Market Overview

| Study Period | 2021 - 2031 |

|---|---|

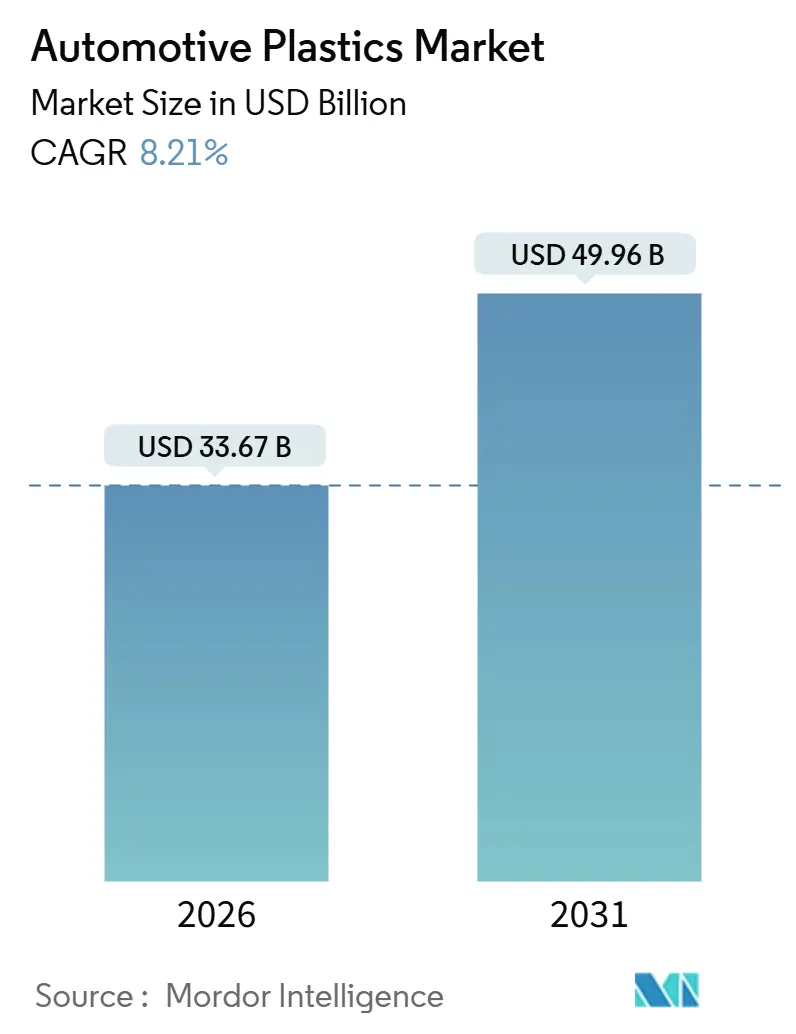

| Market Size (2026) | USD 33.67 Billion |

| Market Size (2031) | USD 49.96 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

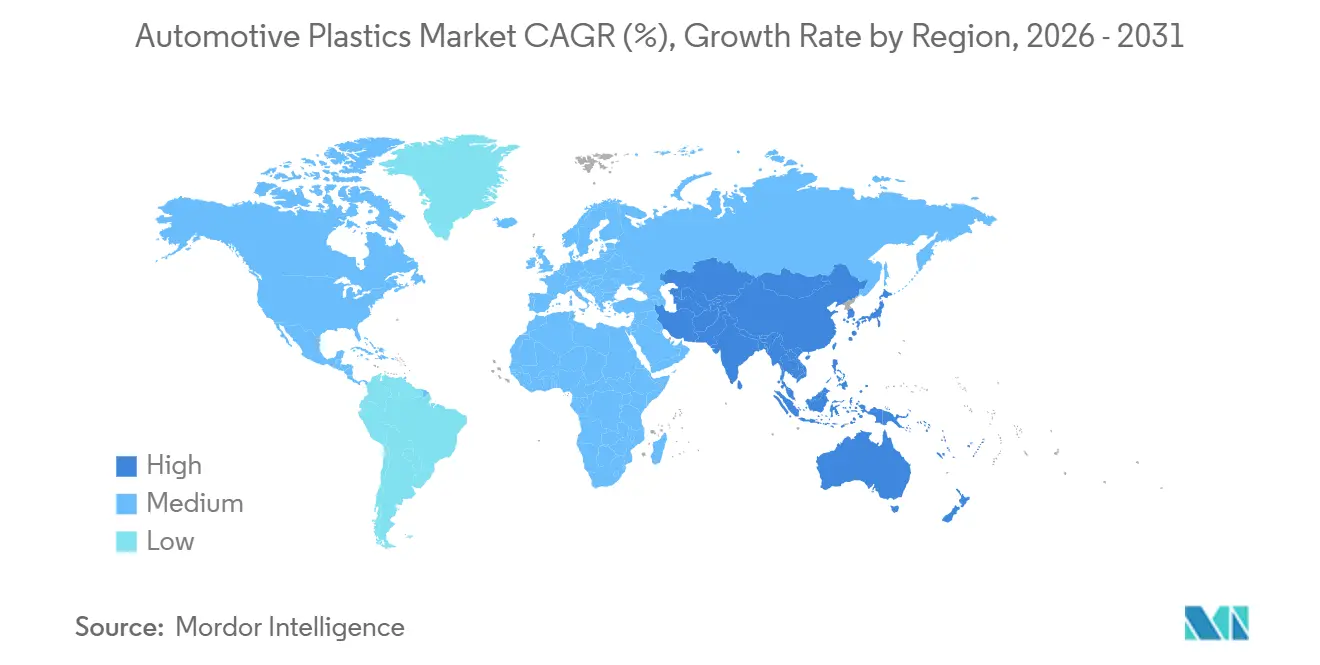

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Plastics Market Analysis by Mordor Intelligence

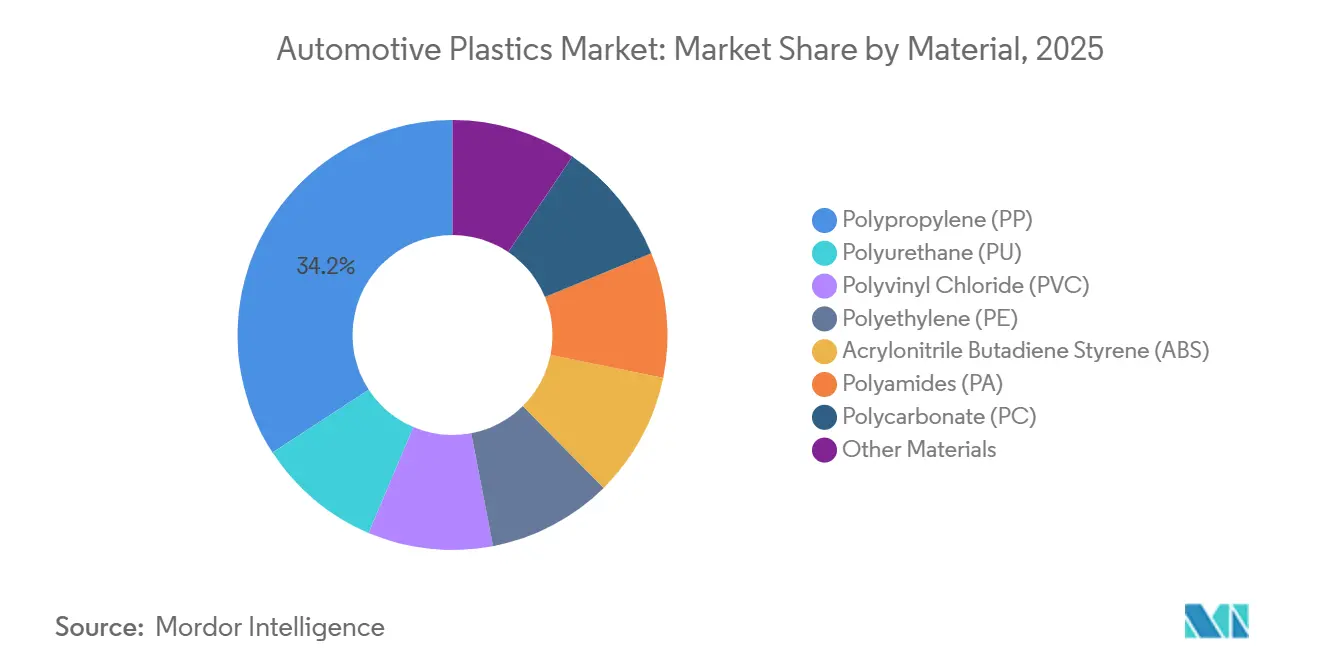

The Automotive Plastics Market size is estimated at USD 33.67 billion in 2026, and is expected to reach USD 49.96 billion by 2031, at a CAGR of 8.21% during the forecast period (2026-2031). Lightweighting mandates, expanding electric-vehicle (EV) output, and circular-economy quotas are converging, turning plastics from cost-cutting inputs into essential enablers of regulatory compliance and vehicle differentiation. Polypropylene’s 34.22% share in 2025 underscores its cost-performance balance across bumper fascia and interior trim, while polyamide’s 8.92% CAGR signals rising thermal demands in turbocharged and hybrid powertrains. Electric vehicles are advancing at a 10.93% CAGR as skateboard platforms integrate 15-20 kg of extra polymers in battery covers and structural floor pans. Asia-Pacific, at 49.11% of global volume, is expanding at 9.94% CAGR, propelled by China’s EV target for 2026 and India’s production-linked incentives for engineering-resin localization.

Key Report Takeaways

- By material, polypropylene led with 34.22% revenue share in 2025, while polyamide recorded the fastest 8.92% CAGR through 2031.

- By application, interior components accounted for 32.98% of the automotive plastics market size in 2025, whereas under-bonnet parts are advancing at an 8.96% CAGR.

- By vehicle type, conventional platforms commanded an 81.96% share in 2025, yet electric vehicles are expanding at a 10.93% CAGR to 2031.

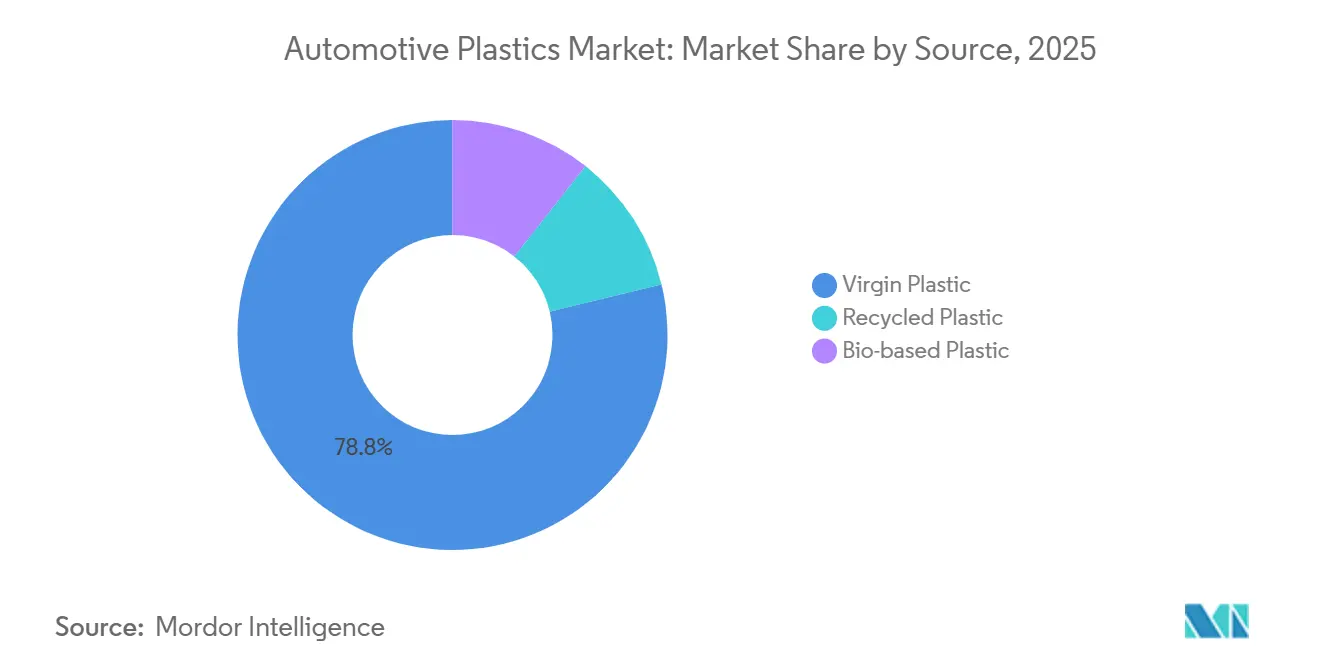

- By source, virgin grades held 78.79% of the automotive plastics market share in 2025, and bio-based grades are projected to grow at a 10.80% CAGR.

- By geography, Asia-Pacific dominated with a 49.11% share in 2025, and the region is forecast to post a 9.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Automotive Plastics Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory CO₂ targets driving lightweighting | +1.8% | EU, China, North America | Medium term (2-4 years) |

| EV production surge elevating plastics/vehicle | +2.1% | Global, with APAC and EU leading | Medium term (2-4 years) |

| Cost and design flexibility versus metals | +1.5% | Global | Short term (≤2 years) |

| Mandatory recycled-content quotas in EU vehicles | +1.2% | EU, spill-over to North America | Long term (≥4 years) |

| Rise of skateboard EV platforms allowing 15-20 kg more plastic integration | +1.6% | Global, early gains in China, the US | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory CO₂ Targets Driving Lightweighting

In the EU, stricter fleet-average CO₂ caps, alongside North America's fuel-economy adjustments, are pushing automakers to shed weight from their models. Glass-fiber-reinforced polypropylene, offering significant weight reduction over steel at a modest cost premium, emerges as the most cost-effective compliance solution. China's dual-credit scheme boosts demand further, incentivizing lightweight vehicles and accelerating the shift to polymers in door panels and tailgates. Mass-market platforms are now integrating plastics into structural areas traditionally reserved for metals, narrowing the performance divide between standard and advanced materials. ISO marking standards ensure traceability at the end of a product's life, harmonizing weight reduction efforts with circular-economy initiatives.

EV Architecture Unlocking Structural and Thermal Roles

Battery-electric platforms utilize more plastics per vehicle compared to their ICE counterparts. This is largely due to components like battery covers, thermal-management housings, and flat-floor pans, which leverage polymers for their electrical insulation properties and design flexibility. Tesla's Model Y features one-piece polycarbonate-ABS shields, reducing part count and assembly time. Given the heightened emphasis on arc-tracking resistance, flame-retardant polycarbonate and high-CTI polyamides have become the go-to materials for battery-module covers and 800-volt connectors. The initial model years of an EV program see the highest plastic usage, with subsequent redesigns often opting for metals to cut costs. With the introduction of new EU battery regulations emphasizing recycled content, there's a surge in demand for post-consumer polycarbonate and nylon.

Mandatory Recycled-Content Quotas Reshaping Supply Chains

The recycled-content requirement in European vehicles by 2030 is pushing OEMs to lock in long-term offtake agreements with recyclers and qualify post-consumer polypropylene for Class-A surfaces. Mechanical recycling retains tensile strength, yet color and odor hurdles limit interior-visible use. Chemical recycling addresses purity but elevates feedstock cost, flipping the historical price hierarchy as certified recycled polypropylene now sells at a premium against virgin resin. France’s AGEC law layers a malus tax on low-recycled-content models, accelerating OEM investments in closed loops. South Korea’s expanded EPR scheme funnels support into collection networks but still recovers only a portion of end-of-life vehicle plastic.

Skateboard EV Platforms Consolidating Part Counts

Flat-floor skateboard designs streamline assembly by merging steel stampings into sizable plastic moldings, allowing for late-stage model differentiation. Rivian’s innovative composite floor pan, which combines polypropylene with continuous glass fiber, achieves significant weight reduction while maintaining the torsional rigidity of a unibody[1]Rivian Automotive Inc., “Platform Architecture Briefing 2025,” rivian.com. Meanwhile, Chinese EV startups, free from the constraints of legacy tooling, are integrating more structural plastics into each vehicle than established OEM counterparts. Suppliers boasting the capability to mold large parts and offering co-design assistance are reaping a larger market share. However, adhering to global safety standards means crash test cycles can extend development timelines[2]National Highway Traffic Safety Administration, “Proposed CAFE Standards 2027-2032,” nhtsa.gov .

Restraints Impact Analysis of Automotive Plastics Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-linked resin prices | -0.9% | Global | Short term (≤2 years) |

| OEM qualification delays for bio-based engineering plastics | -0.5% | EU, North America | Medium term (2-4 years) |

| Microplastic tyre and brake-dust directives limiting certain polymer blends | -0.3% | EU, spill-over to California | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Volatility Compressing Margins

Polypropylene and polyethylene, tracking petrochemical feedstocks with a lag, experience quarterly price swings. These fluctuations often lead to contract renegotiations and strain already thin supplier margins. In Q1 2025, a rally in Brent crude pushed European polypropylene prices higher. This surge triggered force-majeure clauses and delayed launch dates for two major OEMs. The concentrated upstream capacity makes polyamide markets particularly vulnerable; for instance, a caprolactam outage led to a significant spike in PA6 prices. Additionally, index-linked pricing transfers risk to automakers, complicating their multi-year cost forecasts. Meanwhile, smaller compounders, lacking robust balance sheets, are either consolidating or exiting the sector.

Microplastic Regulations Limiting Polymer Choices

Upcoming EU regulations on microplastics are set to impact exterior parts prone to abrasion. This poses a challenge for styrenic copolymers used in wheel-arch liners and underbody shields. Meanwhile, California's SB 1263 law, effective by 2028, limits mass loss in standardized abrasion tests. This rule effectively sidelines traditional ABS and PP-EPDM blends. To comply, OEMs are resorting to polyurethane coatings, which not only raise material costs but also complicate recycling efforts. Coated parts become more challenging to sort and reprocess. In Japan, a pilot program for a low-shedding label is underway, with potential mandatory status by 2027, leading to a fragmentation of global standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Plastics Market Segment Analysis

By Material:

High-Heat Polyamides Climb on Thermal DemandsPolypropylene held the largest share at 34.22% in 2025 due to its dominance in interior panels and bumper skins. Polyamide’s 8.92% CAGR reflects higher continuous-use temperatures in turbocharged and hybrid engines that exceed polypropylene limits. The market size for polyamide in automotive plastics is set to grow significantly. Furthermore, if EV battery covers transition to high-CTI nylon grades, polyamide's market share in automotive plastics could increase further. While polyurethane steadily carves out its niche in seating and NVH roles, benefiting from thinner foams that reduce weight, PVC is ceding ground to phthalate-free thermoplastic polyolefins in European car interiors.

Premium polycarbonate is making strides with its applications in panoramic roofs and LED lighting lenses. ABS, despite facing density penalties, continues to be the go-to choice for glossy interior trims. Polyethylene's performance mirrors overall production trends. However, multilayer HDPE fuel tanks, fortified with EVOH barriers, are now setting the standard by adhering to stricter evaporative regulations. Specialty resins like PBT and PPA are carving out significant roles in sensor housings and 800-volt busbars, commanding price premiums due to their dimensional stability. And as the industry moves towards global sourcing and recycling, standardized ISO abbreviations are proving invaluable.

By Application:

Under-Bonnet Parts Outpace Interior GrowthInterior components captured 32.98% of 2025 revenue, yet their CAGR lags high-heat under-bonnet parts that grow at 8.96%. The automotive plastics market for under-bonnet parts is expected to expand as turbocharged downsized engines and hybrid cooling loops raise operating temperatures. Air-intake manifolds now rely on glass-fiber-reinforced PA66 for weight savings and optimized airflow, while radiator end tanks transition to PPA.

Exterior panels are growing steadily as OEMs weigh lightweighting benefits against repairability costs. Other applications, including fluid reservoirs, high-voltage connectors, and chassis shields, see a mix shift toward high-value engineering resins as 48-volt and 800-volt architectures proliferate. Under-bonnet parts, though a smaller portion of volume, account for a significant share of material value because of premium resin pricing.

By Vehicle Type:

EV Platforms Drive Plastics IntensityConventional vehicles retained 81.96% volume in 2025. However, electric vehicles (EVs) are incorporating more polymers per unit, propelling a 10.93% CAGR. Skateboard frames are doing away with transmission tunnels, paving the way for large-format plastic floor pans that can replace multiple stampings. Battery covers made from polycarbonate or polyamide are required to comply with UL 94 V-0 and IP67 standards. Chinese EV manufacturers are leading the charge, specifying higher amounts of structural plastics, a move that puts them ahead of traditional OEMs still reliant on metal tooling.

While early EV models were heavily engineered, future redesigns might revert to metals for cost efficiency, potentially tempering growth post-2030. Hybrid vehicles, positioned between pure EVs and internal combustion engines (ICEs), showcase a moderate intensity of plastics. They necessitate extra battery-module covers but still utilize conventional under-bonnet components.

By Source:

Bio-Based Grades Gain Strategic RelevanceVirgin grades still dominated with 78.79% in 2025, but bio-based plastics expanded at 10.80% CAGR as OEMs hedge crude exposure and pursue carbon-neutral claims. Notably, castor-oil-derived PA10.10 not only rivals the performance of PA66 but does so with a commendable reduction in cradle-to-gate emissions. Meanwhile, bio-based polypropylene, derived from sugar-cane ethanol, is currently undergoing pilot trials, lauded for its seamless compatibility with existing tooling. Recycled plastics are on an upward trajectory, especially as EU quotas are set to escalate in the coming years. Yet, a challenge looms: their premium pricing transforms recycled content into a short-term margin obstacle.

While mechanical recycling successfully preserves tensile properties, it grapples with color stability issues. This challenge has led to a pivot towards chemical-recycling pathways, which, despite their higher costs, produce a quality akin to virgin materials. In Asia, South Korea and Japan are broadening their Extended Producer Responsibility (EPR) schemes. However, a fragmented dismantling process has stagnated recovery rates. Additionally, smaller compounders face the brunt of compliance costs tied to ISO environmental labels.

Geography Analysis

APAC Automotive Plastics Market

Asia-Pacific held a 49.11% share in 2025 and is advancing at a 9.94% CAGR, the strongest among regions. China's ambitious EV production target fuels a significant surge in polypropylene demand. Meanwhile, India's production-linked incentives are catalyzing the establishment of new compounding plants by industry giants like BASF, LG Chem, and Lotte. Japan's commitment to carbon-neutral fleets is driving a notable uptick in the adoption of castor-oil-based polyamides. Southeast Asia is emerging as a secondary hub, with Chinese and Korean suppliers strategically bolstering capacities in Thailand and Indonesia to mitigate geopolitical risks.

North America Automotive Plastics Market

North America is charting a steady course. The US Inflation Reduction Act's domestic-content rules are steering compounding operations back to Texas and Louisiana. Meanwhile, Mexico, despite being a significant resin supplier in the region, grapples with stringent USMCA value-content thresholds. Canada is outpacing the U.S. in growth, driven by incentives promoting premium EV production, which leans heavily on engineering plastics.

EMEA and South America Automotive Plastics Market

Europe is navigating a steady growth trajectory, even amidst stagnant vehicle builds. Demand remains buoyed by aggressive mandates for recycled content and commitments to PVC-free interiors. Germany is streamlining its capacity for better utilization, while France and Italy are banking on EV purchase subsidies. South America is witnessing growth. Braskem's pilot project on bio-based polypropylene could position Brazil as a future export hub, albeit with commercial scalability still two years away. The Middle East and Africa are growing at a commendable pace, bolstered by Saudi localization efforts and assembly hubs in South Africa.

Competitive Landscape

The automotive plastics market is moderately fragmented. Strategic focus centers on chemical-recycling pilots that turn post-consumer polycarbonate and nylon into mass-balance feedstocks, helping suppliers decouple margins from crude swings. Braskem and Haldor Topsoe commercialize bio-ethanol-derived polypropylene, while LG Chem partners with CJ CheilJedang on sugar-based polyamide.

Automotive Plastics Industry Leaders

BASF SE

SABIC

Dow

Covestro AG

LyondellBasell Industries Holdings B.V.

- *Disclaimer: Major Players sorted in no particular order

Automotive Plastics Market Companies Covered in this Report

- Arkema

- Asahi Kasei Advance Corporation

- BASF SE

- Borealis AG

- Braskem

- Celanese Corporation

- Covestro AG

- Daicel Corporation

- Dow

- dsm-firmenich

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- INEOS

- LANXESS

- LG Chem

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals Inc.

- SABIC

- TEIJIN LIMITED

Recent Industry Developments in Automotive Plastics Market

- July 2024: LyondellBasell introduced Schulamid ET100, a new interior-grade polyamide compound designed for lightweight door-window frames with low odor performance.

- June 2024: Dow completed the acquisition of Circulus, a recycler of plastic waste into post-consumer recycled grades, and signed an MoU targeting 3 million metric tons of circular and renewable solutions annually by 2030.

Automotive Plastics Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the automotive plastics market as the annual revenue generated from virgin, recycled, and emerging bio-based thermoplastic and thermoset resins molded into functional components inside, outside, or beneath light and heavy vehicles. Typical polymers include polypropylene, polyurethane, PVC, PE, ABS, PA, PC, and related engineering grades. According to Mordor Intelligence, parts such as bumpers, instrument panels, battery housings, and coolant pipes are fully captured under this scope.

Scope exclusion: components whose fiber reinforcement exceeds fifty percent by weight, rubber/elastomer blends, and adhesive sealants are outside this assessment.

Segments Covered in This Report

- By Material

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Polyethylene (PE)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyamides (PA)

- Polycarbonate (PC)

- Other Materials

- By Application

- Exterior

- Interior

- Under Bonnet

- Other Applications

- By Vehicle Type

- Conventional / Traditional Vehicles

- Electric Vehicles

- By Source

- Virgin Plastic

- Recycled Plastic

- Bio-based Plastic

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed tier-one molder executives, masterbatch suppliers, OEM body-in-white engineers, and regional trade officers across Asia-Pacific, Europe, and the Americas. These conversations clarified emerging resin substitution rates in EV platforms, realistic scrap-loop recovery yields, and regional price pass-through mechanisms that secondary sources rarely quantify.

Desk Research

Mordor analysts first compiled public domain datasets from sources such as OICA vehicle build statistics, Eurostat ProdCom plastic part codes, UN Comtrade HS-3926 flows, and national recycling registries, which outline polymer movement into automotive applications. Additional context came from industry associations, Society of Plastics Engineers, ACEA technical papers, and the US Department of Energy lightweighting targets, supplemented by company 10-Ks and investor decks that disclose material mix roadmaps. Paid intelligence from D&B Hoovers and Dow Jones Factiva aided in validating producer revenues by resin family. This list is illustrative; many other references were reviewed during evidence gathering.

Market-Sizing & Forecasting

A top-down build began with 2024 light and heavy vehicle production, multiplied by average plastic kilograms per vehicle, which are then valued using regional average selling prices by resin. Bottom-up cross-checks, sampled supplier revenues, molding capacity utilizations, and channel checks helped fine-tune totals. Key model variables include vehicle build rates, resin density shifts toward high-heat grades, polymer price curves, and statutory recycled-content milestones. Forecasts employ multivariate regression coupled with scenario analysis to reflect EV penetration paths and weight-reduction mandates; gaps in bottom-up inputs are bridged through normalized ASP benchmarks validated in stakeholder interviews.

Data Validation & Update Cycle

Model outputs undergo variance checks against trade statistics and producer disclosure, followed by peer review. We refresh every twelve months, with interim revisions triggered by greater than ten percent swings in vehicle output, resin prices, or regulation. A final analyst pass is completed before release to ensure clients receive the most current view.

How Mordor Intelligence's Automotive Plastics Market Size Compares to Other Published Estimates

Published estimates often diverge because firms choose different component scopes, polymer coverage, and refresh cadences.

We anchor our baseline on clearly verifiable build volumes and resin usage factors agreed upon by market practitioners, whereas others may rely on broad polymer demand pools or dated cost curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 33.52 B (2025) | Mordor Intelligence | - |

| USD 31.63 B (2024) | Global Consultancy A | Focuses on interior and exterior trim only and applies uniform ASP across regions |

| USD 44.12 B (2024) | Regional Consultancy B | Rolls total polymer demand into auto share without isolating end-use conversion factors |

| USD 30.0 B (2023) | Industry Journal C | Base year predates EV scale-up and relies on limited post-COVID production recovery data |

In summary, clients choose Mordor's numbers because they trace back to transparent vehicle counts, resin mix metrics, and a disciplined yearly refresh that collectively deliver a balanced, decision-ready starting point.

Key Questions Answered in the Report

How fast will demand for plastics in vehicles grow between 2026 and 2031?

The automotive plastics market is forecast to expand at an 8.21% CAGR, rising from USD 33.67 billion in 2026 to USD 49.96 billion by 2031.

Which material will see the quickest adoption in next-generation powertrains?

Polyamide is advancing at an 8.92% CAGR because high-heat zones in turbocharged and hybrid engines exceed the limits of polypropylene.

Why are electric vehicles important for polymer suppliers?

EV skateboard platforms add more plastics per unit for battery covers, flat-floor pans, and thermal housings, delivering double-digit demand growth despite lower unit share.

Which region offers the fastest growth opportunity to 2031?

Asia-Pacific, led by China and India, is pacing the field with a 9.94% CAGR thanks to large EV production targets and incentives for local resin compounding.

Page last updated on: