Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

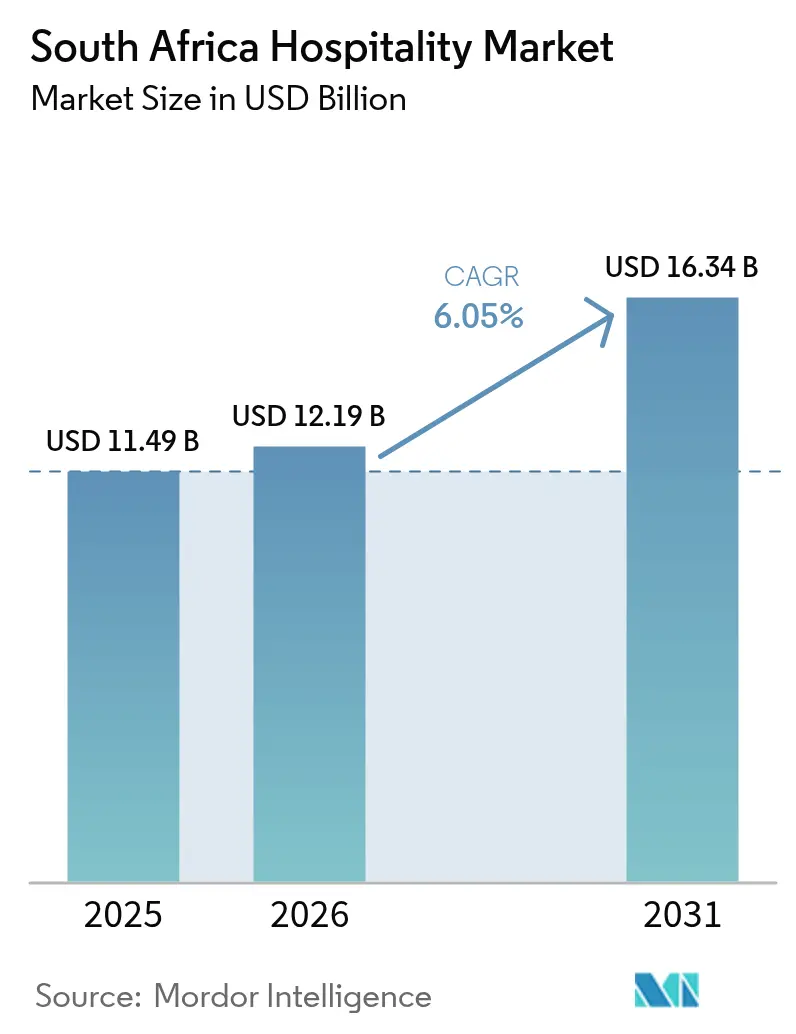

| Base Year Market Size (2025) | USD 11.49 Billion |

| Market Size (2026) | USD 12.19 Billion |

| Market Size (2031) | USD 16.34 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

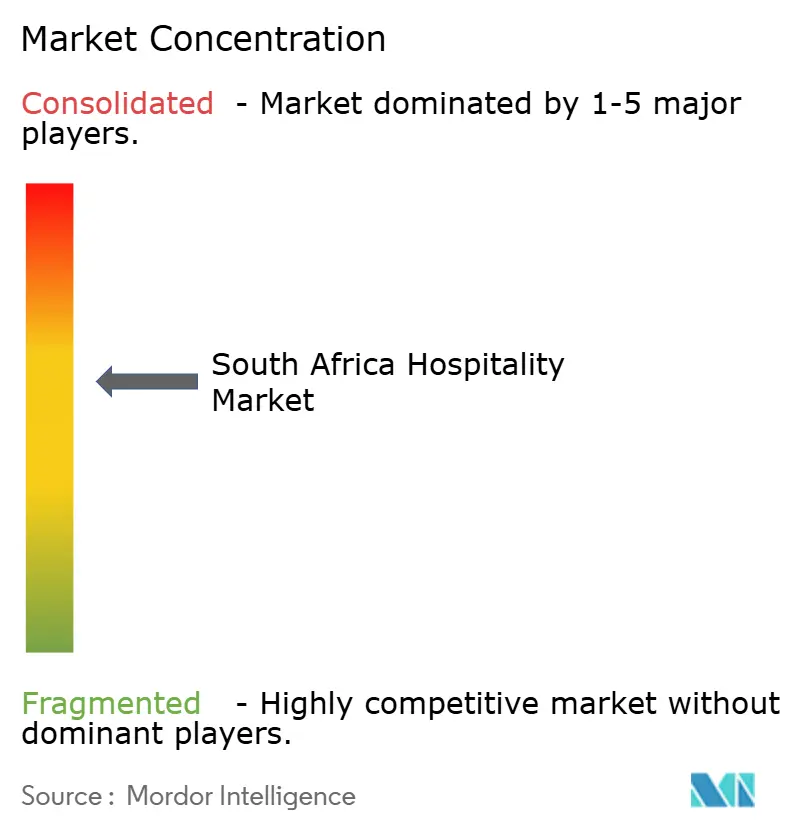

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Hospitality Market Analysis by Mordor Intelligence

The South Africa Hospitality market size is expected to grow from USD 11.49 billion in 2025 to USD 12.19 billion in 2026 and is forecast to reach USD 16.34 billion by 2031 at 6.05% CAGR over 2026-2031.

The post-pandemic rebound in international arrivals, the recovery of meetings and events, and supportive government incentives position the sector for sustained growth. Business travel holds a larger-than-average revenue contribution because corporate visitors extend stays for leisure activities, while digital-nomad demand is building on the back of the new Remote Work Visitor Visa. Chain-hotel dominance, rising use of direct booking channels, and a shift toward extended-stay formats are reshaping competitive strategies. Growth opportunities cluster around Western Cape’s premium leisure corridor, township-based cultural tourism, and green retrofits that hedge against South Africa’s power and water constraints.

Key Report Takeaways

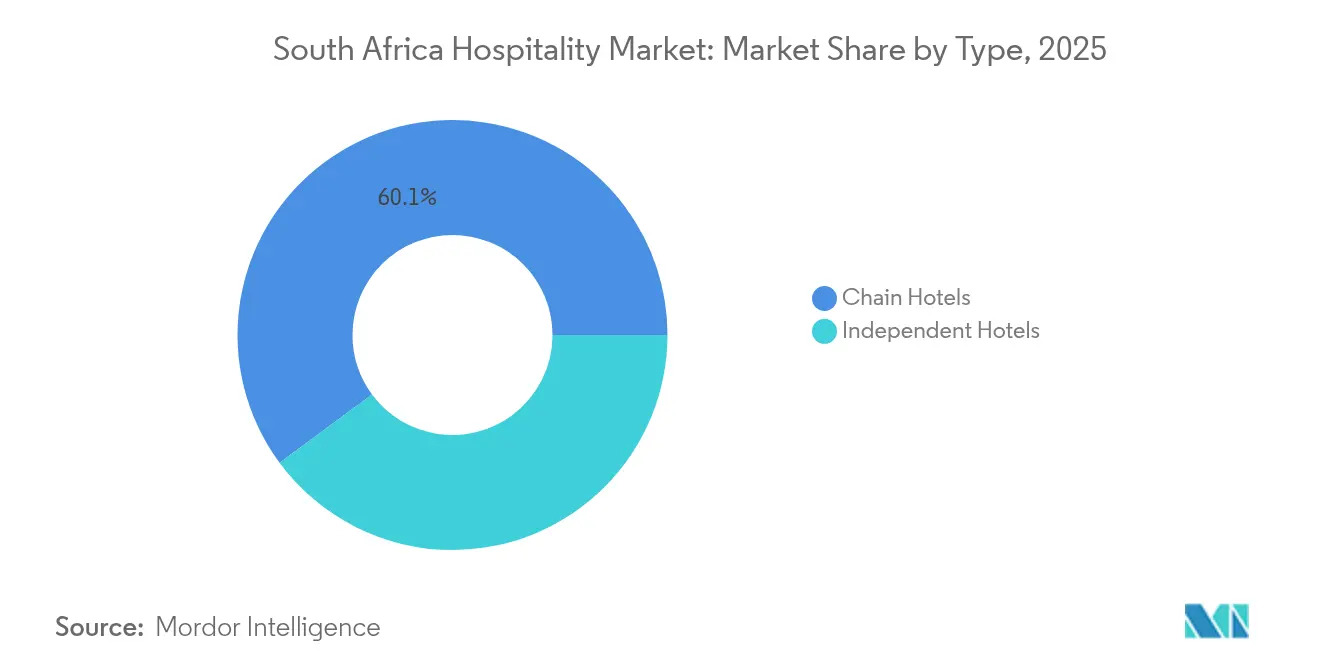

- By type, chain hotels led with 60.12% of South Africa hospitality market share in 2025, while independent hotels are advancing at a 7.52% CAGR through 2031.

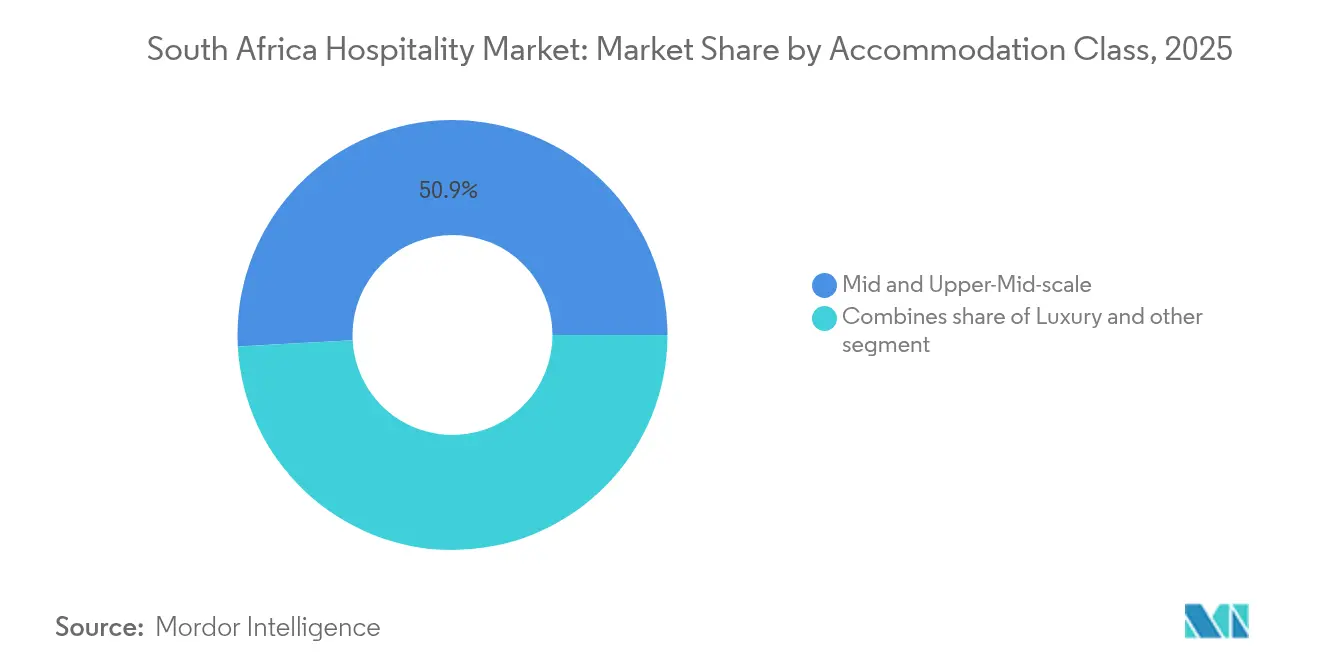

- By accommodation class, mid and upper-mid-scale properties accounted for 50.85% of South Africa hospitality market share in 2025; service apartments are forecast to expand at an 11.1% CAGR to 2031.

- By booking channel, online travel agencies captured 45.70% of South Africa hospitality industry share in 2025, whereas direct digital reservations are growing fastest at 12.05% CAGR through 2031.

- By geography, Gauteng held 29.95% of South Africa hospitality market share in 2025; Western Cape is the fastest-growing region with a 7.05% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound in international tourist arrivals | +1.8% | Western Cape & Gauteng | Medium term (2-4 years) |

| Government Tourism Recovery Plan incentives | +0.9% | National | Short term (≤ 2 years) |

| Expansion of domestic low-cost airline routes | +0.7% | National | Medium term (2-4 years) |

| Growth of MICE events in major metros | +1.1% | Gauteng & Western Cape | Long term (≥ 4 years) |

| Rise of township & cultural tourism demand | +0.4% | National | Long term (≥ 4 years) |

| Investment in green retrofits driven by the energy crisis | +0.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Tourist Rebound Accelerates Business Travel

International tourist arrivals surged to 8.92 million in 2024, with business travel representing a critical 15% segment that generates disproportionate economic impact through extended stays and premium accommodation preferences[1]South African Tourism, “South Africa’s Tourism Rebound Gains Momentum,” southafrica.net. . The recovery pattern reveals strategic shifts in source markets, with Ghana's arrivals increasing 149% following visa waiver agreements, while traditional European markets lag behind pre-pandemic levels by approximately 15%. This geographic rebalancing is reshaping accommodation demand patterns, as African visitors typically favor mid-scale properties while overseas tourists drive luxury segment occupancy. The upcoming G20 Summit in November 2025 is projected to generate a 30% increase in hotel demand compared to 2024, with average nightly rates expected to reach USD190 during the event. Cape Town's tourism sector demonstrates the recovery's momentum, achieving a 72.50% occupancy rate and 20.10% year-on-year RevPAR growth, positioning it as the country's premier destination for both leisure and business travelers.

Government Recovery Plan Incentives Spur Hotel Investment

The Tourism Recovery Plan's tax rebates and marketing funds are reducing capital expenditure risks for hotel developers, creating favorable conditions for property expansion and refurbishment projects. The Tourism Equity Fund, relaunched in November 2023, provides targeted financial assistance to promote inclusive participation in the sector, while the Green Tourism Incentive Programme encourages sustainable practices among tourism businesses[2]Department of Tourism, “Inaugural Township and Village Tourism Expo,” tourism.gov.za. . These incentives are particularly effective in secondary markets where development costs remain manageable compared to prime urban locations. The Market Access Support Programme helps smaller enterprises participate in national and international tourism trade shows, addressing historical barriers to market entry for community-based accommodation providers. The introduction of the Remote Work Visitor Visa in October 2024 represents a strategic pivot toward attracting high-spending digital nomads, with Cape Town projected to contribute USD 3.78 billion (ZAR70 billion) to GDP by 2026 through this segment alone.

Domestic Low-Cost Airlines Unlock Regional Demand

The proliferation of domestic low-cost carrier routes is democratizing access to previously underserved destinations, generating weekend travel demand beyond traditional metro-to-metro corridors[3]Tourism Update, “Meetings and Incentives,” tourismupdate.co.za.. This connectivity improvement is particularly significant for the Garden Route and coastal regions, where accommodation providers can now capture spontaneous leisure travel that was previously constrained by transportation costs and complexity. Regional airports are experiencing increased passenger throughput, creating opportunities for accommodation providers to develop packages targeting domestic travelers seeking affordable short-break experiences. The route expansion coincides with improved tourism safety measures and enhanced marketing of diverse destinations beyond Cape Town and Kruger National Park, addressing the historical concentration of tourism spend in primary markets[4]SATSA, “State of Tourism in South Africa,” satsa.com. . The trend supports the government's objective of achieving more equitable tourism distribution across all nine provinces, reducing dependency on traditional gateway cities for hospitality sector growth.

MICE Expansion Transforms Business-Accommodation Mix

The meetings, incentives, conferences, and exhibitions sector contributed USD 21 million (ZAR 388.5 million) to the South African economy in 2024, with the South Africa National Convention Bureau securing 63 bids for international events valued at USD 64.9 million (ZAR 1.2 billion). Meetings Africa 2024 attracted over 350 exhibitors and 3,000 delegates, demonstrating the sector's capacity to generate concentrated accommodation demand during traditionally low-occupancy periods. The event technology market supporting MICE activities is expanding at 10.30% annually, driving demand for hotels with advanced digital infrastructure and flexible meeting spaces. International conference organizers increasingly prioritize sustainability, with 87% of event professionals viewing green practices as essential, creating opportunities for eco-certified accommodation providers to capture premium MICE bookings. Corporate travel patterns are evolving toward longer stays that blend business and leisure activities, increasing per-visitor accommodation revenue and encouraging hotels to develop packages targeting the growing "bleisure" segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic power-grid load-shedding | -2.1% | National | Long term (≥ 4 years) |

| Water scarcity in drought-prone provinces | -1.3% | Western, Eastern & Northern Cape | Medium term (2-4 years) |

| Safety and security concerns impacting tourist confidence | –0.9% | National, especially urban hubs like Johannesburg & Cape Town | Short term (≤ 2 years) |

| Delays in public infrastructure improvements | –0.7% | Secondary cities and tourism corridors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Load-Shedding Inflates Operating Costs

Stage-6 outages compel large hotel groups to spend over USD 5.4 million (ZAR 100 million) per month on diesel, eroding margins and forcing smaller properties to curtail services. Proposed 36.11% tariff hikes threaten further profitability erosion. Load-shedding disrupts digital booking platforms, refrigeration, and laundry operations, directly affecting guest satisfaction. Capital-intensive solar and battery projects now represent defensive investments against revenue losses, yet 3-5 year payback windows test liquidity. The energy crisis is accelerating the adoption of green retrofit technologies, creating a competitive advantage for properties that can guarantee an uninterrupted power supply to business travelers and conference organizers who cannot tolerate operational disruptions.

Water Scarcity Raises Sustainability Risks

South Africa faces a projected 17% water deficit by 2030, with Cape Town demand set to reach 1.2 billion liters per day. The Lesotho Highlands pipeline maintenance has already disrupted supply to Gauteng and the Free State for six months in 2024–2025. Hotel operators spend on desalination, boreholes, and grey-water systems; during Cape Town’s Day Zero crisis, tourist water-literacy campaigns preserved service continuity. In Johannesburg, intermittent outages obligate hotels to install storage tanks and treatment units, inflating capital budgets. The water crisis is most acute in drought-prone provinces where tourism development is constrained by resource availability, limiting accommodation supply expansion in potentially attractive destinations along the Eastern and Northern Cape coastlines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent Hotels Capture Experience-Driven Demand

Independent properties grew revenue at 7.52% CAGR between 2025 and 2026 as travelers favored localized design and personalized service. Chain hotels still command 60.12% of South Africa hospitality market share because loyalty programs and standardized quality appeal to corporate travelers. Independent operators deploy asset-light digital marketing, social-media storytelling, and partnerships with local artisans, which resonate with visitors seeking cultural immersion. Investors view boutiques favorably for above-average RevPAR potential, but procurement and distribution efficiencies remain challenges. Chain brands counter by launching soft-brand collections that promise uniqueness with back-office scale, intensifying competition for experiential demand.

Second-tier cities with heritage landmarks have become testing grounds where independents match hotel conversions to historic buildings, adding authenticity without brand constraints. Luxury chains rely on global reservation systems, yet their uniform standards can alienate guests craving local flavor. The South Africa hospitality market benefits from this diversity because mid-priced, culturally embedded independents fill the gap between economy chains and high-end resorts.

By Accommodation Class: Service Apartments Lead Extended-Stay Upswing

Mid and upper-mid-scale properties provided 50.85% of South Africa hospitality market size in 2025, reflecting balanced value and comfort. Service apartments, however, are expanding at 11.1% CAGR through 2031 as corporate relocations, digital nomads, and long-stay families seek kitchens, workspace, and laundry facilities. Spier Hotel’s 50 luxury serviced units and Steyn City’s 50 extended-stay apartments highlight premium positioning opportunities.

Service-apartment operators bundle housekeeping with flexible lease terms, blurring lines with traditional hotels. Luxury suites retain higher daily rates buoyed by international tourism rebound, while budget hotels contend with Airbnb’s cost-advantage. Green building certifications and energy-efficient appliances tilt preference toward newly built extended-stay assets that promise lower utility bills amid power constraints.

By Booking Channel: Direct Digital Gains Momentum

Online travel agencies controlled 45.70% of South Africa's hospitality market size in 2025, yet direct digital bookings are rising at a 12.05% CAGR. Mobile-first websites, metasearch advertising, and member-only rate guarantees encourage guests to bypass OTAs. Policy changes in large online marketplaces now permit hotels to undercut OTA prices, boosting conversion on brand channels.

Corporate travel managers adopt API-enabled direct contracts that reduce transaction fees, particularly for high-volume MICE itineraries. Independent properties gain pricing control but must invest in search-engine optimization and payment-gateway security to match OTA reach. Wholesale and traditional agents continue to serve group-tour markets, though their share is shrinking as digital adoption deepens.

Geography Analysis

In the South African hospitality market, Gauteng is the largest geographic sub-segment in 2025, accounting for 29.95% of the market share, while the Western Cape is projected to be the fastest-growing sub-segment from 2026 to 2031, with a CAGR of 7.05%. Gauteng maintains leadership in value terms because Johannesburg supplies steady corporate traffic from finance, mining, and ICT sectors, and international conferences cluster around the Sandton Convention Centre. In 2025 the province will host 18 world-class exhibitions, raising mid-week occupancy and average daily rates. Power-grid instability, however, raises generator expenses and pressures operating margins.

Western Cape’s 71% Airbnb occupancy and 20.12% RevPAR jump showcase varied demand streams ranging from wine tourism to adventure sports. Consistent international airlift into Cape Town International Airport and municipal investment in public-transport safety underpin sustained visibility. The province’s adoption of desalination and recycled-water schemes eases drought risk, though tariffs are creeping upward. KwaZulu-Natal’s USD 108.1 million (ZAR2 billion) Club Med Tinley resort illustrates the scale of coastal resort potential outside primary gateways. Eastern Cape’s Big-Seven wildlife reserves and cultural heritage routes offer differentiation but require road upgrades and safety marketing. Northern Cape’s dark-sky reserves anchor niche astro-tourism, yet accommodation density remains thin, presenting ground-floor opportunities for eco-lodges.

Competitive Landscape

South Africa’s hotel industry is characterized by moderate market concentration, with the five largest groups providing the majority of available rooms. Leading brands benefit from extensive footprints and strong local networks, giving them considerable influence over pricing, distribution, and operational standards. Despite this consolidation, there remains room for independent and niche operators to thrive by offering personalized services, unique experiences, or strategic locations. International hotel groups expand primarily through franchise and management agreements, reducing capital risk while accelerating growth. Ambitious expansion targets include plans for significant increases in hotel numbers and room capacity by 2030.

Domestic players capitalize on local market knowledge and vertically integrated food-and-beverage supply chains to maintain cost advantages. Strong financial results, such as one major operator’s USD 83.5 million profit after tax in 2024, demonstrate resilient demand even amid rising utility costs. Alternative accommodation platforms are gaining popularity, particularly among budget travelers, though regulatory and safety considerations temper their rapid growth. Technology investment is a key differentiator, with AI-driven revenue management and guest experience applications helping to improve bookings and customer loyalty. Properties ensuring consistent power and water supply command higher average daily rates, driving increased investment in sustainable infrastructure like solar microgrids and water treatment systems.

The extended-stay segment shows significant growth potential, currently undersupplied despite a robust compound annual growth rate of over 11%. This signals opportunities for specialized operators to enter and expand within the market. Overall, the South African hospitality landscape balances consolidation among major groups with evolving niches and technological innovation. Sustainable and reliable infrastructure investments are becoming critical factors in competitive positioning. As demand continues to recover and evolve, both international and local players are adapting strategies to capture emerging opportunities across market segments.

South Africa Hospitality Industry Leaders

Marriott International (Protea Hotels)

Tsogo Sun Hotels

Southern Sun

City Lodge Hotel Group

Sun International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Marriott International confirmed openings of Morea House Autograph Collection (Camps Bay) and Lord Charles Hotel Tribute Portfolio (Somerset West), strengthening its luxury footprint.

- February 2025: Hyatt scheduled Park Hyatt Johannesburg for Q2 2025, marking brand re-entry to South Africa.

- December 2024: Radisson Collection Hotel Waterfront Cape Town opened with 175 ocean-view rooms.

- October 2024: Steyn City launched a 50-unit luxury serviced-apartment hotel operated by Saxon Hotel.

South Africa Hospitality Market Report Scope

South Africa is geopolitically unique, with natural and cultural diversity that supports a globally compelling tourism proposition. The country has a sizable tourism industry and is one of the world's most popular long-distance destinations. The market is segmented by Type (Chain Hotels and Independent Hotels) and Segment (Service Apartments, Budget and Economy Hotels, Mid and Upper Mid Scale Hotels, and Luxury Hotels). The report also covers a complete background analysis of the hospitality industry in the South African market, including the assessment of the economy and the contribution of the sectors in the economy, a market overview of key segments and emerging trends in the market segments, market dynamics, insights, and key statistics. The report offers market size and forecasts for Hospitality Industry in South Africa in value (USD million) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Gauteng |

| Western Cape |

| KwaZulu-Natal |

| Eastern Cape |

| Free State |

| North West |

| Limpopo |

| Mpumalanga |

| Northern Cape |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Gauteng |

| Western Cape | |

| KwaZulu-Natal | |

| Eastern Cape | |

| Free State | |

| North West | |

| Limpopo | |

| Mpumalanga | |

| Northern Cape |

Key Questions Answered in the Report

What is the current value of South Africa’s hospitality sector?

The South Africa hospitality industry market size is USD 12.19 billion in 2026.

How fast is the sector expected to grow?

The sector is forecast to expand at a 6.05% CAGR, reaching USD 16.34 billion by 2031.

Which province is growing quickest for hotel revenues?

Western Cape leads regional growth with a projected 7.05% CAGR through 2031.

Which accommodation class shows the strongest upside?

Service apartments are the fastest-growing segment, advancing at 11.1% CAGR.

How serious is load-shedding for hotel operators?

Stage-6 power cuts add fuel costs exceeding ZAR 100 million monthly for large chains, reducing margins and accelerating green retrofits.

What government policy most supports future demand?

The Remote Work Visitor Visa aims to inject ZAR 70 billion into local economies by attracting long-stay digital nomads.

Page last updated on: