Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

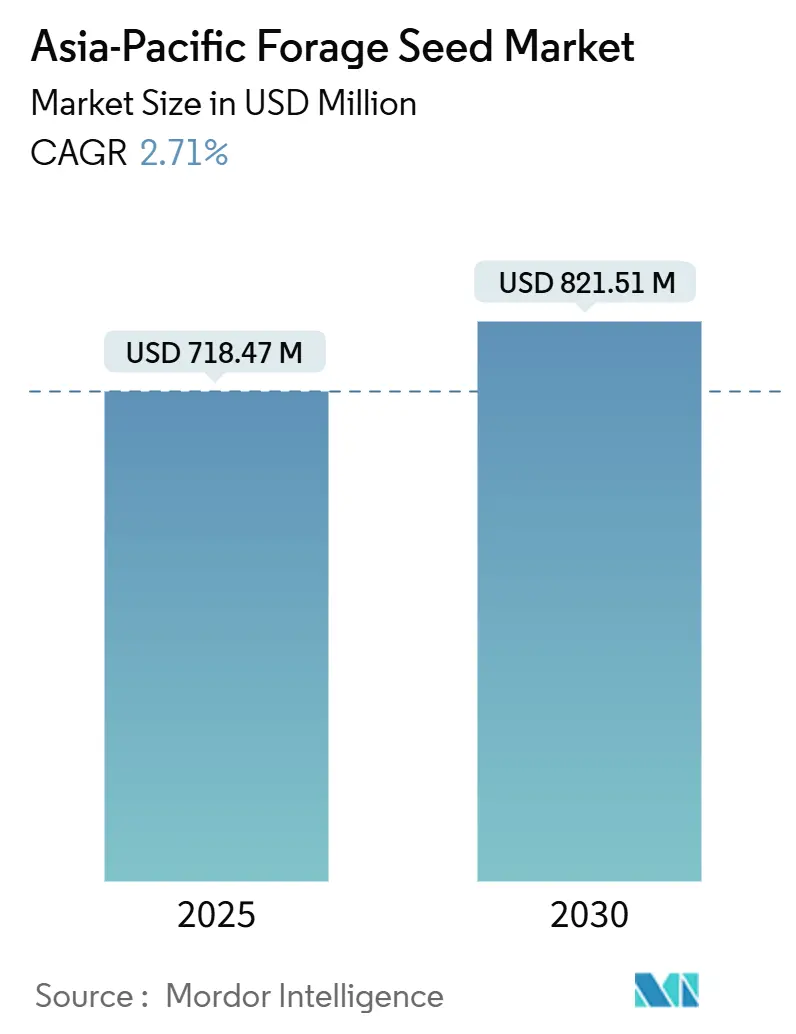

| Market Size (2025) | USD 718.47 Million |

| Market Size (2030) | USD 821.51 Million |

| Growth Rate (2025 - 2030) | 2.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Forage Seed Market Analysis by Mordor Intelligence

The Asia-Pacific forage seed market size stood at USD 718.47 million in 2025 and is forecast to reach USD 821.51 million by 2030, advancing at a 2.71% CAGR. Growth reflects the region’s pivot from grain‐based to forage‐based feeding systems as livestock producers pursue higher milk and meat yields and governments embed fodder security in agricultural policy. Japan’s premium dairy industry and Australia’s technology-oriented seed sector continue to favor certified hybrids, while emerging markets across Southeast Asia accelerate demand for drought-tolerant sorghum and mixed-legume pastures. Carbon-sequestration programs tied to corporate net-zero commitments and expanding e-commerce channels for ag-inputs further stimulate seed adoption, even as weather volatility and counterfeit trade temper expansion[1]Source: Statistics Bureau of Japan, “Official Statistics,” stat.go.jp.

Key Report Takeaways

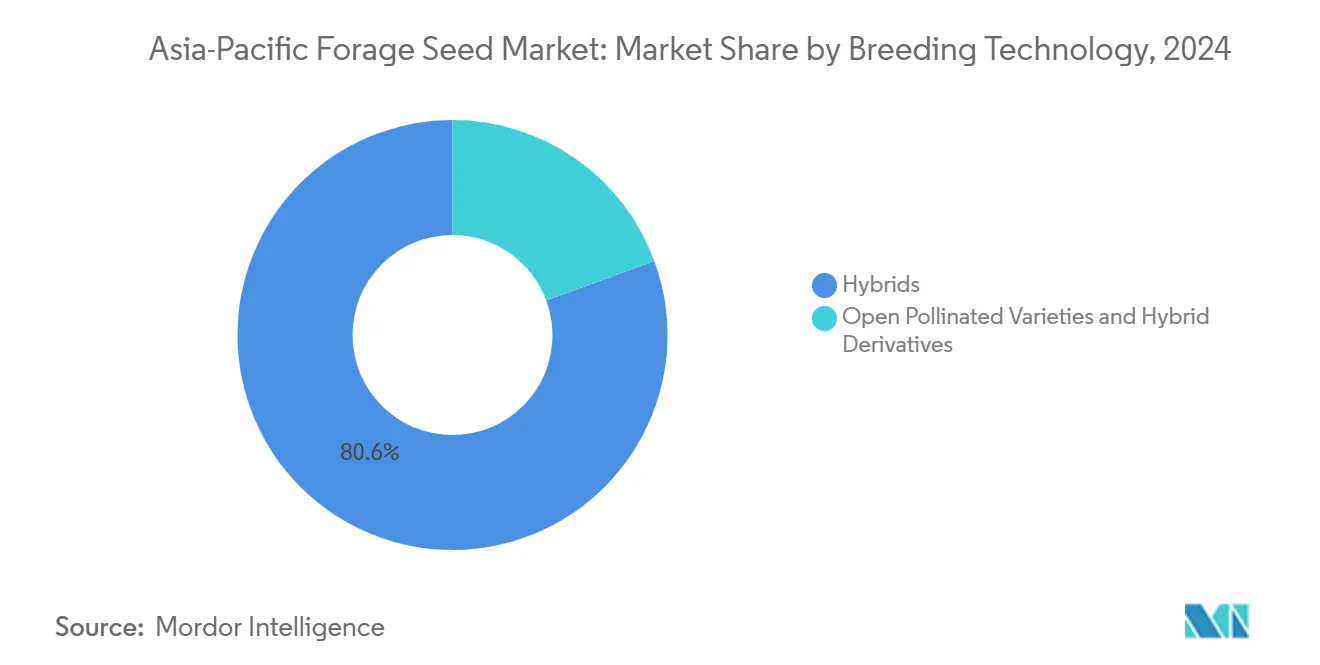

- By breeding technology, hybrids led with 80.60% of the Asia-Pacific forage seed market share in 2024, and are forecast to expand at a 2.77% CAGR through 2030.

- By crop, alfalfa accounted for a 24.90% share of the Asia-Pacific forage seed market size in 2024, while forage sorghum is advancing at a 3.67% CAGR to 2030.

- By geography, Japan held 48.40% revenue share in 2024, while the Philippines records the fastest projected CAGR at 4.62% through 2030.

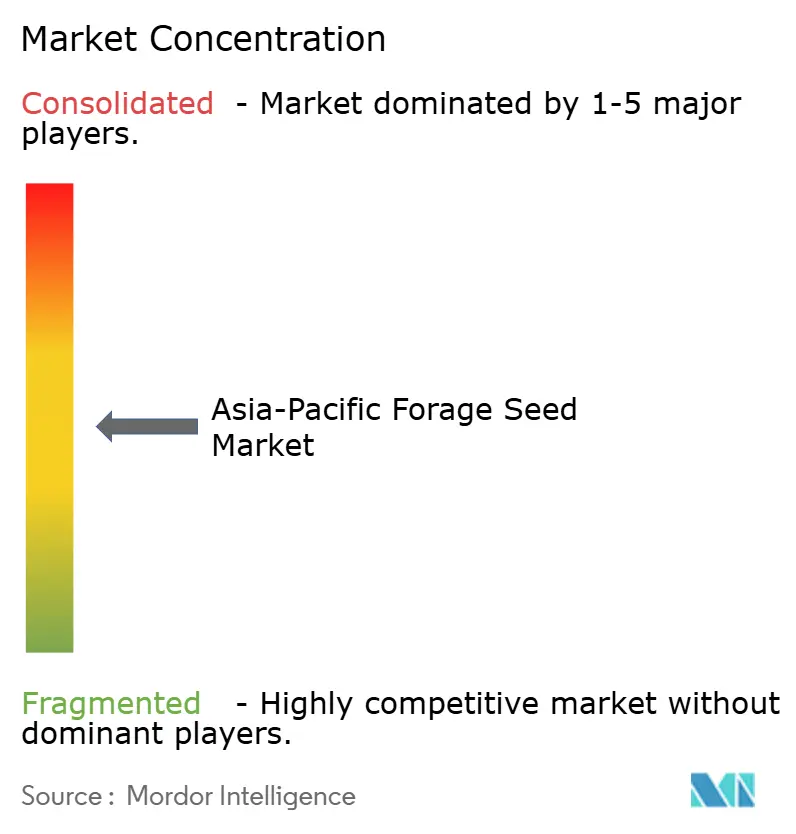

- Advanta Seeds, DLF, Bayer AG, Land O’Lakes Inc., and Royal Barenbrug Group collectively controlled 59% of 2024 revenue in the Asia-Pacific forage seed market.

Asia-Pacific Forage Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding dairy and meat demand in China and India | +0.8% | China, India, and spillover to Southeast Asia | Medium term (2–4 years) |

| Government fodder-security subsidies (India’s National Food Security Mission for Fodder) | +0.6% | India, China, and Thailand | Long term (≥ 4 years) |

| Shift to hybrid seeds for higher dry-matter yield | +0.5% | Australia, Japan, and South Korea | Short term (≤ 2 years) |

| Corporate net-zero targets lifting demand for carbon-sequestering legumes | +0.4% | Developed Asia-Pacific markets | Long term (≥ 4 years) |

| Rapid growth of climate-smart “dry-season” forage programs | +0.3% | Southeast Asia, northern Australia | Medium term (2–4 years) |

| E-commerce ag-input platforms unlocking last-mile seed access | +0.2% | India, China, and Indonesia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Dairy and Meat Demand in China and India

China’s per-capita dairy consumption rose to 42.3 kg in 2024, while India’s livestock sector generated USD 69.7 billion, elevating demand for high-quality forage[2]Source: National Bureau of Statistics of China, “Official Statistics,” stats.gov.cn. Feedlots and integrated dairy companies report 15–20% milk-yield improvements when shifting from straw to quality forage. Consolidating processors such as Modern Dairy and Heritage Foods now contracts acreage dedicated to certified seed varieties, ensuring a stable offtake for seed producers. These structural feed changes ripple into input markets, spurring consistent orders rather than sporadic purchases.

Government Fodder-Security Subsidies Drive Systematic Market Expansion

India’s National Food Security Mission-Fodder (NFSM-Fodder) allocated INR 10 billion (USD 120 million) in 2024–25 to enlarge forage acreage by 2.5 million hectares[3]Source: Ministry of Agriculture and Farmers Welfare, “Programmes, Schemes and Guidelines,” agricoop.nic.in. China’s mandate to replace 20% of feed grain with forage crops by 2025 reinforces region-wide momentum. Thailand mirrors this approach with 50% seed subsidies that lower growers’ upfront costs. Program design increasingly includes seed-multiplication grants and farmer training, stabilizing year-on-year demand for certified varieties. By embedding forage crops into national food-security strategies, policymakers transform episodic markets into institutionalized demand centers for the Asia-Pacific forage seed market.

Shift to Hybrid Seeds for Higher Dry-Matter Yield

Hybrid forage varieties yield 25–35% more dry matter than open-pollinated counterparts, motivating large dairy operations to pay premium prices. Bayer and Corteva funnel USD 50 million annually into Asia-Pacific breeding pipelines that exploit genomic selection to cut the varietal cycle in half. Australian research partnerships through the Grains Research and Development Corporation test drought-tolerant sorghum hybrids that retain 90% yield under water stress. Early adopters in Japan and South Korea confirm shorter growing windows and uniform forage quality, strengthening the business case. Hybrid penetration, therefore, remains a critical lever elevating the Asia-Pacific forage seed market.

Corporate Net-Zero Targets Lifting Demand for Carbon-Sequestering Legumes

Global agribusiness firms commit USD 260 billion annually toward climate-aligned sourcing. Legume-rich pastures sequester 0.5–2.0 metric tons of carbon per hectare per year, qualifying livestock suppliers for carbon credits priced at USD 15–30 per metric ton of CO₂-equivalent. Certified seed suppliers now bundle agronomy services and monitoring tools to verify sequestration, unlocking new revenue for growers. The virtuous cycle bolsters premium legume seed demand, embedding sustainability as a commercial driver for the Asia-Pacific forage seed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weather volatility reducing seed-multiplication yields | −0.4% | Monsoon-dependent regions | Short term (≤ 2 years) |

| Patchy genetically modified organism (GMO) regulatory acceptance | −0.3% | Varies by country | Long term (≥ 4 years) |

| Counterfeit seed trade eroding farmer trust | −0.2% | India, China, and Southeast Asia | Medium term (2–4 years) |

| Declining smallholder pasture acreage from peri-urban land conversion | −0.2% | China, India, and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weather Volatility Reducing Seed-Multiplication Yields

Climate variability cut seed-multiplication yields 15–25% in 2024 as erratic monsoon onset disrupted flowering windows. Hybrid production is particularly vulnerable because parent-line crossing demands precise timing; a missed window can wipe out an entire cycle. Producers resort to controlled-environment facilities, which hike costs 40–60% versus field multiplication, squeezing margins in the Asia-Pacific forage seed market. Insurance products and climate-smart agronomy guidelines are emerging, yet the near-term supply chain remains constrained.

Patchy GMO Regulatory Acceptance Across Asia-Pacific

Japan’s approval process for new GMO crops spans 5–7 years, whereas Australia clears gene-edited varieties within 12 months. China’s evolving rules inject market uncertainty, and India’s pending biotechnology bill could either streamline or further impede adoption. Seed companies must therefore carry duplicative product portfolios, inflating R&D costs and delaying regional launches. Regulatory fragmentation ultimately restrains innovation diffusion in the Asia-Pacific forage seed market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrid Dominance with Emerging Cost Sensitivity

Hybrid seeds held 80.60% of the Asia-Pacific forage seed market share in 2024, thanks to 25–35% yield premiums over open-pollinated lines. This leadership is entrenched in Japan, Australia, and South Korea, where dairy operators value uniformity and feed conversion efficiency. The segment’s 2.77% CAGR trails overall growth, signaling saturation among large commercial farms. Price-sensitive smallholders increasingly favor open-pollinated varieties that permit seed saving, aided by community multiplication schemes promoted by Indian and Thai extension agencies.

Open-pollinated varieties and hybrid derivatives therefore outpace hybrids on a relative basis, expanding access to certified genetics in developing markets. Companies such as DLF and Barenbrug channel R&D into improving drought tolerance and protein content without compromising farmer-saved seed rights. Public-private programs distribute foundation seed, empowering local cooperatives to scale multiplication. As digital channels broaden distribution, this sub-segment will contribute disproportionately to incremental volume, sustaining diversity within the Asia-Pacific forage seed market size trajectory.

By Crop: Alfalfa Retains Value Leadership while Sorghum Drives Volume Growth

Alfalfa commanded 24.90% of the Asia-Pacific forage seed market size in 2024, underpinned by Japanese and South Korean dairy herds that pay USD 15–25 per kilogram for premium cultivars. Controlled-environment greenhouses extend alfalfa production into tropical belts, widening adoption among higher-income producers. Despite climatic constraints, nutritional superiority that lifts milk yields 10–15% ensures alfalfa’s continued value leadership.

Forage sorghum records a 3.67% CAGR through 2030, the fastest within crop categories, as drought-prone Southeast Asian and northern Australian growers pivot toward resilient genetics capable of sustaining 85% yield under water stress. Government climate-smart grants subsidize seed costs, accelerating uptake among mid-scale farmers. Pearl millet, Sudan grass, and multispecies legume blends occupy niche roles, supplying integrated systems focused on soil health and carbon sequestration. Collectively, these dynamics diversify crop demand, reinforcing long-term expansion in the Asia-Pacific forage seed market.

Geography Analysis

Japan accounted for 48.40% of 2024 revenue in the Asia-Pacific forage seed market, illustrating the spending power of intensive dairy producers willing to invest USD 200–400 per hectare on certified hybrids. Precision feeding regimens and stringent quality assurance make predictable forage composition indispensable. Consequently, seed companies custom-tailor cultivars for Japan’s cool-temperate zones, and digital advisory services help aging farmers reduce labor while sustaining yields.

China and India combine scale with policy impetus. China’s directive to replace 20% of feed grain with forage by 2025 institutionalizes demand for hybrids and drought-tolerant sorghum, while India’s NFSM-Fodder subsidies lower entry barriers for smallholders. Seed firms maintain joint ventures with local partners to navigate compliance and localization. Australia, though mature, functions as an innovation hub exporting genetics throughout Southeast Asia, adding a technology premium to regional trade flows.

The Philippines emerges as the fastest-growing market at 4.62% CAGR, energized by USD 200 million in government feed security funding that halves seed costs for growers. Vietnam, Indonesia and Bangladesh represent the next frontier, improved logistics and e-commerce are already shortening supply chains. As cross-border collaborations deepen, seed movement intensifies, underscoring geographic interdependence in the Asia-Pacific forage seed market.

Competitive Landscape

The top five players, Advanta Seeds (UPL Ltd.), DLF A/S, Bayer AG, Land O’Lakes Inc., and Royal Barenbrug Group, held 59% collective market share in 2024, reflecting moderate concentration in the Asia-Pacific forage seed market. Multinationals leverage global germplasm banks yet localize breeding to satisfy diverse climates. Bayer allocates USD 50 million per year to genomic selection targeting faster trait stacking, while DLF A/S invests in tropical cultivar lines for Southeast Asian pastures.

Regional champions exploit niche opportunities. Pacific Seeds specializes in sorghum suited to Queensland’s dry tropics, and Takii Seed develops Japanese-adapted legumes with enhanced digestibility. Partnerships with public institutes such as the Australian Commonwealth Scientific and Industrial Research Organization enable mid-size firms to access cutting-edge phenotyping platforms without massive capital outlay.

Strategic differentiation increasingly focuses on sustainability credentials and climate adaptation rather than traditional yield maximization, as corporate buyers prioritize carbon sequestration potential and drought tolerance alongside productivity metrics. Bayer's USD 50 million annual Asia-Pacific breeding investment targets genomic selection technologies that reduce variety development timelines from 8-10 years to 4-5 years, while Royal Barenbrug Group emphasizes tropical and subtropical variety development for expanding Southeast Asian markets.

Asia-Pacific Forage Seed Industry Leaders

Bayer AG

Land O’Lakes Inc.

Royal Barenbrug Group

DLF A/S

Advanta Seeds (UPL Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Rasi Seeds signed an MoU with ICAR-IGFRI to enhance forage seed supply across India. The collaboration aims to improve livestock nutrition and boost fodder availability through advanced seed technologies. This partnership supports sustainable agriculture and strengthens the forage value chain.

- August 2025: DLF introduced eight new forage grass varieties, offering improved dry-matter yield, disease resistance, and seasonal adaptability. These innovations aim to enhance forage performance and sustainability across diverse agricultural regions.

- August 2024: The Indian Council of Agricultural Research (ICAR), in collaboration with agricultural universities, released seven climate-resilient forage crop varieties as part of a broader launch of 109 new crop varieties, inaugurated by Prime Minister Narendra Modi. These forage crops are designed to enhance livestock feed security across diverse agro-climatic zones in India.

Asia-Pacific Forage Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Alfalfa, Forage Corn, Forage Sorghum are covered as segments by Crop. Australia, Bangladesh, China, India, Indonesia, Japan, Myanmar, Pakistan, Philippines, Thailand, Vietnam are covered as segments by Country.Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Other Traits | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

Crop

| Alfalfa |

| Forage Corn |

| Forage Sorghum |

| Other Forage Crops |

Country

| Australia |

| Bangladesh |

| China |

| India |

| Indonesia |

| Japan |

| Myanmar |

| Pakistan |

| Philippines |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Other Traits | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Crop | Alfalfa | ||

| Forage Corn | |||

| Forage Sorghum | |||

| Other Forage Crops | |||

| Country | Australia | ||

| Bangladesh | |||

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Myanmar | |||

| Pakistan | |||

| Philippines | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms