Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

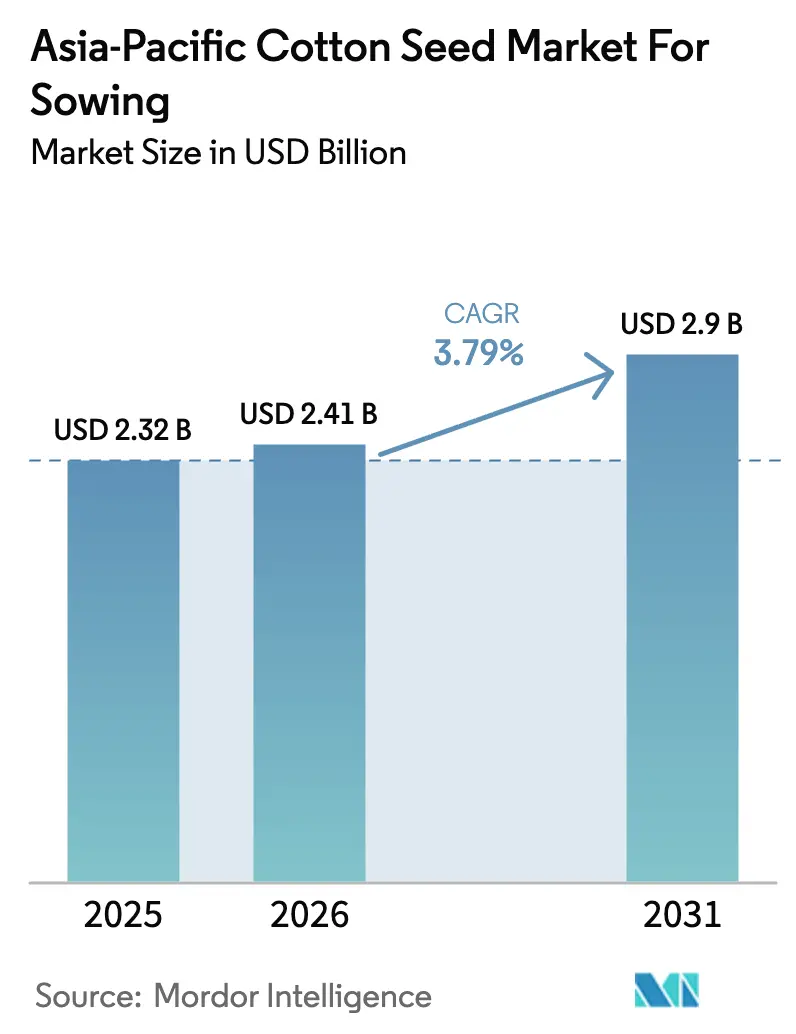

| Base Year Market Size (2025) | USD 2.32 Billion |

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 2.9 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Cotton Seed for Sowing Market Analysis by Mordor Intelligence

Asia-Pacific cotton seed market size for sowing market size in 2026 is estimated at USD 2.41 billion, growing from 2025 value of USD 2.32 billion with 2031 projections showing USD 2.9 billion, growing at 3.79% CAGR over 2026-2031. Strong demand from China’s ultra-high-density sowing systems, India’s hybrid adoption, and Australia’s premium export focus underpin this steady rise. The market benefits from rising uptake of trait-stacked hybrids that curb pesticide costs, government seed subsidies that lower initial outlays for smallholders, and textile industry expansion that rewards fiber quality. Digital seed commerce widens access in remote districts, while climate-smart certification schemes tie genetics to sustainability premiums. Climate adaptation pressures are reshaping variety preferences, with drought-tolerant and heat-resistant traits commanding 20-30% price premiums in water-stressed regions. The convergence of ESG (Environmental, Social, and Governance)-driven apparel sourcing and climate-smart agriculture creates new certification requirements that could restructure competitive advantages over the forecast period.

Key Report Takeaways

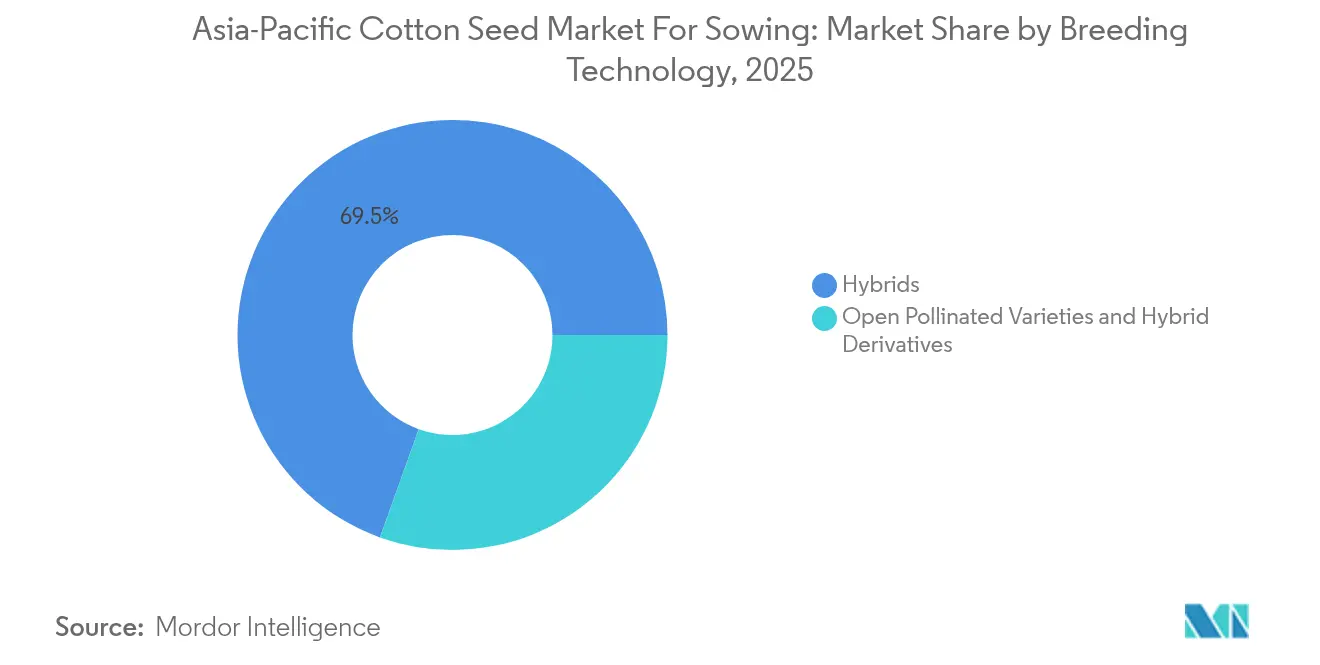

- By breeding technology, hybrids held 69.52% of the Asia-Pacific Cotton Seed for Sowing Market share in 2025, while Open-pollinated varieties and hybrid derivatives are projected to post a 4.04% CAGR through 2031.

- By geography, China commanded 52.86% of the Asia-Pacific Cotton Seed for Sowing Market size in 2025, while Australia is forecast to advance at the fastest 5.55% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Cotton Seed for Sowing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of Bt (Bacillus thuringiensis) and stacked-trait hybrids | +1.2% | The trend is most relevant in China, India, and Pakistan, with adoption expanding to Myanmar and Bangladesh. | Medium term (2-4 years) |

| Government seed subsidies and minimum-support pricing programs | +0.8% | India, Pakistan, Bangladesh primary, China selective support | Short term (≤ 2 years) |

| Rapid expansion of textile spinning capacity | +1.0% | Asia-Pacific core, spillover to cotton-producing regions | Long term (≥ 4 years) |

| Xinjiang’s shift to ultra-high-density sowing driving seed volume growth | +0.6% | The driver is most relevant in China, concentrated in Xinjiang province. | Medium term (2-4 years) |

| Surge in e-commerce seed sales platforms lowering channel costs for smallholders | +0.4% | India, China, and Indonesia are primary expanding across the Asia-Pacific | Short term (≤ 2 years) |

| Climate-smart seed certification schemes linked to ESG (Environmental, Social, and Governance)-driven apparel sourcing | +0.5% | Global, with early adoption in Australia, India, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Bt (Bacillus Thuringiensis) and Stacked-Trait Hybrids

Biotechnology adoption accelerates across Asia-Pacific as farmers confront evolving pest pressures and yield plateau challenges in conventional varieties. China's Ministry of Agriculture approved 12 new Bt (Bacillus Thuringiensis) cotton varieties in 2024, expanding the trait portfolio beyond single-gene Bollgard to stacked constructs combining herbicide tolerance and multiple insect resistance mechanisms [1]Source: China Ministry of Agriculture, “Seed Industry Regulations and Approvals 2024,” MOA, moa.gov.cn. India's experience with pink bollworm resistance to Cry1Ac has accelerated the adoption of dual-gene Bollgard II technology, with stacked-trait varieties now representing 78% of certified hybrid sales. The shift creates substantial revenue opportunities for trait developers and licensed seed companies, as stacked hybrids command 30-40% price premiums over conventional varieties. Regulatory compliance frameworks under OECD (Organization for Economic Co-operation and Development) guidelines ensure trait efficacy validation and resistance management protocols across participating countries.

Government Seed Subsidies and Minimum-Support Pricing Programs

Policy interventions increasingly target seed quality improvement as governments recognize the multiplier effects of genetic potential on agricultural productivity and rural incomes. India's National Food Security Mission allocated INR 3,400 crore (USD 408 million) for seed distribution programs in 2024, with 35% earmarked specifically for cotton seed subsidies in major producing states[2]Source: Ministry of Agriculture and Farmers Welfare, “National Food Security Mission Allocation 2024,” Government of India, agricoop.nic.in. Pakistan's Prime Minister Agriculture Emergency Program provides 50% subsidies on certified cotton seeds, driving adoption rates from 23% in 2022 to 41% in 2024 among smallholder farmers. Bangladesh's Cotton Development Board expanded its seed multiplication program to cover 85,000 hectares, targeting 60% certified seed adoption by 2026. These interventions create artificial demand floors that stabilize seed company revenues while accelerating technology diffusion. The programs particularly benefit companies with strong government relationships and distribution capabilities in rural markets.

Rapid Expansion of Textile Spinning Capacity

Downstream industrial demand fundamentally reshapes cotton seed requirements as spinning mills prioritize fiber quality attributes over traditional yield metrics. Vietnam's textile exports reached USD 44.2 billion in 2024, surpassing China as the largest ready-made garment supplier to the United States, driving cotton imports up 37.7% to 504,198 metric tons in the first four months of 2024. This industrial expansion creates derived demand for high-quality cotton varieties with superior fiber length, strength, and micronaire properties. China's spinning capacity additions of 2.8 million spindles in 2024 concentrate in Xinjiang and coastal provinces, requiring cotton varieties optimized for machine harvesting and processing efficiency. Bangladesh's textile sector recovery from 2023 disruptions drives renewed investment in spinning infrastructure, with 15 new mills commissioned in 2024, representing 450,000 additional spindles.

Xinjiang’s Shift to Ultra-High-Density Sowing Driving Seed Volume Growth

Agricultural mechanization in China's primary cotton region transforms seed consumption patterns through precision planting technologies that optimize plant populations for machine harvesting. The technology requires specialized seed varieties with compact plant architecture and synchronized boll opening, creating opportunities for breeding companies with appropriate germplasm. Seed consumption per hectare increases from 15-18 kg to 28-32 kg under ultra-high-density systems, representing substantial volume growth independent of area expansion. The practice is expanding beyond Xinjiang to other mechanized cotton regions in China and Australia, where labor costs favor capital-intensive production systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile farm-gate cotton prices discouraging seed purchase | -0.9% | Global with an acute impact in India, Pakistan, and Australia | Short term (≤ 2 years) |

| Stringent biotech regulations | -0.6% | Japan, Indonesia, and Thailand are the primary markets affected, with spillover to other Asian countries. | Long term (≥ 4 years) |

| Counterfeit seed proliferation through informal cross-border trade | -0.5% | South Asia and Southeast Asia corridors | Medium term (2-4 years) |

| Water-allocation caps in Australia limiting seed-based area expansion | -0.3% | Australian national, concentrated in the Murray-Darling Basin | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Farm-Gate Cotton Prices Discouraging Seed Purchase

Price volatility fundamentally undermines farmer investment decisions in premium seed technologies, as uncertain returns discourage upfront expenditures on higher-cost genetic materials. Cotton futures on the Intercontinental Exchange fluctuated between 68-89 cents per pound during 2024, creating 31% price volatility that exceeded historical averages and complicated planting decisions for the 2025 season[3]Source: Intercontinental Exchange, “Cotton Futures Price Data 2024,” ICE, theice.com Source: Japan Biosafety Clearing House, “GM Crop Approval Process Guidelines,” BCH Japan, biodic.go.jp . This uncertainty particularly impacts smallholder farmers who lack hedging mechanisms and rely on spot market prices for revenue planning. Indian cotton prices declined 18% between March and August 2024 due to global supply adjustments, causing many farmers to defer premium seed purchases in favor of saved seeds or lower-cost alternatives. The volatility creates cyclical demand patterns that complicate seed company production planning and inventory management.

Stringent Biotech Regulations

Regulatory frameworks in key Asian markets create approval bottlenecks that delay trait commercialization and limit seed company investment returns on biotechnology development. Japan's biosafety assessment process requires 3-5 years for new trait approvals, with additional requirements for environmental impact studies that extend timelines beyond commercial viability windows. Indonesia's moratorium on new GM crop approvals, maintained since 2021, effectively blocks trait-based innovation despite growing pest pressure and yield stagnation in conventional varieties. Thailand's National Biosafety Committee approved only 2 new cotton traits in the past 5 years, compared to 15 approvals in India during the same period. These regulatory constraints force seed companies to maintain parallel breeding programs for GM (Genetically Modified) and non-GM (Genetically Modified) markets, increasing development costs while limiting revenue potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Trait Integration Drives Premium Positioning

Hybrids maintain their commanding 69.52% market share in 2025, reflecting superior agronomic performance and integrated pest management capabilities that justify premium pricing structures across diverse farming systems. The segment's growth trajectory benefits from continuous trait stacking innovations, with companies like Bayer introducing triple-stacked varieties combining Bollgard 3, Roundup Ready Flex, and ThryvOn technologies that deliver 22-28% yield advantages over conventional alternatives in 2023. Transgenic hybrids within this category represent the fastest-growing subsegment, driven by regulatory approvals for new trait combinations and farmer adoption of integrated weed management systems. Non-transgenic hybrids maintain relevance in markets with biotech restrictions, particularly Japan and Indonesia, where conventional breeding achievements in fiber quality and disease resistance support premium positioning.

Open Pollinated Varieties and Hybrid Derivatives project the strongest growth at 4.04% CAGR through 2031, concentrated primarily in Australia, where water-efficient varieties command premium prices amid irrigation constraints. This segment benefits from farmer cost management strategies and seed-saving practices that reduce per-hectare input expenses while maintaining acceptable yield levels. The growth reflects increasing sophistication in conventional breeding programs that incorporate molecular marker technologies and genomic selection methods to accelerate variety development.

Geography Analysis

China's dominant 52.86% market share in 2025 reflects the country's position as both the world's largest cotton producer and most advanced adopter of mechanized production systems that require specialized seed varieties. The market's evolution toward ultra-high-density sowing systems, particularly in Xinjiang province, creates substantial volume growth opportunities as per-hectare seed requirements double from traditional planting densities . Chinese seed companies like Longping High-Tech Agriculture leverage government research partnerships and extensive distribution networks to maintain competitive positioning against multinational trait developers. India represents the second-largest market, where hybrid adoption accelerates through government subsidy programs and increasing pest pressure that favors biotechnology solutions.

Australia emerges as the fastest-growing country market at 5.55% CAGR, driven by premium export demand and advanced breeding programs focused on water-efficient varieties that address irrigation constraints in the Murray-Darling Basin. The country's sophisticated agricultural extension systems and high technology adoption rates create favorable conditions for premium seed varieties that justify higher input costs through superior fiber quality and processing efficiency.

Bangladesh and Vietnam represent emerging growth markets where textile industry expansion drives demand for consistent fiber quality that requires certified seed varieties rather than farmer-saved alternatives. Pakistan's market growth depends heavily on government policy support and water availability, while smaller markets like Myanmar and the Philippines offer long-term potential as agricultural modernization accelerates. Regulatory compliance frameworks under OECD (Organisation for Economic Co-operation and Development) guidelines ensure consistent quality standards across participating countries while facilitating trade in certified genetic materials.

Competitive Landscape

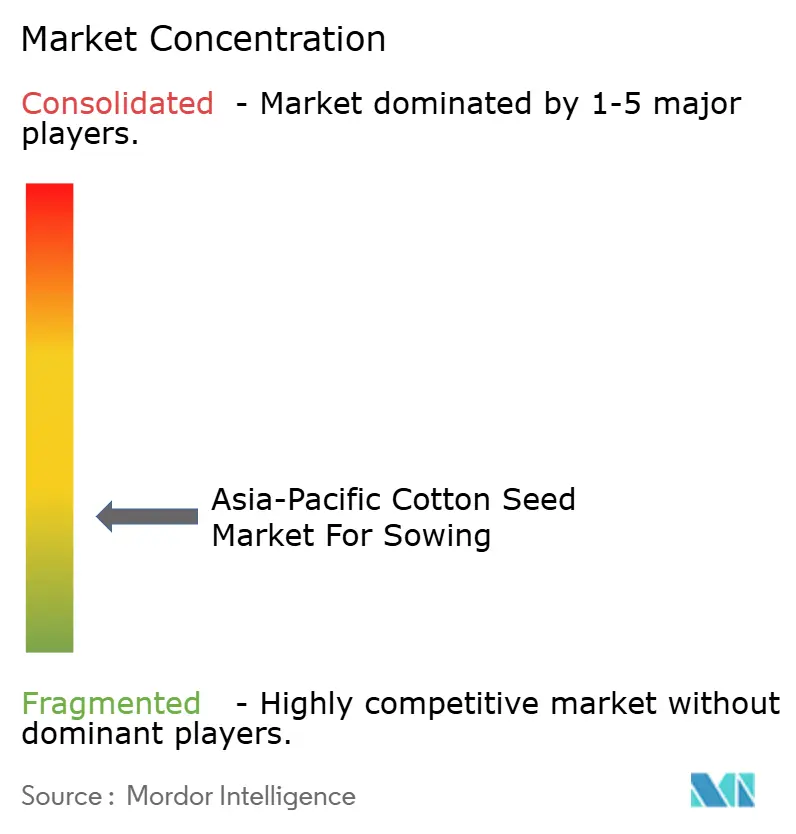

The Asia-Pacific Cotton Seed for Sowing Market exhibits a fragmented structure with a mix of global agrochemical conglomerates and regional seed specialists. Local companies within domestic markets hold significant market shares due to their deep understanding of regional agricultural conditions and established relationships with farmers. Companies like Anhui Tsuen Yin Hi-Tech Seed Industry Co. Ltd, Kaveri Seeds, Krishak Bharati Co-Op Limited (KRIBHCO), Maharashtra Hybrid Seeds Co. (Mahyco), and Bayer AG have a strong regional presence through extensive dealer networks and localized breeding programs. The market has witnessed limited consolidation activity, with companies preferring organic growth through capacity expansion and product development rather than acquisitions.

The competitive dynamics are characterized by the presence of both public and private sector players, with government-affiliated organizations playing a crucial role in seed development and distribution in countries like India and China. Global players like Bayer AG operate through subsidiaries and joint ventures to maintain their market position, while regional players leverage their local expertise and cost advantages. The industry structure promotes healthy competition and innovation, with companies focusing on developing region-specific seed varieties adapted to local growing conditions and pest challenges.

Success in the cotton seed market increasingly depends on companies' ability to develop innovative seed varieties that address specific regional challenges while maintaining cost competitiveness. Incumbent players must focus on strengthening their research capabilities, particularly in biotechnology and genetic improvement, while expanding their distribution reach through strategic partnerships with agricultural input dealers and cooperatives. Companies need to invest in farmer education programs and demonstration farms to build brand loyalty and showcase the benefits of their seed varieties. The development of drought-tolerant and disease-resistant varieties will become crucial as climate change impacts cotton cultivation.

Asia-Pacific Cotton Seed for Sowing Industry Leaders

Anhui Tsuen Yin Hi-Tech Seed Industry Co. Ltd

Kaveri Seeds

Krishak Bharati Co-Op Limited (KRIBHCO)

Maharashtra Hybrid Seeds Co. (Mahyco)

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BASF introduced new FiberMax and Stoneville cotton seed varieties, expanding their portfolio to 13 varieties. The new varieties feature Axant Flex herbicide tolerance technology, the first quad-stacked herbicide trait in cotton, along with three-gene insect control through the TwinLink Plus trait.

- August 2024: The Philippines’ Bureau of Plant Industry approved commercial propagation of Bt (Bacillus thuringiensis) cotton for saw field testing, extension activity, and early adoption reports as Bt cotton varieties moved into farmer use.

- June 2024: Syngenta Group established a joint venture with Longping High-Tech Agriculture to develop next-generation cotton varieties for the Chinese market, combining Syngenta's trait technologies with Longping's local breeding expertise and distribution networks.

Asia-Pacific Cotton Seed for Sowing Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Australia, Bangladesh, China, India, Indonesia, Japan, Myanmar, Pakistan, Philippines, Thailand, Vietnam are covered as segments by Country.Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Insect Resistant Hybrids | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

Geography

| Australia |

| Bangladesh |

| China |

| India |

| Indonesia |

| Japan |

| Myanmar |

| Pakistan |

| Philippines |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Insect Resistant Hybrids | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Geography | Australia | ||

| Bangladesh | |||

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Myanmar | |||

| Pakistan | |||

| Philippines | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms