Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

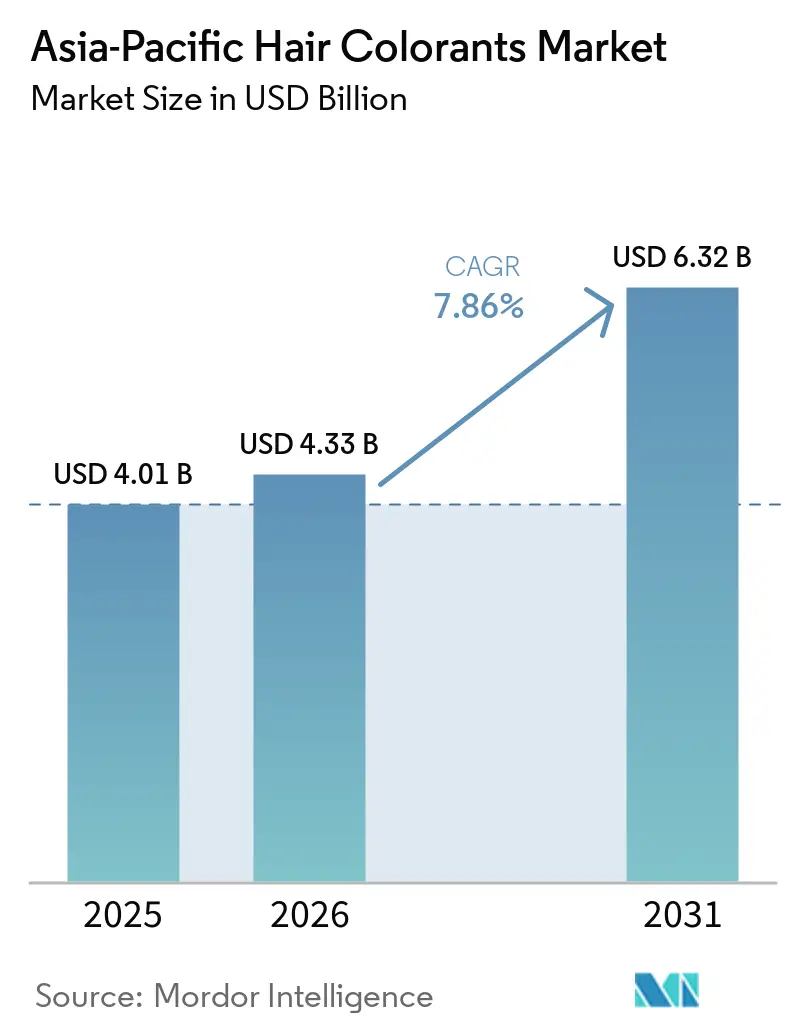

| Base Year Market Size (2025) | USD 4.01 Billion |

| Market Size (2026) | USD 4.33 Billion |

| Market Size (2031) | USD 6.32 Billion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Hair Colorants Market Analysis by Mordor Intelligence

The Asia-Pacific hair colorants market size is expected to grow from USD 4.01 billion in 2025 to USD 4.33 billion in 2026 and is forecast to reach USD 6.32 billion by 2031 at 7.86% CAGR over 2026-2031. In Northeast Asia, an aging demographic is driving sustained demand, while in South and Southeast Asia, a burgeoning middle class is flexing its purchasing power. Technology is bridging the gap between traditional salons and at-home beauty applications, making premium beauty solutions more accessible to a wider audience. Consumers aged 45 and older anchor the demand for gray-coverage products, as this demographic increasingly seeks effective and convenient solutions for hair care. Meanwhile, as incomes rise, first-time buyers in India, Indonesia, and Vietnam are leaning towards ammonia-free and botanical formulations, reflecting a growing preference for products perceived as safer and more natural. Platforms like Douyin, Tmall, and Nykaa are leveraging livestreaming and AI-driven virtual try-on tools, which not only shorten consideration cycles but also encourage shade experimentation, leading to more frequent repeat purchases. These tools enhance consumer engagement by offering personalized experiences and reducing hesitation in product selection. In Japan, South Korea, and China, regulatory shifts are altering formulation strategies, benefiting companies that can swiftly and broadly demonstrate safety and efficacy. This regulatory recalibration is pushing brands to innovate and adapt quickly to maintain compliance and consumer trust.

Key Report Takeaways

- By type, permanent hair colors led with 46.72% of the Asia-Pacific hair colorants market share in 2025, whereas semi-permanent variants are projected to post a 9.08% CAGR to 2031.

- By category, mass products accounted for 67.95% of the Asia-Pacific hair colorants market size in 2025, while the premium tier is on track for a 9.62% CAGR through 2031.

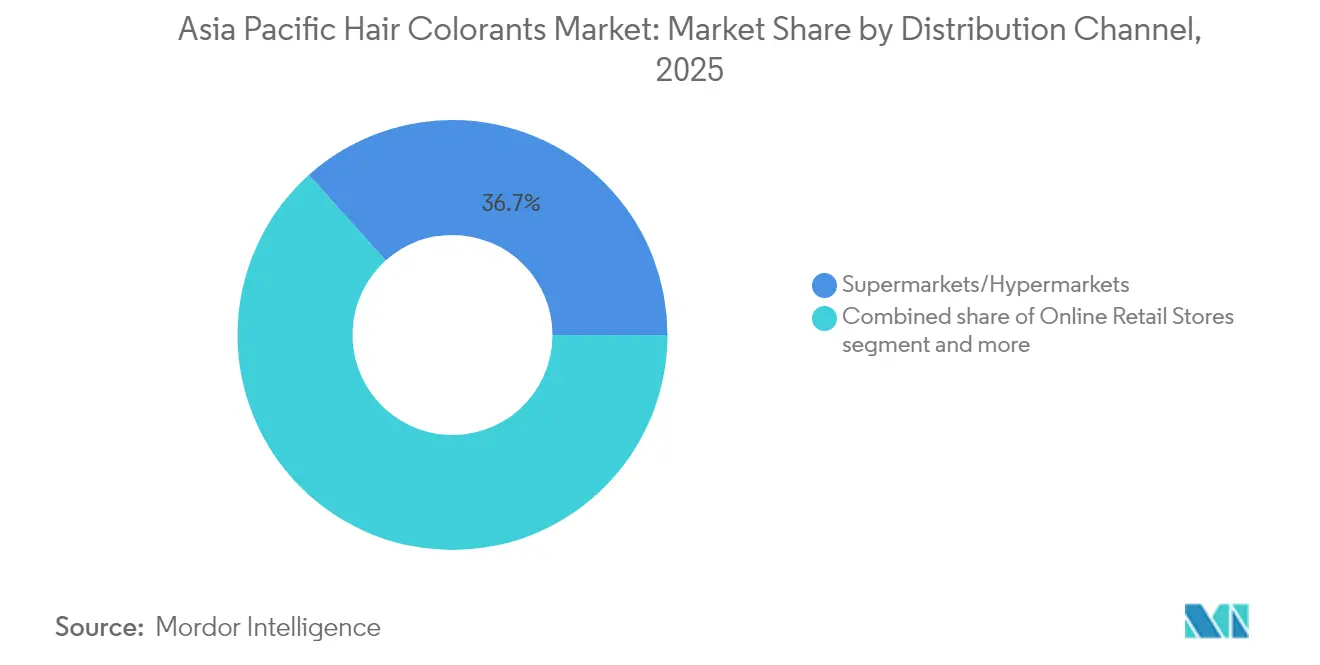

- By distribution channel, supermarkets and hypermarkets commanded 36.65% revenue in 2025, yet online retail is set to expand at an 8.01% CAGR over 2026-2031.

- By geography, China held 33.85% share in 2025, but India is the fastest-growing country with a 10.11% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Hair Colorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income and beauty consciousness | +1.8% | China, India, Indonesia, Vietnam, Thailand | Medium term (2-4 years) |

| Shift toward ammonia-free and natural formulations | +1.5% | Japan, South Korea, urban China, India | Long term (≥ 4 years) |

| Expansion of e-commerce and social commerce | +1.3% | China, India, South Korea, Southeast Asia | Short term (≤ 2 years) |

| Aging population seeking gray-coverage solutions | +1.2% | Japan, South Korea, urban China, Australia | Long term (≥ 4 years) |

| AI/AR virtual try-on accelerating online sales | +0.9% | China, South Korea, Japan, urban India | Medium term (2-4 years) |

| Govt-led "Make-in-India" herbal push | +0.7% | India, with spillover to Bangladesh, Nepal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising disposable income and beauty consciousness

In 2024, key Asia-Pacific economies saw per-capita disposable income rise between 2.1% and 7.6%, giving beauty shoppers more discretionary funds. In Japan and South Korea, consumers earning over USD 30,000 are increasingly investing in gray-coverage products that also serve as scalp-care treatments, reflecting a growing preference for multi-functional beauty solutions. Meanwhile, younger buyers in Indonesia and Vietnam are entering the market with budget-friendly sachets, which provide an accessible entry point for first-time users. A regional consumer study revealed that over 50% of respondents would consider switching brands for products with enhanced hair-health benefits, highlighting the rising importance of innovation in product attributes. This signals to manufacturers the importance of maintaining a diverse pricing strategy: offering premium SKUs for affluent seniors who prioritize quality and efficacy, while also providing affordable, multi-benefit options for newcomers seeking value. As retailers push for localized product ranges that align with city-specific income levels, efficient assortment planning has become essential to meet the varied demands of these diverse consumer segments.

Shift toward ammonia-free and natural formulations

Brands, responding to consumer concerns over ammonia's scalp irritation and its strong odor, are reformulating their products across both premium and mass tiers. In 2024, Godrej Professional Probio made its debut, offering 100% gray coverage in 43 shades without ammonia, specifically catering to salons prioritizing comfort and safety for their clients. Wella Professionals rolled out Illumina Color, leveraging microlight technology to lighten the chemical load while maintaining color brilliance, appealing to professionals seeking high-performance yet gentle solutions. Japan has enacted a new labeling law, emphasizing patch-test warnings for products with p-phenylenediamine, further driving the industry's shift towards blends with fewer irritants to meet regulatory compliance and consumer demand for safer alternatives. In India, supply chains for henna, indigo, and amla are now adopting ISO and organic certifications, signaling a maturation in the use of botanical raw materials and ensuring higher quality and traceability standards. However, the industry faces a looming challenge: weather-related shocks that can diminish crop yields, potentially pushing a temporary reliance on synthetic substitutes, which may impact the market's focus on natural and organic formulations.

Expansion of e-commerce and social commerce

In 2024, beauty e-commerce penetration hit China, South Korea, and in India, reflecting the growing consumer preference for online platforms in the beauty market. Douyin's livestream sessions showcased the power of influencers, raking in beauty GMV that surpassed RMB 500 billion. These sessions highlight how quickly influencers can drive consumer interest and convert it into completed transactions, emphasizing their critical role in the digital beauty ecosystem. Indian e-commerce giants Nykaa, Amazon, and Flipkart now boast over 200 hair-color brands, a stark contrast to the mere 20-30 SKUs found in most tier-2 supermarkets, showcasing the expansive product variety available online. While retailers bolster their online presence with in-store color-matching kiosks and patch-test services to enhance the customer experience, they recognize that sustained digital engagement is crucial for visibility and customer retention. Yet, this reliance on platform algorithms leaves brands vulnerable, as sudden ranking shifts can drastically diminish traffic and impact sales performance.

Aging population seeking gray-coverage solutions

Japan, home to over 36 million residents aged 65 and above, sees this demographic favoring enduring gray coverage that reduces the need for frequent reapplications, making hair care a key market for age-specific innovations.[1]Source: Mizuho Bank, “Medium-term Outlook for Japanese Industry”, mizuhogroup.com This preference stems from the desire for convenience and products that align with their lifestyle needs. Shiseido, in a bid to cater to this audience, conducts complimentary beauty seminars, framing color application as an integral facet of holistic self-care. These seminars not only educate seniors on product usage but also promote a sense of community and well-being. Meanwhile, in South Korea, with per-capita GNI exceeding USD 36,000 in 2024, older consumers continue to be active spenders, even amidst broader economic downturns[2]Source: Ministry of Culture, Sports and Tourism, “2024 per capita GNI of USD 36,624 surpasses Japan, Taiwan”, korea.net. This financial stability enables them to invest in premium products that address their specific needs. Brands are innovating by blending UV filters, anti-hair-loss peptides, and moisturizers into their gray-coverage offerings, aiming to siphon market share from neighboring hair-care categories. These formulations cater to both aesthetic and functional demands, providing comprehensive solutions for aging hair. A notable strategic opportunity emerges in subscription models, which promise auto-shipped refills every six weeks, ensuring sustained consumer engagement without the need for physical store visits. This model not only enhances convenience but also fosters brand loyalty by maintaining consistent product availability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent chemical-safety regulations | −0.5% | Japan, South Korea, China, ASEAN | Short term (≤ 2 years) |

| Allergy and sensitivity concerns | −0.3% | Global, higher incidence in Japan, South Korea | Medium term (2-4 years) |

| Counterfeit and grey-market colorants | −0.4% | China, India, Indonesia, Vietnam | Medium term (2-4 years) |

| Climate-driven plant-pigment supply shocks | −0.2% | India, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent chemical-safety regulations

In 2024, Japan amended its Pharmaceutical and Medical Device Act, mandating prominent front-of-pack warnings for dyes like p-phenylenediamine and toluene-2,5-diamine[3]Source: Ministry of Health, Labour and Welfare, “THE JAPANESE PHARMACOPOEIA”, mhlw.go.jp. This change also extended the lead times for compliance labeling. Meanwhile, South Korea imposed a ban on 15 additional ingredients, pushing local brands to swiftly reformulate their products. In China, brands must now provide in-vivo efficacy data before they can make anti-gray or anti-hair-loss claims on their packaging. This requirement can inflate launch budgets by an additional USD 50,000-200,000 per SKU and delay the process by six to 12 months. While ASEAN has introduced a harmonized directive for mutual recognition of safety assessments, discrepancies in language-specific labeling rules continue to disrupt supply chains. Furthermore, smaller firms, often without dedicated regulatory teams, are increasingly collaborating with contract manufacturers. This shift allows them to distribute documentation costs across a broader client base.

Counterfeit and grey-market colorants

In 2023, China's State Administration for Market Regulation confiscated over 3,200 cases of counterfeit cosmetics, with many found to contain undisclosed heavy metals, posing significant health risks to consumers. In 2024, India's CDSCO seized illegal hair dyes worth INR 50 million in Delhi, further exposing weaknesses in monitoring rural supply chains and enforcement mechanisms. Counterfeit products can undercut genuine SKUs by as much as 60%, not only eroding revenue streams but also severely impacting brand trust and consumer loyalty. In response, leading brands are now incorporating QR-code authentication on their packaging to combat counterfeiting. For instance, L’Oréal's 2024 pilot program in Shanghai enables consumers to verify product authenticity in mere seconds, enhancing transparency and trust. However, enforcement actions remain largely reactive: seizures typically happen post-consumer complaints, rather than preemptively before market entry. This reactive approach prolongs the challenge of maintaining premium pricing and addressing the broader issue of counterfeit goods in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type

In 2025, the Asia-Pacific hair colorants market saw permanent dyes leading the charge, accounting for 46.72% of the total revenue. Their widespread appeal can be attributed to a strong preference for long-lasting gray coverage and consistent shade retention, especially among salon-goers. Brands like Wella are at the forefront, introducing advanced formulations like Illumina Color, which reduce chemical stress and offer fade resistance for up to eight weeks. This segment thrives on its durability and the trust of mature consumers, who often prioritize reliability and quality over experimentation. Innovations in this category are increasingly emphasizing safety and sensory experiences, such as minimizing scalp irritation and enhancing the overall application process. Yet, with mid-tier competitors exerting pricing pressures, market players are compelled to invest heavily in research and development to uphold their premium status and differentiate their offerings in a competitive landscape.

Semi-permanent colorants are emerging as the region's fastest-growing segment, with projections indicating a robust 9.08% CAGR. Their rising popularity is largely fueled by Gen Z's penchant for frequent color changes, often inspired by social media trends favoring pastel and neon shades. These colorants cater to a younger demographic that values self-expression and flexibility, making them a preferred choice for temporary transformations. Moreover, lighter compliance regulations and reduced entry barriers have made these colorants more accessible, especially to younger consumers and those coloring at home. In Japan, stricter allergen labeling standards, particularly impacting oxidative dyes, are redirecting innovation budgets. Brands are now pivoting towards softer, non-sensitizing wash-out tints. Godrej and Hoyu are leading this shift, offering ammonia-free and quick-application formats. These innovations not only prioritize user comfort and time efficiency but also enhance purchase frequency through bundled aftercare products, which include conditioners and treatments designed to prolong color vibrancy and maintain hair health.

By Category: Premium Segment Gains Despite Mass Dominance

In 2025, mass hair color products dominated the Asia-Pacific market, capturing 67.95% of the total market share. This stronghold is largely attributed to price-sensitive consumers in rural China, tier-2 cities in India, and Indonesia, where sachets priced under USD 1 are a hit. These affordable options cater to a broad demographic, particularly in regions where disposable incomes remain limited, making them a preferred choice for everyday use. Yet, urban consumers are making a noticeable pivot towards premium SKUs, drawn by added perks like scalp care, botanical ingredients, and AI-driven shade selection. Major players, including L’Oréal Professional and Kao’s Goldwell, are bolstering their salon presence by offering exclusive services and products tailored to meet evolving consumer preferences. Meanwhile, Amorepacific is harnessing advanced scalp analysis tech to validate the costs of salon visits, providing a personalized experience that appeals to high-income consumers. Additionally, regulatory compliance costs are propelling the growth of the premium segment, as companies find it easier to absorb these expenses at elevated price points, ensuring product quality and safety.

Forecasts indicate the premium segment will outpace others with a robust CAGR of 9.62% through 2031, fueled by rising disposable incomes in nations like Japan, South Korea, and Singapore. This segment is also riding the wave of sustainability trends, such as recyclable packaging and renewable energy, striking a chord with eco-conscious consumers in Australia and the Philippines. These initiatives not only enhance brand reputation but also align with the growing demand for environmentally responsible products. Multinational giants are adeptly balancing their offerings to cater to both budget and premium markets. A case in point is Procter & Gamble, which seamlessly pairs Pantene sachets with Wella Professionals salon products, ensuring accessibility for price-sensitive buyers while maintaining a foothold in the premium category. The growing margin contribution from the premium segment underscores its strategic significance, even as mass formats continue to lead in volume. This dual approach allows companies to maximize market penetration while addressing diverse consumer needs.

By Distribution Channel: Online Retail Disrupts Supermarket Dominance

In 2025, supermarkets and hypermarkets captured the lion's share of the market, accounting for 36.65% of total revenue. Their success stems from drawing in high foot traffic and prominently displaying impulse products. These traditional retail outlets remain a go-to for customers prioritizing convenience and in-person guidance. Yet, as digital innovations reshape shopping habits, health-and-beauty chains like Watsons are leading the charge. By incorporating tools like color try-on mirrors, they're seamlessly merging offline expertise with online ease in Southeast Asia. This not only elevates the shopping experience but also bolsters the standing of supermarkets and hypermarkets amidst the growing e-commerce wave.

Online retail channels are witnessing the most rapid growth, boasting an impressive CAGR of 8.01%. This surge is largely fueled by the rise of livestreaming sales and the ability to fulfill orders on the same day from regional warehouses. China stands at the forefront of this online boom. A significant catalyst was Douyin's introduction of one-click checkout during beauty demos, which dramatically heightened online sales conversions. Meanwhile, in India, e-commerce is on a fast track, with platforms like Nykaa championing at-home beauty kits. These kits, birthed during pandemic lockdowns, are now encouraging users to experiment beyond salon confines. To navigate challenges like platform algorithm shifts and rising commissions, industry frontrunners are embracing omnichannel tactics. These include strategies like ship-from-store, click-and-collect, and cross-channel loyalty programs. Additionally, they're ensuring adherence to regulations, especially concerning transparency in livestream marketing.

Geography Analysis

In 2025, China accounted for 33.85% of the Asia-Pacific hair colorants market revenue, driven by its 1.4 billion-strong population and a well-established e-commerce framework. However, growth is showing signs of moderation; L’Oréal reported a 3.1% dip in sales for North Asia during the initial nine months of 2024, attributed to a softer consumer sentiment. Stricter regulatory mandates now require clinical proof for anti-gray claims, significantly increasing costs and time. As a result, multinationals are opting for country-specific SKUs over pan-regional packs. Despite this, export data reveals that Chinese manufacturers are capitalizing on RCEP tariff benefits. Notably, cosmetics exports from Guangzhou to RCEP member states surged by 72.5%, reaching RMB 2.59 billion in 2023, suggesting that production capabilities are outpacing domestic demand.

India emerges as the fastest-growing market, projected to grow at a 10.11% CAGR. Godrej's expansion worth INR 3.5 billion in Baddi and Dabur's INR 2 billion enhancement in Jammu are set to boost ammonia-free and henna-based production capacities. However, erratic monsoons in 2024 led to reduced henna harvests in Rajasthan, causing a surge in raw material prices by double digits. In response, brands are diversifying their supplier networks across multiple states and exploring hedging substitutes to maintain their natural product claims. The merger and acqusition landscape is buzzing, highlighted by Marico's minority stake acquisition in Just Herbs and Nykaa's investment in Dot & Key, signaling a strategic move to engage with emerging direct-to-consumer brands.

Japan, South Korea, and Australia stand out as affluent yet aging markets, offering lucrative rewards for premium innovations. Products targeting gray coverage are seeing heightened demand, especially from seniors willing to invest in low-odor creams that promise eight-week color retention with minimal scalp irritation. Shiseido's prominence as the leading foreign brand in Japan in 2024 can be attributed to its specialized salon education programs catering to older clientele. With a per-capita GNI exceeding USD 36,000, South Korea showcases resilience against economic fluctuations, a trait further enhanced by Amorepacific's innovative use of AI scalp diagnostics for personalized color care upselling. Australia's diverse demographic landscape not only broadens shade portfolios but also benefits from steady unit growth due to positive migration trends. Southeast Asia is catching up swiftly, with Indonesia, Thailand, and Vietnam reaping the rewards of robust e-commerce platforms like Shopee and Lazada. Riding this wave, Chinese brand Biqian is making its mark with affordable sub-USD 3 sachets, appealing to the youth's value segment. Meanwhile, in the Philippines and Malaysia, a growing environmental consciousness is prompting companies to emphasize recyclability in their messaging, aiming for premium shelf visibility.

Competitive Landscape

The Asia-Pacific hair colorants market displays moderate concentration. L’Oréal, Henkel, Kao, Procter & Gamble, and Shiseido leverage their substantial research and development budgets, diverse distribution channels, and adept navigation of regulations to command the largest market share. A testament to this commitment, Henkel inaugurated a CNY 100 million research and development center in Shanghai in January 2024, focusing on color chemistry tailored for Asia's thicker, straighter, and darker hair, while ensuring swift compliance with evolving ingredient regulations. Meanwhile, multinationals are harnessing AI innovations, with L’Oréal's Beauty Genius, Kao's K27 strategy, and Amorepacific's SensornoidTM leading the charge in personalized shade matching and data-driven insights.

Regional players are carving out their own spaces, often intertwining cultural narratives with botanical authenticity. For instance, Godrej Consumer Products infuses Ayurveda into its ammonia-free hair color range, distributing through an expansive network of 45,000 salons across India. Similarly, Dabur promotes its henna-infused Vatika line through both drugstores and e-commerce platforms. Amorepacific and Shiseido, on the other hand, are capitalizing on the global allure of K-beauty and J-beauty, respectively, turning their rich heritage into a premium pricing strategy. Meanwhile, disruptive Chinese brands like Florasis and Perfect Diary are tapping into national pride, offering products at sub-USD 10 price points on local platforms, directly challenging established players.

However, the industry's heavy reliance on platform algorithms poses a collective risk. In 2024, Chinese authorities cracked down on misleading cosmetic claims, leading to influencers having to retract product endorsements mid-campaign. This incident underscored many brands' limited direct access to consumers. Additionally, the widespread issue of counterfeiting is squeezing profit margins, pushing the industry to explore solutions like QR-code authentication and blockchain technology, albeit with a call for collective industry collaboration.

Asia-Pacific Hair Colorants Industry Leaders

L'Oreal SA

Henkel AG & Co. KGaA

Godrej Consumer Products Limited

Kao Corporation

Coty Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Italy's Actium Plus unveiled Procalp Activ Color+, a dermatologist-approved permanent hair color, in India. This cutting-edge product guarantees vibrant, enduring results with full grey coverage, all while being gentle on sensitive scalps. Thanks to the advanced Intellicolor™ Technology, Procalp Activ Color+ ensures uniform color absorption. It's also enriched with nourishing ingredients that bolster hair strength and reduce breakage.

- September 2025: Chik Quick Crème Hair Color delivered a vibrant, natural hue with complete grey coverage in a mere 10 minutes, streamlining the coloring process. Infused with the benefits of amla and bhringraj, it nourishes while it colors. The ammonia-free formula ensures a milder experience and is crafted for easy application, appealing to those desiring a swift, effective, and convenient hair coloring solution that prioritizes hair health.

- March 2025: Paradyes introduced India's inaugural semi-permanent hair color brand, boasting chemical-free, vibrant shades specifically for Indian hair. Their lineup features Glossy Hair Tints for a natural, bleach-free look lasting over 20 washes, and Timeless Hair Tints for permanent, 100% grey coverage. With no PPD, ammonia, or resorcinol, the formulas guarantee a safe application, enhanced by nourishing herbal infusions.

- November 2024: CavinKare's Indica debuted the Indica Natural and Nourish Crème Hair Color, marking its entry into the crème hair color arena. This product boasts a low-dye chemical formula for a healthier coloring experience. Priced at Rs. 15, it promises 100% grey coverage in shades like Natural Black, Dark Brown, and Burgundy. Infused with nourishing oils such as onion, argan, and coconut, it appeals to Indian consumers with a penchant for sustainable beauty.

Asia-Pacific Hair Colorants Market Report Scope

Hair colorants are a group of commercial products that can change the color of hair in a wide range of tones and shades, from very light blonde to black and everything in between, including golden ash, reddish, mahogany, violet, etc. The product type, distribution channel, and geographic segments of the Asia-Pacific hair colorants market. Based on the product type, the market is segmented into bleachers, highlighters, permanent colorants, semi-permanent colorants, and other hair colorants. Based on the distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, department stores, pharmacies and drugstores, specialist retailers, online retail, and others. Based on country, the market is segmented into China, India, Japan, Australia, and the Rest of Asia Pacific. The report offers the market size and forecasts in value (USD million) for the above segments.

By Type

| Bleachers |

| Highlighters |

| Permanent Colorants |

| Semi-Permanent Colorants |

| Temporary Colorants |

By Category

| Mass |

| Premium |

By Distribution Channel

| Health and Beauty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Distribution Channels |

Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Type | Bleachers |

| Highlighters | |

| Permanent Colorants | |

| Semi-Permanent Colorants | |

| Temporary Colorants | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Health and Beauty Stores |

| Supermarkets/Hypermarkets | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Country | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific hair colorants market in 2026 and how fast is it growing?

The market stands at USD 4.33 billion in 2026 and is forecast to reach USD 6.32 billion by 2031, registering a 7.86% CAGR.

Which product type is expanding the fastest?

Semi-permanent hair colors lead growth with a projected 9.08% CAGR to 2031 as younger buyers favor fashion shades and wash-out formats.

Why is India considered the most attractive growth market?

Government incentives for herbal manufacturing, rising disposable income, and rapid e-commerce penetration support a 10.11% CAGR through 2031.

How are regulations affecting product development?

Stricter safety and efficacy rules in Japan, South Korea, and China extend launch timelines by up to 12 months and raise formulation costs, favoring firms with strong compliance infrastructure.

Page last updated on: