Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

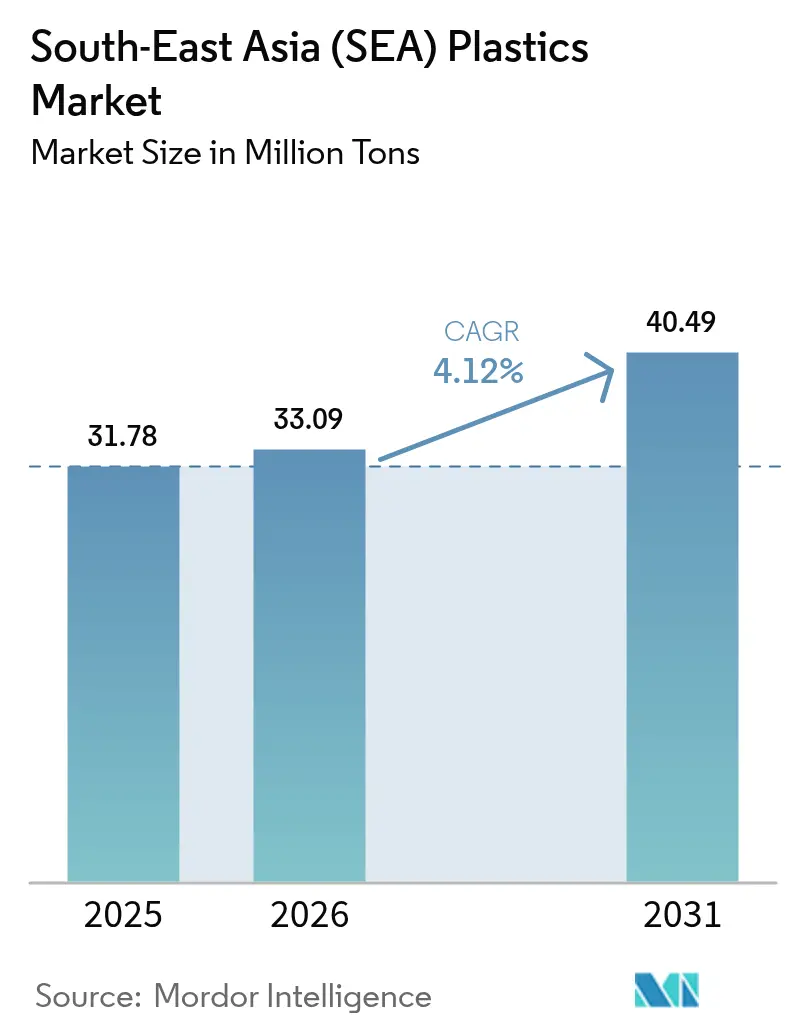

| Base Year Market Size (2025) | 31.78 Million tons |

| Market Volume (2026) | 33.09 Million tons |

| Market Volume (2031) | 40.49 Million tons |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

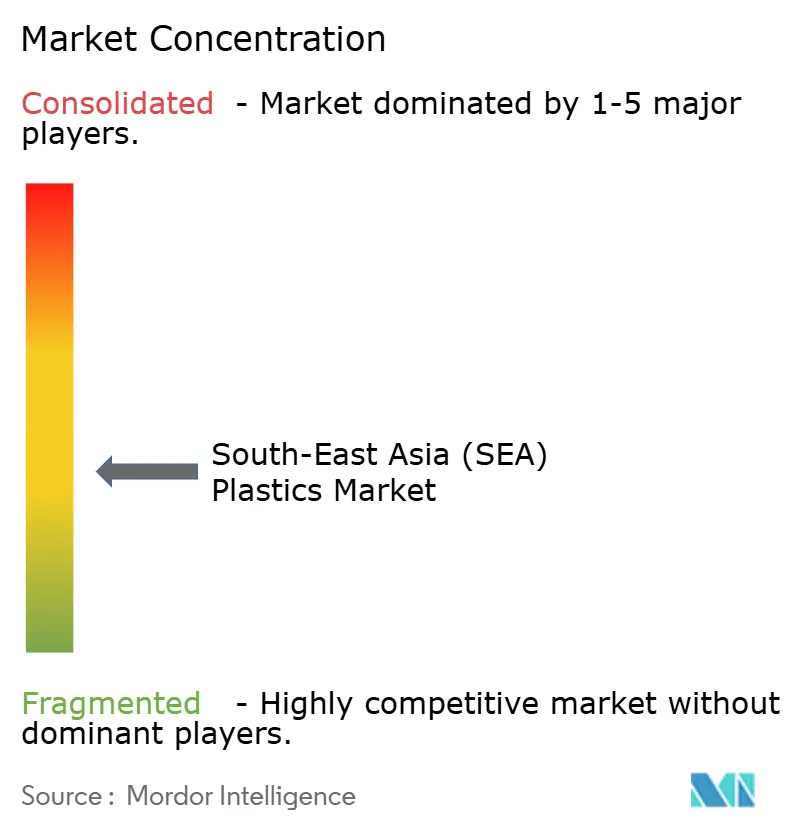

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South-East Asia (SEA) Plastics Market Analysis by Mordor Intelligence

The South-East Asia Plastics Market size was valued at 31.78 million tons in 2025 and is estimated to grow from 33.09 million tons in 2026 to reach 40.49 million tons by 2031, at a CAGR of 4.12% during the forecast period (2026-2031). From October 2024 to December 2025, the petrochemical landscape witnessed a significant transformation. Investments in crackers and downstream units transitioned from a heavy reliance on imports to achieving regional self-sufficiency. Indonesia and Vietnam have solidified their positions as key players in the polyolefin supply chain, a domain once dominated by Middle-East feedstock. In 2025, while traditional commodity resins dominated the volume, the tightening spreads between propane and naphtha began to erode profit margins. As a result, converters were prompted to shift towards engineering grades and bioplastics, drawn not only by their premium pricing but also by their resilience against feedstock price fluctuations.

Key Report Takeaways

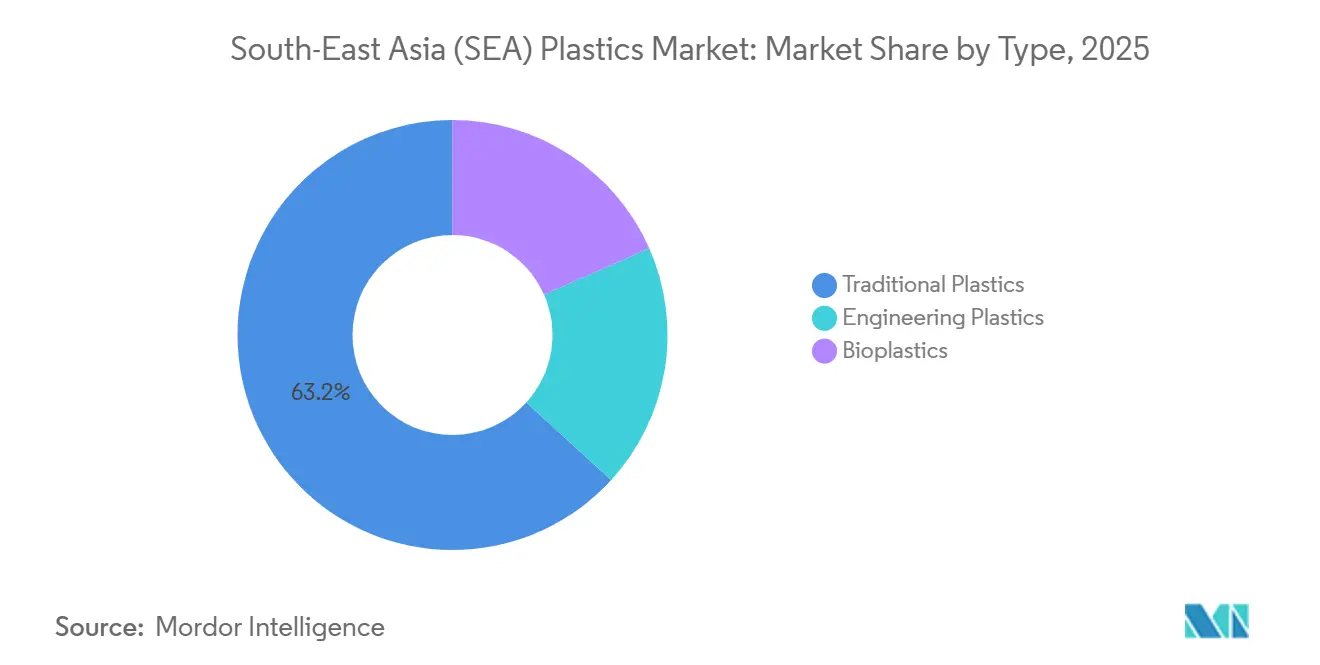

- By type, traditional plastics held 63.22% of the South-East Asia plastics market share in 2025; bioplastics are advancing at a 4.56% CAGR through 2031.

- By technology, injection molding accounted for 41.96% of the South-East Asia plastics market size in 2025; blow molding is set to expand at a 4.71% CAGR to 2031.

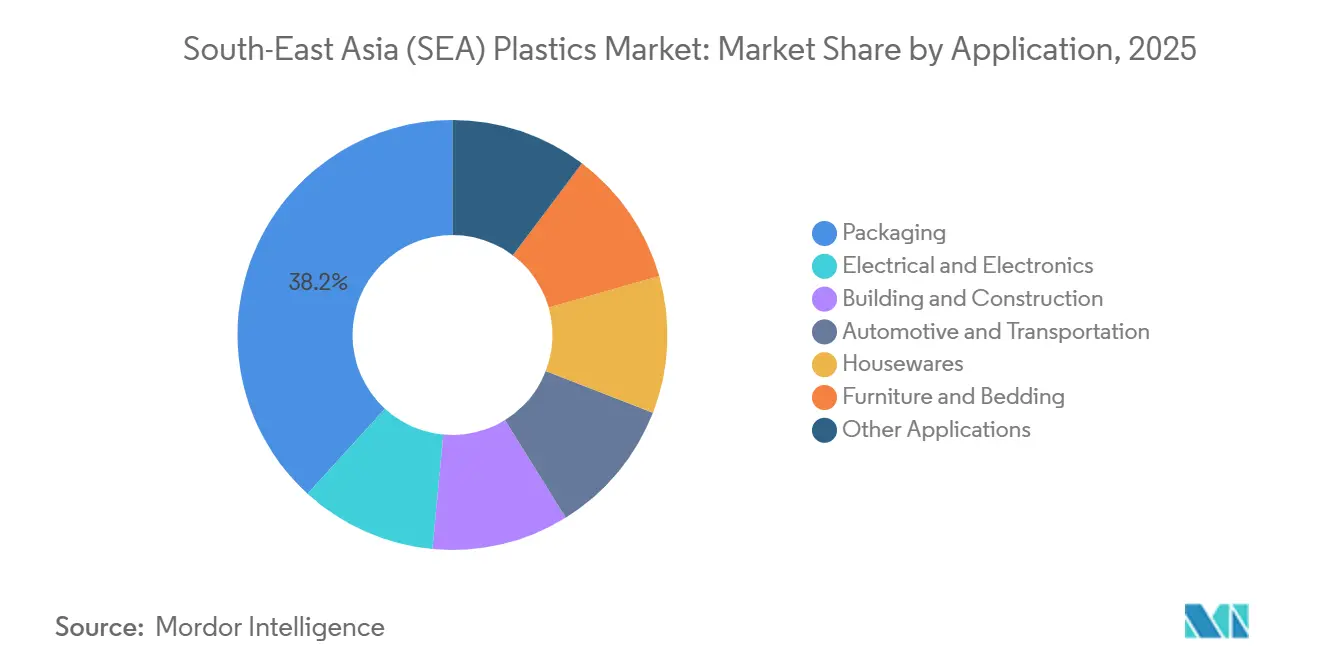

- By application, packaging led with 38.22% volume share in 2025, whereas building and construction is forecast to grow fastest at 4.87% CAGR through 2031.

- By geography, Indonesia commanded 34.26% of the South-East Asia plastics market share in 2025, while Vietnam is projected to grow at a 4.56% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South-East Asia (SEA) Plastics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid capacity expansions in Indonesia and Vietnam | +1.2% | Indonesia, Vietnam, with spillover to Thailand and Malaysia | Medium term (2-4 years) |

| Infrastructure megaproject pipeline fuelling construction plastics | +0.9% | Indonesia (IKN), Thailand (Land Bridge), Malaysia (MRT3), Vietnam (North-South Expressway) | Long term (≥4 years) |

| Government-sponsored petro-chemical SEZ corridors | +0.7% | Indonesia (Tuban, Bontang), Thailand (Map Ta Phut), Malaysia (Pengerang), Vietnam (Long Son) | Medium term (2-4 years) |

| Data-center boom driving specialty insulation foams | +0.5% | Singapore, Malaysia, Indonesia (Jakarta, Batam), Thailand (Bangkok) | Short term (≤2 years) |

| Regional marine-debris pledges accelerating recycled-content uptake | +0.6% | ASEAN-wide, with early adoption in Thailand, Philippines, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Capacity Expansions in Indonesia and Vietnam

In October 2025, Lotte Chemical Indonesia's LINE complex began producing ethylene and downstream polyethylene (PE), representing a significant step in reducing the nation's dependence on imported polyolefins and lowering the freight premiums for LLDPE film. In contrast, Vietnam's SCG-backed Long Son project, which aims to produce ethylene, faced a setback in October 2024 due to unresolved LPG offtake deals, with discussions for a restart slated for August 2025. The surge in new capacity has heightened pricing competition, pressuring Thai and Malaysian compounders as Indonesian and Vietnamese converters pursue backward integration. This evolution has eroded the once-robust profit margins in cross-border resin trading. Meanwhile, in a strategic move, PETRONAS' RAPID cracker is now targeting automotive and packaging contracts, previously dominated by buyers in Jakarta and Hanoi.

Infrastructure Megaproject Pipeline Fueling Construction Plastics

Major infrastructure projects across South-East Asia, such as Thailand's Land Bridge corridor, Indonesia's Nusantara capital, Malaysia's MRT3 rail, and Vietnam's North-South Expressway, are expected to drive a significant demand for pipes, insulation, and panels during the forecast period of 2026–2031. This demand, dominated by specifications of HDPE, PVC, and polyurethane, indicates a long-cycle trend. However, this reliance might expose converters to risks of schedule delays, potentially leaving their inventory stranded for up to nine months.

Government-Sponsored Petro-Chemical SEZ Corridors

Tax holidays of up to 20 years in Indonesia's Tuban zone, along with a duty-free naphtha policy at Thailand's Map Ta Phut estate, have significantly reduced capital costs, accelerating decisions regarding cracker and downstream final investment decisions (FIDs)[1]Indonesia Investment Coordinating Board, “Badan Koordinasi Penanaman Modal,” bkpm.go.id. Similarly, Malaysia's Pengerang and Vietnam's Long Son estates are introducing comparable incentives. However, this influx of incentives raises concerns about potential regional over-capacity in commodity grades by the forecast period of 2026–2031, particularly if the automotive and electronics sectors fail to meet the anticipated levels of consumption.

Data-Center Boom Driving Specialty Insulation Foams

By the forecast period 2026–2031, Southeast Asia's data-center capacity is expected to grow significantly, driven by hyperscalers establishing regional hubs in Singapore, Jakarta, and Bangkok to support latency-sensitive workloads. Each megawatt of IT load requires polyurethane and polyisocyanurate rigid foams for thermal insulation. Singapore leads in density but faces land constraints, which are pushing new developments to Johor, Malaysia. Indonesia's Batam and Cikarang zones have added capacity, while Thailand's Eastern Economic Corridor is targeting further growth. This segment provides consistent opportunities for foam replacements and retrofits.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Naphtha and ethane feedstock price volatility | -0.8% | ASEAN-wide, with acute impact in Singapore, Thailand, Malaysia (import-dependent markets) | Short term (≤2 years) |

| Chronic shortage of compounding/processing technicians for engineering plastics | -0.4% | Thailand, Malaysia, Vietnam (automotive and electronics clusters) | Medium term (2-4 years) |

| Green-premiums shrinking virgin resin competitiveness versus r-PET and r-PP | -0.3% | Philippines, Thailand, Vietnam (EPR-regulated markets) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Naphtha and Ethane Feedstock Price Volatility

Between January 2024 and September 2025, Singapore's naphtha crack spreads experienced significant growth, which increased ethylene contract prices. This development reduced converter margins, as finished-goods pricing lagged by up to ninety days. Smaller Indonesian molders, purchasing on spot terms, faced notable quarterly cost fluctuations[2]Indonesia Plastics Industry Association, “INAPLAS Survey 2025,” inaplas.org. These market dynamics highlighted the challenges faced by industry players in managing pricing volatility and maintaining profitability in a rapidly changing environment.

Chronic Shortage of Compounding/Processing Technicians

Thailand's electronics sector is expected to face a shortage of engineers. In Malaysia, automotive manufacturers are experiencing technician vacancies, which are causing delays in scaling up the polypropylene-talc and ABS-PC production lines. Meanwhile, Vietnam, part of the Asia-Pacific region, is producing fewer specialized operators annually than required. This shortage is hindering the country's ability to advance into engineering plastics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Volume Still Anchored in Commodities While Bioplastics Outperform

In 2025, traditional plastics dominated the market, accounting for 63.22% of the volume. The cost-effective use of polyethylene and polypropylene in packaging, piping, and household items largely drove this dominance. Demand for polyethylene remained robust, bolstered by the uptake of HDPE pipes in Indonesia's Nusantara relocation. Meanwhile, in both Thailand and Indonesia, the adoption of polypropylene for EV battery trays further underscored its growing significance. Engineering plastics, while yielding higher margins than their counterparts, faced constraints due to labor shortages and the influx of cheaper imports from China. Bioplastics, though holding a modest market share, showcased a promising 4.56% CAGR projected until 2031. This growth was largely attributed to a PLA facility that plays a pivotal role in supplying carton closures.

Looking ahead, the margin outlook presents a mixed picture. Commodity producers, benefiting from a domestic cost advantage post Lotte Indonesia’s cracker start-up, now grapple with tightening propane-to-naphtha discounts, putting pressure on their profit spreads. Engineering plastics, demanding ISO 9001-certified compounding lines, face a significant hurdle: only 14 percent of regional converters meet this stringent standard. While bioplastics fetch a premium price, their application remains confined to compostable foodservice ware, a niche where brands are willing to pay a premium for sustainability.

By Technology: Injection Molding Dominates, Blow Molding Gains Share

In 2025, injection molding, driven by demand from automotive interiors, appliance housings, and consumer goods, accounted for 41.96% of the total output. In a significant development, ALPLA Thailand adopted energy-efficient all-electric machines, resulting in reduced cycle times and a significant decrease in scrap rates. Meanwhile, blow molding has been on an upward trajectory, growing at a compound annual growth rate (CAGR) of 4.71% during the forecast period of 2026–2031. This growth is largely attributed to beverage manufacturers localizing PET bottles in response to extended producer responsibility (EPR) regulations. In a strategic expansion, Uniloy Malaysia announced a capacity increase in June 2025.

Extrusion demand has been closely linked to infrastructure projects, but only a small portion of regional extruders meet the PE100 pipe standards. This shortfall limits the supply of pipes for potable-water networks. While rotational, thermoforming, and compression molding processes exist, they collectively hold a smaller market share. Their limited adoption is primarily due to higher tooling costs and extended production cycles.

By Application: Packaging Retains Lead, Construction Becomes the Fastest Mover

In 2025, packaging dominated with a 38.22% volume share, encompassing everything from rigid beverage bottles and flexible snack films to personal-care containers. Indorama's Karawang recycling hub produces r-PET, which adheres to stringent FDA and EFSA food-contact regulations. Meanwhile, construction plastics, primarily HDPE pipes, PVC conduits, and polyurethane insulation, are witnessing a CAGR of 4.87% CAGR during 2026-2031, fueling major projects like Nusantara and the Land Bridge.

While the electronics and automotive sectors demand flame-retardant materials like ABS, PBT, and nylon, they grapple with technician shortages in Thailand and Malaysia, constraining their capacity. In the housewares sector, reliance on commodity resins is overshadowed by a surge in Chinese imports, which now hold a significant market share, squeezing domestic profit margins.

Geography Analysis

In 2025, Indonesia commanded a dominant 34.26% share of the South-East Asia plastics market, driven by new cracker outputs and strong demand from converters in Java and Sumatra. While domestic resin boasts a cost advantage over Middle Eastern imports, the country's low formal waste-collection rates compel r-PET producers to source feedstock from Japan and Australia.

Vietnam is experiencing the region's fastest growth, with a recorded 4.56% CAGR through 2031. This surge is fueled by substantial foreign direct investment, predominantly steering electronics and auto assembly operations to parks in Hanoi and Ho Chi Minh City.

Thailand, focusing on ABS and polycarbonate production, operates out of Map Ta Phut. Meanwhile, Malaysia’s Pengerang hub, churning out olefins and aromatics annually, grapples with a deficit in skilled compounding labor. Singapore, with an eye on the future, is steering its efforts towards renewable feedstock upgrading and research and development, rather than bulk resin production. This pivot is bolstered by significant investment in green chemicals, slated to continue through 2028. In contrast, the Philippines, Cambodia, Laos, Myanmar, and Brunei, collectively holding a small share, find themselves importing commodity resins but capitalizing on their low-cost molding capabilities.

Competitive Landscape

The South-East Asia plastics market is moderately fragmented. Strategic focuses are shifting toward feedstock adaptability, local sourcing, and sustainability. SCG's significant investment in retrofitting its Map Ta Phut cracker for ethane aims to mitigate risks associated with naphtha price fluctuations. Promising avenues include engineering-plastics compounding for electric vehicle (EV) battery enclosures, establishing chemical recycling frameworks in the Philippines and Vietnam, and crafting specialty foams compliant with UL 94 V-0 and R-6.0 standards for data-center HVAC systems.

South-East Asia (SEA) Plastics Industry Leaders

SCG Chemicals PCL

PT Chandra Asri Petrochemical Tbk

PETRONAS Chemicals Group Berhad

LOTTE Chemical Titan

Indorama Ventures

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: South Korea’s Dongsung launched a new 81,000 m² polyurethane (PU) production facility in Karawang, Indonesia, marking a major expansion of its global manufacturing footprint. With an annual capacity of 67,000 tons and projected revenue of USD 150 million, the plant will supply PU-based materials to markets across Southeast Asia, the Americas, and Europe.

- March 2024: An Phat Holdings announced a partnership with South Korea’s SKC Group to establish a biodegradable PBAT (Polybutylene Adipate Terephthalate) production facility in Hai Phong, Vietnam. The plant, with an annual capacity of 70,000 tons, is expected to begin operations in Q3 2025.

South-East Asia (SEA) Plastics Market Report Scope

Plastic is a synthetic material made from a wide range of organic polymers, such as polyethylene, PVC, nylon, etc., that can be molded into shape while soft and then set into a rigid or slightly elastic form.

The plastics market is segmented by type, technology, application, and geography. By type, the market is segmented into traditional plastics, engineering plastics, and bioplastics. By technology, the market is segmented into injection molding, blow molding, extrusion, and other technologies. By application, the market is segmented into packaging, electrical and electronics, building and construction, automotive and transportation, housewares, furniture and bedding, and other applications. The report also covers the market size and forecasts for the market in 6 countries across the region. For each segment, the market sizing and forecasts have been done based on volume (Tons).

By Type

| Traditional Plastics |

| Engineering Plastics |

| Bioplastics |

By Technology

| Injection Molding |

| Blow Molding |

| Extrusion |

| Other Technologies |

By Application

| Packaging |

| Electrical and Electronics |

| Building and Construction |

| Automotive and Transportation |

| Housewares |

| Furniture and Bedding |

| Other Applications |

By Geography

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Philippines |

| Singapore |

| Rest of South-East Asia |

| By Type | Traditional Plastics |

| Engineering Plastics | |

| Bioplastics | |

| By Technology | Injection Molding |

| Blow Molding | |

| Extrusion | |

| Other Technologies | |

| By Application | Packaging |

| Electrical and Electronics | |

| Building and Construction | |

| Automotive and Transportation | |

| Housewares | |

| Furniture and Bedding | |

| Other Applications | |

| By Geography | Indonesia |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Philippines | |

| Singapore | |

| Rest of South-East Asia |

Key Questions Answered in the Report

What is the forecast volume for plastics consumption in South-East Asia by 2031?

The South-East Asia Plastics Market size was valued at 31.78 million tons in 2025 and is estimated to grow from 33.09 million tons in 2026 to reach 40.49 million tons by 2031, at a CAGR of 4.12% during the forecast period (2026-2031).

Which country shows the fastest growth in resin demand through 2031?

Vietnam leads with a projected 4.56% CAGR driven by electronics and automotive investments.

How large is the packaging segment compared with construction plastics?

Packaging held a 38.22% share in 2025, while construction is the fastest-growing segment at a 4.87% CAGR to 2031.

Why are converters shifting toward engineering and bio-based resins?

Margin compression on commodity grades from narrower propane-to-naphtha spreads and a regulatory push for sustainable materials encourages the adoption of higher-value resins.

Page last updated on: