Asia-Pacific Professional Scalp Treatment Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

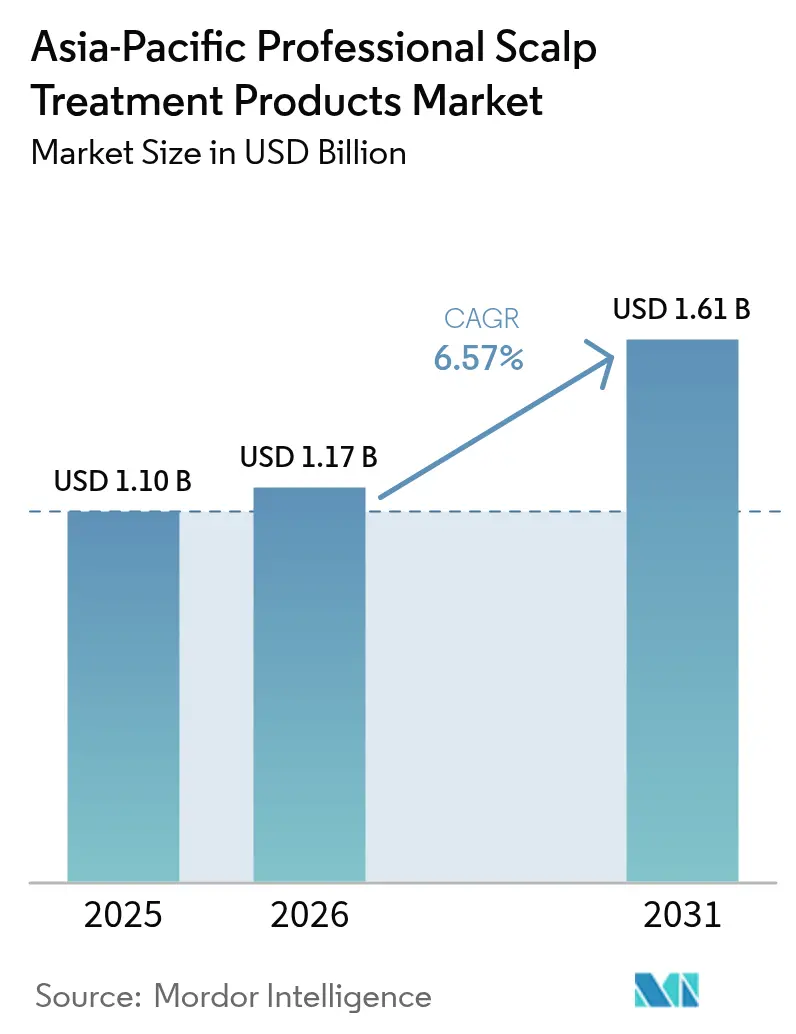

| Base Year Market Size (2025) | USD 1.1 Billion |

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Professional Scalp Treatment Products Market Analysis by Mordor Intelligence

The Asia-Pacific professional scalp treatment products market size is expected to grow from USD 1.1 billion in 2025 to USD 1.17 billion in 2026 and is forecast to reach USD 1.61 billion by 2031 at 6.57% CAGR over 2026-2031. Intensifying urban pollution, rising disposable incomes, and a shift from reactive hair repair toward preventive scalp wellness are steering demand for clinical-grade products across the region’s salons and premium retail outlets. Technological advances—most notably AI-enabled diagnostics and micro-encapsulation of actives—allow manufacturers to demonstrate measurable efficacy, reinforcing consumer willingness to pay premium prices. Natural and dermatologist-tested formulations earn trust among millennial and Gen Z shoppers. At the same time, rapid salon premiumization in China, Japan, and South Korea transforms scalp treatments into high-margin bundled services. Competitive dynamics remain fluid as heritage Japanese and European players defend territory against Korean innovators and digitally native start-ups that emphasize personalized routines and direct-to-consumer fulfillment.

Key Report Takeaways

- By product type, scalp-care shampoos captured 43.80% of the Asia-Pacific professional scalp treatment products market share in 2025, whereas exfoliant scrubs are forecast to accelerate at a 6.65% CAGR through 2031.

- By distribution channel, retail commanded 51.20% of the Asia-Pacific professional scalp treatment products market size in 2025, while salon sales are expanding at a 5.05% CAGR to 2031.

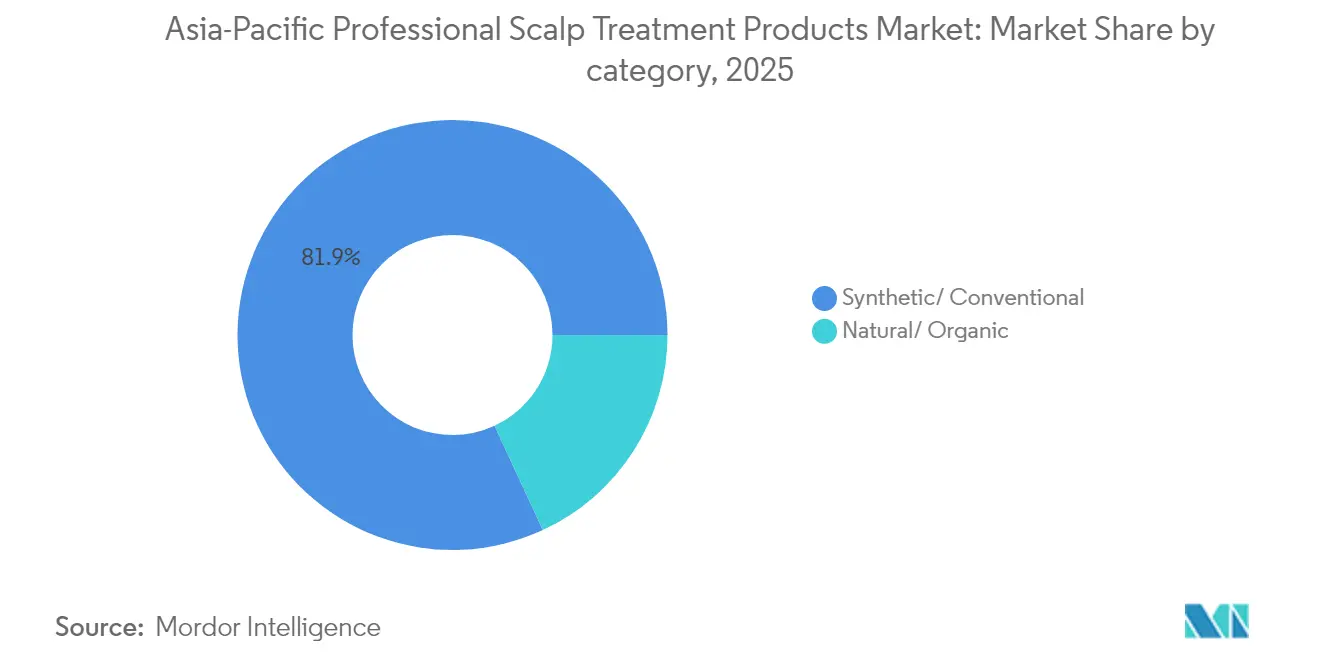

- By category, synthetic formulations constituted 81.90% value share in 2025; natural and organic lines are poised for a 7.12% CAGR over the next five years.

- By country, China led with 36.40% value share in 2025, while India is set for the fastest growth at a 6.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Professional Scalp Treatment Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of scalp disorders across urban APAC centres | 1.8% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Premiumisation of salon visits and service bundling in China, Japan & Korea | 1.5% | China, Japan, South Korea | Short term (≤ 2 years) |

| Natural/dermatologist-tested ingredient innovation | 1.2% | Global APAC | Long term (≥ 4 years) |

| Technological advancements in product formulation | 1.0% | Japan, South Korea, Singapore | Medium term (2-4 years) |

| Proliferation of trichology clinics in Tier-2 Chinese & Indian cities | 0.9% | China, India | Long term (≥ 4 years) |

| AI-powered scalp diagnostic devices in high-end salons | 0.6% | Japan, South Korea, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Scalp Disorders in Urban APAC

Airborne particulates and lifestyle stress combine to heighten seborrheic dermatitis, dandruff, and scalp sensitivity in megacities such as Beijing, Delhi, and Jakarta. Clinics in India reported 40% year-over-year growth in trichology consultations, while Richfeel expanded from 65 to more than 85 outlets between 2024 and 2025[1]Richfeel, “Richfeel Hair Transplant & Cosmetic Centres,” richfeel.com. As medical framing gains traction, professional regimens move from discretionary indulgence to requisite therapy, stimulating recurrent product usage and subscription-style treatment packages. Salons integrate microscopic scalp imaging to visualize pathology and justify premium fees, anchoring trust in professional recommendations. This medicalization widens the addressable base of the Asia-Pacific professional scalp treatment products market beyond traditional beauty consumers and insulates demand from macroeconomic volatility.

Premiumization of Salon Visits and Service Bundling

Head-spa culture in China, Japan, and Korea reshapes consumer expectations by packaging diagnostics, exfoliation, and follow-up retail products into 60- 90-minute rituals that command 3-4 × the ticket price of a standard haircut. Bundling lengthens dwell time, elevates perceived expertise, and drives higher customer lifetime value. Tier-2 Chinese cities adopt these experiential formats as rising middle-class consumers seek metropolitan wellness standards closer to home. Salon operators, in turn, secure back-bar exclusivity agreements with manufacturers, ensuring consistent sell-through of premium lines. The trend cements a lucrative sales channel for the Asia-Pacific professional scalp treatment products market while lowering churn for participating brands.

Natural and Dermatologist-Tested Ingredient Innovation

Millennial and Gen Z buyers routinely scrutinize INCI lists, favoring ECOCERT- or COSMOS-certified botanicals over synthetic preservatives. Korean entities filed 42.9% of global hair-loss cosmetic patents in 2025, with natural actives representing half of those submissions. Botanical extracts like green tea polyphenols and fermented ginseng gain traction once validated by peer-reviewed dermatology studies[2]Jaewon Ko, “Patent Applications for Hair-Loss Cosmetics in Korea Rank First Worldwide,” mk.co.kr. Laboratory testing augments the storytelling heritage of Asian traditional medicine, enabling brands to command 15-20% price premiums without sacrificing clinical credibility. Formulators respond with micro-encapsulated delivery systems that protect phytochemicals from oxidative degradation, elevating efficacy metrics that resonate in both salon and retail settings.

Technological Advancements in Product Formulation

AI-driven platforms such as Shiseido’s VOYAGER process half a million data points to predict ingredient interactions, compressing R&D timelines from months to weeks. Nanolipid carriers ferry actives through the stratum corneum to follicular roots, while micro-bubbles enhance cleansing without sulfates, sustaining consumer appetite for gentler formulations. Smart bottles embed NFC chips that sync with salon diagnostics, reminding clients to restock before product efficacy wanes. These innovations differentiate premium launches, elevate switching costs, and fortify the competitive moat surrounding advanced players in the Asia-Pacific professional scalp treatment products industry.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of professional treatments versus mass hair-care alternatives | -1.4% | India, Thailand, Malaysia, Indonesia, Vietnam, Philippines | Short term (≤ 2 years) |

| Grey-market and counterfeit product penetration on marketplaces | -0.8% | China, India, Southeast Asia | Medium term (2-4 years) |

| Fragmented regulatory and import duty regimes across APAC | -0.7% | Global APAC | Long term (≥ 4 years) |

| Shortage of certified trichology-skilled salon professionals | -0.5% | India, Thailand, Malaysia, Indonesia, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Professional Treatments

Five-to-ten-fold price gaps between professional formulas and mass-market shampoos deter adoption in lower-income economies. Budget-sensitive buyers in India and Indonesia often equate scalp wellness with discretionary beauty rather than health, stalling conversion rates. Brand owners pilot bridge-pricing strategies—mini-dose ampoules, installment-based salon packages, and entry-level SKUs—to broaden the funnel without diluting luxury positioning. Over time, improved socioeconomic indicators are expected to narrow the affordability divide, mitigating this drag on the Asia-Pacific professional scalp treatment products market.

Grey-Market and Counterfeit Product Penetration

Digital marketplaces simplify cross-border selling, giving counterfeiters low-cost access to brand-building assets they do not own. Near-perfect replicas of packaging for premium Japanese lines have surfaced on peer-to-peer platforms, threatening consumer safety and eroding trust. Authenticity seals, blockchain batch tracing, and salon-exclusive QR verification apps now form a multilayered defense. Despite progress, enforcement disparities across APAC jurisdictions extend litigation timelines and inflate compliance expenses, tempering near-term growth prospects of the Asia-Pacific professional scalp treatment products market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoos Retain Primacy as Scrubs Accelerate

Scalp-care shampoos accounted for 43.80% of the Asia-Pacific professional scalp treatment products market share in 2025, underlining their status as the essential first step in salon protocols and at-home maintenance. Therapeutic blends incorporating zinc pyrithione, salicylic acid, or green tea deliver clinically proven relief from dandruff and inflammation, differentiating professional SKUs from mass offerings. The segment’s stability affords brand owners predictable volume, allowing economies of scale that fund upstream R&D.

Exfoliant scrubs are poised to grow at a 6.65% CAGR to 2031, making them the fastest-rising niche within the Asia-Pacific professional scalp treatment products market. Inspired by skincare routines, consumers perceive scrubs as deep-cleanse complements to weekly regimens, validating premium pricing for granule-based or enzymatic formulations. Salon professionals favor scrubs for their visible “before-and-after” impact, which reinforces client confidence and drives retail take-home sales.

By Distribution Channel: Retail Dominates While Salons Gain Momentum

Retail captured 51.20% of the Asia-Pacific professional scalp treatment products market size in 2025, buoyed by specialty beauty chains and e-commerce platforms that stock salon-grade SKUs alongside mainstream labels. Online education modules and influencer content demystify professional jargon, enabling informed at-home usage without a stylist’s supervision. The channel also appeals to expatriates and travelers who prefer replenishment outside their home market.

Conversely, salon sales are expanding at a 5.05% CAGR, propelled by bundled service models that integrate diagnostics, exfoliation, and customized after-care. High-end chains embed AI microscopes into every station, printing micro-analysis reports that double as product prescriptions. The experiential differentiation available in salons fortifies stickiness, lifting average bill values and underpinning sustainable growth for the Asia-Pacific professional scalp treatment products market.

By Category: Synthetic Scale Holds, Natural Builds Loyalty

Synthetic formulations commanded an 81.90% share in 2025 with their' reliable performance, cost efficiency, and accelerated regulatory approvals. Decades of toxicology data streamline NMPA submissions in China and PMDA clearances in Japan, making synthetics the default for speed-to-market initiatives.

Natural and organic lines, however, will compound at 7.12% annually to 2031, outpacing the broader Asia-Pacific professional scalp treatment products market. Certifications such as ECOCERT and COSMOS, combined with dermatologist-published safety validation, foster consumer trust. Brands leverage fermented botanicals and up-cycled plant oils to balance efficacy with sustainability narratives, capturing a loyal cohort willing to trade up despite price differentials.

Geography Analysis

China's deep-rooted head-spa culture fuels a strong demand for multi-step treatments, effortlessly transitioning from salons to at-home routines. In May 2025, Henkel's USD 1.5 billion acquisition of Shiseido's regional professional hair unit underscores the optimistic outlook for premium offerings. Shanghai and Beijing, with their affluent clientele, see weekly scalp maintenance as a routine self-care practice rather than a luxury. Due to rapid digitalization, salons now harness customer-relationship platforms, automating re-booking and replenishment reminders, effectively safeguarding their market share from e-commerce gray marketers. India's growth story is driven by rising disposable incomes, urban migration, and a surge in scalp inflammation diagnoses, often attributed to pollution and dietary stress. The Asia-Pacific professional scalp treatment products market is thriving in tier-2 cities like Pune and Ahmedabad. Here, new clinics are introducing financing plans to ease the financial burden on clients. At the same time, domestic laboratories are collaborating with Ayurveda institutes, crafting botanically enriched actives. These partnerships align with regulatory preferences for indigenous ingredients, speeding up their market entry.

Japan and South Korea lead the way in technology-driven sophistication, with per-capita spending on scalp wellness exceeding USD 50 in 2025. Korean innovators hold a dominant 56.4% share of biomaterial patents focused on hair-loss solutions, showcasing the nation's dedication to life-science research and development. Singapore stands out as a regional testing ground for omnichannel strategies, capitalizing on its efficient HSA framework to fast-track approvals for new ingredients. Meanwhile, Southeast Asian countries, Thailand, Malaysia, Indonesia, Vietnam, and the Philippines—are witnessing a surge in salon constructions, driven by franchisors eager to establish a foothold, signaling a vast potential for market penetration.

Regulatory Landscape

Regulation for professional scalp treatment products in Asia-Pacific continues to diverge by claim type and route-to-market, with a clear pivot toward evidence-backed efficacy. In China, the National Medical Products Administration (NMPA) treats anti-hair loss claims as special cosmetics requiring registration, and the transition window for legacy special-use cosmetics ended on December 31, 2025. That change raises the bar for claim substantiation and dossier readiness for shampoos, serums, and ampoules positioned for hair-loss prevention.

Japan regulates medicated scalp-treatment products as quasi-drugs under the Ministry of Health, Labour and Welfare (MHLW) and the Pharmaceuticals and Medical Devices Act. Revised quasi-drug standards were phased in through September 30, 2026, with full compliance required from October 1, 2026. Across Southeast Asia, products generally align to the ASEAN Cosmetic Directive (ACD), with local enforcement such as Singapore's Health Products (Cosmetic Products - ASEAN Cosmetic Directive) Regulations (including amendments operational since November 2023) shaping ingredient and labeling compliance for multi-country rollouts. South Korea is tightening oversight of cosmetics purchased via overseas direct-to-consumer channels effective April 2, 2026, increasing compliance complexity for brands selling professional-grade scalp lines through cross-border e-commerce alongside salon distribution.

Competitive Landscape

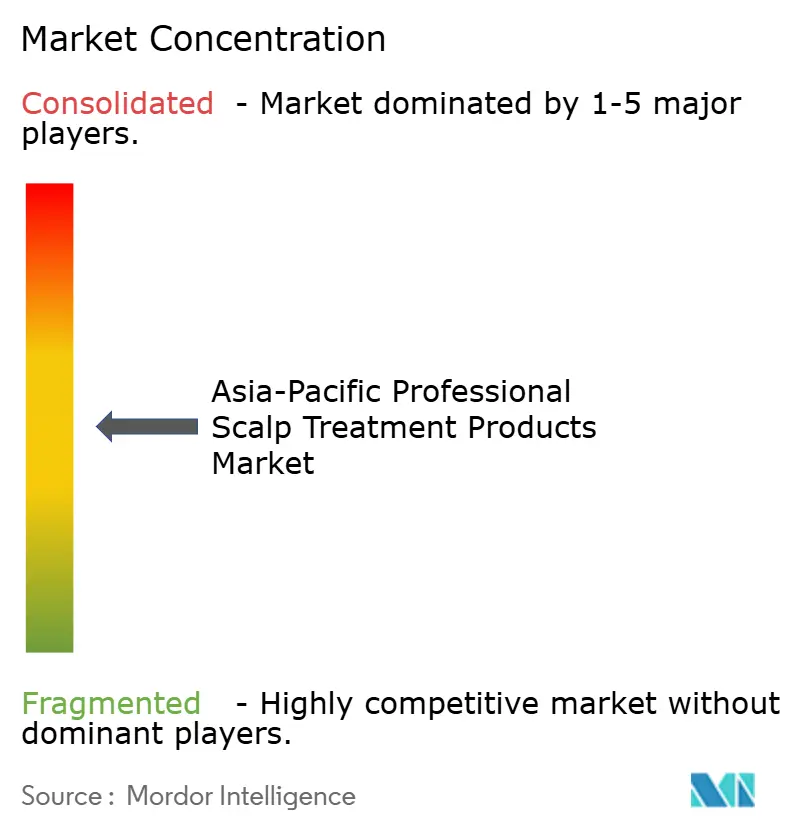

The Asia-Pacific professional scalp treatment products market exhibits moderate concentration, scoring 5 on a 10-point scale. Shiseido Professional, L’Oréal Professionnel, and Kao Corporation leverage decades-long stylist relationships and proprietary R&D pipelines to guard shelf space. Their salon-exclusive umbrellas grant preferential merchandising, training modules, and loyalty incentives that reinforce incumbent strength. Henkel’s 2025 acquisitions of Shiseido’s professional portfolio and P&G’s Vidal Sassoon Greater China operations illustrate escalating consolidation designed to aggregate intellectual property and regional distribution heft.

Against this backdrop, Korean innovators such as Amorepacific deploy AI-guided formulation engines and recyclable packaging to court eco-conscious millennials. Start-ups like Polyphenol Factory launch CES-debuted exfoliant scrubs that marry plant-derived polyphenols with volumizing polymers, carving defensible niches in fast-growing sub-segments. Salon disruptors, including K-HEADSPA, commercialize proprietary equipment and subscription-ready treatment protocols, shifting value capture toward service IP rather than standalone product sales. Intellectual-property intensity escalates as firms invest in microbiome modulation and peptide delivery systems, raising entry barriers for private-label laggards and cementing first-mover advantages within the apac professional scalp treatment products industry.

Asia-Pacific Professional Scalp Treatment Products Industry Leaders

Shiseido Professional (Henkel)

L’Oréal Professionnel

Kao Corporation

Amorepacific Corporation

KOSÉ Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Salon premiumization and the skinification of scalp care are expanding the space for clinical-grade regimens that combine diagnostics, in-salon protocols, and take-home maintenance. L'Oreal's Professional Products Division highlighted this shift in Thailand by deploying AI-powered scalp diagnostics (such as K-Scan) and aligning professional hair and scalp routines with skincare-style actives. The resulting service bundling helps lift retail attach rates in salons, which aligns with the report's observed move from reactive repair to preventive scalp wellness.

Regulatory fragmentation and tighter claim substantiation requirements are also shaping where brands place innovation bets, creating room for compliant, data-supported positioning in special-claim segments such as anti-hair loss and sensitive scalp. Large players are building Asia-focused portfolios that can be localized by hair type and consumer needs, including Kao Corporation's July 2026 strategy that elevates Liese as a strategic Asian hair-care growth brand built on research into black hair and integrated damage-care technologies. On the supply side, ingredient and manufacturing capability investments, including Nicca Chemical Co., Ltd.'s concept plant initiative aimed at increasing production capacity and productivity for hair and scalp care with full-scale operation planned for 2026 or later, support faster scaling of differentiated actives and formats used in professional scalp treatments.

Recent Industry Developments

- July 2026: Kao Corporation announced a plan to expand the Liese hair color series to seven countries and regions in Asia starting August 2026 as part of its Asia-focused hair care growth strategy. The plan strengthens Kao's professional-adjacent salon and premium retail ecosystem by pairing color expansion with damage-care positioning, supporting scalp and hair health routines that are commonly bundled in high-end services.

- October 2025: Shiseido Professional launched the Sublimic Timetic scalp and hair care range across eight Asian markets including Japan, China, Korea, Hong Kong, Taiwan, Singapore, Malaysia, and Thailand. The multi-market rollout indicates a broader push for premium, protocol-driven salon offerings that standardize treatment menus and drive follow-on retail sales across key Asia-Pacific hubs.

- April 2024: Shiseido Professional refreshed visibility for its Adenovital scalp-care proposition through a relaunch activation tied to premium salon treatment experiences in Southeast Asia. This reinforced the brand's emphasis on scalp-first regimens within the professional channel, supporting higher-value service add-ons and recurring product replenishment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of professional scalp treatment products sold across Asia-Pacific for use in salon and professional-led scalp care routines, where the product is positioned to treat or manage scalp concerns and is purchased through professional and associated retail routes.

Scope exclusions: Excludes scalp treatment services, devices, and prescription medicines used for scalp conditions.

Segmentation Overview

- By Product Type

- Scalp-care Shampoo

- Conditioner & Mask

- Oils & Serums/Ampoules

- Exfoliant Scrubs

- Others

- By Distribution Channel

- Salons

- Retail Channels

- By Category

- Natural/ Organic

- Synthetic/ Conventional

- By Country

- China

- Japan

- India

- South Korea

- Taiwan

- Australia

- Singapore

- Thailand

- Malaysia

- Indonesia

- Vietnam

- Philippines

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping scalp and hair care categories in Asia-Pacific, then narrowing it to professional scalp treatment products that are used in salon-led routines. We lean on public sources such as national statistics offices for consumer spending series, health agencies for dandruff and dermatitis awareness indicators, customs portals for import and export flows of relevant cosmetic categories, and standards regulators that publish cosmetics ingredient and labeling rules.

To keep the model grounded, we also review company annual reports, investor presentations, product launch news, and salon industry association publications that describe channel shifts and pricing direction. Patent databases are checked to understand which active ingredients and formats are seeing higher development, which then informs the product-mix assumptions used in the model. For cross-checking company scale and channel exposure, a paid subscription for company financials and intelligence is used in a limited way. The sources listed here are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what is actually sold as a scalp treatment in professional settings, and how it moves through salons, distributors, and premium retail in markets like China, Japan, South Korea, India, and the wider APAC region. We spoke with a mix of brand-side professionals, salon channel executives, distributors, and practitioners to validate pricing ladders, product usage frequency, and how demand changes with promotions and new routine trends.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | |

| Mid tier: 57% | Functional/Unit leaders: 38% | |

| Smaller Players: 17% | Managers: 50% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where Asia-Pacific hair care value is reconstructed into a professional scalp treatment pool using country-level channel splits and the share of scalp-treatment labeled products within professional hair care. Once that demand pool is set, it is pressure-tested using selective bottom-up checks, such as sampled average selling prices by format (serums and ampoules versus masks and exfoliants) multiplied by salon usage volumes and distributor throughput estimates.

A few inputs that matter in this market include the number of active salons and premium outlets by country, the penetration of scalp-focused add-on routines in salon menus, typical pack sizes and recommended-use frequency, online share for professional brands, and the pricing gap between treatment formats and standard hair cleansing products. Where country-level data is thin, we fill gaps using proxy indicators like urban population, premium personal care spend trends, and import intensity for relevant cosmetic categories, and then validate the shares through interviews. For forecasting, scenario analysis is used so we can reflect different paths for premiumization and salon traffic recovery, and the final trajectory is aligned to expert consensus on pricing progression and adoption of scalp wellness routines.

Data Validation & Update Cycle

Outputs are checked in several steps, starting with internal variance tests across countries, product formats, and channel splits so large jumps are challenged early. We compare the final totals against independent signals such as reported beauty and personal care growth rates, visible price moves in professional retail, and trade flow direction for similar cosmetic groupings, and then outliers are reviewed again before sign-off.

The model is also reviewed by another analyst to confirm that assumptions are consistent with interview feedback and desk references. Reports are refreshed annually, and if a material event happens (for example, a major regulation change on cosmetics labeling or a sharp pricing shift in a key country), the assumptions are revisited and the forecast is adjusted. Before delivery, a final pass is done so clients receive an updated view that matches the latest available information.

Mordor Intelligence's Asia Pacific Professional Scalp Treatment Products Market Sizing Compared With Other Published Estimates

Published market values for this space can look far apart because authors do not always use the same definition of what counts as a professional scalp treatment product, and they also pick different timeframes and growth cases. The biggest differences usually come from whether the scope is product-only or product-plus-service, how professional channels are treated, and which countries are included inside Asia-Pacific.

Devices used in clinics and medical spas sit outside Mordor Intelligence's scope, and that inclusion choice can raise totals when other publishers bundle device revenues with topical products. Some estimates also extend the scope into consumer retail scalp care and count general anti-dandruff shampoos as treatment by default, which inflates volume in high-population markets. We also see that refresh cadence and currency timing can shift the USD value even when local consumption is stable, due to fast-moving pricing and exchange rates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.10 B (2025) | |

| Global Consultancy A | USD 2.80 B (2026) | Includes professional-use devices and clinic procedure-linked revenues alongside topical products, and uses a longer 2026 to 2035 horizon that can compound higher growth assumptions. |

| Regional Consultancy B | USD 1.80 B (2026) | Uses a broader channel definition that blends salon and general retail availability, and the starting year differs, which changes the assumed price base and currency conversion timing. |

Looking at the spread, the main driver is what gets counted as a product market versus a wider professional scalp care ecosystem, and that is where device and clinic-linked revenue treatment creates the largest gap. When scope is kept product-only and tied to clear channel and format assumptions, the resulting market value stays easier to trace back to practical demand and repeatable inputs.

Key Questions Answered in the Report

How much are professional scalp treatment products worth across Asia-Pacific in 2026?

Sales equal USD 1.17 billion, reflecting strong demand for preventive scalp wellness solutions.

What compound annual growth rate is forecast through 2031?

Value is projected to rise at a 6.57% CAGR, taking sales to USD 1.61 billion by 2031.

Which product type currently contributes the most revenue?

Scalp-care shampoos lead with 43.80% share thanks to their role as the first step in salon and at-home regimens.

Which product category shows the fastest expansion?

Exfoliant scrubs are growing at a 6.65% CAGR as multi-step routines gain popularity.

Which sales channel captures the largest portion of purchases?

Retail accounts for 51.20% of value, driven by beauty specialty chains and e-commerce convenience.

Page last updated on: