fastest in semiconductor-based healthcare devices?

Asia Pacific leads growth with a 12.38% CAGR through 2031, bolstered by government fab incentives in China and India and rising demand from aging populations.

Which application segment shows the highest growth potential?

Lab-on-Chip Diagnostics is forecast to grow at 12.12% CAGR, outpacing Medical Imaging as point-of-care testing gains reimbursement backing.

How do advanced technology nodes influence edge AI adoption in medical devices?

Sub-28 nm processes such as TSMC’s N5 deliver up to 1.8× performance-per-watt improvements, enabling real-time inference in portable imaging and wearable monitors.

What are the main barriers to upgrading existing hospital equipment?

High retrofit costs, often exceeding 40% of new-system prices, and lengthy regulatory re-approval cycles discourage hospitals from integrating new semiconductor modules into legacy scanners.

Which components are gaining share within optoelectronics?

Photonic integrated circuits combining laser emission, modulation, and detection on silicon are driving Optoelectronics segment growth at a 12.03% CAGR through 2031.

Page last updated on: