Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 34.33 Billion |

| Market Size (2026) | USD 37.45 Billion |

| Market Size (2031) | USD 57.86 Billion |

| Growth Rate (2026 - 2031) | 9.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Luxury Hotel Market Analysis by Mordor Intelligence

The Asia-Pacific luxury hotel market size stands at USD 34.33 billion in 2025 and is projected to reach USD 57.86 billion by 2031, reflecting a 9.10% CAGR over 2026-2031 The Asia-Pacific luxury hotel market is experiencing varied demand patterns that require portfolio-specific yield strategies and precise channel management. Operators are leveraging targeted pricing and differentiated room types to balance weekend leisure peaks with mid-week corporate demand. Early adoption of AI-driven revenue and personalization workflows has boosted booking conversions and ancillary spend, creating a digital capability gap among competitors. Loyalty programs are increasingly integrated with curated wellness and cultural experiences to sustain average daily rates without diminishing perceived value. Stakeholders are emphasizing product differentiation, sustainability upgrades, and owned-channel activation to reduce volatility and strengthen rate leadership. Investment is focused on scarce trophy assets in select urban and resort hubs to secure durable pricing power and stable cash flows. Affluent traveler demand is strengthening in Australia, Indonesia, and Singapore, while Chinese operators are adjusting rates and inventory to local market conditions. Wellness offerings are now central to booking decisions, with integrated spa and fitness programs supporting higher rate premiums. Direct channels, enhanced by AI-personalized offers and loyalty-led benefits, are enabling brands to recapture margins and optimize customer lifetime value.

Key Report Takeaways

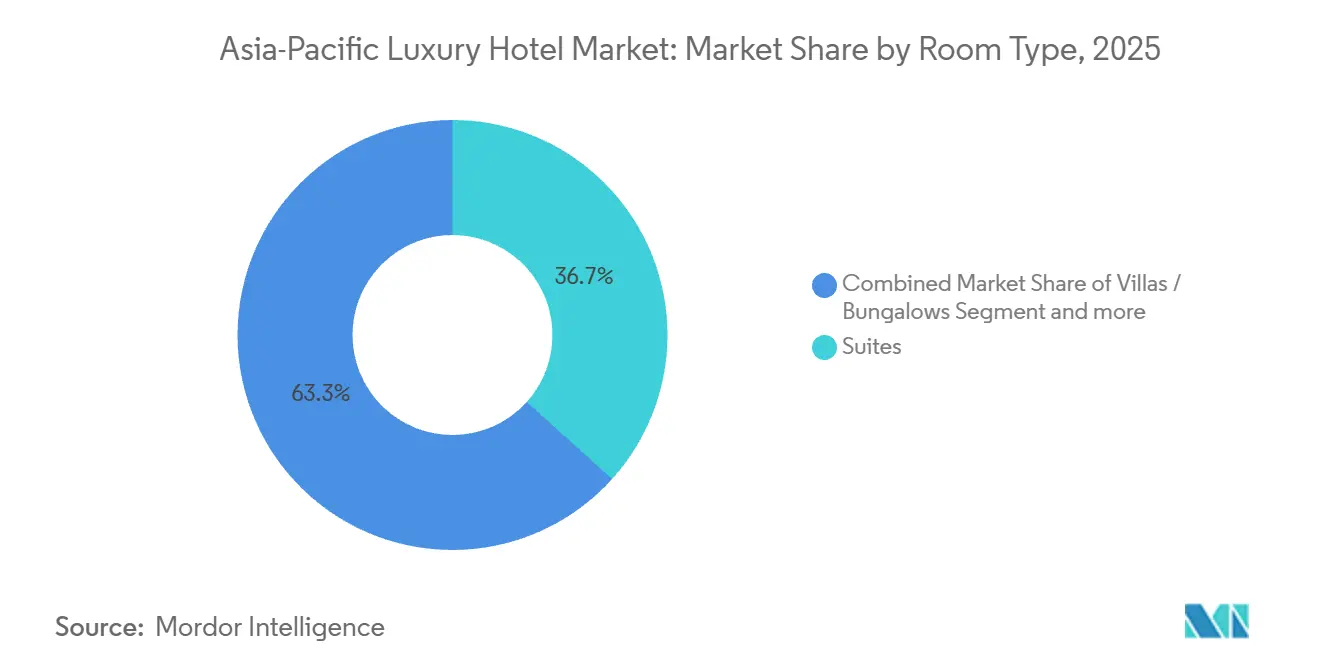

- By room type, Suites held 36.68% of the Asia-Pacific luxury hotel market share in 2025, while Villas/Bungalows are forecast to expand at a 9.13% CAGR through 2031.

- By booking channel, Online Travel Agencies accounted for 40.21% of bookings in 2025, while Direct Booking is projected to grow fastest at a 10.60% CAGR.

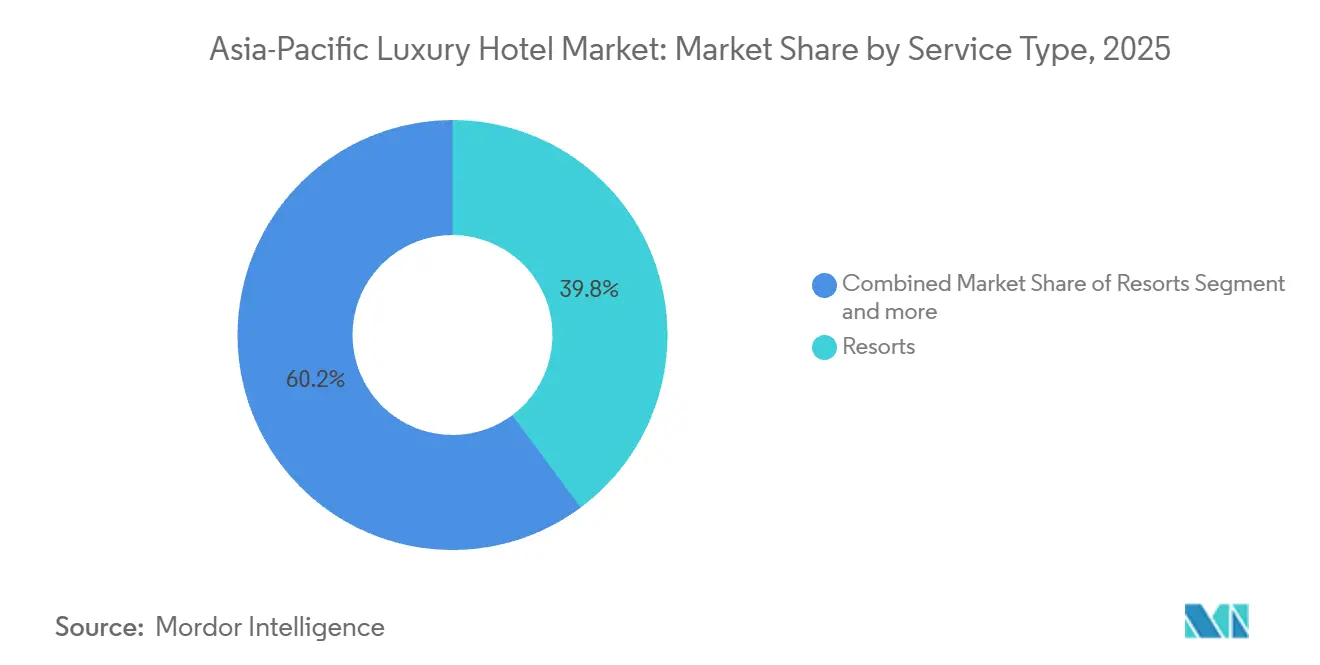

- By service type, Resorts commanded a 39.82% share of the Asia-Pacific luxury hotel market size in 2025, and the Other Service Types segment is expected to grow at a 10.05% CAGR.

- By country, China accounted for 43.62% of the Asia-Pacific luxury hotel market share in 2025, while India is projected to post the highest growth at a 15.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Luxury Hotel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Affluence Among Middle-Class and High-Net-Worth Individuals in Asia-Pacific | +2.1% | Strongest in Australia, Indonesia, Singapore | Medium term (2-4 years) |

| Recovery in Travel and Investment in Tourism Infrastructure Following the Pandemic | +1.8% | Vietnam, Thailand, Japan | Short term (≤ 2 years) |

| Rising Outbound Travel from China and India Within the Asia-Pacific Region | +1.6% | Core APAC with Southeast Asia spillover | Medium term (2-4 years) |

| Government Support and Incentives Promoting Luxury Tourism | +1.3% | Vietnam, Thailand, Japan | Short term (≤ 2 years) |

| Growth of Ultra-Luxury Branded Residential Properties Connected to Hotels | +1.2% | Vietnam, Japan, Singapore | Long term (≥ 4 years) |

| Expansion of Long-Stay Workcation Offerings for Remote Employees in Southeast Asia | +1.1% | Philippines and broader Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Affluence Among Middle-Class and High-Net-Worth Individuals in Asia-Pacific

Asia Uplift highlights the rapid growth of affluent and high-net-worth travelers in Asia Pacific, with the region projected to account for 50% of global air passenger growth and 35% of leisure travel spending by 2025. China and India are leading this surge, supported by relaxed visa regulations, expanded international flight connectivity, and increased urban wealth. Rising incomes and a growing middle class are driving demand for premium accommodations, luxury resorts, and personalized experiences. Southeast Asia is also seeing significant growth as emerging markets adopt higher discretionary spending on leisure and travel. This trend is creating strong opportunities for luxury hotel operators to target multi-day stays, curated experiences, and high-value services that appeal to affluent travelers.[1]Source: Amadeus Research Team, “Travel Trends 2025: Asia Uplift,” Amadeus, amadeus.com. AI-enabled merchandising and conversational booking tools are lifting cross-sell and upsell rates, indicating that tech-forward operators can widen ADR and RevPAR gaps within the Asia-Pacific luxury hotel market. The net effect is a reweighting of capital and brand attention toward submarkets and product types where affluent travelers reward experience depth and privacy, a pattern that is reshaping portfolio priorities in the Asia-Pacific luxury hotel market.

Recovery in Travel and Investment in Tourism Infrastructure Following the Pandemic

Inbound flows and air capacity additions are improving regional connectivity, which supports longer stays and multi-stop itineraries in the Asia-Pacific luxury hotel market. International visitor arrivals in the Asia Pacific region reached 295.7 million in the first half of 2025, reflecting a 92.6 % recovery compared to pre‑pandemic levels, highlighting the strength of the travel rebound across the region.[2]Source: Pacific Asia Travel Association (PATA), “Asia-Pacific Tourism Nearing Full Recovery: Reaching 295 Million in the First Half of 2025,” PATA, pata.org Japan’s strong international visitation in 2024 reinforced pricing power in gateway cities where new supply trails demand, helping premium hotels secure higher rate tiers. Vietnam’s ongoing visa facilitation and direct-flight additions have reduced friction for long-haul and near-haul leisure travelers, benefiting resort operators positioned on established coastal corridors. Thailand and select island destinations are managing more competitive dynamics as alternative accommodations expand, prompting traditional luxury hotels to enhance value propositions and offer curated services. The underlying theme is that infrastructure alignment matters as much as demand recovery, as markets combining air access, luxury retail adjacencies, and high-service inventory tend to achieve stronger yield outcomes.

Rising Outbound Travel from China and India Within the Asia-Pacific Region

Regional travel patterns show Chinese and Indian travelers allocating more trips within Asia, which diversifies destination demand and extends premium shoulder-weekend patterns in the Asia-Pacific luxury hotel market. Operators report resilient domestic corporate demand in India alongside strengthening premium leisure, with room signings accelerating, including a 90% year-on-year increase in India signings reported by one major brand during 2025, which positioned new assets to capture rising outbound and domestic flows in the Asia-Pacific luxury hotel market.[3]Source: Hyatt Newsroom, “Record Pipeline: Hyatt Enters 2026 with 148,000 Rooms,” Hyatt, newsroom.hyatt.com. India’s top-tier city performance in 2025 also reflected stronger rate discipline with RevPAR gains in Delhi and Mumbai that supported brand expansion pipelines across the Asia-Pacific luxury hotel market. Properties that localize culinary, wellness, and concierge services for Mandarin, Cantonese, and Hindi speakers are seeing better conversion and rate realization, since personalization is now an expected baseline in the Asia-Pacific luxury hotel market. As travel preferences continue to evolve toward privacy, longer stays, and curated experiences, villas, suites with kitchenettes, and service-rich resort formats stand to gain wallet share in the Asia-Pacific luxury hotel market.

Government Support and Incentives Promoting Luxury Tourism

Visa policy liberalization and targeted hospitality support are compressing ramp-up times for new properties in receptive destinations within the Asia-Pacific luxury hotel market. Vietnam’s broader visa access has eased planning for multi-country trips, which in turn helps upscale and luxury resorts increase their conversion of high-intent travelers in the Asia-Pacific luxury hotel market. Thailand’s facilitation measures point in the same direction even as operators navigate cyclical headwinds, which keeps attention on experiential differentiation to defend rate integrity in the Asia-Pacific luxury hotel market. Japan’s emphasis on universal design and sustainability-linked upgrades positions premium inventory to meet rising accessibility and environmental standards without compromising service depth in the Asia-Pacific luxury hotel market. These policies are most effective when paired with direct air links and high-service hospitality ecosystems, which can add meaningful length-of-stay and average spend across the Asia-Pacific luxury hotel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure and Land Acquisition Costs in Prime Locations | -1.4% | Japan, Singapore, South Korea | Long term (≥ 4 years) |

| Macroeconomic Instability and Currency Fluctuations | -0.9% | China, Thailand, select island markets | Short term (≤ 2 years) |

| Increased ESG Compliance Expenses for Luxury Properties | -0.7% | Singapore and cross-border portfolios | Medium term (2-4 years) |

| Competitive Pressure from Ultra-Luxury Short-Term Rental Platforms | -0.6% | Bali and major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Land Acquisition Costs in Prime Locations

Elevated per-key valuations in core Asian gateways have kept many would-be entrants on the sidelines, which limits greenfield luxury supply in the Asia-Pacific luxury hotel market. Sponsor underwriting must assume high ADR and steady occupancy to clear financing hurdles, and cyclical dips can impair coverage ratios in projects with traditional leverage across the Asia-Pacific luxury hotel market. Higher construction and borrowing costs make projects more equity intensive, and lenders are favoring conservative structures that ration development in land-scarce districts within the Asia-Pacific luxury hotel market. As a result, management contracts, franchise platforms, and attached branded-residence models are gaining traction because they reduce balance-sheet risk while preserving fee income in the Asia-Pacific luxury hotel market. The trade-off is lower operating leverage during upswings, which requires operators to scale brand-led demand generation to maintain growth in the Asia-Pacific luxury hotel market.

Macroeconomic Instability and Currency Fluctuations

Soft operating conditions in China during 2025 underscored forecast sensitivity in a market that anchors regional volume, which has pushed portfolio operators to rebalance exposure across nearby leisure corridors in the Asia-Pacific luxury hotel market. Currency moves and capital-market shifts complicate outbound travel budgets and weigh on rate realization for long-haul trips, which redirects some premium demand toward intraregional destinations in the Asia-Pacific luxury hotel market. Dollar-denominated debt paired with local-currency revenue can pressure margins when hedging costs rise faster than ADR, which reinforces the case for localized financing and dynamic pricing in the Asia-Pacific luxury hotel market. When volatility intensifies, rate integrity and length-of-stay management become more important than occupancy at any cost, especially in resorts and villas that depend on curated experiences in the Asia-Pacific luxury hotel market. Operators that match local demand pulses with precise room-type and channel mixes tend to preserve pricing power even when macro headwinds are present in the Asia-Pacific luxury hotel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Room Type: Villas Capture Extended-Stay Premiums

Suites held the largest share at 36.68% in 2025, while Villas/Bungalows are set to grow at the fastest pace with a 9.13% CAGR through 2031 in the Asia-Pacific luxury hotel market. Longer-stay executives and multi-generational leisure travelers are tilting toward private outdoor space and service-rich formats, which supports higher effective rates for villas in the Asia-Pacific luxury hotel market. Remote and hybrid work has increased the appeal of residences and villas with dedicated workspace and strong connectivity, a shift that benefits resorts with flexible inventory in the Asia-Pacific luxury hotel market. Standard luxury rooms remain volume anchors for groups and corporate programs, while penthouses and presidential suites serve brand halo roles rather than scale revenue engines in the Asia-Pacific luxury hotel market. The outcome is a more segmented room-mix strategy where properties balance suite density with higher-yield villa clusters to address distinct length-of-stay and privacy preferences in the Asia-Pacific luxury hotel market.

Operators are redesigning greenfield resort projects to expand detached or semi-detached inventory that can flex between owner use and hotel-managed rental pools, which keeps utilization high in the Asia-Pacific luxury hotel market. Villas that integrate wellness spaces and family-friendly layouts tend to capture incremental nights, especially when paired with light-touch but attentive service in the Asia-Pacific luxury hotel market. Urban luxury hotels are also experimenting with small-footprint residential-style suites to retain travelers who might otherwise pivot to serviced apartments in the Asia-Pacific luxury hotel market. Where land constraints limit standalone villas, brands are layering service elements that emulate villa experiences, including private dining, in-room wellness, and micro-retreat programming within suites in the Asia-Pacific luxury hotel market. This approach broadens addressable demand without overcommitting to single-use configurations in the Asia-Pacific luxury hotel market.

By Booking Channel: Direct Platforms Reclaim Margin

Online Travel Agencies commanded 40.21% of bookings in 2025, yet Direct Booking is the fastest-growing channel at a 10.60% CAGR, a spread that signals margin recapture opportunities in the Asia-Pacific luxury hotel market. Brands are implementing AI-driven personalization and dynamic bundling to convert high-intent traffic and grow owned-channel share across the Asia-Pacific luxury hotel market. Technology partners report that hotel adoption of automated merchandising and mobile-first flows improves direct conversion and ancillary attachment in the Asia-Pacific luxury hotel market. Direct channels also facilitate richer pre-arrival preference capture and loyalty integration, which strengthens retention and reduces reliance on third-party pricing in the Asia-Pacific luxury hotel market. As these capabilities mature, the gap between digital leaders and laggards will widen in both revenue and cost outcomes across the Asia-Pacific luxury hotel market.

Distribution plumbing remains uneven, with only a fraction of property-management systems in Asia offering seamless integrations to all major third-party platforms, a gap that can drag conversion and pricing precision in the Asia-Pacific luxury hotel market. Operators that cleanly connect inventory, rates, and availability across direct and indirect pipes can manage parity and tactical fences more effectively within the Asia-Pacific luxury hotel market. Corporate and wholesale segments continue to play anchoring roles in certain cities, yet their rate ceilings underscore the strategic importance of owned-channel growth in the Asia-Pacific luxury hotel market. Brands are also training reservations teams and on-property staff to support conversational commerce, which complements self-serve digital journeys in the Asia-Pacific luxury hotel market. The result is a more resilient mix where direct bookings fund continuous experience improvements in the Asia-Pacific luxury hotel market.

By Service Type: Hybrid Models Accelerate

Resorts commanded 39.82% share in 2025, and the Other Service Types segment that includes branded residences, serviced estates, and hybrid hospitality is forecast to grow at 10.05% CAGR in the Asia-Pacific luxury hotel market size. Resorts benefit from the rise of wellness-centered itineraries and longer leisure stays that favor integrated amenities in the Asia-Pacific luxury hotel market. Hybrid formats expand monetization by combining ownership and transient elements, which can smooth seasonality in the Asia-Pacific luxury hotel market. Business and airport hotels are reconfiguring asset plans with more suites, club floors, and flexible spaces to align with mixed-use demand in the Asia-Pacific luxury hotel market. Suite hotels sit between traditional room products and villas, absorbing family and small-group stays that need privacy and light self-catering in the Asia-Pacific luxury hotel market.

Branded-residential attachments add extended-stay and repeat-visit potential that complements resort ADR ambitions within the Asia-Pacific luxury hotel market. As brands standardize owner services and rental-pool operations, these hybrids can create fee streams and brand visibility beyond classic hotel channels in the Asia-Pacific luxury hotel market. Urban luxury formats are also incorporating club lounges and curated wellness to keep higher-spend guests in-house longer in the Asia-Pacific luxury hotel market. Operators that align formats with local regulations and urban plans tend to unlock incremental floor area and mixed-use synergies in the Asia-Pacific luxury hotel market. These shifts converge on a single goal, which is to capture a broader set of high-value trips across the Asia-Pacific luxury hotel market.

Geography Analysis

China held 43.62% of regional value in 2025 and remains a volume cornerstone, while its future growth trail will depend on the pace of domestic demand normalization in the Asia-Pacific luxury hotel market. India’s hospitality sector began 2025 on a strong note, with RevPAR rising 16.3 % year-on-year and 8 % sequentially, driven by robust leisure and corporate demand. Key cities such as Bengaluru, Delhi, Mumbai, Chennai, and Hyderabad recorded notable growth, reflecting diverse demand drivers across urban centers. The quarter saw 79 new hotel signings, adding nearly 9,500 keys, alongside 31 openings, signaling continued investor confidence and an active development pipeline. Strategic brand expansions and acquisitions are supporting market depth, particularly in the luxury and upper-upscale segments.[4]Source: JLL Report, “Indian Hospitality RevPAR Jumps 16.3% in Q1 2025,” HRAWI, hrawi.com. Japan’s service bar remains high, with 16 properties receiving 5-star ratings in the 2026 Forbes Travel Guide, a quality signal that supports sustained ADR premiums in the Asia-Pacific luxury hotel market. Mature markets such as Australia and South Korea continue to emphasize asset refresh cycles and technology upgrades to align with guest expectations in the Asia-Pacific luxury hotel market.

Southeast Asia shows the widest performance dispersion, with Vietnam’s policy facilitation and air connectivity helping resort corridors gain share within the Asia-Pacific luxury hotel market. Thailand and select island destinations are managing tighter competition from alternative accommodations, which is encouraging brand-led experiential differentiation in the Asia-Pacific luxury hotel market. Singapore’s disciplined supply environment sustains rate resilience and nudges owners toward ancillary revenue optimization over volume growth in the Asia-Pacific luxury hotel market. Indonesia’s higher-spending traveler base presents structural upside that will depend on ongoing connectivity and service-quality lifts in secondary destinations across the Asia-Pacific luxury hotel market. Across these geographies, successful operators localize product and programming to mirror source-market preferences in the Asia-Pacific luxury hotel market.

Competitive Landscape

The Asia-Pacific luxury hotel market remains highly competitive, with international chains, regional champions, and strong independent operators all contributing to growth. Leading global brands are expanding their presence across both mature and emerging markets, focusing on luxury and upper-upscale segments to capture rising affluent demand. Portfolio strategies prioritize capital-light models through management and franchise agreements, enabling broader brand reach and loyalty program engagement. Hotel owners are emphasizing service differentiation and experience design to maintain average daily rates and attract curated stays. Overall, the market rewards operators who balance scale with tailored, high-quality guest experiences.

Operators are complementing portfolio expansion with technology investments aimed at improving yield management and guest personalization. AI-powered revenue and merchandising tools are enhancing booking conversion and ancillary spend, while travelers increasingly expect customized experiences both online and on-property. Uneven distribution system integration continues to challenge rate parity and inventory control for some hotels. Brands with strong connectivity and mobile-first direct channels report better loyalty engagement and repeat visitation. Execution in service, digital readiness, and distribution effectiveness is increasingly defining competitive advantage beyond mere scale.

Domestic champions are also scaling rapidly, aligning new hotel pipelines with growing premium travel demand. Indian operators are expanding across formats and market segments, while global groups are consolidating presence in secondary cities and emerging resort corridors to mitigate market volatility. Strategic focus on technology adoption, format diversity, and loyalty monetization is shaping operator performance. Consistent guest experiences and efficient direct-channel management remain critical to outperforming competitors. The overall trend reflects an ongoing arms race in service quality, digital capability, and owned-channel optimization across the Asia-Pacific luxury hotel market.

Asia-Pacific Luxury Hotel Industry Leaders

Marriott International

Hilton Worldwide Holdings

Hyatt Hotels Corporation

Accor S.A.

InterContinental Hotels Group (IHG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Marriott International announced 187 new deals in Asia-Pacific excluding China representing more than 28,000 rooms, plus 201 additional deals in Greater China, expanding its asset-light growth focus across the region.

- February 2026: Sixteen Japanese hotels received 5-star ratings in the 2026 Forbes Travel Guide, the highest concentration in Asia-Pacific, validating quality leadership and rate premiums for top-tier properties.

- February 2026: IHCL reported a portfolio of 617 hotels and a pipeline of 256 properties heading into fiscal 2026, reflecting continued expansion and geographic diversification in and beyond India.

- January 2026: Hyatt stated it entered 2026 with a record 148,000 rooms in its global development pipeline, with multiple Asia-Pacific openings scheduled over the next several years and a regional mix biased toward luxury and upper-upscale.

Asia-Pacific Luxury Hotel Market Report Scope

A luxury hotel is defined as a hotel that provides a luxurious accommodation experience to the guest. Luxury hotels typically accommodate high-paying guests and the services and dining are expected to be of high quality. A complete background analysis of the North America Luxury Hotel Market, which includes an assessment of the emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview, is covered in the report.

The Asia-Pacific Luxury Hotel Market is Segmented by Service Type (Business Hotel, Airport Hotel, Suite Hotel, Resort, and Other Service Hotels) and by Geography (China, India, Japan, Australia, Thailand, Vietnam, Rest of Asia-Pacific). The report offers market size and forecasts for the Asia-Pacific Luxury Hotel Market in terms of value (USD billion) for all the above segments.

By Room Type

| Standard Luxury Room |

| Suites |

| Villas / Bungalows |

| Penthouses & Presidential Suites |

By Booking Channel

| Direct Booking (Brand Website, Call Center) |

| Online Travel Agencies (OTA) |

| Travel Agents / Tour Operators |

| Corporate Contracts |

By Service Type

| Business Hotels |

| Airport Hotels |

| Suite Hotels |

| Resorts |

| Other Service Types |

By Geography

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | Singapore | |

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| By Room Type | Standard Luxury Room | ||

| Suites | |||

| Villas / Bungalows | |||

| Penthouses & Presidential Suites | |||

| By Booking Channel | Direct Booking (Brand Website, Call Center) | ||

| Online Travel Agencies (OTA) | |||

| Travel Agents / Tour Operators | |||

| Corporate Contracts | |||

| By Service Type | Business Hotels | ||

| Airport Hotels | |||

| Suite Hotels | |||

| Resorts | |||

| Other Service Types | |||

| By Geography | Asia-Pacific | India | |

| China | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| South East Asia | Singapore | ||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Vietnam | |||

| Philippines | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the Asia-Pacific luxury hotel market?

The Asia-Pacific luxury hotel market size is USD 34.33 billion in 2025 and is projected to reach USD 57.86 billion by 2031 at a 9.10% CAGR, supported by rising affluent demand and wellness-led stays.

Which room and channel segments are leading performance in Asia-Pacific luxury hospitality?

Suites held 36.68% share in 2025 while Villas/Bungalows post the fastest growth at 9.13% CAGR, and OTAs held 40.21% of bookings as Direct Booking grows fastest at 10.60% CAGR.

Which service types show the strongest momentum in the Asia-Pacific luxury hotel market?

Resorts led with 39.82% share in 2025 and the Other Service Types segment, including branded residences and hybrid formats, is set to expand at a 10.05% CAGR, aided by wellness and longer-stay trends.

Which countries anchor demand and growth for premium hotels across Asia-Pacific?

China accounted for 43.62% of 2025 value while India is the fastest-growing at 15.98% CAGR through 2031, with strong RevPAR momentum in Delhi and Mumbai.

How are brands using technology to improve performance in Asia-Pacific luxury hospitality?

Operators using AI-driven personalization and revenue tools report higher conversion and ancillary attachment, while traveler expectations for tailored digital journeys continue to rise.

What strategies are owners and operators using to protect margins in the region?

Owners are leaning into direct-channel growth, hybrid hospitality formats, and experience-led differentiation, while calibrating room mix and rate fences by market conditions across the Asia-Pacific luxury hotel market.

Page last updated on: