Asia-Pacific Automotive Plastics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

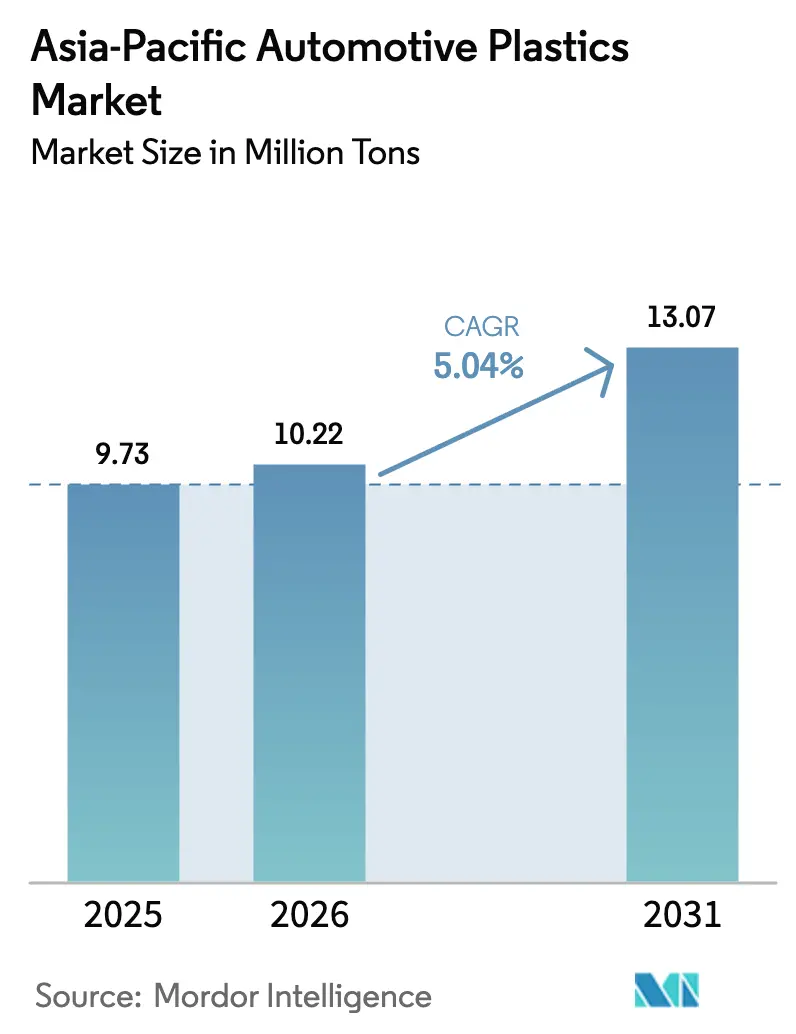

| Base Year Market Size (2025) | 9.73 Million tons |

| Market Volume (2026) | 10.22 Million tons |

| Market Volume (2031) | 13.07 Million tons |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Automotive Plastics Market Analysis by Mordor Intelligence

Asia-Pacific Automotive Plastics Market size in 2026 is estimated at 10.22 Million tons, growing from 2025 value of 9.73 Million tons with 2031 projections showing 13.07 Million tons, growing at 5.04% CAGR over 2026-2031. Steady electric-vehicle roll-outs, stringent lightweighting rules, and expanding recycling mandates underpin the momentum. Original equipment makers are embedding recycled or bio-based grades to meet score-card targets, while quick-cycle injection moulding keeps costs in check. Polypropylene maintains leadership because of its versatility and low density, yet rapid growth in polycarbonate and polyamide points to rising demand for high-heat and high-voltage parts. Regional supply chains continue to rebalance after shipping bottlenecks at Panama and Suez canals curtailed feedstock flows, pushing processors to localize resin sourcing. Heightened regulatory scrutiny, particularly on microplastics and verified recycled content, is turning sustainability compliance into a decisive competitive lever across the automotive plastics market.

Key Report Takeaways

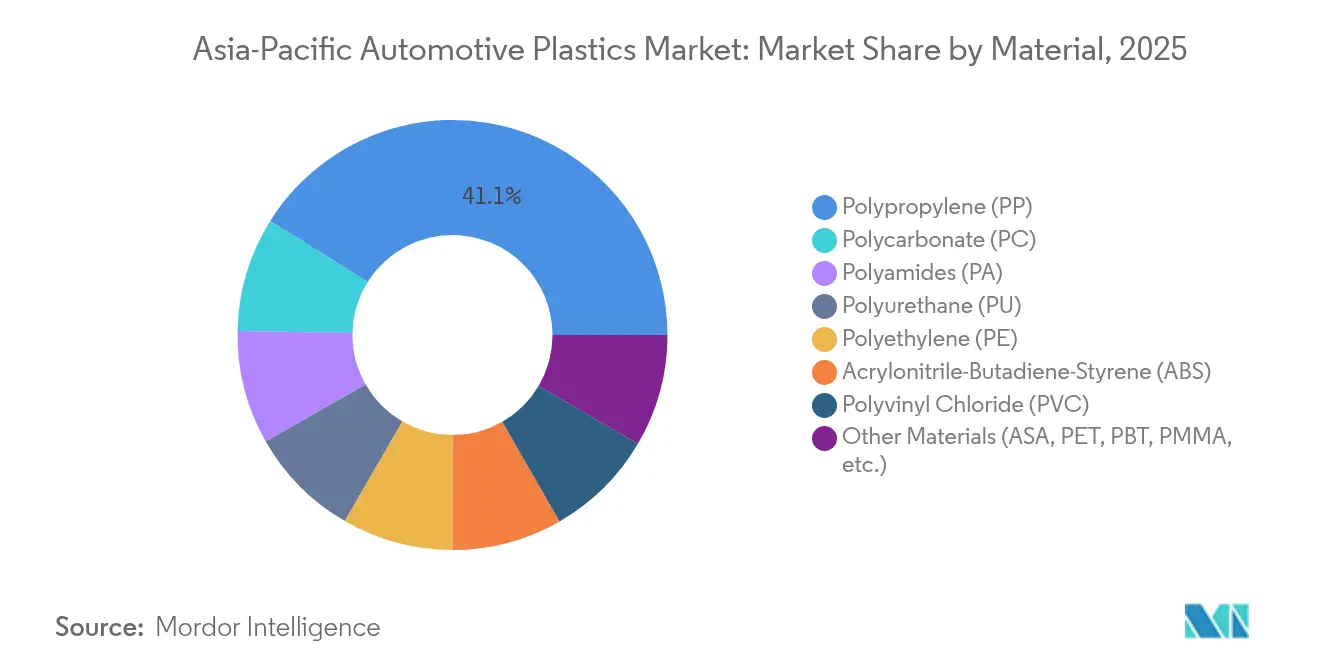

- By material, polypropylene led with 41.10% automotive plastics market share in 2025, while polycarbonate recorded the fastest 7.12% CAGR through 2031.

- By vehicle type, conventional vehicles held 82.95% share of the automotive plastics market size in 2025; electric vehicles are expanding at an 8.35% CAGR to 2031.

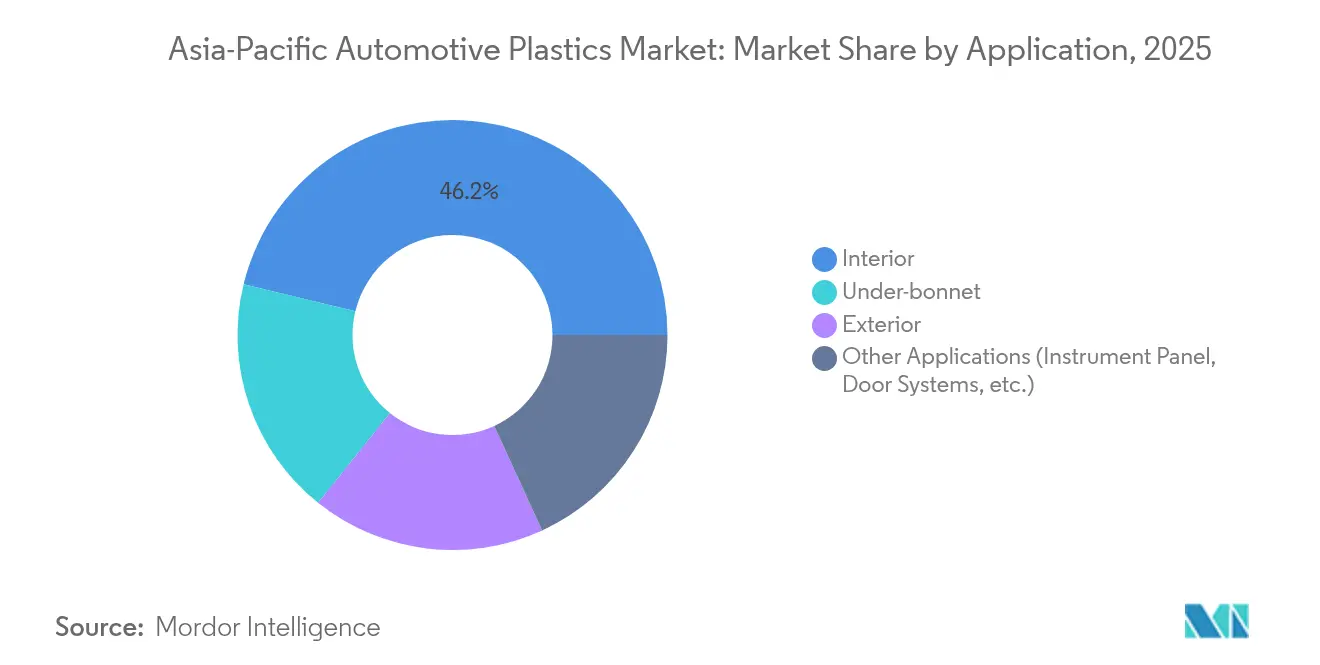

- By application, interior parts accounted for 46.20% of the automotive plastics market size in 2025 and under-bonnet parts are advancing at a 7.42% CAGR over 2026-2031.

- By geography, China captured 41.40% share in 2025, whereas India is projected to log the highest 6.38% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Automotive Plastics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting Mandate Compliance | +1.2% | Global, strongest in China and India | Medium term (2-4 years) |

| Growing Polypropylene Penetration in Interiors and Exteriors | +0.8% | APAC core, spill-over to ASEAN | Long term (≥ 4 years) |

| Surge in Electric-Vehicle Production Volumes | +1.5% | China, India, ASEAN early adopters | Short term (≤ 2 years) |

| Cost Reduction via High-throughput Injection Moulding | +0.7% | Manufacturing hubs: China, Thailand, Vietnam | Medium term (2-4 years) |

| OEM Score-card Targets for Bio-based/Recycled Plastics | +0.9% | Japan, South Korea leading, China following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweighting Mandate Compliance

Regulatory authorities across Asia-Pacific tie fleet-average emissions to weight reduction goals. Automakers respond by substituting metals with advanced polypropylene blends that deliver complex geometries at lower cost. Borealis Fibremod long-glass-fiber polypropylene helped reduce the weight of Volkswagen’s Multivan by 200 kg and met stiffness targets. Gigacasting adoption, first popularised by Tesla, is reshaping body-in-white strategies and puts pressure on plastics suppliers to justify structural roles. To keep pace, compounders introduce chemical foaming agents such as Avient Hydrocerol that cut door-panel weight by 20% while lowering carbon dioxide emissions[1]Polymer Additives World, “Avient Hydrocerol Optimises Door Panel Weight,” polymeradditives.com . In China, where battery-electric vehicles are forecast to command 52.9% of total light-vehicle sales by 2036, lightweight plastic modules that also manage heat are becoming indispensable.

Growing Polypropylene Penetration in Interiors and Exteriors

Polypropylene’s noise-dampening and processing advantages are driving adoption in high-performance components. Röchling Automotive intake manifolds trimmed cabin noise by 10–15 dB compared with polyamide alternatives and saved 15% on material cost. Research teams in Japan blend cellulose nanofibres into polypropylene, boosting impact strength while preserving full recyclability, a feature attractive under extended-producer-responsibility laws. Compounds with 30% post-consumer resin from Sirmax now appear in door panels, cutting lifecycle carbon footprints by 21% and meeting odor thresholds. Exterior cladding benefits from ultraviolet-stable grades such as LyondellBasell CirculenRecover that retain dimensional integrity while offering 20% recycled content. Process optimisation studies confirm that higher packing pressure mitigates shrinkage, reinforcing polypropylene’s appeal for visible Class-A surfaces.

Surge in Electric-Vehicle Production Volumes

Government incentives across ASEAN pushed electric-vehicle penetration from 9% in 2023 to 13% in 2024. EV platforms call for flame-retardant, high-temperature plastics such as BASF Ultramid T6000 polyphthalamide that survives 1 000 thermal-shock cycles between -40 °C and 150 °C. Injection-moulded thermoplastic battery enclosures developed by Engel and SABIC consolidate multiple metal parts into a monolithic design, lowering cost and tooling complexity. Celanese Zytel HTN and Fortron PPS extend operating windows to 180 °C, meeting coolant-system safety margins. National targets, such as Thailand’s 30-at-30 policy and Indonesia’s 600 000-unit ambition by 2030, reinforce near-term demand for specialised resins that satisfy both thermal and dielectric criteria.

Cost Reduction via High-throughput Injection Moulding

Processors across the automotive plastics market deploy MuCell micro-cellular foaming to trim resin consumption without compromising strength. Ensinger reports cycle-time cuts and reduced warpage since adopting the nitrogen-blown technique in 2023. Integrated energy-management systems that combine mold cooling, heat pumps, and material pre-heating yield marked efficiency gains and lower greenhouse-gas intensity. Machinery builders such as FCS Machinery enjoy order backlogs to 2026 thanks to soaring new-energy-vehicle demand. Automation platforms tie real-time sensor feedback to AI-driven optimisation, illustrated by Atomic Industries and LS Mtron moulds equipped with 46 I/O ports. Injection-Moulded Structural Electronics technology integrates wiring into plastic skins, slashing component counts and boosting design freedom.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycling Infrastructure Gaps and Regulatory Pressure | -0.6% | China, India infrastructure challenges | Medium term (2-4 years) |

| Volatility in Raw-material (Naphtha/Propylene) Pricing | -0.9% | Global, acute in import-dependent markets | Short term (≤ 2 years) |

| Emerging Alloy-Aluminium Substitution in Structural Parts | -0.4% | Premium segments, China EV market | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recycling Infrastructure Gaps and Regulatory Pressure

Extended-producer-responsibility rules proliferate, yet collection and sorting capacity lag vehicle scrappage rates in several markets. India’s End-of-Life Vehicles Rules 2025 introduce comprehensive online tracking but omit detailed plastic quotas, limiting immediate circularity gains. Vietnam mandates a 22% recycling rate for rigid PET packaging, signaling future obligations for automotive plastic modules that raise compliance costs. Japan’s mature stewardship programmes still focus on packaging, so automotive parts fall outside current take-back streams. Technical studies show that bumper regrind loses impact resistance if primer removal is incomplete, underscoring the need for chemical recycling to complement mechanical routes. Supply-chain collaborations such as Yanfeng-Trinseo aim to bridge the gap by scaling dissolution and advanced-sorting technologies that meet 2030 targets.

Volatility in Raw-material (Naphtha / Propylene) Pricing

Shipping snarls at Panama and Suez canals cut Chinese access to North-American propane, pushing polypropylene margins down to USD 55 per ton from USD 200 in early 2024. China’s polypropylene capacity will exceed local demand by 68% in 2025, forcing producers into export or run-rate cuts. Geopolitical actions such as Beijing’s 74.9% provisional duty on US polyacetal exports render American product uncompetitive in its biggest offshore market. Red Sea disruptions and Panama-Canal droughts prolong transit times, eroding just-in-time resin inventories that tier-one suppliers rely on. Vertical-integration moves, like SCG Chemicals’ USD 700 million ethane upgrade in Vietnam, help dampen feedstock shocks and lower carbon intensity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polypropylene Adapts to High-Performance Demands

Polypropylene commands the largest slice of the automotive plastics market at 41.10% volume share. ExxonMobil Achieve Advanced grades lift impact strength above legacy copolymers, allowing thinner structures that lower mass and support a USD 55 per-ton margin squeeze. Polycarbonate delivers the fastest 7.12% CAGR as processors embrace Covestro mechanically recycled content for glazing and lighting housings. Thermoplastic polyurethane supply is set to tighten once BASF’s Zhanjiang mega-line ramps up, responding to electrification needs that require flexible cable jacketing in 800 V architectures.

The automotive plastics market size for engineering resins is climbing with acrylonitrile-butadiene-styrene shifting toward biomass styrene monomer and polyamide 66 seeing 40 000-ton capacity increments in Shanghai. Polyethylene still supports packaging and lightweight exterior trims, whereas PVC faces image pressure under circularity pledges. Specialty families like ASA, PBT, and PMMA supply niche roles such as weather-resistant grilles and scooter battery packs. As Asia-Pacific refineries convert crude to chemicals, upstream integration provides cost buffers that safeguard polypropylene’s foothold against the surging engineering-resin cohort.

By Vehicle Type: Electric Vehicles Drive Specialised Material Uptake

Conventional vehicles still consume 82.95% of total automotive plastics volume in 2025, but incremental weight-out initiatives elevate plastic content per car. Intake manifolds in polypropylene now reach acoustic benchmarks that once required heavier polyamide configurations, showcasing cost advantages. Engine covers and fluid reservoirs increasingly adopt chemically foamed polypropylene, further lifting lightweighting headroom.

Electric vehicles post an 8.35% CAGR and push the automotive plastics market toward flame-retardant, dielectric, and thermally conductive grades. Engel-SABIC battery enclosures demonstrate that a single moulding replaces multi-piece aluminium boxes, reducing assembly fasteners and improving recyclability. Celanese PPS cool-plate systems allow tighter battery-cell spacing, extending vehicle range within a fixed pack volume. Government roadmaps—Indonesia’s 600 000-unit goal and Malaysia’s plan for 20% EV penetration—support long-run resin demand growth. Injection-moulding machine backlogs until 2026 indicate that Tier-one suppliers continue to lock in capacity dedicated to EV components.

By Application: Interior Parts Retain Volume Lead while Under-bonnet Surges

Interior modules absorbed 46.20% of all automotive plastics use in 2025. Door-panel makers that integrate 30% recycled polypropylene lower cradle-to-gate emissions by 21% without violating volatile-organic-compound thresholds. IMSE technology embeds touch controls directly into instrument panels, reducing harness weight and assembly steps. Exterior skins benefit from long-glass-fiber polypropylene tailgates that match metal stiffness and shave kilograms from rear closures.

Under-bonnet demand grows at a 7.42% CAGR, driving automotive plastics market share gains for high-heat families. DSM Arnitel HT lets turbo-ducts form in a single shot, coping with 180 °C continuous exposure while halving cost against multi-material assemblies. Avery Dennison high-heat PA66 stands up to 165 °C excursions and meets tightening thermal-shock profiles in downsized engines. Injection-moulded glass-reinforced PA 6 hybrids introduced by LANXESS improve load-bearing performance in power-unit mounts and front-end carriers. The automotive plastics market size attached to these high-temperature niches is projected to expand in tandem with turbocharging and electrification platforms through 2031.

Geography Analysis

China retained 41.40% automotive plastics market share in 2025, anchored by global light-vehicle output leadership and a massive chemical production base. Margin headwinds emerged when canal disruptions throttled US propane inflows, sending domestic polypropylene spreads to USD 55 per ton. The country’s polypropylene capacity overhang, forecast to climb 68% in 2025, invites export pressure yet also lowers resin costs for local converters. Battery-electric vehicles are likely to command 52.9% of 2036 sales, widening the addressable pool for high-performance plastics that deliver thermal management and flame-retardancy. Geopolitical levies, such as the 74.9% duty on US polyacetal, encourage accelerated in-house specialty-resin expansion.

India shows the fastest 6.38% CAGR, underpinned by USD 87 billion planned petrochemical investments and policies allowing 100% foreign direct investment. Automotive plastics market size gains stem from capacity additions at BASF’s Gujarat and Maharashtra compounds that feed growing domestic demand. The End-of-Life Vehicles Rules 2025 create an online marketplace for scrappage certificates and battery recycling, indirectly boosting reclaimed plastic components. Though India recorded a 7.02 million-ton polymer trade deficit in 2023-24, expansions toward 46 million-ton national nameplate capacity by 2030 aim to narrow the shortfall.

Japan and South Korea operate at the technological frontier but grapple with volume constraints. Japanese vehicle output fell 8.8% in 2024 to 6.01 million units, reducing polyether-polyol consumption. Even so, Toray Advanced Materials Korea boosted PPS resin capacity by 5 000 tons, targeting a global 6% annual demand rise in EV drivetrain parts. South Korea’s draft recycling enforcement mandates authenticated recycled content, spurring investment in digital traceability platforms.

ASEAN markets display mixed volumes yet favourable policy frameworks. Light-vehicle sales slipped 5.4% in 2024 across ASEAN-6, but EV penetration improved to 13%. Thailand’s 30-at-30 strategy earmarks tax incentives to localise battery module production, elevating demand for flame-retardant polypropylene and polyamide enclosures. Vietnam secures upstream resilience through SCG Chemicals’ USD 700 million ethane enhancement, while domestic compounders like Polyplastics supply battery-pack PBT to home-grown e-scooter manufacturer Selex Motors. Indonesia intends to raise EV capacity to 600 000 units by 2030, courting resin producers for joint ventures near nickel and cobalt resources.

Competitive Landscape

The automotive plastics market exhibits moderate consolidation. Global majors BASF, SABIC, and LyondellBasell leverage feedstock integration and broad engineering-resin portfolios. Covestro differentiates on circularity through its Guangdong recycling complex that will boost recycled-content polycarbonate output to 60 000 tons by 2026[2]Covestro Newsroom, “Mechanical-Recycling Polycarbonate Line Starts in Guangdong,” covestro.com . Kingfa, LG Chem, and Asahi Kasei use regional proximity and tailored grades to win business from rapidly expanding Tier-one moulders tied to Chinese and Korean automakers.

Competitive intensity pivots on electrification and sustainability. Yanfeng and Trinseo combine advanced mechanical recycling with dissolution technology to supply dashboards meeting 2030 end-of-life mandates. Covestro’s flame-retardant thermoplastic polyurethane targeting 150 °C cable applications rounds out high-voltage offerings and reinforces safety credentials in the automotive plastics industry.

Mergers and alliances reshape the field. ADNOC and OMV agreed to acquire Nova Chemicals for USD 13.4 billion, integrating the asset into Borouge-4 and creating the world’s largest single-site polyolefin hub aimed at Asia demand pull. AI-enabled optimisation platforms from Atomic Industries grant moulders live feedback, reducing scrap and speeding new-tool validation. Supply chain resilience is now a value proposition as processors hedge against maritime chokepoints by dual-sourcing propane and commissioning regional cracker investments.

Asia-Pacific Automotive Plastics Industry Leaders

BASF SE

Covestro AG

SABIC

LG Chem

LyondellBasell Industries Holdings B.V

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Polyplastics launched PLASTRON LFT RA627P, an eco-friendly long fiber-reinforced polypropylene (PP) automotive plastic for automotive applications. The material features low density, high specific rigidity, and excellent damping properties, making it suitable for various automotive components.

- January 2025: Covestro announced an investment in the low triple-digit million Euro range to expand its polycarbonate production at the Hebron, Ohio facility. The expansion includes the construction of new production lines for customized polycarbonate, an automotive plastic. This expansion strengthens the company's North American supply capabilities and supports Asian automotive manufacturers' global operations.

Asia-Pacific Automotive Plastics Market Report Scope

Automotive plastics are engineering plastics that have high performance which makes them compatible with the rigorous demands of the automotive industry. Generally, they are versatile, making them suitable for achieving the needed innovation in the industry. The use of engineering plastics in automobiles reduces vehicle weight, which also supports improving the fuel efficiency of the vehicle.

The automotive plastics market is segmented by material, application, vehicle type, and geography. By material, the market is segmented into polypropylene (PP), polyurethane (PU), polyvinyl chloride (PVC), polyethylene (PE), acrylonitrile butadiene styrene (ABS), polyamides (PA), polycarbonate (PC), and other materials (acrylonitrile styrene acrylate (ASA), polyethylene terephthalate (PET), polybutylene terephthalate (PBT), Acrylic (PMMA)). By application, the market is segmented into the interior, exterior, under-bonnet, and other applications (instrument panel, powertrain, door systems, etc.). By vehicle type, the market is segmented into conventional/traditional vehicles and electric vehicles. The report also covers the market size and forecasts for automotive plastics in 5 countries across the Asia-Pacific region. For each segment, the market sizing and forecasts have been done based on volume (tons).

| Polypropylene (PP) |

| Polyurethane (PU) |

| Polyvinyl Chloride (PVC) |

| Polyethylene (PE) |

| Acrylonitrile-Butadiene-Styrene (ABS) |

| Polyamides (PA) |

| Polycarbonate (PC) |

| Other Materials (ASA, PET, PBT, PMMA, etc.) |

| Conventional/Traditional Vehicles |

| Electric Vehicles |

| Exterior |

| Interior |

| Under-bonnet |

| Other Applications (Instrument Panel, Door Systems, etc.) |

| China |

| India |

| Japan |

| South Korea |

| ASEAN |

| Rest of Asia-Pacific |

| By Material | Polypropylene (PP) |

| Polyurethane (PU) | |

| Polyvinyl Chloride (PVC) | |

| Polyethylene (PE) | |

| Acrylonitrile-Butadiene-Styrene (ABS) | |

| Polyamides (PA) | |

| Polycarbonate (PC) | |

| Other Materials (ASA, PET, PBT, PMMA, etc.) | |

| By Vehicle Type | Conventional/Traditional Vehicles |

| Electric Vehicles | |

| By Application | Exterior |

| Interior | |

| Under-bonnet | |

| Other Applications (Instrument Panel, Door Systems, etc.) | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the Asia-Pacific automotive plastics market size today and how fast is it growing?

The market reached 10.22 million tons in 2026 and is projected to climb to 13.07 million tons by 2031, reflecting a 5.04% CAGR.

Which resin commands the largest share of automotive plastics in the region?

Polypropylene leads with 41.10% share because its low density, easy processing, and cost advantages suit both interior and exterior vehicle parts.

How is electric-vehicle adoption influencing material demand?

Accelerating EV production—up from 9% to 13% of ASEAN-6 sales in 2024—drives uptake of flame-retardant and high-temperature plastics for battery enclosures, inverters, and coolant systems.

What regulations most affect automotive plastics usage?

Lightweighting and circular-economy rules such as India’s End-of-Life Vehicles 2025 framework and South Korea’s draft recycled-content verification mandate are pushing OEMs toward recyclable or bio-based grades.

Why are raw-material price swings a concern for converters?

Canal disruptions and oversupply have pushed China’s polypropylene margins down to USD 55 per ton, forcing processors to hedge feedstock sourcing and invest in vertical integration.

Page last updated on: