Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

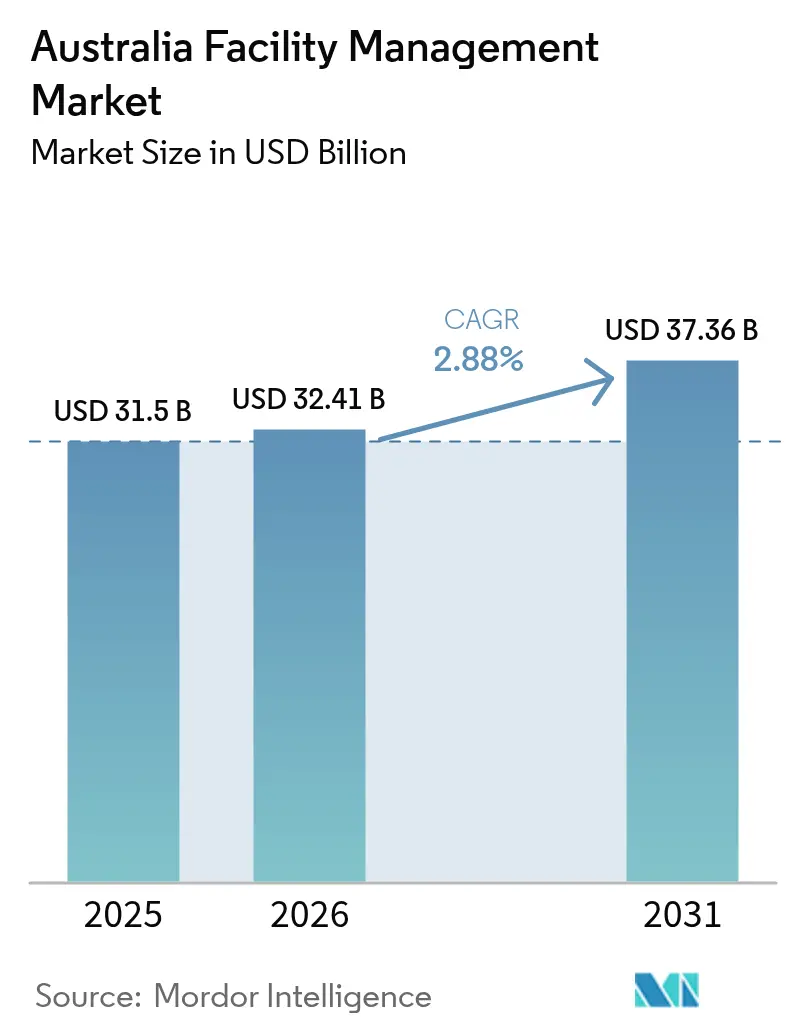

| Base Year Market Size (2025) | USD 31.50 Billion |

| Market Size (2026) | USD 32.41 Billion |

| Market Size (2031) | USD 37.36 Billion |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

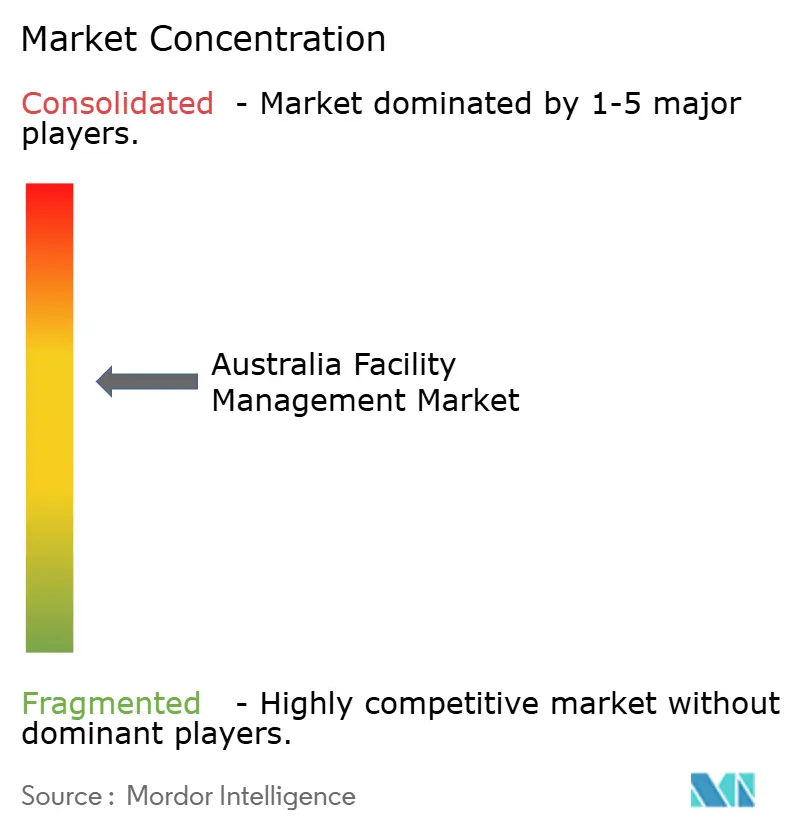

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Facility Management Market Analysis by Mordor Intelligence

The Australia facility management market size was valued at USD 31.50 billion in 2025 and estimated to grow from USD 32.41 billion in 2026 to reach USD 37.36 billion by 2031, at a CAGR of 2.88% during the forecast period (2026-2031). This measured expansion reflects the sector’s pivot from simple cost reduction toward strategic asset optimization and mandatory climate-related reporting. Large infrastructure projects delivered through Public Private Partnership frameworks are bringing facility management providers into project planning stages, while national sustainability rules introduced in 2025 embed ESG compliance into day-to-day operations. Digitalization, from IoT sensors to AI platforms, is now central to performance-based contracts that promise measurable uptime and energy-efficiency outcomes. Outsourcing remains the dominant approach, yet differentiation hinges on technology investment, data transparency, and lifecycle asset management. Rising energy price volatility and an acute shortage of skilled technicians impose operational pressure, but they also accelerate uptake of predictive maintenance and remote monitoring solutions that alleviate labor constraints.[1]Australian Broadcasting Corporation, “Rich in resources, but Australia's energy costs have tripled and manufacturers are hurting,” abc.net.au

Key Report Takeaways

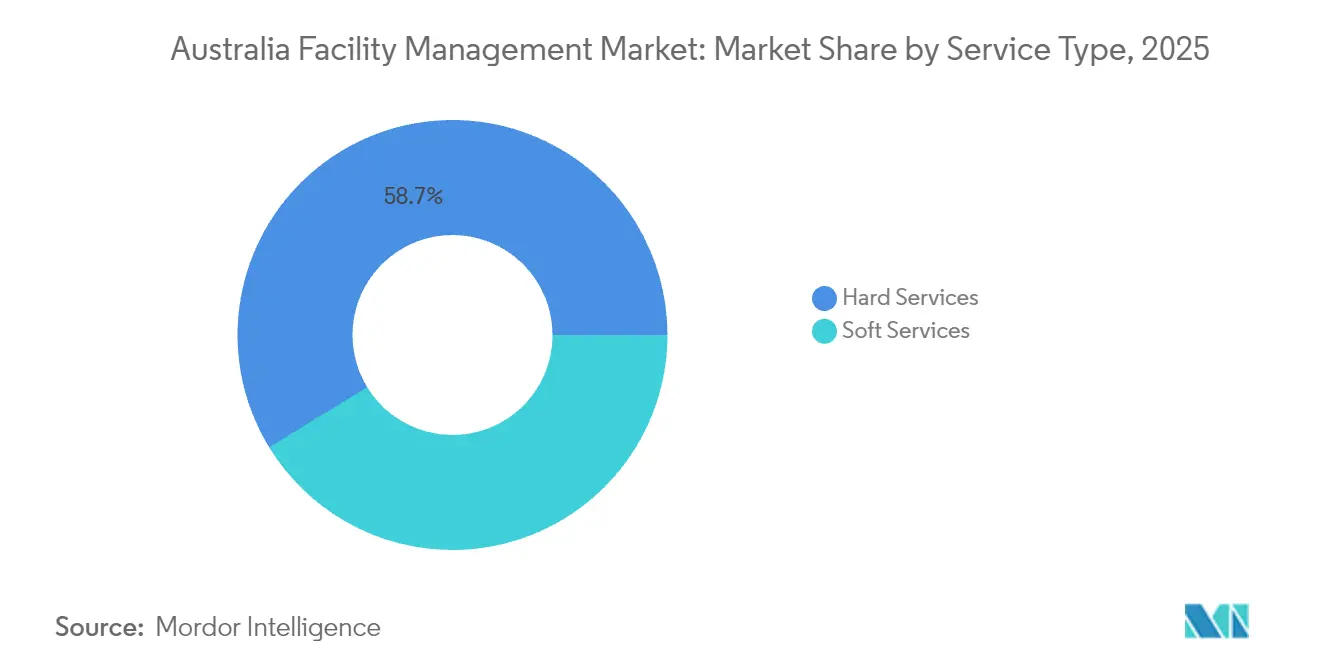

- By service type, hard services led with 58.74% of Australia facility management market share in 2025, while soft services are forecast to expand at a 3.55% CAGR to 2031.

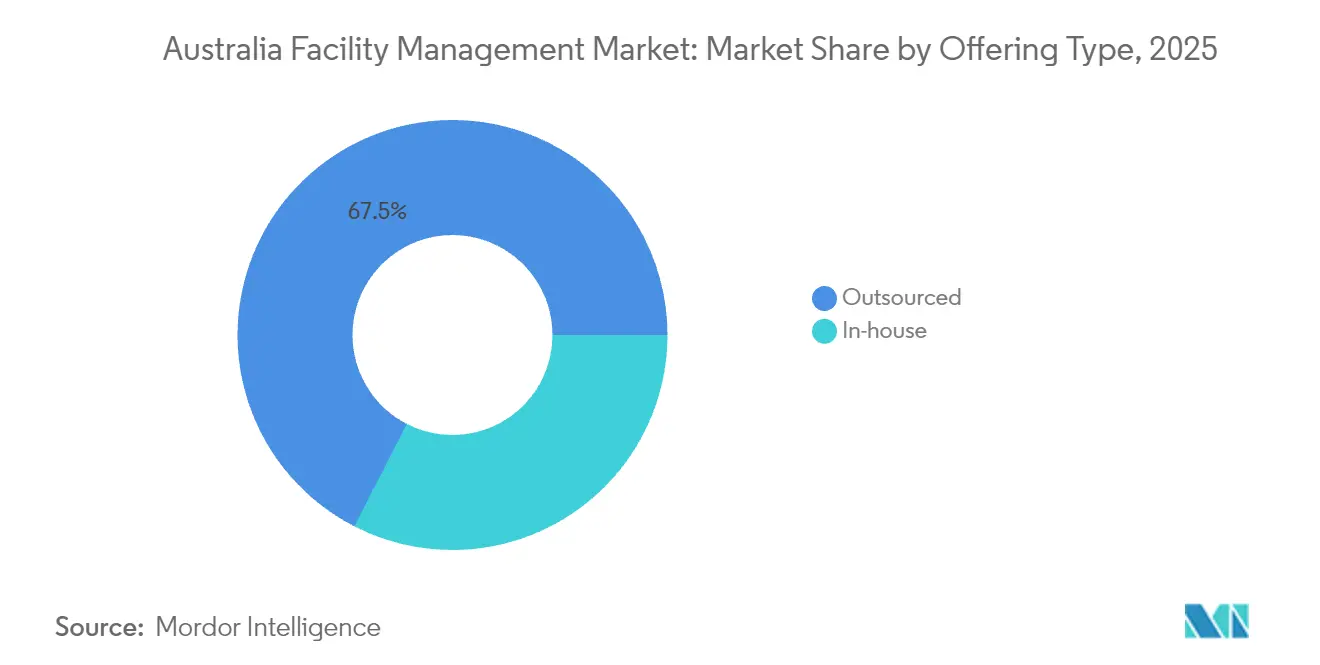

- By offering type, outsourced models accounted for 67.45% of Australia facility management market share in 2025 and are advancing at a 3.62% CAGR through 2031.

- By end-user industry, the commercial segment held 37.05% of the Australia facility management market size in 2025; institutional and public infrastructure is projected to register the fastest 3.18% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation and smart building technologies | +0.8% | National; early uptake in Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Increasing outsourcing trend | +0.6% | National; strongest in metropolitan areas | Short term (≤ 2 years) |

| ESG compliance and sustainability requirements | +0.5% | National; stricter in NSW and Victoria | Long term (≥ 4 years) |

| Infrastructure development and government investments | +0.4% | Queensland, Victoria, NSW corridors | Medium term (2-4 years) |

| Rising demand for integrated FM models from PPP projects | +0.3% | National; concentrated in major hubs | Long term (≥ 4 years) |

| Edge AI and predictive analytics cutting lifecycle costs | +0.2% | Major cities expanding to regional centres | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation and Smart Building Technologies

Nationwide roll-outs of IoT sensors, cloud control platforms, and AI analytics are redefining facility performance standards. International Towers Sydney integrates over 1 million real-time data points to automate lighting, HVAC, and security, delivering double-digit energy savings compared with traditional systems. CSIRO estimates USD 13.7 billion in cumulative national utility savings over a decade if similar digital controls are adopted at scale. [2]Commonwealth Scientific and Industrial Research Organisation, “Scoping the Digital Innovation Opportunity for Energy Productivity in Non-Residential Buildings,” energy.gov.au A successful case is the GPT Group, which lowered energy intensity by 52% and saved USD 20 million annually after deploying an enterprise ESG platform. Adoption momentum is strongest in premium commercial towers but is spreading to logistics hubs and healthcare campuses as predictive maintenance reduces downtime and offsets high labour costs.

Increasing Outsourcing Trend

Organisations are handing non-core functions to specialist partners that offer regulatory know-how, data analytics, and outcome-based pricing. Integrated service contracts secured by ISS at Roy Hill’s mining operations extend beyond cleaning and catering to include sustainability metrics and community engagement. The Queensland Government’s Facilities Management Improvement Initiative illustrates public-sector appetite for bundled services to manage AUD 14.8 billion in assets, with early pilots reporting measurable cost and compliance benefits.[3]The State of Queensland, “Beenleigh company to deliver steel for Queensland Train Manufacturing Program,” qld.gov.auOutsourcing growth is underpinned by the recognition that in-house teams lack scale to fund predictive analytics or ESG reporting tools now required under Australian Sustainability Reporting Standards.

ESG Compliance and Sustainability Requirements

Mandatory climate disclosures effective from 2025 oblige large entities to track Scope 1 and Scope 2 emissions and outline decarbonisation pathways. Macquarie Group’s pledge to reach net-zero operations in 2025 showcases private-sector ambition and sets a high bar for FM providers tasked with real-time carbon reporting. The rule set widens to waste, water, and indoor environmental quality, pushing FM bidders to embed lifecycle sustainability dashboards into proposals. Rio Tinto’s USD 5–6 billion decarbonisation plan, targeting a 50% cut in operational emissions by 2030, further elevates demand for providers able to integrate renewable energy assets and low-carbon materials into maintenance regimes.

Infrastructure Development and Government Investments

Pipeline projects such as the North East Link tunnel PPP, the New Footscray Hospital, and the Logan–Gold Coast Faster Rail collectively inject billions of AUD into transport and healthcare assets, each with 20- to 25-year maintenance obligations baked into the financial close.[4]Infrastructure Pipeline, “New Footscray Hospital,” infrastructurepipeline.org Facility management tenders now require evidence of lifecycle costing, community engagement, and digital twin integration from day one. The trend tightens collaboration between construction consortia and long-term operators, favouring FM companies with design-for-maintenance expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labour shortages | -0.7% | National; acute in regional areas | Short term (≤ 2 years) |

| High initial investment costs for technology integration | -0.4% | National; burdens smaller providers | Medium term (2-4 years) |

| Fragmented regulatory compliance across states | -0.3% | National; complexity varies by state | Long term (≥ 4 years) |

| Volatile energy prices impacting Opex savings ROI | -0.5% | National; industrial sites most affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled Labour Shortages

Seventy-seven percent of employers cannot find technicians and tradespeople, up from 39% in 2020, according to the national employer body. The shortage pushes average wages higher, strains service quality, and lengthens response times, especially in regional towns competing with mining projects. Companies increase apprenticeships and virtual-reality training, yet the pipeline lags demand. Consequently, providers scale remote diagnostics and autonomous cleaning robots to stretch limited human resources.

Volatile Energy Prices Impacting Opex Savings ROI

Residential tariffs rose 14% in 2024, with comparable spikes for commercial users, complicating guaranteed-savings clauses in FM contracts. Manufacturers cite triple-digit increases since 2022, forcing some plants to curtail shifts, which in turn depresses FM revenue tied to occupancy. Providers respond by offering energy-risk-sharing models and on-site solar plus battery solutions that hedge grid volatility. However, smaller FM firms face capital constraints when procuring renewables or advanced analytics platforms, limiting their competitive stance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Infrastructure Complexity

Hard services accounted for 58.74% of the Australia facility management market size in 2025 due to mandatory HVAC, electrical, and fire-safety compliance. Predictive asset management tools are migrating from rail stock to high-rise towers, enabling condition-based maintenance that lifts asset uptime and trims spare-parts inventory. Energy-efficiency retrofits and IAQ mandates keep mechanical, electrical, and plumbing contractors in high demand. Soft services, though smaller in share, are rising at a 3.55% CAGR as clients reconfigure offices for hybrid work and hospitality-grade experiences. Workplace experience apps merge cleaning, catering, and concierge touchpoints into a single digital interface, boosting service transparency. The convergence of hard and soft portfolios favours vendors that can offer integrated dashboards covering critical systems and tenant amenities in one SLA.

Asset-specific insights reinforce growth: smart HVAC retrofits cut energy draw by 9-10% against legacy systems, underpinning demand amid volatile tariffs. Fire and life-safety upgrades gain traction as tall-building stock rises in Sydney and Melbourne, while remote monitoring of lifts and generators counters technician shortages. Within soft services, eco-certified cleaning chemicals and robotic scrubbers address ESG reporting needs and labour gaps, positioning sustainability-linked service lines as premium offerings.

By Offering Type: Outsourced Models Accelerate Integration

Outsourced provision captured 67.45% share in 2025 and is forecast to expand at 3.62% CAGR, keeping the Australia facility management market ahead of in-house models. Boards seek to redirect capital toward digital transformation and leave compliance, roster management, and asset analytics to specialised firms. Single-service contracts fade as bundled and integrated packages gain traction; bundled engagements consolidate two or three discrete services, whereas integrated deals place every site-related function under one point of accountability. Integrated FM deployments often embed IoT gateways and CMMS platforms by default, a cost few in-house teams can justify.

Outsourcing momentum is reinforced by regulatory stakes: climate disclosures, modern slavery rules, and Indigenous participation targets all require specialised reporting frameworks. Providers pitch outcome-based compensation tied to energy and uptime metrics, shifting financial risk from asset owners to FM partners. The model resonates with PPP sponsors, health networks, and global corporate tenants aiming to benchmark portfolio performance across continents.

By End-User Industry: Commercial Sector Leads Digital Adoption

Commercial real estate held 37.05% of the Australia facility management market share in 2025 thanks to premium office towers, data centres, and retail complexes that demand 24/7 availability and ESG certification. High-rise stock in Sydney’s Barangaroo and Melbourne’s Docklands acts as a proving ground for AI-enabled building operating systems. Tenant amenities such as touchless access and live IAQ dashboards move from nice-to-have to lease differentiators. Meanwhile, institutional and public infrastructure grows at 3.18% CAGR to 2031, buoyed by hospital expansions and rail megaprojects that require stringent safety and asset-management regimes.

Education campuses adopt flexible classrooms and blended-learning tech, raising maintenance complexity around AV gear and occupancy-sensor networks. Transportation nodes invest in cyber-secured SCADA and CCTV upgrades, which combine physical and digital risk oversight. Industrial clients, particularly mining and advanced manufacturing, need remote monitoring and harsh-environment maintenance protocols. Hospitality and multi-housing rebound with wellness-centred refurbishments, demanding FM partners who can harmonise guest services, energy control, and waste diversion targets in one dashboard.

Geography Analysis

New South Wales leads the Australia facility management market, anchored by Sydney’s headquarters cluster and PPP pipeline. Enhanced Work Health and Safety rules raise compliance workloads and favour providers with accredited processes. The Clarence Correctional Centre adds a 25-year facilities scope to the region, creating steady demand for security, cleaning, and technical maintenance. Sydney’s smart-city ambitions spur pilots of 5G-enabled building twins and micro-grid integration.

Victoria charts robust growth through investments such as the AUD 2 billion New Footscray Hospital PPP, which obliges whole-of-life FM oversight for 25 years. Melbourne’s manufacturing and logistics spine elevates demand for industrial FM specialists, particularly as renewable-energy mandates accelerate warehouse solar installs. Cultural and sporting venues in the state require adaptable service models able to scale for events yet minimise idle-time costs. Energy price swings are pronounced for Victorian manufacturers, intensifying adoption of demand-response and on-site generation.

Queensland’s facility management sector benefits from the Logan–Gold Coast Faster Rail and Train Manufacturing Program, together exceeding AUD 6 billion, that embed integrated FM into rail depot and station operations. Tourist precincts on the Gold Coast drive refurbishment cycles focused on environmental certifications to attract international visitors. Western Australia’s market remains shaped by government maintenance frameworks and the resources sector, with Programmed’s long-running state contract underlining a preference for consolidated regional suppliers. South Australia, Tasmania, and the Northern Territory together present niche opportunities in defence, space infrastructure, and eco-tourism lodges, yet distance and thin labour pools compel heavy reliance on remote monitoring technologies.

Competitive Landscape

Competition is moderate with a tendency toward consolidation as clients consolidate spend with fewer, full-service partners. International majors—ISS, Sodexo, Serco, CBRE—vie alongside domestic operators Ventia, Spotless, and Programmed. The ACCC’s 2024 cartel action against Ventia and Spotless over Defence base contracts underlines the high stakes in federal tenders and raises compliance scrutiny across the field. Technology investment is the prime differentiator; CBRE’s new Building Operations & Experience division pools facilities, property, and workplace services into a USD 20 billion revenue stream supported by unified data platforms.

Providers build in-house analytics hubs and strike alliances with software vendors to embed real-time asset health dashboards into client portals. ESG credentials are now standard bid requirements, pushing firms to quantify carbon reduction delivered through retrofits or electrification projects. Indigenous procurement quotas in government contracts spur joint ventures with First Nations enterprises, reshaping subcontracting structures. Smaller, regionally focused companies survive by specialising in heritage-listed sites, remote mining camps, or high-security defence locations where large corporates lack local depth.

M&A activity remains brisk as firms seek scale and niche capabilities. CBRE’s acquisition of J&J Worldwide Services expands defence facilities coverage and deepens engineering competencies, while ISS targets healthcare and mining verticals through multi-year contract extensions. Investors view AI-powered maintenance platforms as growth multipliers, prompting private-equity interest in mid-tier specialists with proprietary software. Entry barriers—state licensing, union agreements, and capital-intensive technology—protect incumbent positions yet simultaneously slow disruptive entrants.

Australia Facility Management Industry Leaders

ISS Australia

Sodexo Facilities Management Services

Australia Facilities Management

Ventia Services Group

Serco Facilities Management

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CBRE Group announced the creation of its Building Operations & Experience segment following the acquisition of Industrious National Management Company, unifying enterprise, local, and property management services to generate about USD 20 billion in revenue.

- December 2024: The ACCC filed civil cartel proceedings against Spotless Facility Services and Ventia Australia for alleged price fixing on Defence estate maintenance contracts.

- October 2024: ISS secured a multi-year extension at Roy Hill’s mining operation in Western Australia, adding sustainability initiatives and data-driven maintenance to its integrated scope.

- October 2024: ISS celebrated 25 years with SA Health, highlighting expansion across multiple hospitals and the launch of South Australia’s largest vaccination hub.

Australia Facility Management Market Report Scope

Facility management confines multiple disciplines to ensure functionality, comfort, safety, and efficiency of any building by integrating people, place, process, and technology. While Hard services include physical and structural services like fire alarm system lifts, among others, soft services include cleaning, landscaping, security, and similar human-sourced services, providing a solution to end-users such as Commercial Buildings, Retail, Government, Public Entities, etc.

The Australia facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Region

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| Rest of Regions |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Region | New South Wales | |

| Victoria | ||

| Queensland | ||

| Western Australia | ||

| Rest of Regions | ||

Key Questions Answered in the Report

What is the projected size of the Australia facility management market by 2031?

The Australia facility management market size is forecast to reach USD 37.36 billion by 2031.

Which service category currently dominates the market?

Hard services, covering HVAC, MEP, and safety systems, commanded 58.74% of market share in 2025.

Why are outsourced models gaining traction?

Outsourced models offer expert regulatory compliance, advanced analytics, and lifecycle asset management that many organisations cannot achieve with in-house teams.

How are energy price fluctuations affecting facility management contracts?

Volatile tariffs complicate guaranteed-savings clauses, prompting FM providers to include energy-risk-sharing models and renewable energy solutions in contracts.

Which end-user segment is expanding fastest through 2031?

Institutional and public infrastructure facilities, buoyed by government rail and hospital projects, are projected to grow at a 3.18% CAGR.

Page last updated on: