Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.1 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Vegetable Seeds Market Analysis by Mordor Intelligence

The China vegetable seeds market size was valued at USD 1.05 billion in 2025 and estimated to grow from USD 1.1 billion in 2026 to reach USD 1.38 billion by 2031, at a CAGR of 4.64% during the forecast period (2026-2031). This sustained advance stems from Beijing’s push for agricultural self-reliance, accelerated regulatory approval for gene-edited crops, and rapid gains in protected cultivation acreage. Steady investments in domestic breeding centers, the rollout of e-commerce seed channels, and rising Gen-Z demand for diverse vegetables reinforce both volume and value growth in the China vegetable seeds market. Competition remains fragmented, with the top five suppliers jointly holding less share of the China vegetable seeds market in 2024, creating room for consolidation, specialty crop focus, and technology-driven differentiation. Opportunities center on hybrids tailored for automated greenhouse systems, counterfeit-proof distribution models, and varieties optimized for climate resilience.

Key Report Takeaways

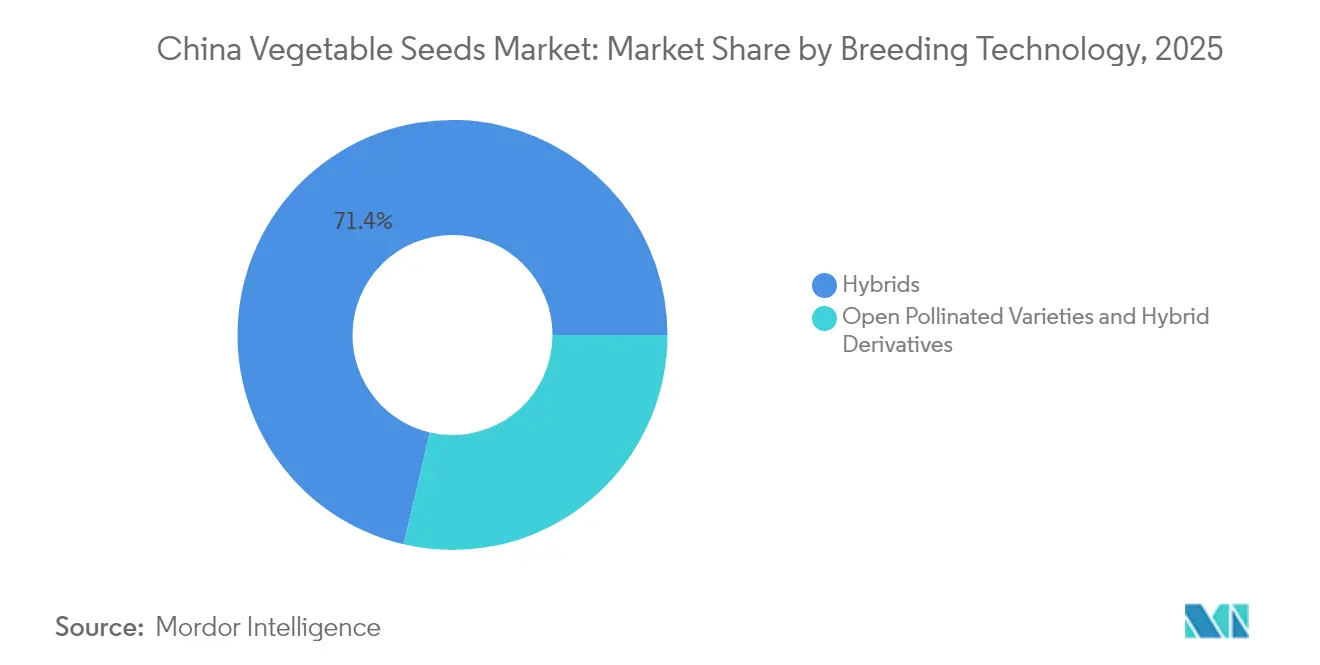

- By breeding technology, hybrids captured 71.35% revenue share of the China vegetable seeds market in 2025, while the segment is advancing at a 4.72% CAGR through 2031.

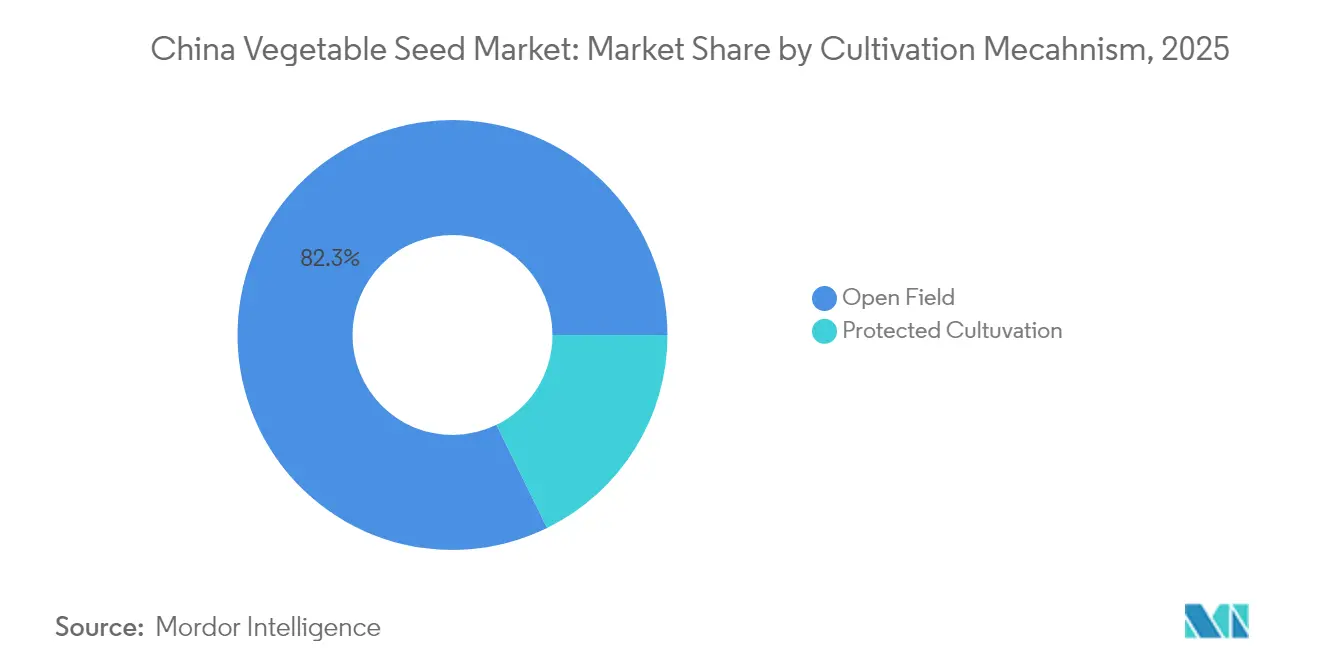

- By cultivation mechanism, Open Field cultivation accounted for 82.25% of the China vegetable seeds market size in 2025, while protected cultivation is growing at a 6.98% CAGR to 2031.

- By crop family, Solanaceae led with 35.05% of China vegetable seeds market share in 2025, while unclassified vegetables are forecast to post a 5.55% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Vegetable Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government push for seed industry self-reliance | +1.2% | National, with focus on Hainan and Gansu breeding hubs | Long term (≥ 4 years) |

| Rapid adoption of protected cultivation | +0.9% | Yangtze River Delta, expanding to Pearl River Delta | Medium term (2-4 years) |

| Expansion of e-commerce seed channels | +0.6% | Nationwide and higher use in tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Vegetable diet diversification by Gen-Z | +0.5% | Major urban centers such as Beijing, Shanghai, and Shenzhen | Medium term (2-4 years) |

| Growth of contract farming for exports | +0.7% | Shandong, Hebei, and Fujian | Medium term (2-4 years) |

| Advances in CRISPR-Cas breeding | +0.8% | National and concentrated in leading research institutes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Push for Seed Industry Self-Reliance

Beijing earmarked RMB 2.4 billion (USD 336 million) in 2024 to upgrade biological breeding capacity, channeling funds to vegetable research programs.[1]Source: State Council Information Office, “Central Document No. 1 Implementation Guidelines,” scio.gov.cnPreferential tax treatment for firms whose varieties contain at least 80% domestic genetics shortens payback on R&D. Nanfan, branded as China’s “Seed Silicon Valley,” enables two to three breeding cycles per year, cutting product development timelines by one-third while supporting localized germplasm banks that protect intellectual property. Accelerated review pathways now trim 12–18 months off domestic variety approvals, keeping the China vegetable seeds market responsive to shifting consumer and climatic demands.[2]Source: Ministry of Agriculture and Rural Affairs, “Gene-Edited Crop Variety Approval Announcement,” moa.gov.cn

Rapid Adoption of Protected Cultivation in the Yangtze River Delta

Jiangsu alone added 150,000 hectares of greenhouse space in 2024, a 23% jump over 2023, with integrated IoT nodes tracking moisture, temperature, and nutrients.[3]Source: Jiangsu Agricultural Technology Extension Center, “Protected Cultivation Development Report 2024,” jsagri.gov.cn Yield gains of 35-50% and crop loss reductions near 70% make premium hybrid seeds economically attractive despite higher upfront costs. Greenhouse produce trades at 40-60% price premiums versus open-field equivalents, justifying specialized seed lines engineered for uniform growth under LED lighting and hydroponic systems. These conditions steadily lift the China vegetable seeds market as protected cultivation spreads across affluent coastal provinces.

Expansion of E-Commerce Seed Channels

Seed sales through digital platforms rose 45% year-over-year in 2024, positioning online marketplaces as the fastest-growing distribution route. Embedded QR codes let growers verify authenticity directly with breeders, curbing counterfeit circulation that previously caused farm losses of RMB 1.2 billion (USD 168 million) annually. The platform model enables seed companies to gather real-time market intelligence on variety performance and farmer preferences, accelerating breeding program responsiveness to market demands. Direct-to-farm shipping trims transaction costs 15-20%, making higher-value hybrids more accessible and enlarging the addressable base for the China vegetable seeds market.

Vegetable Diet Diversification Among Gen-Z Consumers

Urban residents aged 18-35 lifted vegetable intake 28% between 2022 and 2024, favoring novel colors, flavors, and functional nutrition. Demand for purple carrots, rainbow chard, and antioxidant-rich peppers spurs breeders to create visually striking, nutrient-dense varieties. The trend toward "Instagram-worthy" food presentation drives demand for visually distinctive varieties, enabling seed companies to differentiate products based on aesthetic characteristics rather than solely on yield or disease resistance. Health-conscious consumers increasingly seek vegetables with enhanced antioxidant content, creating opportunities for biofortified varieties developed through conventional breeding or gene editing techniques.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit seed circulation | -1.3% | Tier-3 and tier-4 cities | Short term (≤ 2 years) |

| Climate-induced disease outbreaks | -1.1% | National and higher risk in southern provinces | Medium term (2-4 years) |

| Regulatory delays for gene-edited hybrids | -0.8% | Nationwide | Medium term (2-4 years) |

| Farm-level labor shortages | -0.9% | Rural regions, especially central provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Seed Circulation in Tier-3 Cities

Law enforcement tallied more than 200 counterfeit seed cases in 2024, with individual growers losing RMB 20,000 (USD 2,800) to RMB 45,000 (USD 6,300) per incident. Qualification-renting business models enable unscrupulous operators to use legitimate companies' licenses for illegal seed production, complicating enforcement efforts and regulatory oversight. Rural distribution networks often lack proper storage facilities and cold chain infrastructure, leading to seed quality degradation that farmers may attribute to variety performance rather than handling issues. The problem disproportionately affects vegetable seeds due to higher unit values and complex breeding characteristics that are difficult for farmers to verify before planting.

Climate-Induced Disease Outbreaks

Unpredictable rainfall and temperature swings in 2024 fueled downy mildew and bacterial wilt epidemics, slashing yields and boosting vegetable prices by 40%. Pathogens evolve faster under climate stress, eroding resistance genes. Climate change accelerates pathogen evolution and migration patterns, rendering existing resistance genes ineffective and requiring constant breeding program updates to maintain variety performance. The economic impact extends beyond direct crop losses to include increased pesticide applications, reduced marketable yields, and consumer concerns about food safety and quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Extend Lead as R&D Accelerates

Advanced breeding techniques position hybrid varieties as the dominant force in China's vegetable seed market, capturing 71.35% market share in 2025 while maintaining the strongest growth momentum at 4.72% CAGR through 2031. The segment's leadership stems from superior yield consistency, disease resistance, and uniformity characteristics that justify premium pricing for commercial growers seeking predictable returns on investment. CRISPR-Cas gene editing applications accelerate hybrid development timelines, with Chinese research institutions successfully modifying tomato varieties for enhanced lycopene content and broccoli cultivars with improved heat tolerance. Open pollinated varieties and hybrid derivatives occupy the remaining 28.65% market share, serving price-sensitive farmers and organic production systems that prohibit hybrid technology use.

The technology gap between hybrid and open-pollinated varieties continues widening as breeding companies concentrate R&D investments in proprietary genetics that generate recurring revenue streams through annual seed purchases. Hybrid varieties demonstrate 25-40% yield advantages over open-pollinated alternatives in controlled trials, with particularly strong performance under stress conditions including drought, disease pressure, and suboptimal growing environments. Small-scale farmers increasingly adopt hybrid seeds despite higher upfront costs due to improved crop reliability and reduced risk of total crop failure. The regulatory approval of gene-edited varieties in December 2024 creates additional differentiation opportunities for hybrid developers while open-pollinated varieties remain limited to conventional breeding improvements.

By Cultivation Mechanism: Protected Systems Propel Premium Seed Demand

Open-field cultivation maintains largest market share of 82.25% in 2025 through cost advantages and suitability for commodity vegetable production, though growth rates lag at 4.08% CAGR as farmers face increasing pressure from weather variability and labor constraints. Protected systems command 40-60% price premiums for their produce, justifying higher seed costs and enabling farmers to invest in premium varieties with enhanced characteristics. Climate change impacts drive additional adoption of protected cultivation as insurance against extreme weather events that can destroy entire open-field crops. The technology integration includes automated seeding, transplanting, and harvesting equipment that requires uniform seed germination and plant characteristics, favoring hybrid varieties over traditional open-pollinated seeds.

Protected cultivation emerges as the fastest-growing segment at 6.98% CAGR through 2031 despite representing only 17.75% market share in 2025, reflecting the economics of intensive production systems that optimize land utilization and extend growing seasons. Greenhouse and tunnel systems enable year-round vegetable production with 2-3 crop cycles annually compared to single harvests in open-field systems, creating demand for specialized seed varieties adapted to controlled environments. The Yangtze River Delta region leads protected cultivation adoption with over 400,000 hectares under cover, utilizing IoT sensors, automated irrigation, and climate control systems that require seeds optimized for artificial growing conditions.

By Crop Family: Solanaceae Maintains Command While Diversity Rises

Solanaceae varieties, dominated by tomato production, maintain market leadership with 35.05% share in 2025, benefiting from strong domestic consumption and export demand for processed products. Tomato breeding programs focus on developing varieties with extended shelf life, enhanced processing characteristics, and resistance to emerging viral diseases that threaten production stability. Chinese consumers' preference for fresh tomatoes in cooking applications supports continued demand growth, while food processing companies require specific varieties with high solids content and uniform ripening characteristics for sauce and paste production. Chili and eggplant varieties within the Solanaceae family serve specialized market segments with distinct flavor profiles and culinary applications that resist substitution by other crop families.

Unclassified vegetables represent the fastest-growing segment at 5.55% CAGR through 2031, driven by consumer diversification toward specialty crops including asparagus, lettuce, and exotic leafy greens that command premium pricing in urban markets. This category benefits from Gen-Z dietary preferences for plant-based nutrition and visually appealing ingredients that enhance social media food presentation. Brassicas, Cucurbits, and Roots and Bulbs maintain stable market positions with growth rates aligned to overall market expansion, serving established consumption patterns and traditional cooking methods. The Ministry of Agriculture and Rural Affairs promotes crop diversification through technical support programs that encourage farmers to experiment with non-traditional varieties, supporting the growth of unclassified vegetable segments.

Geography Analysis

Regional specialization shapes the China vegetable seeds market. The Yangtze River Delta supplies over 35% of the national greenhouse capacity, driving advanced seed uptake for controlled environments. Shandong Province delivers 28% of total seed output, benefiting from legacy breeding centers and export-oriented logistic corridors.

Southern provinces, Guangdong, Fujian, and Hainan leverage tropical climates for year-round multiplication. Hainan’s Nanfan hub alone enables two to three breeding cycles annually, speeding product turnover. Northern belts such as Hebei and Henan prioritize large-scale mechanized production, selecting varieties compatible with automated harvesters.

Western regions remain nascent but receive infrastructure upgrades that will gradually stimulate seed demand as cold-chain access improves. Climate risk distribution also varies: typhoons pressure the south, while northern zones gain extended seasons, reshaping the trait priorities breeders pursue across the China vegetable seeds market.

Competitive Landscape

The China vegetable seeds market exhibits fragmentation with the top 5 companies controlling limited combined market share, creating opportunities for both consolidation and niche specialization strategies. Market concentration remains limited due to diverse crop requirements, regional preferences, and the technical complexity of developing varieties adapted to China's varied climatic conditions. International players like Syngenta Group leverage global breeding expertise and established distribution networks to maintain market leadership, while domestic companies capitalize on local market knowledge and government support for indigenous seed development.

The competitive dynamic increasingly favors companies with integrated breeding programs that combine conventional techniques with biotechnology applications, particularly CRISPR gene editing capabilities that accelerate variety development. Technology adoption serves as the primary differentiation factor, with leading companies investing heavily in digital agriculture platforms, precision breeding techniques, and data analytics capabilities that enhance farmer relationships and market responsiveness. Beijing Dabeinong Technology's approval for gene-edited varieties in December 2024 demonstrates how regulatory compliance capabilities create competitive advantages in biotechnology applications Ministry of Agriculture and Rural Affairs.

White-space opportunities exist in specialty crop segments where consumer preferences drive demand for unique varieties that command premium pricing, including heritage tomatoes, exotic peppers, and nutritionally enhanced vegetables. Emerging disruptors focus on direct-to-farmer sales models through e-commerce platforms that bypass traditional distributor networks and provide better margins for both seed companies and growers. The Ministry of Agriculture and Rural Affairs' seed industry development policies favor companies demonstrating technological innovation and domestic breeding capabilities, influencing competitive positioning and market access opportunities.

China Vegetable Seeds Industry Leaders

Syngenta Group

Hefei Fengle Seed Industry

Yuan Longping High-Tech Agriculture (CITIC Agri Fund)

Groupe Limagrain

Takii & Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mitsui & Co. acquired a 34% interest in Tianjin Derit Seeds, a Chinese company that breeds and sells hybrid vegetable seeds. This investment aligns with Mitsui's expansion in the Asian agricultural input market and reinforces its international seed business strategy.

- March 2025: The International Seed Federation (ISF) at the 2025 China Seed Congress focused on strengthening partnerships with Chinese stakeholders in plant breeding innovation, seed technology, and germplasm exchange. The congress demonstrated China's commitment to enhancing its domestic seed industry, including the vegetable segment, through international cooperation and regulatory harmonization.

- February 2024: Shouguang, known as China's "vegetable capital," is strengthening its domestic vegetable seed breeding programs to decrease dependence on imported varieties. The region currently produces more than 260 vegetable varieties and distributes seeds to over 20 Chinese provinces.

China Vegetable Seeds Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Open Field, Protected Cultivation are covered as segments by Cultivation Mechanism. Brassicas, Cucurbits, Roots & Bulbs, Solanaceae, Unclassified Vegetables are covered as segments by Crop Family.Breeding Technology

| Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

Cultivation Mechanism

| Open Field |

| Protected Cultivation |

Crop Family

| Brassicas | Cabbage |

| Carrot | |

| Cauliflower and Broccoli | |

| Other Brassicas | |

| Cucurbits | Cucumber and Gherkin |

| Pumpkin and Squash | |

| Other Cucurbits | |

| Roots and Bulbs | Garlic |

| Onion | |

| Potato | |

| Other Roots and Bulbs | |

| Solanaceae | Chilli |

| Eggplant | |

| Tomato | |

| Other Solanaceae | |

| Unclassified Vegetables | Asparagus |

| Lettuce | |

| Peas | |

| Spinach | |

| Other Unclassified Vegetables |

| Breeding Technology | Hybrids | |

| Open Pollinated Varieties and Hybrid Derivatives | ||

| Cultivation Mechanism | Open Field | |

| Protected Cultivation | ||

| Crop Family | Brassicas | Cabbage |

| Carrot | ||

| Cauliflower and Broccoli | ||

| Other Brassicas | ||

| Cucurbits | Cucumber and Gherkin | |

| Pumpkin and Squash | ||

| Other Cucurbits | ||

| Roots and Bulbs | Garlic | |

| Onion | ||

| Potato | ||

| Other Roots and Bulbs | ||

| Solanaceae | Chilli | |

| Eggplant | ||

| Tomato | ||

| Other Solanaceae | ||

| Unclassified Vegetables | Asparagus | |

| Lettuce | ||

| Peas | ||

| Spinach | ||

| Other Unclassified Vegetables | ||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms