Hong Kong Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

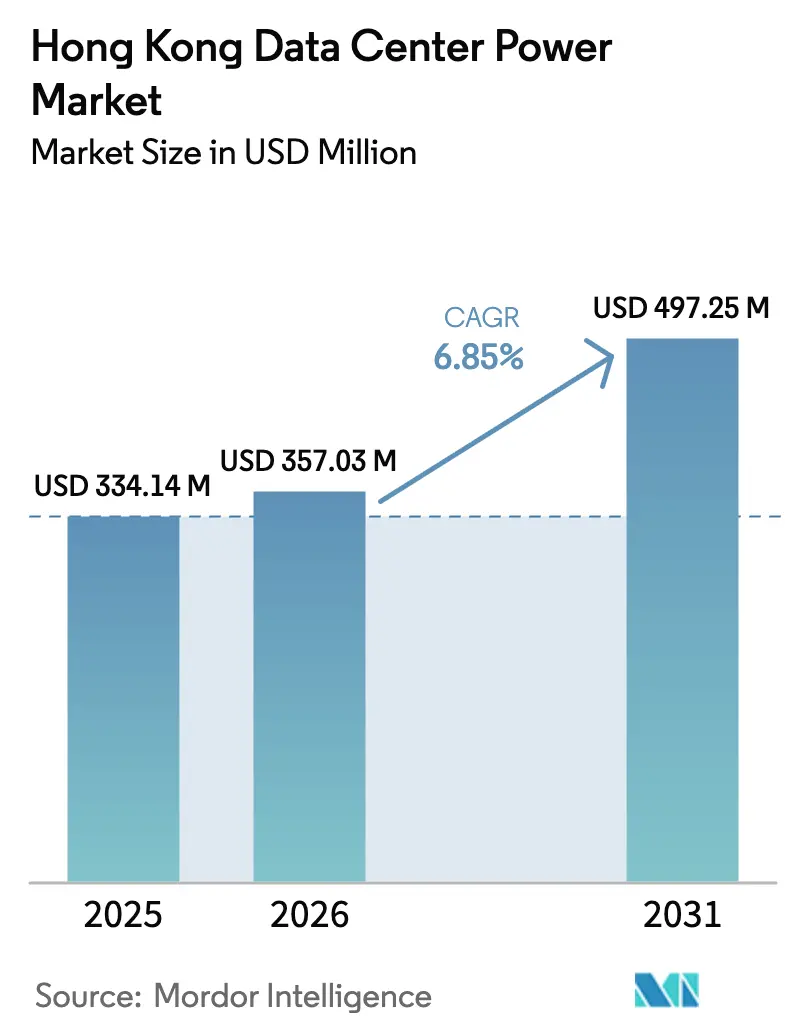

| Base Year Market Size (2025) | USD 334.14 Million |

| Market Size (2026) | USD 357.03 Million |

| Market Size (2031) | USD 497.25 Million |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Data Center Power Market Analysis by Mordor Intelligence

The Hong Kong data center power market size is expected to grow from USD 334.14 million in 2025 to USD 357.03 million in 2026 and is forecast to reach USD 497.25 million by 2031 at 6.85% CAGR over 2026-2031. Expansion is fueled by hyperscale cloud deployments, the government’s 3,000 petaflops AI Supercomputing Centre, and mission-critical demand from the banking and insurance sector. Operators continue to invest despite land scarcity because Hong Kong offers unparalleled cross-border latency advantages for workloads tied to mainland China. Reliability also remains a differentiator: utilities report an annual average of just 2.6 minutes of unplanned outages, prompting sustained uptake of high-efficiency UPS systems. Meanwhile, the transition to renewable energy and the China Southern Grid interconnection are prompting upgrades to switchgear and storage so facilities can blend grid and green power. As a result, the Hong Kong data center power market is expected to remain one of the fastest-growing power equipment segments in Asia-Pacific through 2030

Key Report Takeaways

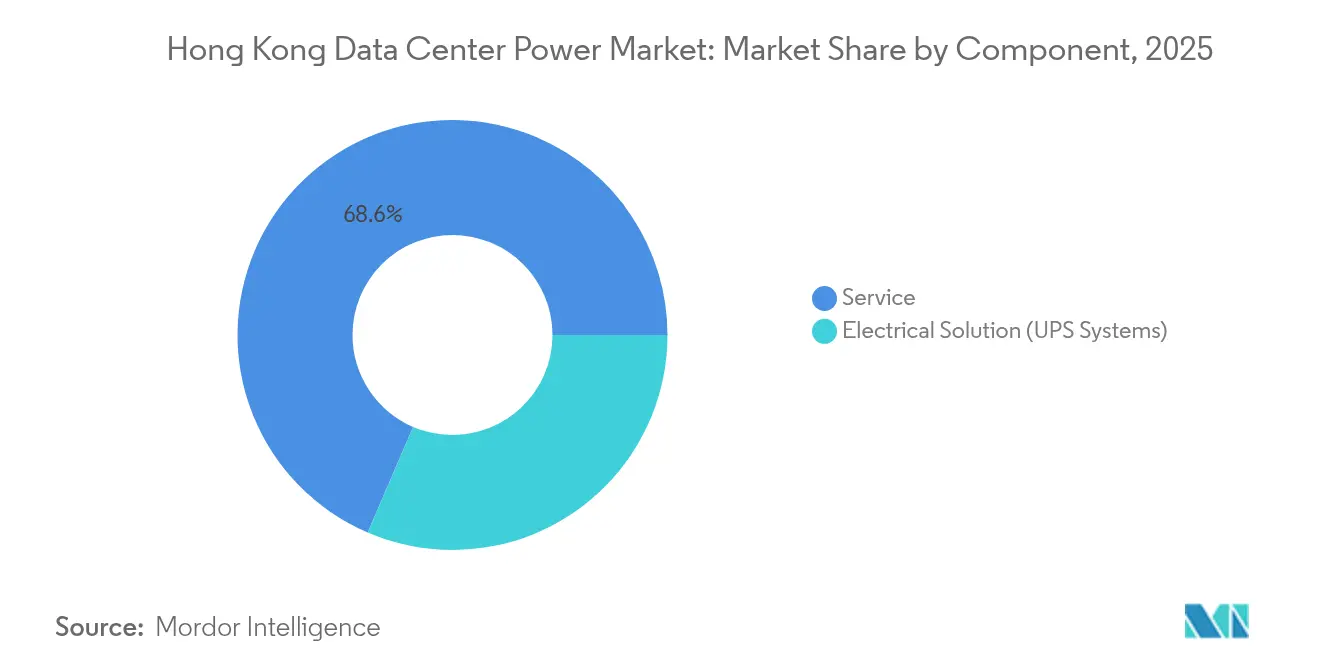

- By component, UPS systems led with 31.45% of Hong Kong data center power market share in 2025; intelligent PDUs will grow fastest at a 9.65% CAGR to 2031.

- By data center type, colocation providers held 53.80% revenue share of the Hong Kong data center power market in 2025, while hyperscale/cloud providers are projected to expand at an 10.65% CAGR through 2031.

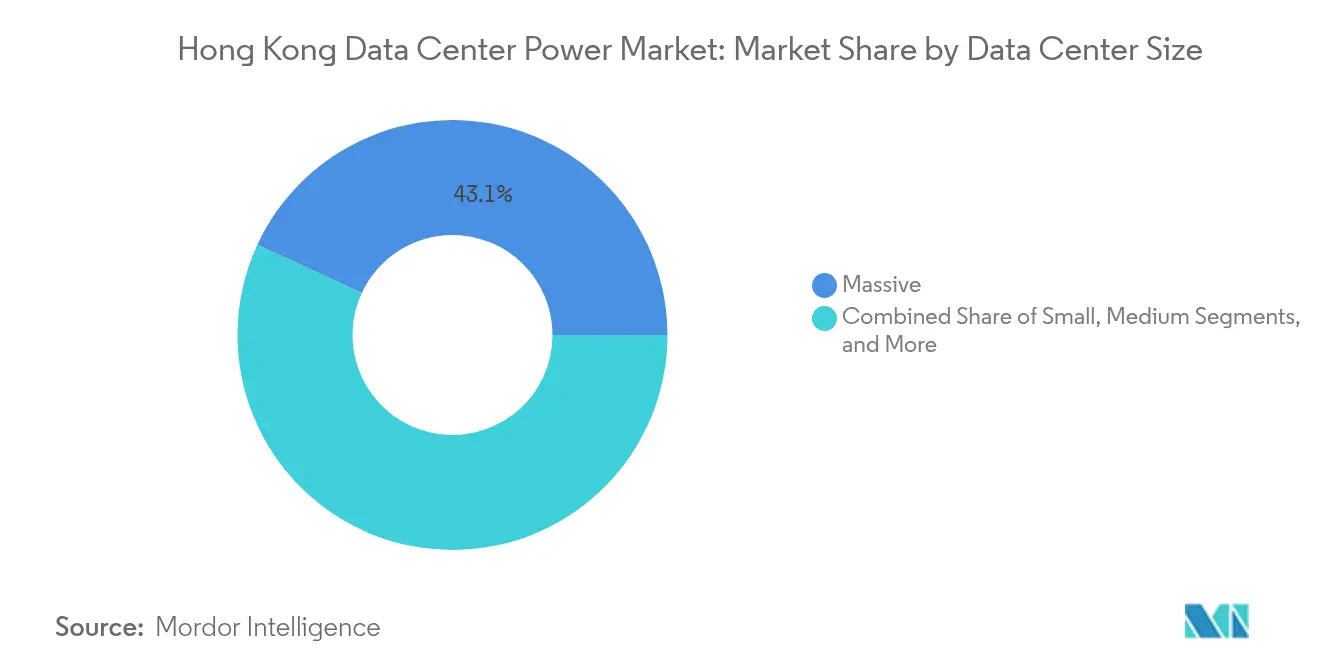

- By size, massive facilities accounted for 43.10% share of the Hong Kong data center power market size in 2025; mega-scale sites are poised to rise at a 11.9% CAGR between 2026-2031.

- By tier level, Tier 3 installations captured 50.55% of the Hong Kong data center power market share in 2025, whereas Tier 4 is forecast to grow at a 8.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong Kong Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscale and cloud adoption | +1.8% | Hong Kong SAR, with spillover to Greater Bay Area | Medium term (2-4 years) |

| Hong Kong AI-supercomputing initiatives | +1.2% | Hong Kong SAR, Northern Metropolis development zones | Long term (≥ 4 years) |

| Mission-critical uptime demand from BFSI | +0.9% | Hong Kong SAR, Central and Admiralty financial districts | Short term (≤ 2 years) |

| Transition toward renewable/green power | +0.7% | Hong Kong SAR, with mainland China grid connections | Long term (≥ 4 years) |

| Cross-border grid interconnection with China Southern Grid | +0.5% | Hong Kong SAR, Guangdong Province border areas | Medium term (2-4 years) |

| Adoption of modular Li-ion UPS and fuel-cell gensets in high-rise DCs | +0.4% | Hong Kong SAR, Tseung Kwan O and Kwai Chung clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in hyperscale and cloud adoption

Hyperscale operators have doubled confirmed capacity pipelines from 317 MW in 2023 to 700 MW, compelling local providers to raise rack densities and deploy high-efficiency switchgear that can serve AI clusters exceeding 30 kW per rack.[1]Cushman & Wakefield, Asia Pacific Data Centre Update 2024, cushmanwakefield.com Vacancy has tightened to 21% as Microsoft and other cloud majors reroute canceled Western builds into Asia, raising demand for fast-to-deploy prefabricated power rooms. Financing rounds such as BDx’s 2025 issuance illustrate capital momentum behind this scale-out

Hong Kong AI-supercomputing initiatives

The new 3,000 petaflops center at Cyberport and a second planned facility at Sandy Ridge will concentrate GPU-rich workloads that require redundant 100 MVA feeds and liquid-cooled busways.[2]Zen Soo, South China Morning Post, scmp.com Government outlays exceeding HKD 150 billion since 2018 have signaled long-term policy support, encouraging manufacturers to localize high-density UPS skids and immersion-ready battery cabinets

Mission-critical uptime demand from BFSI

Financial exchanges settling HKD 33 trillion in listed equity value rely on 99.99% service levels, driving multistack redundancy with N+2 diesel plus dual Li-ion strings.[3]Hong Kong Government Information Services, info.gov.hk Equinix maintains 35 diesel gensets and purpose-built trading rooms that can fail-over without human intervention

Transition toward renewable and green power

HK Electric plans to phase out coal by the early 2030s and target 4% offshore-wind contribution by 2027, prompting operators to specify PCS-based storage and dynamic transfer switches for mixed-source loads. SUNeVision now offsets a portion of campus demand through renewable energy certificates purchased from CLP.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and maintenance cost | -0.8% | Hong Kong SAR, particularly Central and premium locations | Short term (≤ 2 years) |

| Sky-high Hong Kong real-estate prices | -1.1% | Hong Kong SAR, with acute impact in urban core areas | Long term (≥ 4 years) |

| Extra-territorial data–security rules dampening FDI | -0.6% | Hong Kong SAR, affecting international operators | Medium term (2-4 years) |

| Sub-station approval delays due to land scarcity | -0.9% | Hong Kong SAR, development zones and industrial areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High installation and maintenance cost

Power tariffs rose 6.8% for HK Electric customers in 2025, and stringent electrical codes lengthen commissioning cycles, pushing lifecycle costs well above regional peers. LEED Platinum builds require premium materials and specialist labor, elevating capex for operators targeting sustainability-conscious tenants

Sky-high Hong Kong real-estate prices

Only two land parcels remain zoned for data center use, and bureaucracy means projects average eight years from tender to launch, locking in rent escalations that curb new-build economics. SUNeVision’s MEGA Plus campus illustrates how exclusive government lots give incumbents a structural edge over new entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems Lead Infrastructure Modernization

UPS systems held 31.45% of 2025 spending, reflecting non-negotiable uptime benchmarks set by Hong Kong’s clearinghouses and digital banks. Lithium-ion racks replace valve-regulated lead-acid batteries in high-rise rooms, cutting floor loading and extending cycle life. Schneider Electric’s Galaxy VXL, co-engineered with NVIDIA, ships in 2025 with AI-ready load profiles suitable for 30 kW GPU racks. Generators retain relevance, yet hydrogen pilots from Hitachi Energy signal a shift toward zero-carbon standby.

Intelligent PDUs are expected to post a 9.65% CAGR through 2031 as operators seek granular consumption data to satisfy ESG reporting. Remote power panels are gaining favor in multi-story builds where vertical bus risers feed separate halls. As renewable penetration rises, hybrid flywheel-battery strings and bidirectional inverters will become baseline specifications.

By Data Center Type: Colocation Dominance Faces Hyperscale Challenge

Colocation accounted for 53.80% revenue in 2025, leveraging carrier neutrality and 180+ submarine cable landings to attract regional SaaS and fintech tenants. The Hong Kong data center power market size for colocation surpassed USD 179.7 million in 2025, expanding at a steady 5.75% CAGR. Hyperscale footprints, however, are growing 10.65% annually as cloud giants negotiate entire buildings under single-tenant agreements.

This shift is prompting jurisdictional competition for substation slots. Delta Electronics’ prefabricated 1.7 MW power trains shorten hyperscale deployment by four months, a critical advantage in the Hong Kong data center power market. Enterprises continue to anchor smaller suites for regulatory or latency reasons, but forward demand is decisively tilting toward cloud operators that can pre-commit 20-MW blocks.

By Data Center Size: Massive Facilities Drive Current Demand

Massive sites (10-50 MW) captured 43.10% share in 2025, translating to a Hong Kong data center power market share of nearly USD 144 million that year. These campuses balance land scarcity with economies of scale by stacking 12-15 stories and dedicating entire floors to electrical rooms. Cooling densities reach 2 kW/m², making inline-liquid loops common.

Mega-scale builds above 50 MW show the fastest 11.9% CAGR as hyperscale AI clusters require contiguous halls of 10,000 m² each. Operators must coordinate directly with CLP for 132 kV feeds and plan ten-year transformer roadmaps. Small and medium facilities still serve edge analytics for logistics and e-commerce, but contribute a shrinking slice of new megawatt uptake.

By Tier Level: Tier 3 Standards Meet Financial Sector Demands

Tier 3 dominated with 50.55% share in 2025, underpinning the Hong Kong data center power market size for high-availability builds that exceeded USD 168.9 million that year. Concurrent maintainability remains the golden rule for financial clients and stock exchange participants. CITIC Telecom CPC’s recent Tier 3+ site validates how N+1 topology suffices when coupled with geographically separate disaster-recovery seats.

Tier 4 is growing 8.85% per year because AI training clusters cannot tolerate even brief switchover. Fault-tolerant switchgear and dual utility pathways are becoming standard quotes for hyperscale build-to-suit projects. Lower tiers find relevance only in edge content caching and non-regulated enterprise IT, indicating that reliability remains a monetizable differentiator in Hong Kong.

Geography Analysis

Hong Kong’s industrial power corridor in Tseung Kwan O now houses one-third of total capacity, anchored by four submarine cable landing stations that cut latency to Guangzhou to under 9 ms . Dense zoning means sites stack vertically: MEGA-i delivers 1.5 kVA per standard rack across a 350,000-sq-ft footprint that once held a textile factory. High humidity and typhoon exposure necessitate IP55-rated switchboards, while seawater proximity dictates stainless steel busbar casings.

The Northern Metropolis policy unlocks brownfield plots in the New Territories, and the second AI Supercomputing Centre at Sandy Ridge will create a fresh 100 MVA pull on the grid by 2028. Cross-border feeds via the Black Point joint venture let operators tap surplus photovoltaic output from Guangdong during midday peaks, helping to satisfy the 7.5-10% renewable target for 2035. Government incentives for rooftop solar on industrial sheds further enable on-site micro-grids, although roof loading on pre-1990 slabs often requires reinforcement.

Hong Kong’s network topology integrates 17 active submarine cables and three terrestrial fiber crossings, ensuring sub-5 ms round-trip time to Shenzhen fintech clusters. Regulatory certainty under common law draws trading houses that need enforceable contracts outside mainland jurisdiction. Concurrently, the new cybersecurity bill will classify data centers as critical infrastructure from 2026, raising minimum diesel autonomy from 24 to 48 hours for Tier 3 and above. Collectively, these factors preserve Hong Kong’s status as Greater Bay Area connectivity gateway despite real-estate and land-banking limitations

Competitive Landscape

Local incumbents dominate: SUNeVision controls more than 280 MW across six campuses and benefits from exclusive government land grants reserved for high-tier data center use. Development lead times average eight years, turning land tenure and zoning expertise into formidable entry barriers. International firms such as Equinix compete on multi-cloud exchange services and boast 75-plus MW of standby generation supporting live trading floors.

Technology leadership is now a strategic wedge. Global Switch introduced direct liquid cooling in 2024 to cut PUE by 0.12 across GPU halls. CLP’s Grid-V monitoring platform layers 3,000 IoT sensors onto main substations, offering near-real-time fault analytics that colocation tenants tout in service-level contracts. Prefabricated edge pods from Huawei and Delta shorten deployment cycles for AI labs that cannot wait for multiyear builds.

Looking ahead, hyperscale self-builds could pressure wholesale rates, but limited land listings constrain how far cloud players can vertically integrate. Operators able to secure renewable PPAs or hydrogen exemptions are likely to claim ESG-oriented tenants first. Consulting-led systems integrators, meanwhile, gain relevance by steering projects through new cybersecurity audits and cross-border power-import paperwork, broadening the ancillary ecosystem supporting the Hong Kong data center power market.

Hong Kong Data Center Power Industry Leaders

Eaton Corporation.

Vertiv Group Corp.

Schneider Electric SE

Caterpillar Inc.

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hong Kong SAR confirmed a second AI Supercomputing Centre at Sandy Ridge under the Northern Metropolis blueprint, adding 3,000 petaflops of capacity

- May 2025: BDx secured fresh financing to expand its Tseung Kwan O campus, underscoring investor confidence despite land scarcity.

- March 2025: Legislative Council enacted the Protection of Critical Infrastructures (Computer Systems) Bill, imposing cybersecurity standards on data centers effective in 2026

- February 2025: CLP Power launched the AI-driven Grid-V platform for predictive maintenance across 3,000 sensors and cameras

- December 2024: Schneider Electric introduced the Galaxy VXL UPS and liquid-cooled AI cluster designs targeting 30 kW racks

- September 2024: Global Switch deployed direct liquid cooling in its Hong Kong facility to serve high-density GPU floors.

Hong Kong Data Center Power Market Report Scope

Data center power refers to the power infrastructure, including electrical components and electrical distribution systems, that provide the power necessary to operate and support the devices and servers within the data center. It includes various components and technologies designed to ensure a reliable, uninterruptible power supply for data center IT equipment, including uninterruptible power supplies (UPS), power distribution units (PDU), backup generators, and other power management solutions tailored to the specific needs of data centers. Data center operators achieve data center redundancy through duplicated components to maintain uninterrupted operations in the event of failure of some components and to maintain uptime during maintenance.

The data center power market in Hong Kong is segmented by power infrastructure (electrical solutions (UPS systems, generators, power distribution solutions [PDU, switchgear, critical power distribution, transfer switches, remote power panels, and others], and service) and end user (IT & telecommunication, BFSI, government, media & entertainment, and other end-users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Electrical Solutions | UPS Systems | |

| Generators | Diesel Generators | |

| Gas Generators | ||

| Hydrogen Fuel-cell Generators | ||

| Power Distribution Units | ||

| Switchgear | ||

| Transfer Switches | ||

| Remote Power Panels | ||

| Energy-storage Systems | ||

| Service | Installation and Commissioning | |

| Maintenance and Support | ||

| Training and Consulting | ||

| Hyperscaler/Cloud Service Providers |

| Colocation Providers |

| Enterprise and Edge Data Center |

| Small Size Data Centers |

| Medium Size Data Centers |

| Large Size Data Centers |

| Massive Size Data Centers |

| Mega Size Data Centers |

| Tier I and II |

| Tier III |

| Tier IV |

| By Component | Electrical Solutions | UPS Systems | |

| Generators | Diesel Generators | ||

| Gas Generators | |||

| Hydrogen Fuel-cell Generators | |||

| Power Distribution Units | |||

| Switchgear | |||

| Transfer Switches | |||

| Remote Power Panels | |||

| Energy-storage Systems | |||

| Service | Installation and Commissioning | ||

| Maintenance and Support | |||

| Training and Consulting | |||

| By Data Center Type | Hyperscaler/Cloud Service Providers | ||

| Colocation Providers | |||

| Enterprise and Edge Data Center | |||

| By Data Center Size | Small Size Data Centers | ||

| Medium Size Data Centers | |||

| Large Size Data Centers | |||

| Massive Size Data Centers | |||

| Mega Size Data Centers | |||

| By Tier Level | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

Key Questions Answered in the Report

What is the current value of the Hong Kong data center power market?

The market is valued at USD 357.03 million in 2026 and is projected to reach USD 497.25 million by 2031.

Which component category commands the largest share?

UPS systems lead with 31.45% of 2025 spending due to stringent uptime requirements in financial services and cloud workloads.

How fast are hyperscale data centers growing compared with colocation?

Hyperscale and cloud facilities are expected to expand at an 10.65% CAGR to 2031, outpacing colocation’s mid-single-digit growth as AI clusters drive new demand.

What is the biggest geographic cluster for facilities in Hong Kong?

Tseung Kwan O hosts roughly one-third of live capacity because it offers industrial zoning, available substations, and subsea cable landings.

How is Hong Kong addressing sustainability in data center power?

Utilities are phasing out coal, deploying offshore wind, and enabling renewable energy certificates, while operators adopt Li-ion UPS, fuel-cell gensets, and direct liquid cooling to cut emissions.

Why do most facilities aim for Tier 3 certification?

Tier 3 offers concurrent maintainability with 99.982% uptime, balancing reliability and capex, which suits the financial exchanges and banks that dominate Hong Kong’s tenant mix.

Page last updated on: