Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.4 Billion |

| Market Size (2026) | USD 7.58 Billion |

| Market Size (2031) | USD 8.57 Billion |

| Growth Rate (2026 - 2031) | 2.48% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Maize Seed Market Analysis by Mordor Intelligence

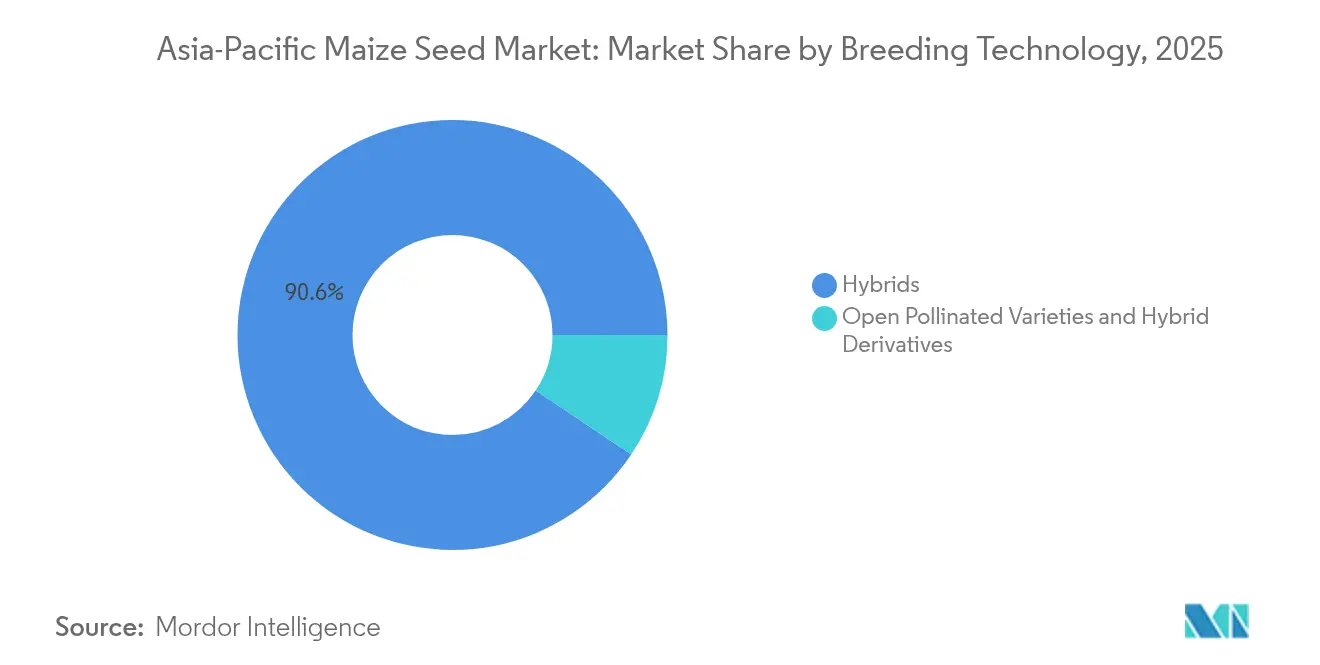

Asia-Pacific maize seed market size in 2026 is estimated at USD 7.58 billion, growing from 2025 value of USD 7.4 billion with 2031 projections showing USD 8.57 billion, growing at 2.48% CAGR over 2026-2031. This moderate growth pace reflects the region’s steady transition away from saved seed toward commercial hybrids in response to rising demand for feed-grade corn, supportive minimum-support-price reforms, and the expansion of precision agriculture adoption. China’s 82.2% revenue dominance underscores both its technological leadership and the scale of its corn belt, while Bangladesh leads growth with a 6.77% CAGR as poultry integrators intensify local grain sourcing. Hybrid varieties command 91.1% of the Asia-Pacific maize seed market, yet open-pollinated varieties and hybrid derivatives post the fastest 3.41% CAGR, signaling a dual-speed landscape where resource-constrained farmers pursue intermediate genetics before graduating to full hybrids. Competitive intensity revolves around trait stacking for drought tolerance, last-mile distribution strength, and bundled precision services that optimize seeding densities for mechanized harvest.

Key Report Takeaways

- By breeding technology, hybrids captured 90.62% of the Asia-Pacific maize seed market share in 2025, while open-pollinated varieties and hybrid derivatives posted the fastest 3.28% CAGR through 2031.

- By country, China held 81.65% of the Asia-Pacific maize seed market size in 2025, while Bangladesh records the highest 6.55% CAGR through 2031.

- The top five players controlled approximately 29% of the total market value in 2024. These major companies include Bayer AG, Corteva Agriscience, Advanta Seeds, Beidahuang Kenfeng Seed Co., Ltd, and Syngenta Group.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Maize Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid replacement of saved seed with single-cross hybrids | +0.8% | China, India, Vietnam, and Thailand | Medium term (2-4 years) |

| Government minimum-support-price (MSP) reforms in India and Pakistan | +0.6% | India, Pakistan, and Bangladesh | Short term (≤ 2 years) |

| Expansion of feed-grade corn demand from Southeast Asian poultry integrators | +0.4% | Thailand, Philippines, Vietnam, and Indonesia | Medium term (2-4 years) |

| Roll-out of drought-tolerant maize hybrids via CIMMYT–public sector alliances | +0.3% | India, Bangladesh, Myanmar, and Pakistan | Long term (≥ 4 years) |

| Precision-ag services bundling seed and drone-based variable-rate sowing | +0.2% | China, Australia, Japan, and Thailand | Long term (≥ 4 years) |

| Carbon-credit monetization programs rewarding high-yield maize rotations | +0.1% | Australia, India, China, and Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid replacement of saved seed with single-cross hybrids

Vietnam’s GM corn acreage expanded from 4% in 2015 to 26.5% in 2022, showcasing how demonstration plots and contract farming accelerate hybrid uptake. Yield advantages of 20–30% over open-pollinated varieties and uniformity needed for mechanized harvest drive adoption. Local extension programs promote side-by-side trials that visibly de-risk premium seed purchases. Feed mills increasingly mandate hybrid grain in supply contracts, further pulling demand. The trend embodies agriculture’s broader shift from subsistence production to input-intensive commercial cultivation across the Asia-Pacific maize seed market.

Expansion of feed-grade corn demand from Southeast Asian poultry integrators

Thailand’s poultry industry consumes 8.0–8.5 million metric tons of corn annually, yet produces only 4.9 million metric tons, forcing imports and raising local grain prices. Charoen Pokphand Foods’ USD 2 billion expansion in the Philippines stipulates local corn sourcing with 14% moisture content, driving hybrid seed uptake.[1]Source: Philippine News Agency, “Thai Firm Set to Pour in Additional P1-B Investments,” pna.gov.ph Large integrators bypass intermediaries through direct farmer contracts, standardizing hybrid varieties and quality specifications. As urban meat consumption rises, feed mills in Vietnam and Indonesia replicate the model, sustaining hybrid demand in the Asia-Pacific maize seed market.

Roll-out of drought-tolerant maize hybrids via CIMMYT–public sector alliances

CIMMYT’s DroughtTEGO lines deliver 20–35% higher yields under water stress and now enter national trials in Bangladesh and Myanmar.[2]Source: CIMMYT, “TELA Maize Project Advancements,” cimmyt.org Public research institutes supply locally adapted parental lines while private firms scale multiplication and distribution. Governments fast-track approvals for stress-tolerant traits under climate-resilience programs, shortening commercialization timelines. The collaboration accelerates product pipelines for environments most vulnerable to erratic rainfall.

Precision-ag services bundling seed and drone-based variable-rate sowing

China operated 80,000 agricultural UAVs that covered 93.3 million hectares in 2024, enabling variable-rate seeding according to fertility maps.[3]Source: International Rice Research Institute, “IRRI-XAG Partnership on Drone-Based Sowing,” irri.org Partnerships such as IRRI and XAG package hybrid seed with drone services that optimize plant populations and lower labor costs. The service appeals to mid-size farms moving toward mechanization, generating recurring revenue for seed firms through annual service contracts. By aligning planting density to yield potential, farmers extract maximum value from hybrid genetics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented last-mile distribution in Myanmar, Laos, and Cambodia | -0.3% | Myanmar, Laos, Cambodia, and rural Indonesia | Medium term (2-4 years) |

| Slow biotech trait approval timelines in Indonesia and Thailand | -0.4% | Indonesia, Thailand, and Malaysia | Long term (≥ 4 years) |

| Rising counterfeit seed incidence despite QR-code tagging | -0.2% | India, Pakistan, Bangladesh, and Vietnam | Short term (≤ 2 years) |

| Climate-linked insurance gaps limiting hybrid adoption in rain-fed zones | -0.5% | India, Bangladesh, Pakistan, and Myanmar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising counterfeit seed incidence despite QR-code tagging

Counterfeit seed proliferation undermines farmer confidence and legitimate market growth despite industry efforts to implement authentication technologies including QR-code verification systems [counterfeit seed issues research]. Sophisticated counterfeiting operations replicate packaging and authentication features, making detection difficult for farmers and retailers without specialized equipment. The problem proves particularly acute in markets with weak intellectual property enforcement and limited penalties for seed counterfeiting.

Slow biotech trait approval timelines in Indonesia and Thailand

Indonesia’s multi-agency review process subjects each GM event to overlapping food, feed, and environmental assessments, extending approval to five years or longer. Thailand’s precautionary stance amid political debates keeps field trials limited. These lags prevent local farmers from accessing insect-resistant or herbicide-tolerant traits already commercialized in the Philippines and Vietnam, widening productivity gaps. Seed companies divert Research and Development budgets toward markets with clearer pathways, slowing trait innovation for these countries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Drive Value While Open-Pollinated Varieties Accelerate

Hybrids dominated the Asia-Pacific maize seed market with 90.62% revenue share in 2025, reflecting overwhelming farmer preference for higher yields and grain uniformity. Non-transgenic hybrids remain the mainstay because many countries retain cautious biotech policies, though the Philippines and Vietnam record robust transgenic penetration. Bayer’s short-stature and Preceon systems exemplify ongoing hybrid innovation aimed at mechanization efficiency and lodging resistance. The Asia-Pacific maize seed market size for hybrids is projected to rise modestly at a 2.32% CAGR, supported by contract farming and precision-ag bundling.

Open-pollinated varieties and hybrid derivatives secure the fastest 3.28% CAGR as they bridge affordability and performance for cash-constrained farmers. Seed reuse for up to two seasons lowers input costs while still delivering 10–15% yield gains over saved seed. Local firms position these seeds in smaller pack sizes and flexible credit schemes, capturing demand in Myanmar, Cambodia, and the upland regions of Vietnam. As rural purchasing power rises, this segment serves as a stepping-stone toward full hybrid adoption, ensuring diverse demand layers across the Asia-Pacific maize seed market.

Geography Analysis

China commanded 81.65% of the Asia-Pacific maize seed market share in 2025. China’s dominance reflects extensive public investment in seed innovation, strong domestic demand, and vertically integrated distribution that moves genetics from laboratory to village retail in one growing season. Yet the mature nature of its hybrid adoption caps incremental volume growth, gains come from trait premiums, digital farming services, and climate-resilient offerings. National carbon programs reward conservation tillage and high biomass hybrids, adding a new revenue layer for elite genetics providers.

Bangladesh delivers the fastest 6.55% CAGR, propelled by surging poultry feed demand and public-private breeding alliances that fast-track drought-tolerant hybrids. South Asia provides the next demand frontier. India’s MSP reforms and expanding mechanization support adoption among fragmented landholders, evidenced by a 435,000-hectare summer maize area increase in 2025. Pakistan’s differentiated MSP and fertilizer subsidies extend similar incentives. Both markets confront distribution complexity and counterfeit risks, but the rising feed and starch industries create compelling pull factors.

Southeast Asia represents a mosaic shaped by policy and industry structure. Vietnam’s 26.5% GM corn share showcases successful biotech integration. Thailand faces regulatory delays yet relies heavily on imports, pushing poultry integrators to champion local productivity gains. The Philippines remains regionally progressive on biotech approvals, while Indonesia balances food security goals with cautious trait governance. In Australia and Japan, high labor costs and sustainability regulations fuel investment in precision planting and carbon-efficient hybrids, creating premium niches within the broader Asia-Pacific maize seed market.

Competitive Landscape

The Asia-Pacific maize seed market remains fragmented, with the top five suppliers holding an estimated 29% combined share, leaving room for regional specialists to carve niches. Bayer AG holds a significant market share due to a broad hybrid portfolio, an advanced trait pipeline, and digital FarmRise services that integrate prescription planting with input management. Corteva Agriscience maintains a notable presence, focusing on drought-tolerant and low-input hybrids tailored to smallholders.

Local champions such as Advanta Seeds leverage deep distribution networks and smaller pack sizes to reach underserved villages, while Chinese firms like Beidahuang Kenfeng benefit from state support and proximity to vast corn belts. Strategic thrusts revolve around trait stacking for multiple stress tolerance, precision-ag service bundling that embeds seed within drone-sowing packages, and geographic expansion into emerging frontier markets.

Partnerships with public research bodies, exemplified by the IRRI and ICRISAT integrated seed systems vision, shorten breeding cycles and align products with evolving climate challenges. Sustainability credentials grow more salient as carbon markets reward hybrids that maximize biomass and input efficiency, giving firms new levers to differentiate offerings in the Asia-Pacific maize seed market.

Asia-Pacific Maize Seed Industry Leaders

Corteva Agriscience

Bayer AG

Syngenta Group

Advanta (UPL Ltd.)

Beidahuang Kenfeng Seed Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bayer AG introduced ten pipeline products, including Preceon smart corn and the CRW4 rootworm trait, which have potential for global expansion. These innovations are expected to impact maize seed offerings in the Asia-Pacific region.

- April 2025: The International Rice Research Institute (IRRI) and International Crops Research Institute for the Semi-Arid Tropics (ICRISAT) established a joint vision (2025-2027) to enhance integrated seed systems in South Asia. This initiative focuses on distributing drought-tolerant maize varieties to support climate-resilient maize cultivation in the Asia-Pacific region.

- November 2024: Best Agrolife Ltd received approval for two patented crop-protection products aimed at maize, with projected USD 140 million annual Asian revenue.

Asia-Pacific Maize Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Australia, Bangladesh, China, India, Indonesia, Japan, Myanmar, Pakistan, Philippines, Thailand, Vietnam are covered as segments by Country.Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Insect Resistant Hybrids | ||

| Other Traits | ||

| Open Pollinated Varieties & Hybrid Derivatives | ||

Country

| Australia |

| Bangladesh |

| China |

| India |

| Indonesia |

| Japan |

| Myanmar |

| Pakistan |

| Philippines |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Insect Resistant Hybrids | |||

| Other Traits | |||

| Open Pollinated Varieties & Hybrid Derivatives | |||

| Country | Australia | ||

| Bangladesh | |||

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Myanmar | |||

| Pakistan | |||

| Philippines | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms