Asia-Pacific Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

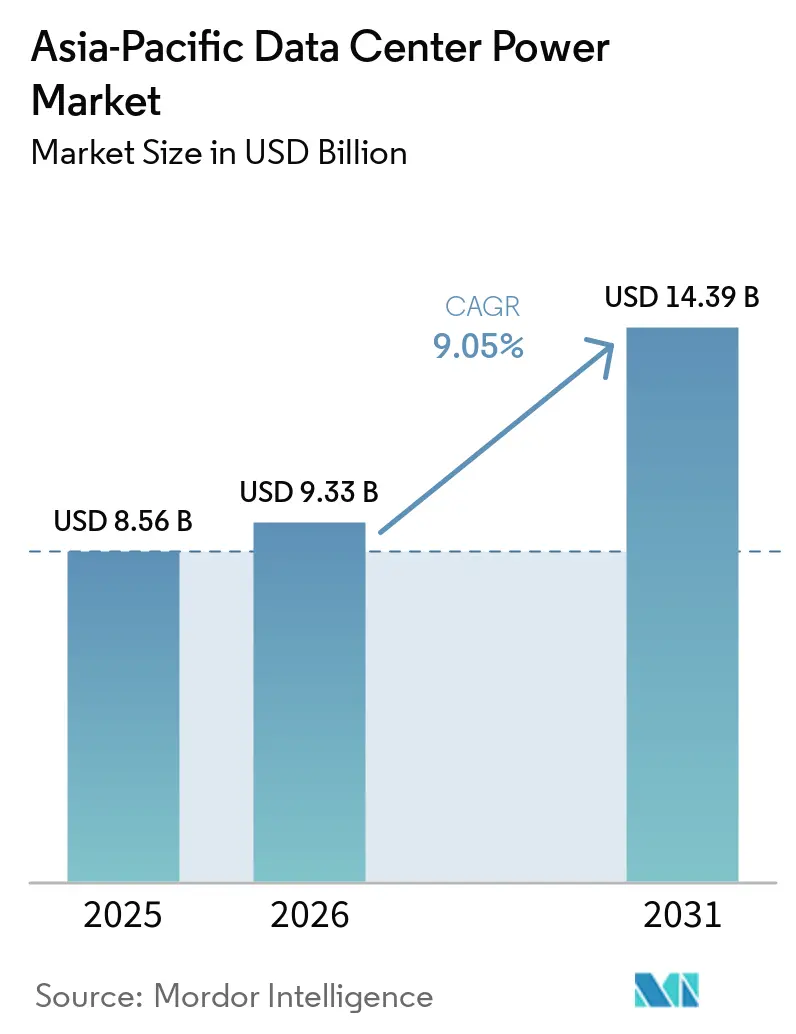

| Base Year Market Size (2025) | USD 8.56 Billion |

| Market Size (2026) | USD 9.33 Billion |

| Market Size (2031) | USD 14.39 Billion |

| Growth Rate (2026 - 2031) | 9.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Data Center Power Market Analysis by Mordor Intelligence

The Asia-Pacific data center power market size was valued at USD 8.56 billion in 2025 and estimated to grow from USD 9.33 billion in 2026 to reach USD 14.39 billion by 2031, at a CAGR of 9.05% during the forecast period (2026-2031). Rapid hyperscale campus construction, sovereign AI programs and rising rack densities that routinely exceed 40 kW are driving sustained equipment demand. Governments across China, India and Singapore link digital-economy goals to local infrastructure, which lifts long-term investment visibility. At the same time, electricity prices in mature hubs such as Singapore and Japan keep operator focus on high-efficiency UPS, intelligent PDUs and on-site battery energy storage. Supply-chain headwinds for copper and semiconductors persist, yet domestic manufacturing expansions by major vendors are shortening lead times and supporting project schedules.

Key Report Takeaways

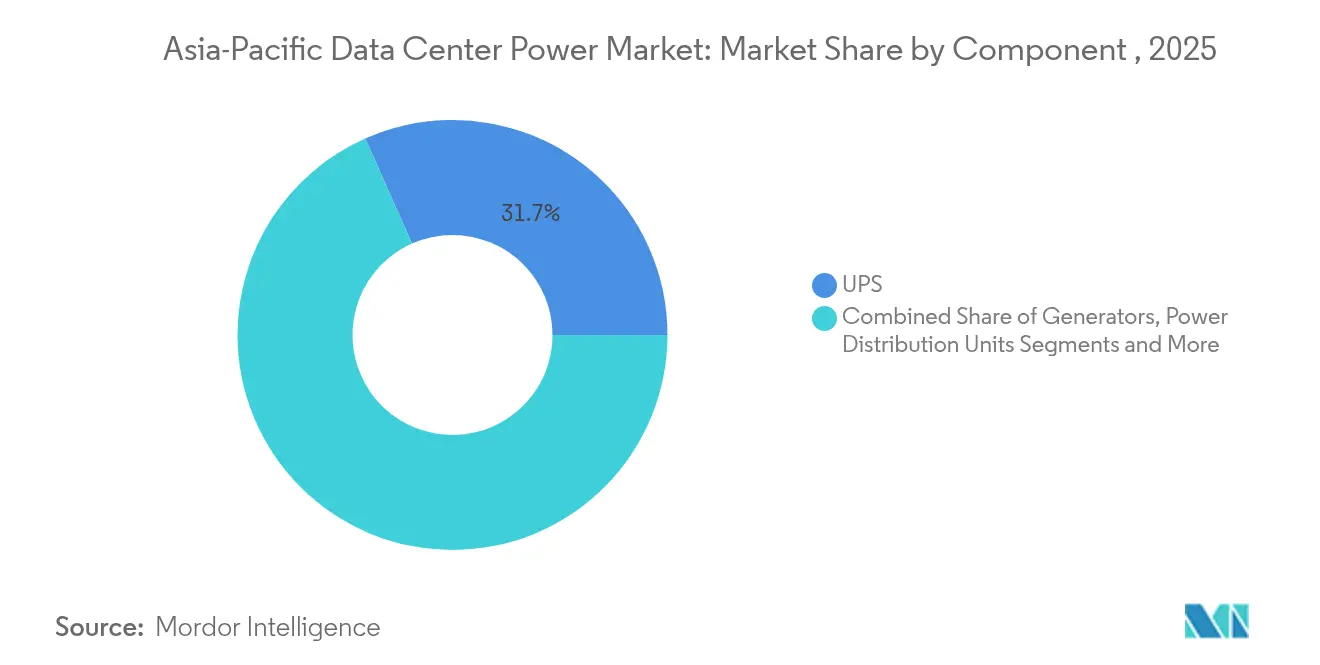

- By component, UPS systems led with 31.65% revenue share in 2025, while power distribution units are projected to expand at a 10.3% CAGR through 2031.

- By data center type, colocation providers held 53.85% of the Asia-Pacific data center power market share in 2025; hyperscale providers are advancing at a 10.05% CAGR to 2031.

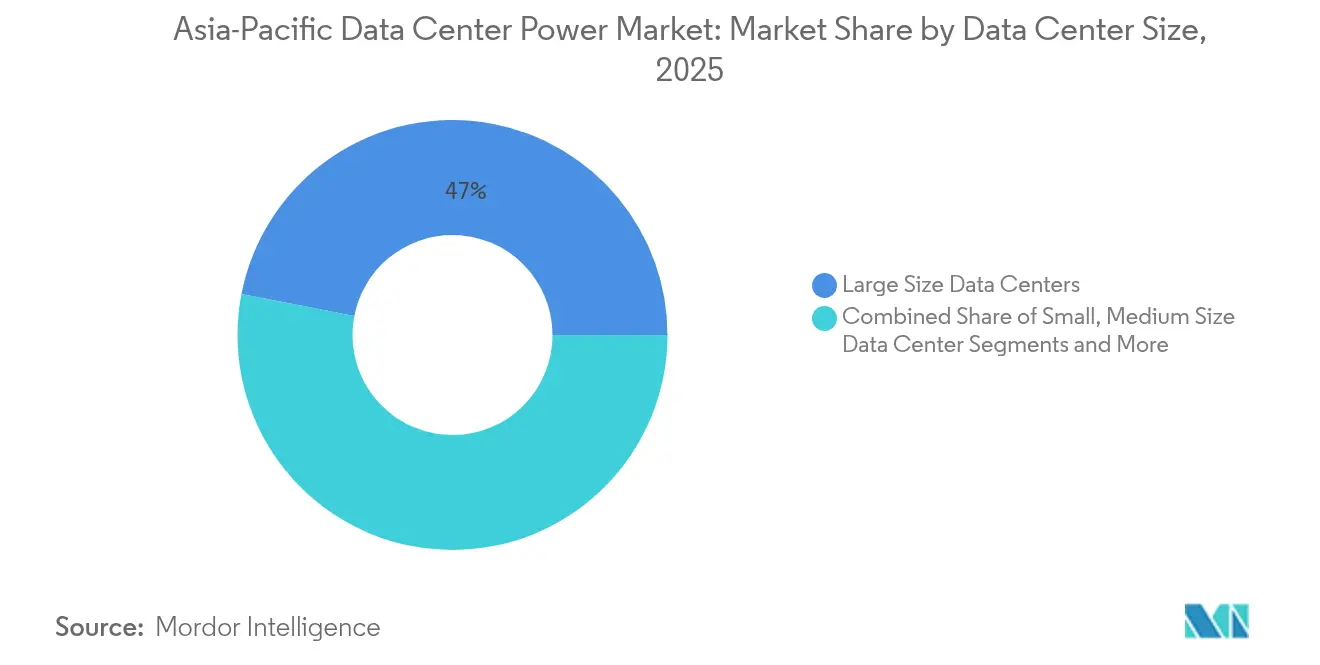

- By size, large facilities accounted for 46.95% of the Asia-Pacific data center power market size in 2025, whereas mega-scale sites will grow at an 10.95% CAGR.

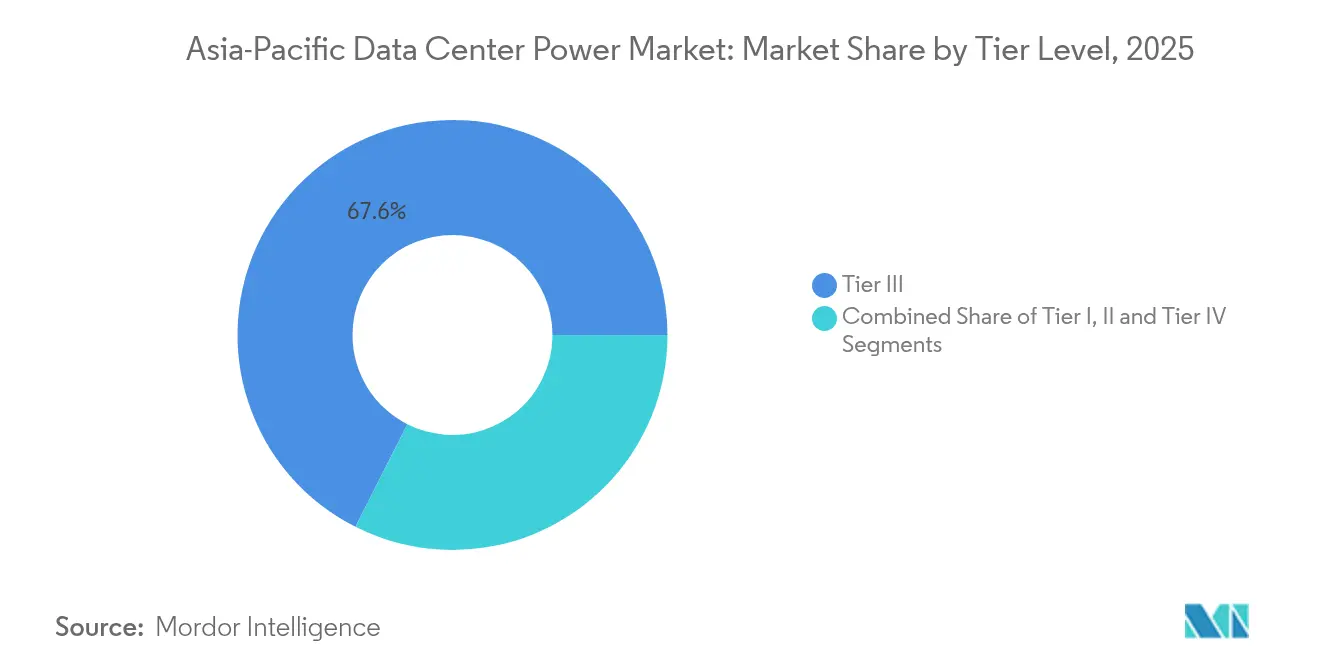

- By tier, Tier III facilities dominated with a 67.55% share in 2025, while Tier IV deployments are growing at a 11.35% CAGR.

- By country, China led with 23.10% share in 2025 and India is forecast to record an 11.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale & AI-led mega-campus build-out | +2.8% | China, India, Singapore, Japan | Medium term (2-4 years) |

| Government digital-economy & data-sovereignty incentives | +1.9% | APAC core, spill-over to ASEAN | Long term (≥ 4 years) |

| Cloud/5G traffic surge elevating power density | +2.1% | Global, concentrated in urban APAC hubs | Short term (≤ 2 years) |

| High electricity tariffs boosting demand for efficient UPS & PDUs | +1.4% | Singapore, Japan, Australia | Medium term (2-4 years) |

| Grid-connection delays driving onsite micro-grids | +1.1% | Tier-1 APAC cities, high-density markets | Short term (≤ 2 years) |

| Corporate 100%-renewable commitments (on-site solar + BESS) | +1.3% | Global, led by multinational corporations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale & AI-led Mega-Campus Build-out

AI training clusters now demand 40-50 kW per rack, more than five times traditional deployments, forcing total redesigns of distribution topologies and redundancy schemes. [1]Digital Realty, “AI Workloads and Data Center Design,” digitalrealty.comWide-bandgap power semiconductors such as silicon carbide reduce conversion losses, while liquid cooling becomes standard in new halls to maintain thermal stability, Oak Ridge National Laboratory. Projects like Singtel’s Banyan Park II in Singapore specify seismic-resilient busways and rack-level liquid manifolds to future-proof against higher AI loads. These systems integrate battery storage for ride-through support, smoothing grid transients, and enabling more aggressive load step changes without generator starts. The cascading effect raises specification levels across colocation builds as tenants request AI-ready capacity.

Government Digital-Economy & Data-Sovereignty Incentives

Policies in China and India require domestic data residency, obliging cloud providers to commission local hyperscale campuses and upgrade power distribution for higher availability tiers. Singapore’s public–private research program with Equinix funds USD 4 million in sustainable power prototypes targeting tropical operating conditions.[2]Equinix, “Equinix and NUS Launch Co-Innovation Facility,” equinix.com ASEAN frameworks encourage renewable integration that could meet 30% of data-center demand by 2030. Incentive schemes in Malaysia and Vietnam grant tariff rebates for facilities that deploy on-site solar and high-efficiency UPS. As regulation sets clear procurement timelines, volume commitments for switchgear and energy storage rise, supporting predictable supply-chain scaling.

Cloud/5G Traffic Surge Elevating Power Density

5G rollout accelerates edge nodes and pushes more packet processing into data centers, raising average electrical load per square meter. Colocation operators retrofit older halls with higher-capacity busways and modular lithium-ion strings to cope with unpredictable step loads from virtualized network functions.[3]Cummins, “Battery Energy Storage for Data Centers,” cummins.com Edge racks in urban micro-facilities rely on compact DC power shelves that integrate UPS, monitoring and automatic transfer in a single frame. Grid capacity constraints in Hong Kong and Tokyo spur battery-based peak-shaving so operators avoid costly demand-charge spikes. Together these factors compress traditional reserve margins and elevate specification baselines for intelligent PDUs and branch-circuit monitoring.

High Electricity Tariffs Boosting Demand for Efficient UPS & PDUs

Industrial electricity costs in Singapore and Japan top USD 0.17 per kWh, so a 1% conversion-loss improvement can save tens of thousands of dollars annually for a 10 MW facility. Modern UPS designs achieve 96–97% online efficiency and incorporate eco-mode algorithms that raise full-load performance during off-peak periods. Intelligent PDUs measure per-outlet energy, allowing AI-assisted workload placement that balances heat output and defers new air-handling units. Time-of-use tariffs in Australia make lithium-ion storage attractive for load shifting, underpinning combined UPS-plus-battery systems that defend against both outages and tariff spikes. Government rebate programs on high-efficiency equipment additionally compress payback cycles, hastening refresh decisions.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front capex for high-efficiency power systems | -1.2% | APAC emerging markets, cost-sensitive deployments | Short term (≤ 2 years) |

| Grid & land constraints in Tier-1 APAC hubs | -1.8% | Singapore, Hong Kong, Tokyo, Sydney | Medium term (2-4 years) |

| Diesel-price volatility inflating generator OPEX | -0.9% | Global, particularly remote APAC locations | Short term (≤ 2 years) |

| Skilled-labour gap for liquid-cooling power installs | -0.7% | APAC core markets, emerging technology deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-front Capex for High-Efficiency Power Systems

Advanced UPS and silicon-carbide converters cost up to 40% more than legacy equipment, a hurdle for smaller providers with constrained balance sheets. Liquid-cooling integration demands factory-prefabricated busbar and pump manifolds, raising installation complexity and lead times. In emerging economies where average rack loads still hover near 8 kW, operators often delay upgrades until customer demand materializes. Financing mechanisms such as energy-as-a-service contracts are beginning to spread, but adoption remains uneven, limiting near-term penetration of the most efficient architectures.

Grid & Land Constraints in Tier-1 APAC Hubs

Land scarcity in Singapore and Hong Kong limits greenfield plots, forcing vertical builds that complicate high-capacity transformer placement. Local utilities impose multi-year queues for new substation connections that exceed 50 MW, delaying project timelines. Operators respond with on-site micro-grids that combine solar canopies and battery storage, yet these solutions raise capex and engineering complexity. In Tokyo, seismic codes drive heavier structural designs, further tightening floor-space budgets available for switchgear rows. Such constraints slow the rollout of new capacity despite strong underlying demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Intelligent Distribution Drives Growth

UPS systems held the largest 31.65% revenue share in 2025 within the Asia-Pacific data center power market, underscoring their role in safeguarding always-on digital services. Adoption of lithium-ion batteries and silicon-carbide power trains pushes online efficiency above 96%, trimming operating expenditures despite higher unit prices. The component mix is changing as integrated UPS-battery modules reduce footprint and simplify maintenance. Intelligent PDUs, the fastest-growing sub-segment with a 10.3% CAGR, embed per-outlet metering that feeds AI analytics for workload placement, reducing stranded power capacity. Generators retain critical backup status but fuel-cell prototypes are gaining pilot traction among sustainability-focused hyperscalers.

External pressures from electricity-price volatility accelerate the deployment of battery energy storage that doubles as ride-through support and demand-charge mitigation. Switchgear advances concentrate on arc-flash safety and remote diagnostics that lower truck rolls. Remote power panels rise in edge deployments where technicians are scarce and uptime tolerance is low. Service revenue grows as operators contract OEMs for predictive maintenance tied to digital twins, reflecting the rising complexity of modern power trains across the Asia-Pacific data center power industry.

By Data Center Type: Colocation Dominance Meets Hyperscale Expansion

Colocation operators commanded 53.85% of the Asia-Pacific data center power market in 2025 by aggregating enterprise demand and leveraging economies of scale. Their business model supports large multitenant halls where modular 2–3 MW blocks standardize power design and shorten build schedules. Hyperscale cloud providers, however, are expanding at 10.05% CAGR as sovereign-cloud mandates drive local build commitments from global platforms. These sites integrate high-density AI clusters, necessitating direct-to-chip liquid cooling and dedicated 400 VAC busways that traditional colocation layouts rarely accommodate.

Enterprises adopt hybrid architectures, retaining latency-sensitive workloads on-premises while renting burst capacity from colo and hyperscale platforms. Edge nodes proliferate near 5G towers, requiring compact yet highly reliable power shelves that share design DNA with large facilities. Consequently, solutions vendors tailor portfolios that span kilowatt-class edge racks to 150 MW hyperscale farms, reinforcing cross-segment technology transfer within the Asia-Pacific data center power market.

By Data Center Size: Scale Pursuit Intensifies

Large facilities between 10 MW and 30 MW captured 46.95% of 2025 revenue as they balance capital efficiency with manageable engineering complexity. Their design typically employs N+1 generator redundancy and centralized battery rooms that suit mixed-tenant occupancy. Mega-scale sites above 30 MW will post the fastest 10.95% CAGR, reflecting hyperscalers’ preference for contiguous blocks exceeding 50 MW to optimize network cabling, cooling distribution and renewable procurement. At this magnitude, operators deploy 110 kV dedicated substations and consider direct-current distribution to minimize conversion stages, boosting the Asia-Pacific data center power market size for high-voltage equipment lines.

Small and medium data centers remain essential in regional cities where fiber latency to core metros exceeds application tolerances. Yet their share steadily erodes as software-defined interconnection lets enterprises tap large multi-region campuses with sub-5 ms latency for most workloads. The scale shift rewards vendors able to pre-fabricate power rooms and ship containerized switchgear that compress commissioning schedules by months.

By Tier Level: Reliability Spectrum Widens

Tier III facilities dominate with 67.55% share due to their balanced cost-to-availability ratio that suits most enterprise SLAs. They feature dual power paths and concurrent maintainability, enabling scheduled maintenance without shutdown. Tier IV, growing at 11.35% CAGR, requires fault-tolerant architectures with 2N distribution, making them the choice for AI inference clusters and trading platforms where downtime penalties dwarf capital premiums. Their adoption lifts average spend per MW on UPS, switchgear and battery capacity, raising the Asia-Pacific data center power market size for high-redundancy gear.

Operators increasingly blend tier concepts, pairing Tier IV electrical with Tier III mechanical to control capex while meeting uptime goals. Edge micro-sites often remain Tier II but integrate fast-start lithium batteries that offset generator runtime, showing how tier requirements evolve with technology advances.

Geography Analysis

China accounted for 23.10% of 2025 revenue, supported by domestic cloud giants and government targets that mandate PUE below 1.3 in new builds. Its ecosystem benefits from local switchgear and PDU production, though advanced semiconductor availability remains tight. India is the fastest-growing geography at an 11.1% CAGR as data-localization rules compel hyperscalers and fintechs to launch regional campuses. Schneider Electric’s double-digit sales growth underscores robust demand for integrated power-cooling bundles. Japan, Singapore and Australia follow with steady mid-single-digit expansion tied to high reliability standards and rising AI investments.

Indonesia, Malaysia and the Philippines data center power market form emerging tier where supportive policy and rising cloud adoption drive fresh greenfield activity, often on campuses exceeding 100 MW. Differences in grid reliability shape equipment mix: markets with unstable supply favor oversized battery storage and frequent generator testing, influencing purchase patterns across the Asia-Pacific data center power industry.

Competitive Landscape

Competitive intensity is moderate. Schneider Electric, Vertiv, ABB and Eaton together hold a solid share yet face growing competition from Huawei Digital Power and Delta Electronics that blend aggressive pricing with localized support. Vertiv expanded its Pune factory to increase switchgear and UPS output, cutting lead times for regional customers and supporting large hyperscale roll-outs.

Technology convergence drives differentiation. Leading vendors embed battery analytics and PDU metering into single dashboards, leveraging AI to predict failure modes and optimize energy use. Patent activity around silicon-carbide inverter topologies and modular battery strings keeps barriers to entry moderate. Partnerships between OEMs and operators co-develop site-specific architectures such as DC busways and hydrogen-ready generators, strengthening vendor lock-in.

Local manufacturers capture adjacent niches. Japanese firms supply seismic-rated panels, while Australian integrators specialize in remote-area micro-grids tied to renewable farms. Market entrants that focus on hydrogen fuel-cell modules or prefab power rooms can win share in sustainability-driven RFPs, though brand trust and global service footprints remain decisive in Tier IV bids within the Asia-Pacific data center power market.

Asia-Pacific Data Center Power Industry Leaders

ABB

Schneider Electric

Vertiv

Eaton

Caterpillar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Schneider Electric reported 9.3% organic revenue growth in Asia Pacific during Q1 2025, driven by colocation demand and cooling-solution traction.

- March 2025: Vertiv posted 24% higher net sales, with Asia-Pacific up 36% year-on-year and new manufacturing capacity added in Pune, India.

- November 2024: Equinix and the National University of Singapore opened a USD 4 million Co-Innovation Facility for sustainable data-center power research.

- October 2024: Singtel and Hitachi agreed to co-develop AI-ready data centers in Japan featuring green power systems.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Asia-Pacific data center power market as all revenue generated from electrical infrastructure, uninterruptible power supply systems, generators, switchgear, intelligent power distribution units, transfer switches, remote power panels, and associated installation or maintenance services used inside purpose-built, colocation, cloud, edge, and enterprise data centers across fifteen APAC economies.

Scope Exclusions: Stand-alone battery energy storage projects that are not integrated with data center facilities remain outside our scope.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

- By Country

- Australia

- China

- India

- Indonesia

- Philippines

- Singapore

- Malaysia

- Japan

- New Zealand

- Other Asia-Pacific Countries

Detailed Research Methodology and Data Validation

Primary Research

Subsequently, we hold structured interviews with facility design engineers, colocation procurement heads, generator OEM product managers, and regional power utility officers across China, India, Japan, Australia, and key ASEAN hubs. Their insights refine utilization factors, service attach rates, and discount trajectories, filling gaps left by desk research and confirming early assumptions.

Desk Research

Our analysts first collect foundational statistics from neutral public platforms such as UN Comtrade customs data, national energy regulators, the International Energy Agency, and trade bodies like the Asia Cloud Computing Association. We widen the net with corporate filings, quarterly results, investor decks, and reputable news feeds gathered through Dow Jones Factiva. Government procurement portals and Volza shipment records help us gauge incoming volumes of UPS frames and diesel gensets, while Questel patent trends reveal emerging high-density PDU designs. These sources anchor historical demand curves and price corridors before any modeling begins. The listed sources are illustrative; many additional references inform data capture, validation, and clarifications.

Market-Sizing & Forecasting

We build a blended model: a top-down capacity reconstruction using installed IT load (MW) and median electrical infrastructure spend per MW, corroborated with selective bottom-up supplier roll-ups and sampled ASP × shipment checks. Core variables include hyperscale campus pipeline (MW), tier III/IV penetration, average rack density, regional electricity tariffs, and energy efficiency mandates. Multivariate regression projects each driver, while scenario analysis tests grid constraint and renewable supply sensitivities. Where bottom-up estimates are patchy, ratios from nearest proxy markets are applied and then adjusted through expert feedback.

Data Validation & Update Cycle

Outputs pass variance checks against independent capacity trackers and utility sales; anomalies trigger rework before sign-off. Reports refresh annually, with interim updates after material policy or M&A events; a final analyst sweep ensures clients receive the latest view.

Why Mordor's APAC Data Center Power Baseline Commands Reliability

Published numbers often differ because studies vary in component coverage, base years, and refresh pace.

By selecting a 2025 baseline, including service revenue, and updating every twelve months, Mordor offers a decision-ready midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.56 Bn (2025) | Mordor Intelligence | |

| USD 5.09 Bn (2024) | Regional Consultancy A | Excludes services, omits edge facilities, older base year |

| USD 5.80 Bn (2024) | Global Consultancy B | Limited country set and lower hyperscale uptake rate |

Taken together, the comparison shows that Mordor's disciplined scope selection, timely refresh, and mixed method modeling yield a balanced, transparent baseline that stakeholders can trace back to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

How big is the Asia-Pacific Data Center Power Market?

The Asia-Pacific Data Center Power Market size is expected to reach USD 9.33 billion in 2026 and grow at a CAGR of 9.05% to reach USD 14.39 billion by 2031.

What is the current Asia-Pacific Data Center Power Market size?

In 2026, the Asia-Pacific Data Center Power Market size is expected to reach USD 9.33 billion.

Who are the key players in Asia-Pacific Data Center Power Market?

ABB Ltd, Caterpillar Inc., Cummins Inc., Generac Power Systems, Inc. and Kohler Co. are the major companies operating in the Asia-Pacific Data Center Power Market.

What years does this Asia-Pacific Data Center Power Market cover, and what was the market size in 2025?

In 2025, the Asia-Pacific Data Center Power Market size was estimated at USD 9.33 billion. The report covers the Asia-Pacific Data Center Power Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Asia-Pacific Data Center Power Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: