Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

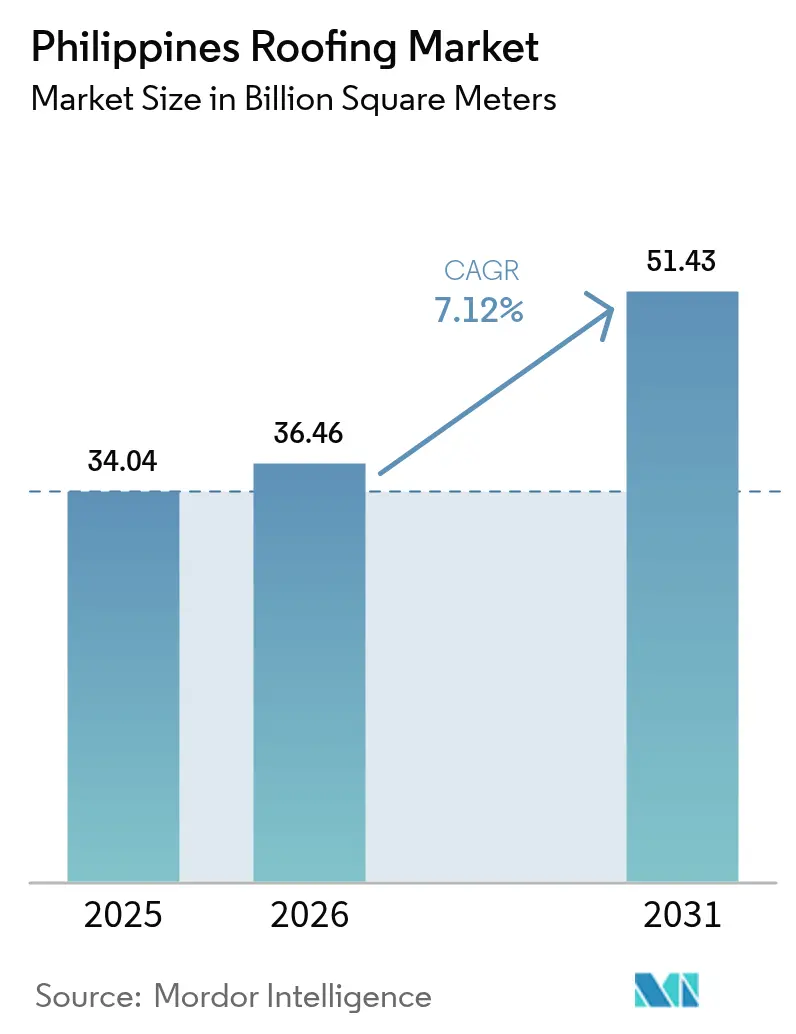

| Base Year Market Size (2025) | 34.04 Billion square meters |

| Market Volume (2026) | 36.46 Billion square meters |

| Market Volume (2031) | 51.43 Billion square meters |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

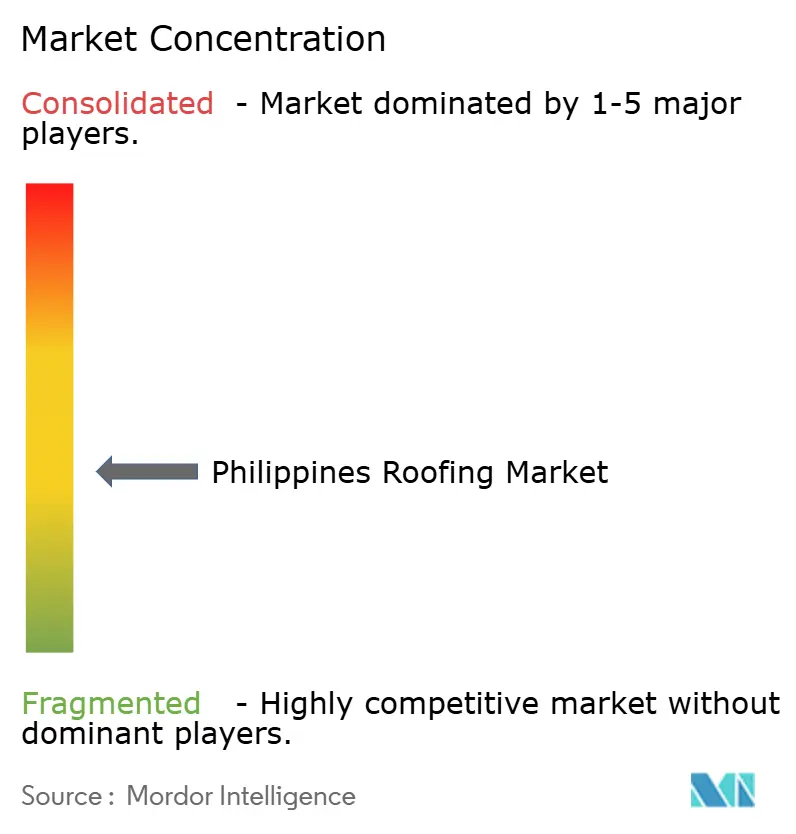

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Roofing Market Analysis by Mordor Intelligence

Philippines Roofing market size in 2026 is estimated at 36.46 billion square meters, growing from 2025 value of 34.04 billion square meters with 2031 projections showing 51.43 billion square meters, growing at 7.12% CAGR over 2026-2031. Growth is underpinned by the Build Better More public works pipeline, resilient overseas Filipino worker (OFW) remittance inflows, and stricter rules that demand typhoon-ready building envelopes. Metal panels dominate because they satisfy the National Structural Code’s wind-load test and act as a ready substrate for rooftop solar, aligning with the Department of Energy’s goal of photovoltaic capacity by 2030. Pag-IBIG’s subsidized mortgage rate and the 4PH housing program’s one-million-units-per-year pledge funnel demand toward cost-effective pre-painted galvanized steel, while regional reconstruction after Super Typhoon Pepito keeps replacement activity elevated. Raw-material price swings and a shortage of TESDA-certified installers temper margins but have not derailed expansion, as local steel mills and global brands race to launch solar-ready, cool-roof products that fetch healthy premiums.

Key Report Takeaways

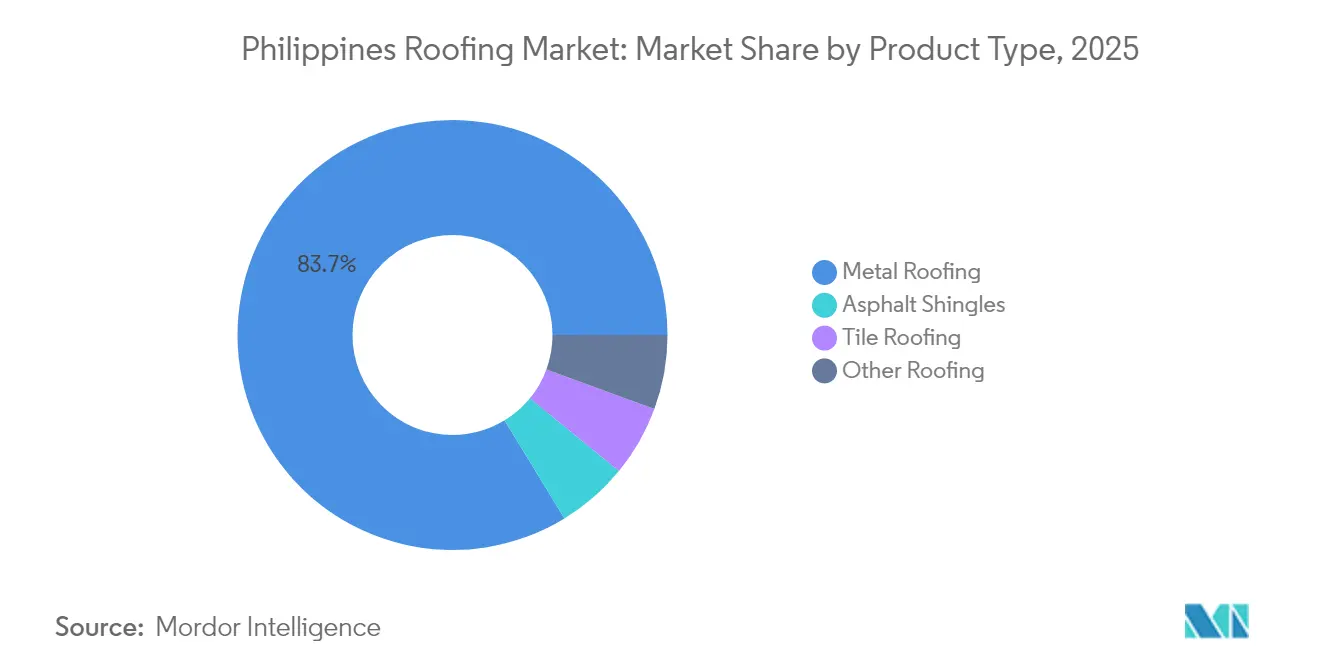

- By product type, metal roofing led with 83.72% of the Philippines' roofing market share in 2025 and is forecasted to grow at a 7.55% CAGR through 2031.

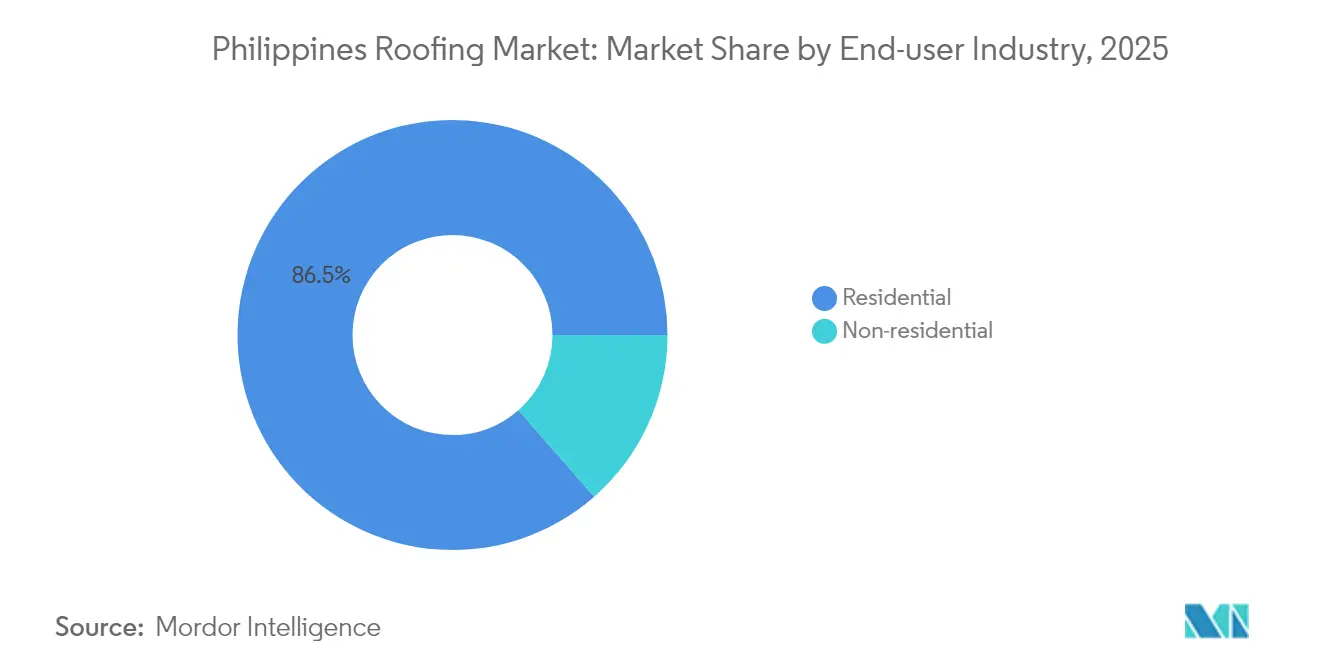

- By end-user industry, the residential segment accounted for 86.45% of the Philippines' roofing market size in 2025 and is projected to expand at a 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Roofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Build Better More infrastructure surge | +1.8% | National, especially Metro Manila, Calabarzon, Central Visayas | Medium term (2-4 years) |

| OFW-funded residential boom | +2.1% | Ilocos, Bicol, Western Visayas | Long term (≥4 years) |

| Green and energy-efficient code momentum | +0.9% | Metro Manila, Cebu City, Davao City | Long term (≥4 years) |

| National push for typhoon-resilient envelopes | +1.5% | Coastal provinces, Eastern Visayas, Bicol | Short term (≤2 years) |

| Emergence of solar-ready metal roofs | +1.2% | Luzon and Visayas grids | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Build Better More Infrastructure Pipeline

The Build Better More plan features flagship projects, including those that specify new roofing for public markets, evacuation centers, and transport hubs. Pre-engineered metal roofs with long-term warranties have become the default option in these tenders, securing significant annual demand throughout the forecast period. National procurement rules now privilege systems with superior wind-uplift ratings, nudging local governments in key regions to copy the federal template. A 2025 budget of PHP 1.507 trillion preserves infrastructure outlays at 5.2% of GDP, smoothing the project pipeline despite fiscal tightening[1]Department of Budget and Management, “National Budget 2025 Infrastructure Allocations,” dbm.gov.ph. This accelerated timetable shortens the public-building replacement cycle in high-traffic facilities, helping sustain the Philippines' roofing market beyond the current construction surge.

Residential Construction Boom Driven by OFW Remittances

OFW remittances increased in 2024, demonstrating growth compared to the previous year and making a significant contribution to GDP. Surveys indicate a notable portion of this income is allocated to homebuilding, resulting in substantial spending on roofs and envelopes. Pag-IBIG’s subsidy lowers effective interest rates on mortgages, encouraging buyers to opt for specific metal brackets. Provinces with large migrant-worker communities, such as Pangasinan and Iloilo, experienced significant growth in residential permits in 2024, surpassing the national average. Since remittances are influenced by global labor demand rather than local economic cycles, this cash flow provides the Philippines' roofing market with a dependable long-term advantage.

Momentum Toward Green and Energy-Efficient Building Codes

The Philippine Green Building Code requires new commercial structures to reduce energy use, a threshold that has been further tightened in DOE Circular DC2024-08-0024. BERDE certifications have increased as developers have pursued cool roofs that reflect more solar heat and trim air conditioning loads. Government offices now mandate reflective metal surfaces on all new buildings, pushing private contractors to standardize on similar materials to streamline procurement. Although cool-roof coatings cost more than standard finishes, paybacks appeal to asset owners with long hold periods. Fast-track permit incentives in Metro Manila for projects that beat efficiency baselines further enlarge this premium niche.

National Push for Typhoon-Resilient Building Envelopes

Typhoon Kristine and Super Typhoon Pepito caused significant infrastructure damage and destroyed numerous homes in late 2024. Post-event audits showed fewer failures on houses clad with pre-painted galvanized steel that meets NSCP 2015 wind-load standards. Municipal engineers in coastal provinces now informally require metal roofs for new permits, further constricting asphalt and tile demand. Insurance carriers respond with premium discounts for certified typhoon-resistant designs, translating safety into a financial benefit. Build Better More also devotes resources to disaster-risk-reduction projects through 2028, many of which involve reroofing public buildings in high-risk zones.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | −1.3% | Nationwide, highest in import-heavy areas | Short term (≤2 years) |

| High upfront cost of premium systems | −0.8% | Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Shortage of certified installers | −0.6% | Regions I, II, V, VIII | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Galvanized-steel prices rose in 2024 as China limited exports and freight rates climbed. With imports covering a significant portion of domestic steel use, currency shifts and trade policies immediately pass through to roof quoting. Bitumen cost spikes squeezed asphalt-shingle margins, prompting manufacturers to curtail promotions in the retrofit channel. Local mills meet only a portion of steel demand, so contractors now shorten price-validity windows, complicating project budgeting. A lack of hedging tools in the Philippine futures market amplifies volatility, discouraging developers from stockpiling ahead of builds. Although backward-integrated players such as Philsteel cushion shocks, the broader Philippines roofing market remains sensitive to global raw-material cycles.

High Upfront Cost of Premium Roofing Systems

Cool-roof, solar-ready panels sell at a premium compared to standard galvanized steel. Energy savings and lower upkeep costs offset this premium over time, yet buyers with limited income struggle to finance the extra outlay. Construction loans often leave little room for upgrades once land and structural costs are paid. Commercial owners with long-term leases accept the payback period, but speculative builders favor cheaper roofs to speed cash recovery. A shortage of green-finance products, such as energy-efficiency mortgages, further slows premium uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Metal Roofing Locks in Solar-Ready Premium

Metal panels accounted for 83.72% of the Philippines Roofing Market share in 2025 and are expected to grow at a rate of 7.55% through 2031, outpacing the overall market. Pre-painted galvanized steel is widely used due to its low weight, compliance with wind codes, and cost-effectiveness, making it the primary choice. Within the metal industry, solar-ready variants are scaling rapidly as installers pair mounting rails with the net-metering boom. Premium coatings are also gaining traction, particularly in coastal zones where corrosion resistance is a priority.

Tile roofs maintain a presence in heritage districts and luxury estates, where aesthetics are prioritized over cost and structural load. However, their heavier weight limits their use in typhoon-prone areas. Asphalt shingles are used in retrofit jobs for older Metro Manila subdivisions where rafters cannot support heavier tiles. Rising bitumen costs and informal coastal bans after severe typhoons are impacting this segment. Other materials, such as bituminous sheets, polycarbonate, and nipa thatch, are used for temporary structures and farms, but their share is declining as public housing increasingly adopts metal roofing.

By End-User Industry: Residential Anchors Volume, Non-Residential Captures Value

The residential channel accounted for 86.45% of the Philippines Roofing Market size in 2025 and is projected to grow at 7.18% from 2025 to 2031, driven by overseas remittances and government housing targets. Single-family homes outside Metro Manila predominantly choose budget aluminum-zinc panels that strike a balance between affordability and typhoon safety. Condominium and townhouse developers in major cities are increasingly adopting cool-roof metal to meet green building standards, driving growth in this premium segment. Government housing projects are also contributing to consistent demand for metal panels.

Non-residential work, while holding a smaller share of volume, contributes a larger share of revenue due to the preference for thicker gauges, cool coatings, and longer warranties in malls, warehouses, and municipal buildings. Infrastructure projects are creating significant demand for roofing materials. Incentives for solar-ready metal roofs are encouraging commercial owners to adopt energy-efficient options, reducing long-term energy costs. Although its growth rate is slightly lower than that of residential work, the higher margins in non-residential work make it a strategic focus for producers.

Geography Analysis

Metro Manila generated significant volume thanks to condominium towers, office build-outs, and civic projects tethered to Build Better More. High-rise sites specify cool-roof, solar-ready metal, whereas older districts still re-cover homes with asphalt shingles when rafter loads are restrictive. Net-metering approvals in the capital reinforced premium demand. Yet land scarcity means fewer square meters of roof per dwelling, capping Metro Manila’s expansion below the national pace.

Calabarzon and Central Visayas jointly represent a substantial portion of the Philippines' roofing market, propelled by OFW-funded self-builds and 4PH sites. Cavite, Laguna, and Cebu accounted for the bulk of the rise in residential permits, largely for single-story homes that standardize on galvanized sheets. Industrial parks surrounding Batangas ports and Mactan Airport also adopt pre-engineered metal roofs with long-term warranties, lifting the average revenue per square meter above the residential norm.

Bicol and Eastern Visayas contribute to the volume but lead growth, underwritten by reconstruction funds after Super Typhoon Pepito. Local permit offices now require metal panels for new builds, accelerating the displacement of tile and asphalt. The rest of Luzon and Mindanao, including Ilocos, Cagayan Valley, Western Visayas, Northern Mindanao, and SOCCSKSARGEN, account for a significant portion of demand. These areas rely on agriculture and remittance income, sustaining a steady flow of single-family projects that keep metal penetration high. Regional variations, therefore, reflect funding sources and disaster exposure, not fundamental material preferences, reinforcing metal’s nationwide supremacy in the Philippines' roofing market.

Competitive Landscape

The Philippines Roofing Market is moderately fragmented. Foreign specialists target niche markets instead of broad volumes. Digitization remains sparse. Very few projects use building information modeling to optimize panel cuts, and modular fabrication is even rarer. Early adopters report waste reduction and faster installation, suggesting process innovation could join product features as a differentiation lever. Given the volatility of raw materials and labor shortages, incumbents that control both steel conversion and field execution appear best positioned to increase their share of the Philippines' roofing market over the next five years.

Philippines Roofing Industry Leaders

Colorsteel Systems Corporation

DN Steel

Union Galvasteel Corporation

Philsteel Holdings Corporation

Jacinto Color Steel Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: GAF Materials LLC introduced eight reflective-roof designs and recycled-content membranes at the International Roofing Expo. GAF's suppliers in the region may benefit from new product offerings.

- February 2025: Owens Corning announced a shingle plant with an annual capacity of 6 million square meters, targeting a 2027 start-up. With the start of the new shingle plant, the company will be able to cater to demand for roofing materials in the Philippines.

Philippines Roofing Market Report Scope

The roofing market encompasses the supply, installation, maintenance, and repair of protective coverings for buildings and structures. Spanning a diverse array of products, from asphalt shingles to metal tiles, it caters to residential, commercial, and industrial construction sectors alike.

The Philippines Roofing Market is segmented by product type and end-user industry. By product type, the market is segmented into asphalt shingles, tile roofing, metal roofing, and other roofing. By end-user industry, the market is segmented into residential and non-residential. For each segment, market sizing and forecasts have been conducted based on volume (square meters).

By Product Type

| Asphalt Shingles |

| Tile Roofing |

| Metal Roofing |

| Other Roofing |

By End-user Industry

| Residential |

| Non-residential |

| By Product Type | Asphalt Shingles |

| Tile Roofing | |

| Metal Roofing | |

| Other Roofing | |

| By End-user Industry | Residential |

| Non-residential |

Key Questions Answered in the Report

What is the current size of the Philippines roofing market?

The Philippines roofing market size is projected to be 36.46 billion square meters in 2026 and is expected to reach 51.43 billion square meters by 2031.

Which material dominates Philippine roofing demand?

Metal panels account for 83.72% of the 2025 volume, as they meet typhoon wind codes and integrate easily with rooftop solar systems.

Why are OFW remittances important to roofing suppliers?

Remittances contribute billions of dollars to annual homebuilding expenditures, supporting steady 7.18% growth in residential roofing volume.

Which region is the fastest-growing roofing market?

Bicol and Eastern Visayas lead with reconstruction funds, accelerating rebuilding.

Page last updated on: